Market Overview

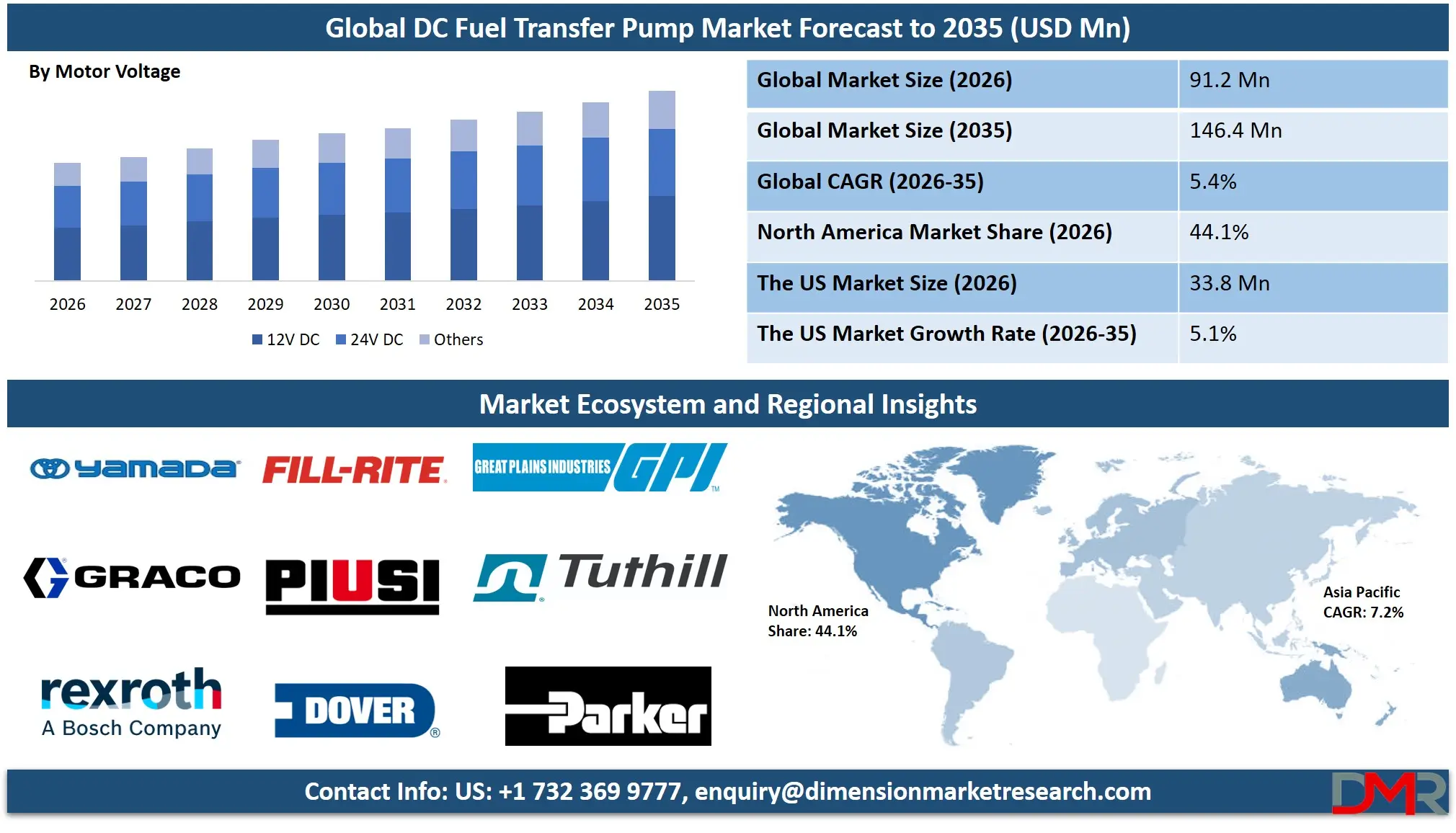

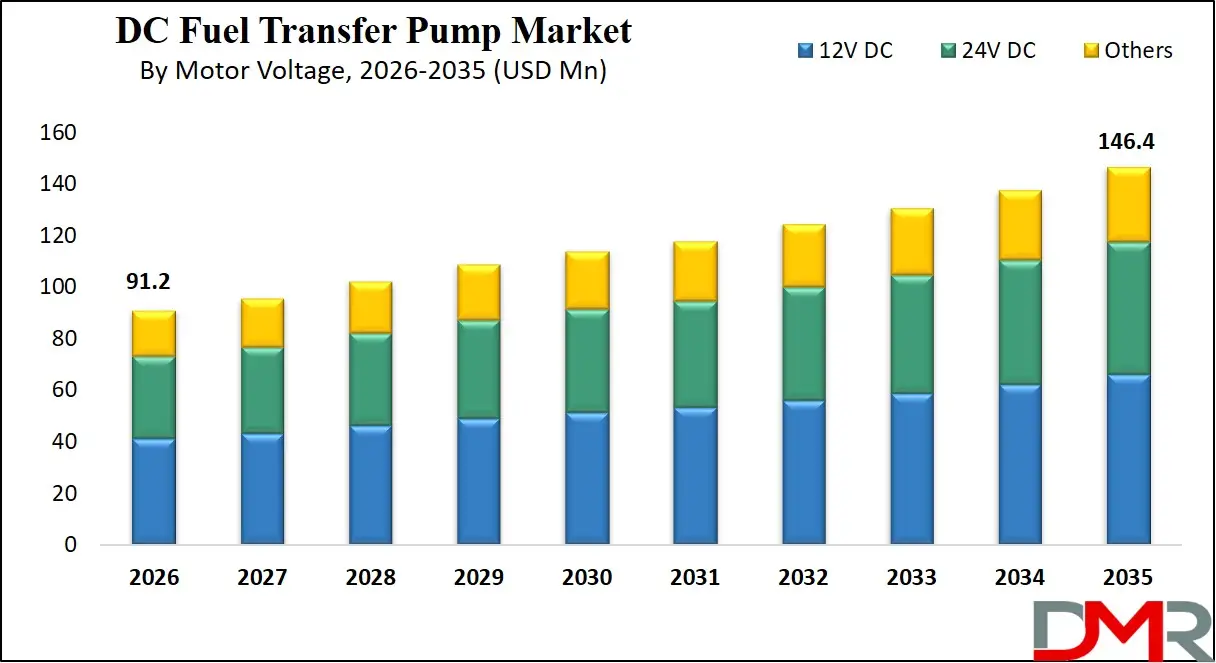

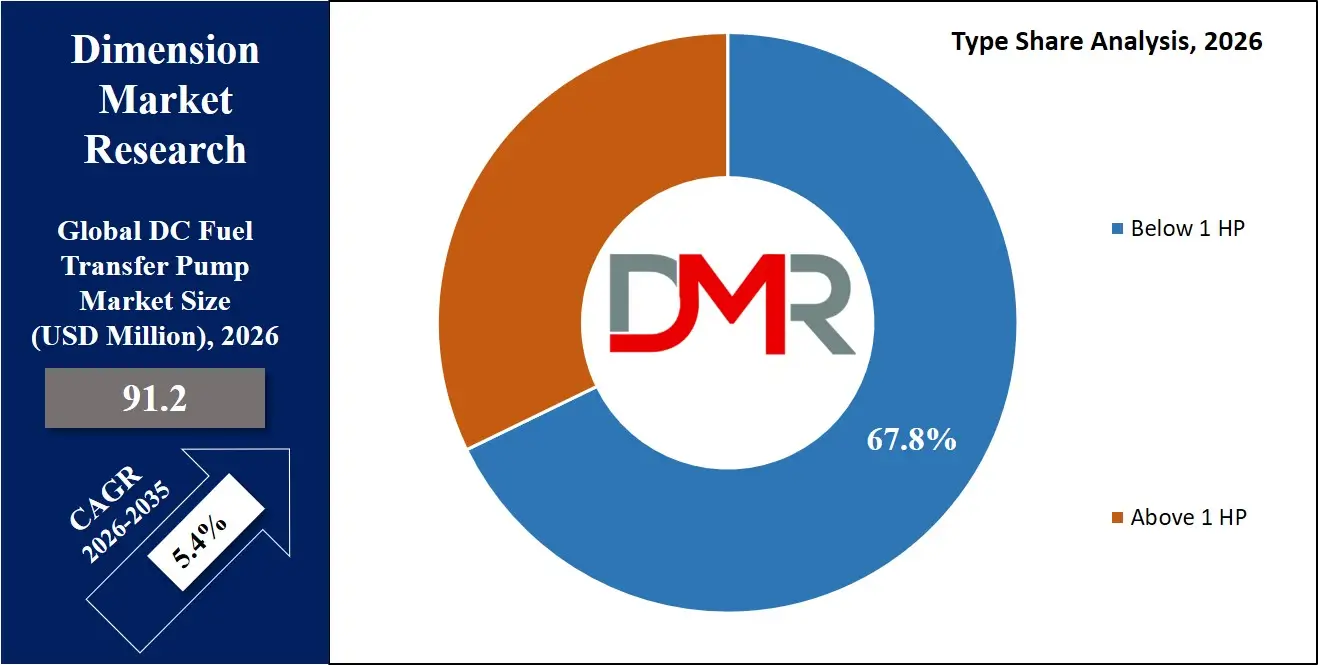

The Global DC Fuel Transfer Pump Market is projected to reach USD 91.2 million in 2026 and grow at a compound annual growth rate of 5.4% from there until 2035 to reach a value of USD 146.4 million.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

This growth reflects increasing demand for decentralized fuel management solutions, rising adoption of off-road vehicles and machinery, expanding applications in mining and military operations, and greater deployment of reliable DC-powered pumping systems across construction sites, agricultural fields, and remote industrial locations. The market expansion is further supported by advancements in brushless DC (BLDC) motor technology, IoT-enabled fuel monitoring, and durable, corrosion-resistant pump materials, along with strengthening global demand for efficient fuel logistics in developing economies.

DC fuel transfer pumps enable rapid, safe, and accurate fuel dispensing in environments where AC power is unavailable or impractical. Through robust DC motor designs, seamless 12V and 24V integration with vehicle electrical systems, and innovative portable configurations, these solutions address critical operational gaps related to refueling efficiency, equipment uptime, and mobile energy security across diverse industries.

Technological advancements, including BLDC pumps with enhanced energy efficiency, integrated flow meters and digital displays, thermal overload protection, smart connectivity for fleet fuel tracking, and compact, lightweight portable units, are transforming the market into a scalable and highly adaptable ecosystem. Integration of advanced filtration systems, anti-spark components for hazardous environments, and multi-fuel compatibility is reshaping operational capabilities in both surface and underground applications.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Growing government and private sector investments in infrastructure development, mining exploration, and defense logistics further accelerate global adoption. However, barriers such as volatility in raw material prices, lack of standardized fuel quality in developing regions, product maintenance challenges in harsh environments, and regulatory variability for hazardous-duty equipment remain. Despite these limitations, the convergence of portable power technology, industrial mobility, and remote asset management positions DC fuel transfer pumps as a cornerstone of global fuel logistics and equipment support through 2035.

