What is the Digital Breast Tomosynthesis Market Size?

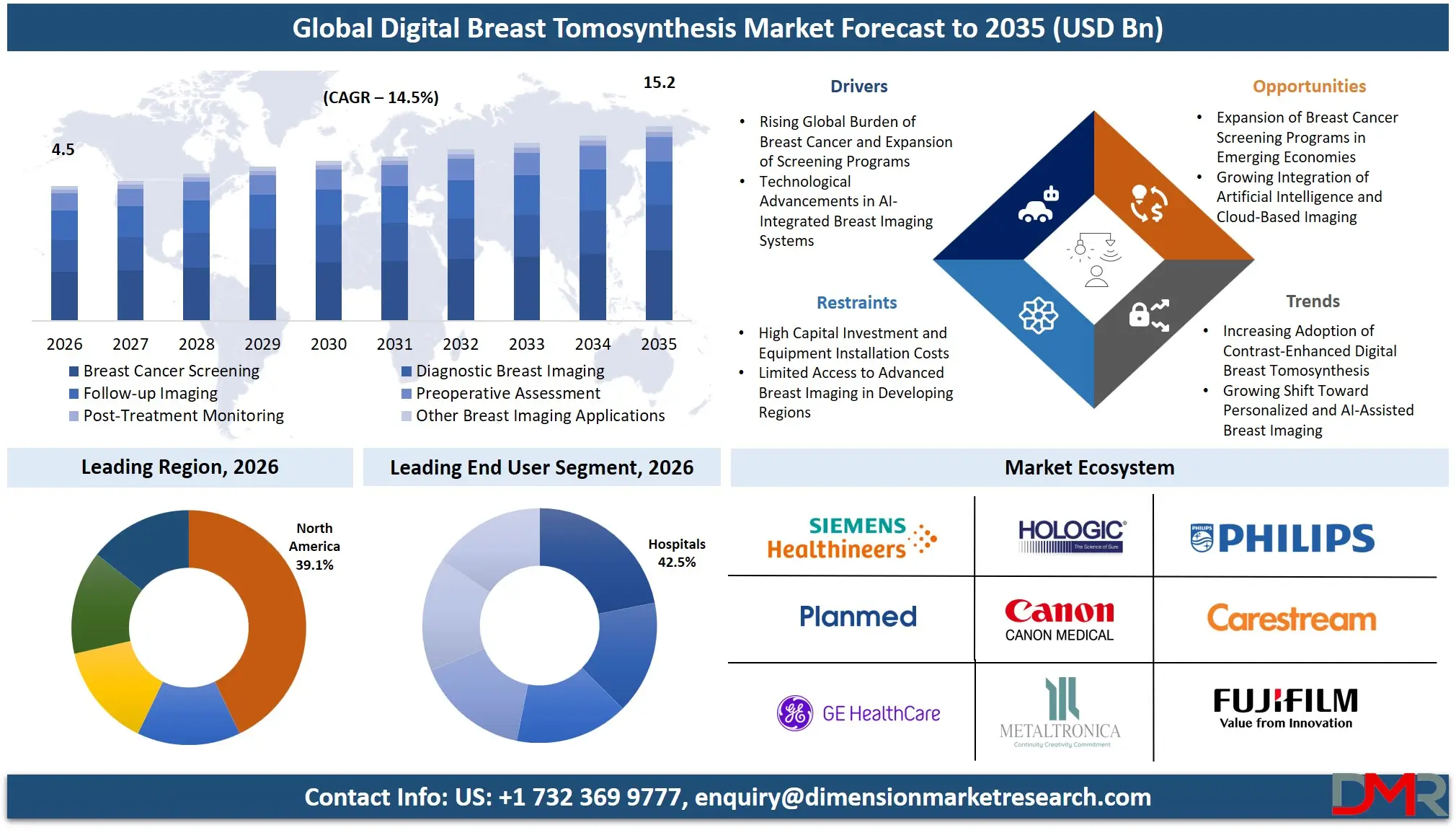

The Global Digital Breast Tomosynthesis Market is expected to reach a value of USD 4.5 billion in 2026, and it is further anticipated to reach USD 15.2 billion by 2035, growing at a CAGR of 14.5% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The digital breast tomosynthesis market is experiencing a high growth rate as healthcare providers intensify their focus on precision diagnostics and transition from conventional 2D mammography to 3D imaging infrastructure. The market consists of advanced hardware systems, AI-powered software, and specialized services that assist healthcare facilities in implementing, maintaining, and optimizing breast imaging workflows. The increasing demand to implement AI-integrated imaging, contrast-enhanced protocols, and synthetic 2D reconstruction is driving the necessity of specialized professional services and continuous hardware-software upgrades. Hospitals and diagnostic imaging centers are the most frequent adopters, with integrated 2D/3D combination systems remaining the most popular due to their clinical versatility and workflow