The US DC Fuel Transfer Pump Market

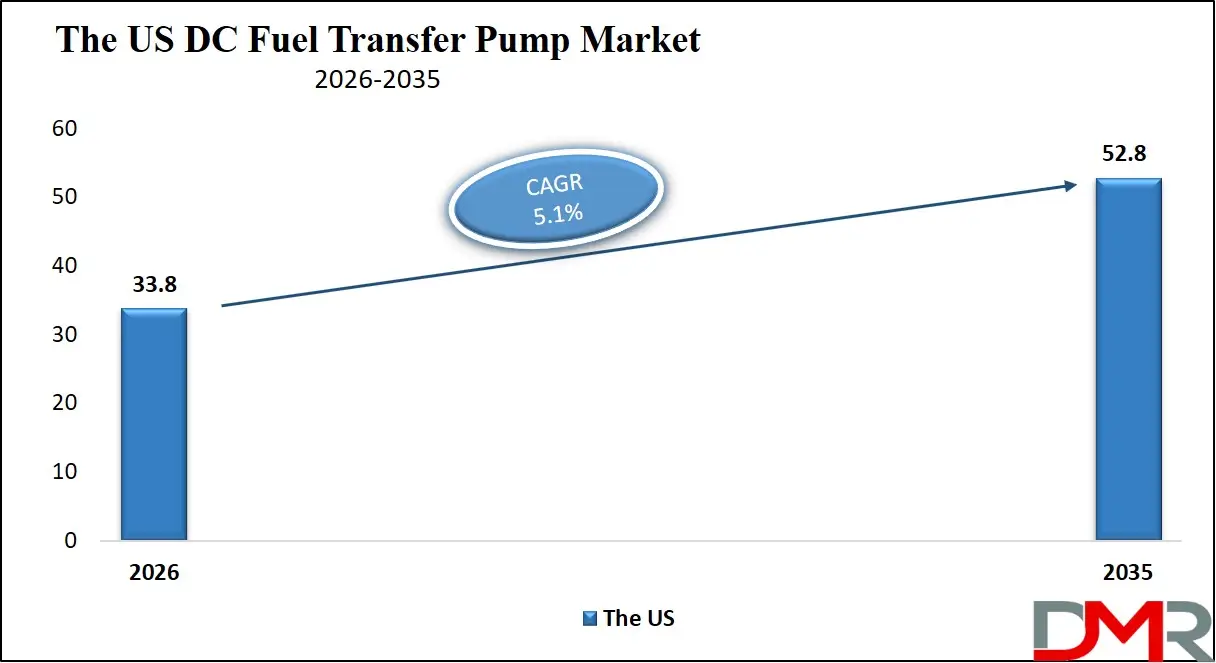

The US DC Fuel Transfer Pump Market is projected to reach USD 33.8 million in 2026 at a compound annual growth rate of 5.1%, reaching USD 52.8 million by 2035. The U.S. leads global adoption due to its mature off-road vehicle ecosystem, robust agricultural and construction sectors, high rates of recreational vehicle (RV) and boating activity, and strong emphasis on operational efficiency in fuel handling.

The national expansion of decentralized fueling solutions on farms, large construction sites, and remote job sites, coupled with growing institutional demand from mining operators and military logistics units, fuels sustained market growth. Major manufacturers such as Fill-Rite, GPI, and Piusi are scaling production and innovating next-generation pump designs optimized for higher flow rates, enhanced durability, and smart monitoring capabilities.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

U.S. federal support through Department of Defense logistics contracts, Bureau of Land Management permits for remote operations, and state-level agricultural modernization grants encourages institutional procurement. Partnerships between pump manufacturers and major original equipment manufacturers (OEMs) for integrated tank systems continue to advance product accessibility and performance standards.

The rapid rise of BLDC pumps with extended motor life, integration with telematics for real-time fuel consumption tracking, and development of compact 12V units for light-duty vehicles and agricultural machinery continues to redefine the U.S. fuel transfer landscape, positioning the country as the global benchmark for DC pumping efficiency and reliability.

The Europe DC Fuel Transfer Pump Market

The Europe DC Fuel Transfer Pump Market is estimated to be valued at USD 28.8 million in 2026 and is further anticipated to reach USD 52.5 million by 2035 at a CAGR of 5.8%, over the forecasted period. Europe's leadership is anchored by strengthening agricultural mechanization, increasing investments in mining exploration within regions like Scandinavia, and harmonized ATEX/IECEx safety regulations for explosive environments across member states.

Countries such as Germany, France, the U.K., Italy, and Sweden are widely adopting DC-powered fuel transfer solutions, driven by elevated equipment mobility requirements, renewable energy integration in remote pumping stations, and EU initiatives like Horizon Europe funding for clean energy and efficient fuel logistics. The U.K.'s construction equipment modernization and Germany's agricultural technology upgrades are particularly active in deploying advanced DC pumps in off-grid locations.

Europe's aging farming workforce demanding easier-to-use equipment, need for precision fuel management, and emphasis on low-emission, energy-efficient motors further drive adoption. Funding through national agricultural subsidies and EU rural development programs supports R&D in BLDC technology, compact portable pumps, and multi-fuel compatible systems.

Operational upgrades on French construction mega sites, German farm cooperatives, and Italian marine ports increasingly deploy fixed DC pump installations with integrated flow monitoring, portable battery-powered units, and corrosion-resistant pumps for coastal applications. With robust safety frameworks, integration into equipment fleet management, and emphasis on operational uptime, Europe remains one of the most advanced regions in DC fuel transfer pump penetration.

The Japan DC Fuel Transfer Pump Market

The Japan DC Fuel Transfer Pump Market is projected to be valued at USD 7.2 million in 2026. It is further expected to witness subsequent growth in the upcoming period, holding USD 13.2 million in 2035 at a CAGR of 6.8%, during the forecast period. Japan's high reliance on imported fuels, concentration of construction and disaster recovery operations, and technologically sophisticated agricultural sector drives strong demand for reliable, efficient DC-powered fuel transfer equipment in both public and private infrastructure projects.

The Ministry of Land, Infrastructure, Transport and Tourism (MLIT) actively supports equipment modernization through national infrastructure resilience planning, prefectural construction project guidelines, and integration into disaster response stockpiles. Japan's leadership in compact, lightweight machinery design and high-efficiency motor technology accelerates innovation in ultra-portable DC pumps suitable for small construction firms, rural agricultural cooperatives, and emergency response vehicles.

Japan's concept of "Smart Agriculture" and "i-Construction", supported by municipal governments and industry associations, integrates DC fuel transfer pumps into next-generation farming and civil engineering operations. Compact pumps are being deployed in Tokyo metropolitan construction sites, Hokkaido farming collectives, and regional disaster recovery bases. Japan's cultural emphasis on precision, reliability, and meticulous equipment maintenance, combined with demographic pressure to boost productivity, positions the country as a high-growth innovator in efficient DC fuel transfer.

Global DC Fuel Transfer Pump Market: Key Takeaways

- Strong Global Market Growth Outlook: The Global DC Fuel Transfer Pump Market is expected to be valued at USD 91.2 million in 2026 and is projected to reach USD 146.4 million by 2035, showcasing rapid expansion supported by rising off-grid fuel demand and operational efficiency awareness.

- High CAGR Driven by Technology Migration: The market is expected to grow at an impressive CAGR of 5.4% from 2026 to 2035, fueled by accelerating adoption in construction and mining, agricultural mechanization in developing regions, military fleet modernization, and increasing frequency of disaster relief operations requiring mobile fueling worldwide.

- Strong Growth Trajectory in the United States: The U.S. DC Fuel Transfer Pump Market stands at USD 33.8 million in 2026 and is projected to reach USD 52.8 million by 2035, expanding at a CAGR of 5.1% due to robust agricultural and construction sectors, strong recreational vehicle penetration, and continuous product innovation.

- North America Maintains Regional Dominance: North America is expected to capture approximately 44.1% of the global market share in 2026, supported by mature off-road vehicle infrastructure, significant private sector investment in equipment efficiency, and early adoption of smart, connected fuel transfer technologies.

- Rapid Advancement in Pump Technologies: Innovations including brushless DC (BLDC) motors for extended life, integrated digital flow meters and totalizers, IoT-enabled fuel management connectivity, and lightweight, corrosion-resistant pump materials are significantly accelerating operational efficiency and equipment uptime.

- Growing Mobile Fuel Demand Boosts Adoption: Rising global equipment density in remote mining, large-scale infrastructure projects, military forward operating bases, and agricultural operations, coupled with widening gaps in fixed fueling infrastructure, is driving sustained demand for reliable, DC-powered mobile fuel transfer solutions.

Global DC Fuel Transfer Pump Market: Use Cases

- Mining Operations: Heavy-duty 24V DC pumps transfer diesel from storage tanks to haul trucks and excavators in remote pit locations, ensuring continuous operation without the need for AC power infrastructure.

- Military Field Logistics: Compact, ruggedized 12V and 24V pumps are deployed in forward operating bases to refuel tactical vehicles, generators, and aircraft from bladders or tankers under austere conditions.

- Agricultural Equipment Servicing: Portable 12V DC pumps enable farmers to refuel tractors and harvesters directly in fields from nurse tanks, maximizing productive time during critical planting and harvesting seasons.

- Construction Site Fueling: Fixed-mount DC pumps integrated with double-walled tanks provide on-site refueling for bulldozers, cranes, and generators, eliminating downtime from traveling to off-site fuel stations.

- Fleet Maintenance & Workshops: Service trucks equipped with battery-powered DC pumps perform emergency refueling and fluid transfer for stranded commercial vehicles, reducing roadside delays.

Global DC Fuel Transfer Pump Market: Stats & Facts

- U.S. Energy Information Administration (EIA): In 2023, the U.S. consumed over 135 billion gallons of diesel fuel, a significant portion used by the construction, agricultural, and mining sectors. Off-road diesel use accounts for roughly 8-10% of total U.S. distillate fuel consumption.

- U.S. Bureau of Labor Statistics: The construction sector employs over 7.5 million people in the U.S., with equipment density requiring extensive on-site fueling. There are approximately 2 million farms operating across the U.S., many relying on mobile fueling solutions.

- International Energy Agency (IEA): Global energy demand for transport, including off-road sectors, is projected to grow by 25% by 2035. Industry and agriculture account for nearly 30% of global final energy consumption.

- World Bank: Mining activities contribute over USD 1.8 trillion to global GDP, driving demand for remote fuel logistics.

- U.S. Department of Defense (DoD): The U.S. military is the single largest consumer of fuel in the world, with massive logistics requirements for tactical refueling equipment.

- National Mining Association: The U.S. mining industry produces over USD 90 billion in minerals and materials annually, requiring substantial fuel inputs.

- U.S. Department of Agriculture (USDA): Farm production expenditures on fuel and oils exceeded USD 15 billion annually in recent years.

- Global Construction Perspectives: Global construction output is expected to grow by 35% by 2030, driven by infrastructure investment in Asia, Africa, and the Middle East.

- Fleet Owner Survey Data: Over 60% of large fleets report using on-site or mobile fueling to improve efficiency and reduce vehicle downtime.