efficiency. The hospital, breast care center, and academic research institute segments are key players as they need high-throughput, compliant, and highly accurate diagnostic ecosystems.

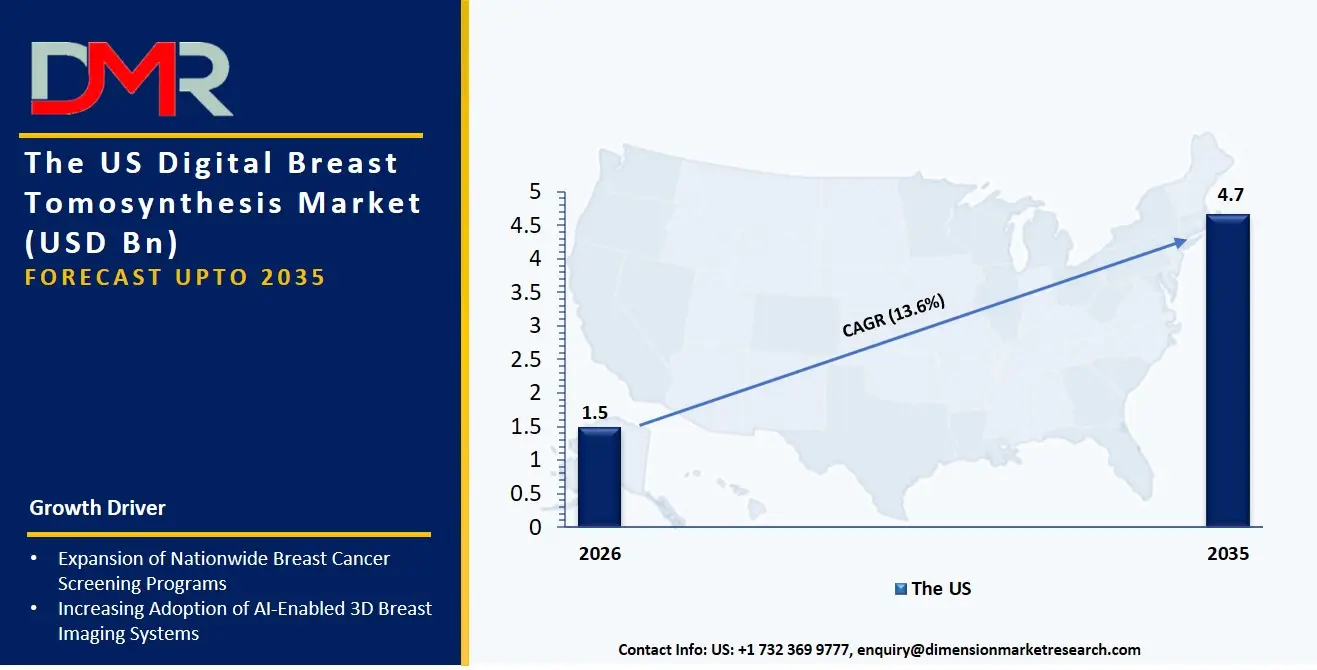

The US Digital Breast Tomosynthesis Market

The US Digital Breast Tomosynthesis Market is projected to reach USD 1.5 billion in 2026 at a compound annual growth rate of 13.6% over its forecast period, culminating in a value of USD 4.7 billion by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US continues to be the largest and most developed market in digital breast tomosynthesis due to the active fleet modernization efforts of large hospital networks and the widespread rollout of AI-based detection tools in outpatient imaging centers. The market has been typified by high demand for AI-integrated DBT systems where radiologists are aimed at enhancing lesion conspicuity while taming escalating screening volumes. Besides, the implementation of synthetic 2D imaging in clinical workflows is producing a similar need in training and education services to regulate standardization and optimize dose management protocols across multi-vendor imaging fleets.