- Off-Highway Research: Global sales of construction equipment exceeded 1.1 million units annually, each requiring regular refueling.

Global DC Fuel Transfer Pump Market: Market Dynamic

Driving Factors in the Global DC Fuel Transfer Pump Market

Growth of Off-Road Mobile Equipment

The global fleet of off-road mobile machinery, including excavators, tractors, mining haul trucks, and generators, continues to expand rapidly, particularly in developing economies. This equipment operates predominantly in areas without reliable grid power, making DC-powered fuel transfer pumps essential for refueling operations. The shift toward larger, more fuel-intensive machinery further amplifies the need for high-flow, durable DC pumps capable of handling frequent, high-volume transfers, driving significant market demand.

Technology Innovation and Energy Efficiency

DC fuel transfer pump innovation has shifted decisively toward energy efficiency and operational intelligence. Advancements in BLDC motor technology, integrated digital metering for precise fuel management, and smart pumps with telematics connectivity lower operational costs and enable predictive maintenance. The development of pumps with higher voltage tolerances, enhanced filtration systems, and intrinsically safe components for explosive environments expands application scope. The convergence of motor design engineering, digital instrumentation, and industrial IoT makes DC fuel transfer more efficient and controllable than ever before.

Restraints in the Global DC Fuel Transfer Pump Market

Raw Material Price Volatility and Supply Chain Disruptions

The production of DC fuel transfer pumps relies on commodities such as copper for motors, aluminum for housings, and various electronic components. Global price fluctuations and supply chain bottlenecks, as witnessed in recent years, directly impact manufacturing costs and lead times. This volatility creates pricing uncertainty for manufacturers and end-users, potentially delaying large-scale procurement projects, particularly for budget-sensitive applications in agriculture and small construction.

Maintenance Challenges in Harsh Environments

DC pumps are frequently deployed in extreme conditions, dusty mines, muddy construction sites, and corrosive marine environments. Despite ruggedization efforts, exposure to contaminants, weather, and continuous duty cycles can lead to premature wear, seal failures, and motor burnout. Limited access to specialized repair services in remote locations compounds downtime, creating a critical gap between equipment reliability expectations and actual field performance, especially for operations lacking dedicated maintenance personnel.

Opportunities in the Global DC Fuel Transfer Pump Market

Expansion into Emerging Economy Infrastructure Projects

Rapidly industrializing regions across Africa, Southeast Asia, and Latin America represent major growth frontiers as governments and private developers launch massive infrastructure, mining, and agricultural projects. Partnerships with equipment dealers, construction firms, and development finance institutions can accelerate pump distribution alongside heavy machinery sales. Localized manufacturing and cost-optimized pump variants tailored to regional voltage standards, fuel types, and purchasing power constraints can unlock massive volume-driven expansion.

Smart Pump Ecosystems and Predictive Analytics

Integration of IoT sensors, GPS tracking, and cloud-based fleet management platforms creates recurring revenue opportunities through telematics subscriptions and predictive analytics for pump maintenance optimization. Data generated from pump utilization patterns can inform fuel logistics planning, theft prevention, and operational efficiency benchmarking. This transforms DC fuel transfer pumps from simple mechanical devices into intelligent nodes within broader industrial asset management networks.

Trends in the Global DC Fuel Transfer Pump Market

Adoption of Brushless DC (BLDC) Motors

BLDC technology is rapidly migrating from specialized applications into mainstream DC fuel transfer pumps. Offering higher efficiency, longer operational life, reduced electromagnetic interference, and quieter operation compared to brushed motors, BLDC pumps are increasingly specified in applications demanding reliability and low maintenance, such as military, aerospace, and premium agricultural equipment. This trend elevates performance standards across the market.

Customization and Application-Specific Pump Design

Market segmentation is deepening with pumps specifically engineered for mining (explosion-proof), marine (corrosion-resistant), and cold-weather (heated components) environments. Application-specific flow rates, material selection, mounting configurations, and certification compliance improve safety and operational suitability. This trend reflects maturation beyond general-purpose designs toward precision-engineered solutions for distinct industrial challenges.

Global DC Fuel Transfer Pump Market: Research Scope and Analysis

By Type Analysis

Above 1 HP Pumps are projected to dominate the Type segment of the Global DC Fuel Transfer Pump Market. This dominance is driven by the growing demand for high-flow transfer rates in heavy-duty applications, including large mining equipment fueling, bulk fuel movement at construction camps, and military forward operating base logistics. Data from large-scale infrastructure projects demonstrating significant time savings with higher horsepower pumps has accelerated adoption across mining, industrial, and large-agriculture sectors. These pumps, while priced at a premium, are increasingly specified in institutional procurement tenders and large-fleet purchases where throughput and duty cycle capability outweigh unit cost considerations.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

While Below 1 HP Pumps represent the historical backbone of light-duty and portable applications and remain widely distributed, their relative share is moderating as larger-scale operations and integrated systems demand higher capacity. However, Below 1 HP units maintain a crucial role in small farms, workshops, and for individual vehicle owners, offering affordability and 12V compatibility. Their volume remains substantial, but the higher unit value and system integration of Above 1 HP pumps secure their leading revenue position throughout the forecast period.

By Motor Voltage Analysis

24V DC Pumps are projected to dominate the global market, fundamentally transforming heavy-duty and industrial refueling operations. Their dominance stems from an unparalleled value proposition for high-demand environments such as mining, large-scale construction, military logistics, and industrial machinery fueling. By enabling higher motor power and faster flow rates without excessive current draw, 24V systems reduce refueling time and improve operational efficiency for heavy equipment. The driving forces behind their market leadership are tri-fold: the widespread adoption of 24V electrical systems in heavy-duty vehicles and machinery, growing demand for rapid fueling in time-sensitive operations, and the declining cost premium of robust 24V motors and controllers. As mining and infrastructure projects prioritize throughput, the economic case for higher-voltage, higher-performance pumps becomes compelling, solidifying these systems as the cornerstone of industrial DC fuel transfer.

12V DC Pumps form the crucial and substantial second-largest segment, effectively bridging the gap between industrial systems and light-duty mobility. These pumps, designed for seamless integration with light-duty vehicles, agricultural machinery, and recreational vehicles, cater to farmers, small contractors, and individual equipment owners. Their strength lies in universal accessibility, ensuring any vehicle with a standard electrical system can serve as a mobile fueling station. By empowering the individual operator rather than relying on fixed infrastructure, this segment addresses the reality that refueling needs are often distributed across vast farmlands or scattered job sites. This balance of convenience and utility makes 12V pumps the primary entry point for first-time buyers and sustained light-commercial market growth. As such, 12V configurations will remain indispensable, meeting the nuanced needs of a decentralized user base.

The Others category, including Brushless DC (BLDC) and high-voltage aerospace applications, represents a smaller but rapidly advancing segment. BLDC pumps are gaining traction in applications demanding maximum efficiency and longevity, while specialized high-voltage pumps serve unique aerospace and military platforms, showcasing the market's high-tech frontier.

By Mounting Type Analysis

Portable Pumps are poised to be the largest and most dominant mounting type segment, driven by powerful global operational trends. The relentless expansion of mobile equipment fleets in agriculture, construction, and emergency response creates a perfect use case: operators need fueling capability wherever the equipment is located. This demand for decentralized, on-demand fueling is where DC pump adoption scales exponentially, ensuring fuel access across geographically dispersed sites. The segment is acutely reinforced by the growing popularity of battery-powered DC pumps, offering true cordless operation independent of a host vehicle's battery, and the enduring utility of simple, low-cost manual pumps for backup or fluid transfer. From remote ranches to disaster zones, the operational imperative for mobility makes portable pumps not merely preferred but often the only viable solution.

Fixed Pumps ranks as the second-largest mounting type segment, fueled by its own distinct operational imperatives. Facilities such as small refueling stations, equipment depots, and fleet maintenance yards require dedicated, always-available pumping solutions. Integrated tank systems, where the pump is permanently mounted on a fuel storage tank, provide a turnkey solution for semi-permanent sites like large construction camps or mine sites. The reliability and readiness of fixed installations justify their selection for locations with predictable, high-volume fueling needs. While more constrained in total unit volume compared to portable pumps, the higher per-unit value and recurring demand from commercial and industrial facilities secure the fixed segment's role as an enduring, stable market pillar.

By Application Analysis

Mining is anticipated to dominate the market as the primary driver and beneficiary of advanced DC fuel transfer pump integration. Mining operations possess the capital budgets for premium, high-durability equipment, the logistical necessity for remote fueling, and the safety-critical nature requiring reliable, often explosion-proof pumps. For them, pump adoption is a strategic imperative to maintain continuous production, satisfy safety regulations, and control operational costs. The mining sector serves as an essential anchor customer for manufacturers, providing predictable, high-volume demand signals that justify investment in ruggedized, high-performance product lines. Their focus on heavy-duty 24V systems, high flow rates, and auditable maintenance records aligns perfectly with the capabilities of advanced Above 1 HP pumps and smart monitoring platforms. This control over fuel logistics enhances their overall operational efficiency and production credibility.

Military represents the vital second-largest application segment, for whom DC pump adoption is a strategic response to unique operational requirements. Confronted with the need to refuel diverse fleets, from light tactical vehicles to heavy armored units and aircraft—in remote, often hostile environments, military forces demand compact, reliable, and multi-voltage-capable pumps. For them, a solution encompassing rugged construction, ease of transport, compatibility with multiple fuel types, and straightforward field maintenance represents a mission-critical capability. Adoption in this segment is often accelerated by geopolitical tensions and peacekeeping commitments. By mastering mobile fuel logistics, these forces ensure operational reach and combat effectiveness.

By End-User Industry Analysis

Oil & Gas is projected to be the largest end-user industry segment, driven by the sector's extensive upstream, midstream, and downstream operations requiring fuel transfer for exploration rigs, pipeline maintenance vehicles, and remote facility generators. The industry's stringent safety requirements drive demand for certified, explosion-proof pumps, while its scale necessitates high-volume, durable equipment. For the Oil & Gas industry, reliable fuel transfer is intrinsic to core operations, from powering drilling equipment to maintaining critical infrastructure. Their focus on operational integrity and safety compliance aligns perfectly with premium pump features and robust certification standards. This reliance on secure fuel logistics reinforces their position as a leading end-user.

Transportation ranks as the second-largest end-user industry segment, encompassing commercial trucking fleets, railroads, marine vessels, and aviation ground support. For these entities, DC fuel transfer pumps are essential for depot fueling, roadside assistance, and marine refueling operations. The segment's focus on minimizing vehicle downtime and optimizing fuel logistics creates strong demand for efficient, portable, and sometimes high-flow pumping solutions. Adoption is driven by the constant pressure to improve fleet utilization and reduce operational costs.

The Global DC Fuel Transfer Pump Market Report is segmented on the basis of the following:

By Type

By Motor Voltage

- 12V DC

- Light-duty vehicles

- Agricultural machinery

- 24V DC

- Heavy-duty vehicles

- Industrial machinery

- Others

- Brushless DC (BLDC)

- High-voltage aerospace applications

By Mounting Type

- Portable

- Manual Pumps

- Battery-powered DC Pumps

- Fixed

- Small refueling stations

- Integrated tank systems

By Application

By End-User Industry

- Oil & Gas

- Transportation

- Manufacturing

- Retail

- Others

Impact of Artificial Intelligence in the Global DC Fuel Transfer Pump Market

- AI for Predictive Maintenance: AI algorithms analyze pump motor vibration data, current draw, and duty cycles to predict component failures before they occur, enabling proactive maintenance scheduling and reducing unplanned downtime in remote mining and construction operations.