The Europe Digital Breast Tomosynthesis Market

The Europe Digital Breast Tomosynthesis Market is estimated to be valued at USD 1.3 billion in 2026 and is further anticipated to reach USD 4.2 billion by 2035 at a CAGR of 13.9%. The regulatory frameworks including EU MDR and country-specific breast screening directives have a significant impact on the European market and drive the need to employ AI-based CAD software and standardized reporting solutions. Accelerated growth of contrast-enhanced digital breast tomosynthesis (CE-DBT) services is also being experienced in the region as oncology centers in Germany and France are trying to balance diagnostic sensitivity with biopsy avoidance. In addition, organized screening programs are challenging service providers to create dedicated PACS integration software to provide seamless data interoperability and image sharing across European healthcare ecosystems.

The Japan Digital Breast Tomosynthesis Market

The Japan Digital Breast Tomosynthesis Market is projected to be valued at USD 435.6 million in 2026 at a CAGR of 12.9%. The Japanese market is unique, with a national mandate to improve cancer detection rates in response to a rapidly aging demographic and dense breast tissue prevalence. High-throughput standalone 3D tomosynthesis systems and maintenance and repair services make up a large part of the spending as large university hospitals migrate from analog and computed radiography systems to digital breast tomosynthesis. There is also a strong need to integrate deeply within the local clinical informatics landscape to bridge the gaps between legacy PACS infrastructure and new AI-driven image visualization and review software, which forms a niche in workflow automation and dedicated breast imaging protocols.

Key Takeaways

- Market Size & Forecast: The Global Digital Breast Tomosynthesis market is projected to reach USD 4.5 billion in 2026, expanding dramatically to USD 15.2 billion by 2035, fueled by the dual drivers of escalating breast cancer prevalence and the mandatory modernization of mammography screening infrastructure with 3D capabilities.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 14.5%, driven by a critical focus on reducing recall rates and the escalating clinical demand for managing high patient volumes with AI-based detection and CAD software.

- Primary Growth Drivers: Key forces include the widespread transition from conventional 2D mammography to tomosynthesis, the need for advanced image reconstruction software to avoid diagnostically challenging artifacts, and the integration of deep learning algorithms requiring specialized hardware upgrades.

- Key Market Trends: Major trends include the rise of contrast-enhanced digital breast tomosynthesis (CE-DBT) for preoperative assessment, the use of AI-powered tools within diagnostic breast imaging to characterize lesions, and the shift toward synthetic 2D imaging as practices prioritize dose reduction and workflow efficiency.

- By Technology Analysis: AI-Integrated Digital Breast Tomosynthesis is expected to dominate clinical discussions due to its potential to improve cancer detection rates and reading speed. Professional services are increasingly required to build seamless system integration layers that connect novel AI-CAD with existing PACS and reporting platforms.

- By Application Analysis: Breast Cancer Screening and Diagnostic Breast Imaging are the most established applications due to established population health protocols. Preoperative Assessment is the fastest-growing application as surgical planning increasingly relies on the three-dimensional tissue architecture provided by DBT to determine disease extent.

- By End User Analysis: Hospitals and Diagnostic Imaging Centers are the most lucrative segments due to their high procedural volumes. Specialty Breast Care Centers are the fastest-growing sector as dedicated women's health facilities seek to create a one-stop, premium diagnostic experience that integrates 3D imaging detectors with immediate expert consultation.

- Regional Leadership: North America is poised to dominate this market with 39.1% of the market share in 2026 due to its well-developed healthcare infrastructure, favorable reimbursement frameworks, and pioneering adoption of AI-integrated systems that establish it as a leader in this market.

What is the Digital Breast Tomosynthesis?

Digital Breast Tomosynthesis services are the specialized clinical implementation, integration, and maintenance offerings that are provided by original equipment manufacturers (OEMs), third-party service organizations, and clinical informatics consultancies to assist healthcare providers through the entire DBT lifecycle. These services, unlike the imaging hardware itself, are related to the how of tomosynthesis adoption. This involves Installation & System Integration to establish optimized image acquisition protocols without disrupting patient throughput, Maintenance & Repair Services to ensure maximum system uptime and consistent image quality, and Training & Education Services to ensure that radiologists and technologists can effectively leverage the advanced capabilities of 3D imaging. With over 85% of accredited breast centers operating DBT systems, professional services are needed to achieve standardization, quality assurance, and operational efficiency, making DBT investments translate into tangible improvements in diagnostic confidence, rather than merely capital equipment expense.