- AI-Driven Fleet Fuel Optimization: Telematics platforms integrate pump data to provide AI-powered recommendations for optimizing refueling routes and schedules across large equipment fleets, minimizing fuel wastage and maximizing machine utilization.

- Smart Leak Detection & Theft Prevention: AI models analyze flow rate anomalies and real-time pressure data from connected pumps to instantly detect potential leaks or unauthorized fuel diversion, triggering automated alerts and enabling rapid response for loss prevention.

- Digital Twin Simulation for System Design: Engineers use AI to create digital twins of fuel transfer systems, simulating pump performance under various flow, pressure, and environmental conditions to optimize system design before physical deployment.

- Inventory and Supply Chain Forecasting: AI predicts demand for spare parts and new pumps based on utilization data, seasonal trends, and infrastructure project timelines, optimizing manufacturer inventory levels and distributor stock availability.

Global DC Fuel Transfer Pump Market: Regional Analysis

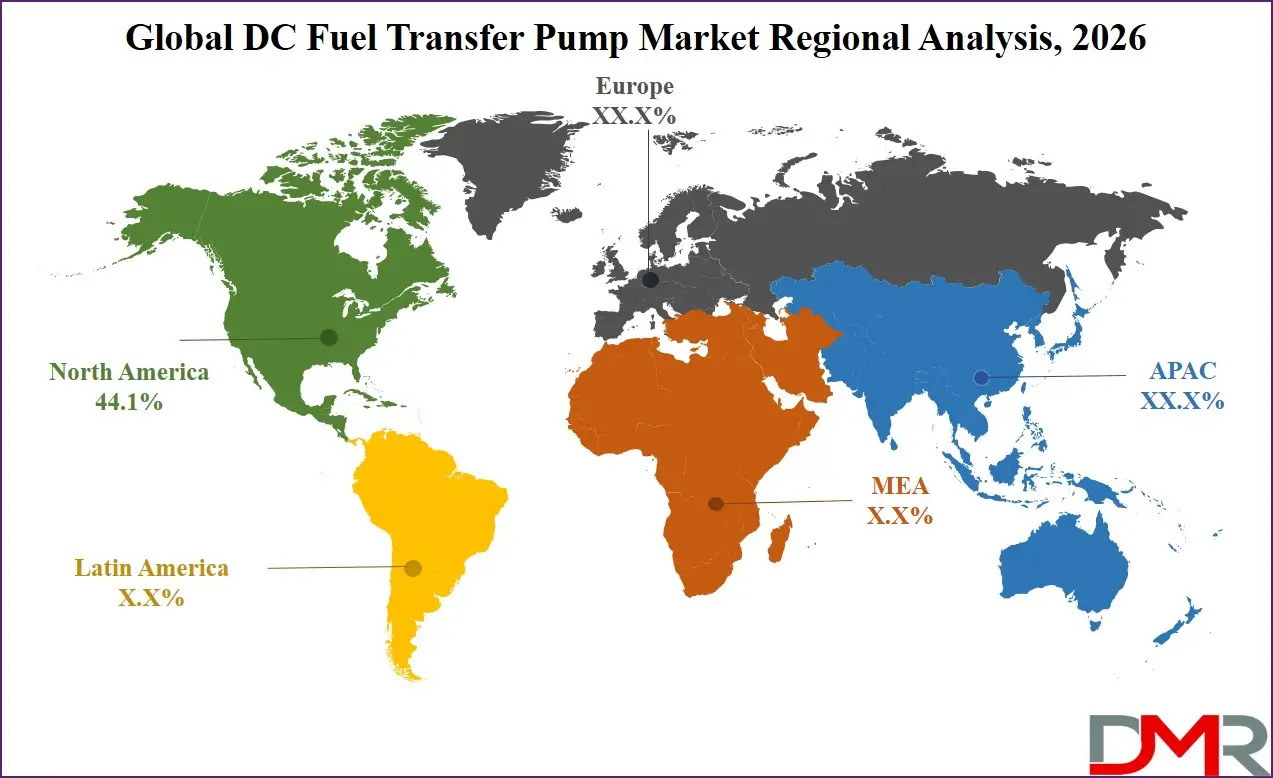

Region with the Largest Revenue Share

North America is projected to dominate the Global DC Fuel Transfer Pump Market with 44.1% of market share by the end of 2026, owing to a powerful combination of high equipment density in agriculture and construction, mature mining sector, robust military logistics spending, and the presence of dominant pump manufacturers. The United States and Canada have rapidly integrated advanced fuel transfer solutions into fleet operations, farm mechanization, and industrial project execution. Major distributors and manufacturers are scaling production and distribution networks to meet sustained institutional and commercial demand.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The region's off-road vehicle and machinery intensity, coupled with expansive agricultural land and large-scale infrastructure renewal, creates a durable multi-channel demand environment. Supportive trade policies and gradual technology-driven replacement cycles further solidify North America's leadership position.