Use Cases

- High-Volume Screening Modernization in Hospitals: Hospital radiology departments hire installation and system integration services to replace aging 2D mammography fleets with integrated 2D/3D combination systems, ensuring seamless PACS integration and enabling high-throughput screening with synthetic 2D images that reduce interpretation time and patient dose.

- AI-Enhanced Lesion Characterization in Diagnostic Imaging: Specialized breast care centers use AI-based detection & CAD software alongside maintenance & repair services to ensure their integrated DBT systems operate at peak performance when analyzing suspicious microcalcifications and architectural distortions, providing a "second reader" for diagnostic breast imaging workflows.

- Clinical Trial Standardization in Academia: Academic and research institutes use training and education services and image reconstruction software to harmonize DBT acquisition parameters across multi-site clinical trials, ensuring that image quality is consistent and compliant with rigorous research data standards for evaluating novel contrast-enhanced imaging techniques.

- Preoperative Surgical Planning Integration: Ambulatory surgical centers deploy image visualization & review software and upgrade/retrofit kits on existing systems to enable surgeons to visualize the three-dimensional extent of a tumor, facilitating precise wire localization and improving the accuracy of breast-conserving surgeries.

How AI is Transforming the Digital Breast Tomosynthesis Market?

AI is fundamentally changing the digital breast tomosynthesis market by accelerating the image interpretation process and enhancing diagnostic precision. In image reconstruction software, AI-based iterative reconstruction techniques have the potential to automatically reduce metal artifacts and anatomical noise, greatly minimizing image degradation and improving the conspicuity of lesions in dense breast tissue. Meanwhile, AI-powered features in AI-based detection and CAD software allow radiologists to better prioritize reading worklists by detecting suspicious regions, predicting the likelihood of malignancy, and suggesting lesion segmentations, reinforcing the shift towards precision medicine.

Clinical operations and business transformation projects are also revolving around AI. In the area of consulting services, intelligent workflow management agents are used to continuously monitor the performance of multiple DBT systems across a health network and identify imaging protocol deviations, calibration drift, and security deficiencies to keep healthcare organizations in line with ACR and MQSA standards. Moreover, generative AI assistants are complementing image visualization and review software by simulating enhancement patterns and modeling future lesion morphology to give researchers a visualization of tumor progression before committing to invasive biopsy protocols.

Market Dynamics

Key Drivers in the Global Digital Breast Tomosynthesis Market

Rising Global Burden of Breast Cancer and Expansion of Screening Programs

The increasing incidence of breast cancer worldwide remains the primary driver of the digital breast tomosynthesis (DBT) market. Governments, healthcare organizations, and cancer societies continue expanding organized breast cancer screening initiatives to promote early diagnosis and improve survival rates. Compared with conventional digital mammography, DBT offers superior lesion visualization, higher invasive cancer detection rates, and reduced recall rates, making it the preferred imaging modality in many healthcare systems. Growing awareness regarding preventive screening, favorable reimbursement policies in developed countries, and continuous investments in national screening infrastructure further accelerate the adoption of DBT technologies across hospitals and diagnostic imaging centers globally.

Technological Advancements in AI-Integrated Breast Imaging Systems

Continuous innovation in digital breast tomosynthesis systems is driving market expansion through improved diagnostic accuracy and workflow efficiency. Artificial intelligence-powered computer-aided detection, synthetic 2D imaging, advanced reconstruction algorithms, and low-dose imaging technologies enable radiologists to identify suspicious lesions with greater confidence while reducing interpretation time. Manufacturers are integrating cloud-based image management, PACS interoperability, and automated reporting solutions to enhance productivity in high-volume screening centers. Increasing regulatory approvals for AI-enabled breast imaging software and growing investments by healthcare providers in precision diagnostics continue strengthening the global adoption of advanced digital breast tomosynthesis platforms.

Restraints in the Global Digital Breast Tomosynthesis Market

High Capital Investment and Equipment Installation Costs

The substantial acquisition cost of digital breast tomosynthesis systems remains a major challenge, particularly for small hospitals and diagnostic centers in developing economies. In addition to purchasing advanced imaging equipment, healthcare providers must invest in software licenses, infrastructure upgrades, installation, staff training, and long-term maintenance. Budget constraints often delay replacement of conventional mammography systems with DBT platforms. Limited reimbursement in certain regions further reduces purchasing incentives. Consequently, the high total cost of ownership continues to restrict broader market penetration, especially among resource-constrained healthcare institutions and emerging healthcare markets.

Limited Access to Advanced Breast Imaging in Developing Regions

Healthcare disparities across low- and middle-income countries continue limiting widespread adoption of digital breast tomosynthesis. Many healthcare facilities lack advanced imaging infrastructure, trained breast imaging specialists, and sufficient financial resources to implement comprehensive screening programs. Rural populations often experience delayed diagnosis because of limited availability of specialized diagnostic services. Inadequate awareness regarding breast cancer screening and inconsistent reimbursement policies further reduce utilization rates. These infrastructure and accessibility challenges restrict market expansion despite increasing global demand for early breast cancer detection and advanced diagnostic imaging technologies.

Growth Opportunities in the Global Digital Breast Tomosynthesis Market

Expansion of Breast Cancer Screening Programs in Emerging Economies

Rapid improvements in healthcare infrastructure across Asia-Pacific, Latin America, the Middle East, and Africa present significant opportunities for digital breast tomosynthesis manufacturers. Governments are investing in nationwide cancer screening initiatives, diagnostic imaging facilities, and women's healthcare programs to improve early breast cancer detection. Increasing healthcare expenditure, expanding insurance coverage, and greater public awareness regarding preventive screening are encouraging adoption of advanced mammography technologies. Manufacturers introducing affordable, scalable DBT solutions tailored for emerging markets are well positioned to capitalize on rising demand and expanding healthcare accessibility.

Growing Integration of Artificial Intelligence and Cloud-Based Imaging

Artificial intelligence and digital healthcare technologies are creating new growth opportunities across the breast imaging ecosystem. AI-assisted lesion detection, automated breast density assessment, workflow optimization, and cloud-based image sharing improve diagnostic accuracy while supporting remote collaboration among radiologists. These innovations address increasing imaging workloads and shortages of experienced breast imaging specialists. Integration with enterprise imaging platforms and tele-radiology networks enables faster reporting and improved clinical decision-making. Continued advancements in AI algorithms and digital healthcare infrastructure are expected to accelerate global adoption of next-generation digital breast tomosynthesis solutions.

Trends in the Global Digital Breast Tomosynthesis Market

Increasing Adoption of Contrast-Enhanced Digital Breast Tomosynthesis

Contrast-enhanced digital breast tomosynthesis (CE-DBT) is emerging as an important advancement in breast imaging by combining functional contrast enhancement with three-dimensional anatomical visualization. The technology improves lesion characterization and diagnostic confidence, particularly among women with dense breast tissue or inconclusive mammography findings. Healthcare providers increasingly evaluate CE-DBT as a cost-effective alternative to breast MRI for selected clinical indications. Ongoing clinical research, product innovation, and regulatory approvals continue expanding the clinical applications of contrast-enhanced tomosynthesis, supporting its growing adoption in comprehensive breast imaging programs.

Growing Shift Toward Personalized and AI-Assisted Breast Imaging

Breast imaging is increasingly evolving toward personalized screening strategies supported by artificial intelligence and patient-specific risk assessment. Healthcare providers are incorporating breast density analysis, clinical history, genetic risk factors, and AI-powered decision support into individualized screening pathways. Digital breast tomosynthesis serves as a central technology within these precision screening programs because of its superior diagnostic performance across diverse patient populations. Simultaneously, AI-assisted workflow automation reduces radiologist workload, improves reporting consistency, and enhances overall operational efficiency, making personalized, technology-enabled breast imaging a defining trend in the global market.