Region with the Highest CAGR

Asia-Pacific holds the highest CAGR of 7.2% and is poised to achieve rapid market share growth due to its massive infrastructure construction boom, rapidly expanding mining sector, and accelerating agricultural mechanization. Countries like China, India, Australia, and Indonesia are investing heavily in mining exploration, transport corridors, and modern farming techniques. China's Belt and Road Initiative and India's National Infrastructure Pipeline are creating fertile ground for industrial and construction equipment adoption, directly driving demand for DC fuel transfer pumps. The region's cost sensitivity is being addressed through domestic manufacturing partnerships, government-subsidized equipment programs, and scaled basic pump configurations optimized for mass distribution. This, combined with immense urbanization-driven development and natural resource extraction, positions APAC as the fastest-growing market for DC fuel transfer systems.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Global DC Fuel Transfer Pump Market: Competitive Landscape

The Global DC Fuel Transfer Pump Market is moderately consolidated, featuring a mix of established industrial equipment manufacturers, specialized fuel handling suppliers, and emerging regional players. Leading fluid transfer equipment players Dover Corporation (Fill-Rite), Great Plains Industries (GPI), and Piusi S.p.A. are leveraging their vast distribution networks and application expertise to capture institutional and commercial market share. Pure-play industrial pump innovators are driving market dynamics with product development focused on durability, accuracy, and compliance with hazardous-duty standards.

Regional manufacturers in Asia and Latin America play increasingly influential roles in expanding the portable and light-duty segments through cost-competitive products and expanding distribution networks. Traditional industrial equipment manufacturers are also entering the space through strategic acquisitions and white-label partnerships, aiming to capture fuel management-specific procurement contracts.

Some of the prominent players in the Global DC Fuel Transfer Pump Market are:

- Fill-Rite

- Great Plains Industries, Inc. (GPI)

- Piusi S.p.A.

- Graco Inc.

- Tuthill Transfer Systems

- Caterpillar Inc.

- Bosch Rexroth AG

- Yamada Corporation

- Parker Hannifin Corporation

- Dover Corporation

- Xylem Inc.

- SPX Flow, Inc.

- Lutz Pumpen GmbH

- Intradin (Shanghai) Machinery Co., Ltd.

- Tera Pump

- MACnaught Pty Ltd

- Zhejiang Yongjia Pump Factory

- Creative Engineers

- YuanHeng Machine

- Tokheim / OPW

- Gilbarco Veeder-Root

- Other Key Players

Recent Developments in the Global DC Fuel Transfer Pump Market

- November 2025: Dover Corporation (Fill-Rite) launched its next-generation NX Series DC fuel transfer pumps featuring integrated digital intelligence for flow rate monitoring, totalizer data, and Bluetooth connectivity for smartphone-based control and fleet management integration.

- October 2025: Great Plains Industries (GPI) unveiled its new line of BLDC fuel transfer pumps, offering 30% longer motor life and 15% higher energy efficiency compared to traditional brushed motors, targeting heavy-duty agricultural and mining applications.

- September 2025: Piusi S.p.A. completed the acquisition of a leading specialist in portable battery-powered DC pump technology, strengthening its off-grid fueling product portfolio and European market access.

- August 2025: Tuthill Corporation secured a multi-year framework agreement to supply ruggedized DC fuel transfer pumps for military field fueling systems across multiple allied nations, marking significant international defense sector expansion.

- July 2025: The International Organization for Standardization (ISO) published updated safety standards for fuel dispensing equipment, driving demand for certified, compliant DC pumps in industrial and hazardous environments.

- June 2025: Graco Inc. announced a national retail placement agreement with a major U.S. farm supply cooperative for its compact 12V DC pumps, signaling mainstream agricultural market maturation and accessibility expansion.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 91.2 Mn |

| Forecast Value (2035) |

USD 146.4 Mn |

| CAGR (2026–2035) |

5.4% |

| The US Market Size (2026) |

USD 33.8 Mn |

| Historical Data |

2020 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Type (Below 1 HP, Above 1 HP), By Motor Voltage (12V DC, 24V DC, Others), By Mounting Type (Portable, Fixed), By Application (Mining, Military, Others), By End-User Industry (Oil & Gas, Transportation, Manufacturing, Retail, Others) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

Fill-Rite, Great Plains Industries, Inc. (GPI), Piusi S.p.A., Graco Inc., Tuthill Transfer Systems, Caterpillar Inc., Bosch Rexroth AG, Yamada Corporation, Parker Hannifin Corporation, Dover Corporation, Xylem Inc., SPX Flow, Inc., Lutz Pumpen GmbH, Intradin (Shanghai) Machinery Co., Ltd., Tera Pump, MACnaught Pty Ltd, Zhejiang Yongjia Pump Factory, Creative Engineers (Malhar Pumps), YuanHeng Machine, Tokheim / OPW, Gilbarco Veeder-Root, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global DC Fuel Transfer Pump Market?

▾ The Global DC Fuel Transfer Pump Market size is estimated to have a value of USD 91.2 million in 2026 and is expected to reach USD 146.4 million by the end of 2035.

What is the growth rate in the Global DC Fuel Transfer Pump Market in 2026?

▾ The market is growing at a CAGR of 5.4% over the forecasted period of 2026.

What is the size of the US DC Fuel Transfer Pump Market?

▾ The US DC Fuel Transfer Pump Market is projected to be valued at USD 33.8 million in 2026. It is expected to witness subsequent growth in the upcoming period as it holds USD 52.8 million in 2035 at a CAGR of 5.1%.

Which region accounted for the largest Global DC Fuel Transfer Pump Market?

▾ North America is expected to have the largest market share in the Global DC Fuel Transfer Pump Market with a share of about 44.1% in 2026.

Who are the key players in the Global DC Fuel Transfer Pump Market?

▾ Some of the major key players in the Global DC Fuel Transfer Pump Market are Fill-Rite, Great Plains Industries, Inc. (GPI), Graco Inc., Tuthill Transfer Systems, Caterpillar Inc., and many others.