Research Scope and Analysis

The Global Digital Breast Tomosynthesis Market is segmented by component, product type, technology, application, and end user. These segments evaluate advancements in 3D breast imaging systems, AI-enabled software, screening and diagnostic applications, healthcare delivery settings, and technology adoption, reflecting increasing demand for accurate breast cancer detection, workflow efficiency, and personalized imaging solutions worldwide.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

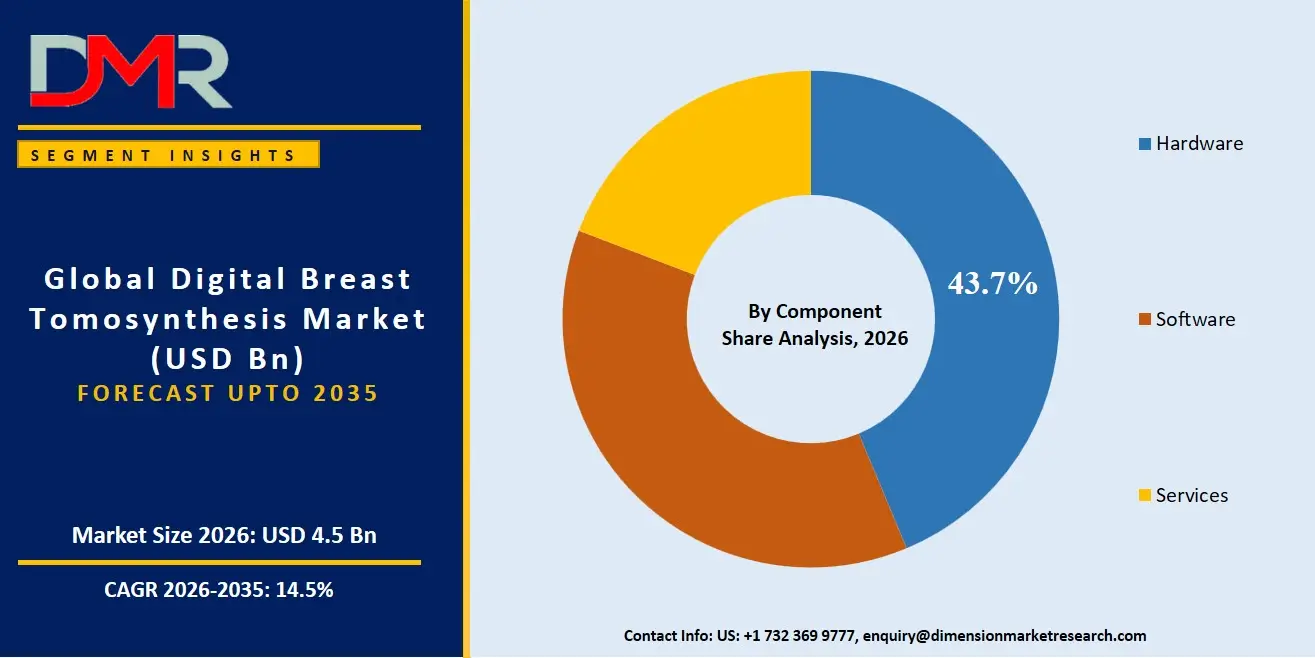

By Component Analysis

Hardware is projected to dominate the Global Digital Breast Tomosynthesis Market as imaging systems, flat panel detectors, X-ray tubes, and acquisition workstations represent the highest capital investment within breast imaging infrastructure. Hospitals and diagnostic centers prioritize advanced DBT hardware to improve lesion detection, reduce tissue overlap, and enhance diagnostic confidence compared with conventional digital mammography. Continuous technological innovations in detector sensitivity, image quality, and radiation dose optimization further drive hardware replacement cycles. The increasing establishment of dedicated breast imaging centers and national breast cancer screening programs worldwide also supports demand for high-performance imaging equipment. Consequently, hardware accounts for the largest revenue share across the digital breast tomosynthesis ecosystem.

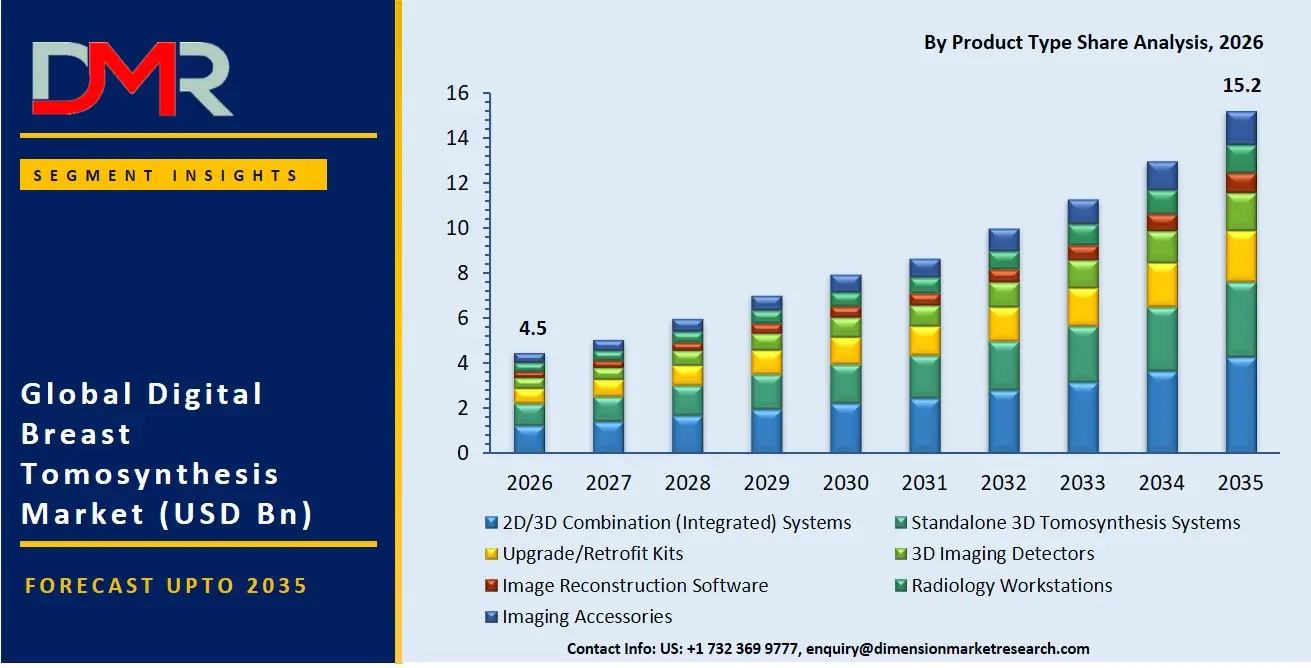

By Product Type Analysis

2D/3D Combination (Integrated) Systems is poised to dominate the product type segment because they enable healthcare providers to perform both conventional digital mammography and three-dimensional breast tomosynthesis using a single imaging platform.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

This dual functionality improves workflow efficiency, reduces equipment costs, and facilitates seamless transition from 2D to advanced 3D imaging. Many breast screening programs continue requiring both image formats, making integrated systems the preferred purchasing choice for hospitals and diagnostic imaging centers. Additionally, reimbursement support in developed healthcare markets and growing clinical evidence demonstrating improved cancer detection rates further strengthen adoption of integrated 2D/3D mammography systems across global healthcare facilities.

By Technology Analysis

Wide-Angle Digital Breast Tomosynthesis is poised to dominate the technology segment due to its superior image reconstruction capability and enhanced visualization of overlapping breast tissues. By acquiring images over a larger angular range, the technology provides improved lesion conspicuity, greater depth resolution, and higher diagnostic accuracy, particularly in women with dense breast tissue. Leading manufacturers continue investing in wide-angle imaging innovations to reduce recall rates and improve early breast cancer detection. Healthcare providers increasingly prefer this technology because it delivers higher clinical confidence while supporting efficient screening and diagnostic workflows, making it the most widely adopted tomosynthesis imaging approach globally.

By Application Analysis

Breast cancer screening is projected to dominates the application segment because digital breast tomosynthesis has become an essential imaging modality for early breast cancer detection. Numerous clinical studies have demonstrated that DBT improves invasive cancer detection while reducing false-positive recalls compared with conventional mammography. National screening programs across North America, Europe, and several Asia-Pacific countries increasingly incorporate tomosynthesis into routine breast cancer screening protocols. Rising breast cancer incidence, expanding awareness campaigns, and government investments in organized screening initiatives continue driving examination volumes. The emphasis on early diagnosis and improved patient outcomes ensures breast cancer screening remains the largest application segment.

By End User Analysis

Hospitals is anticipated to dominate the end-user segment owing to their comprehensive diagnostic imaging infrastructure, high patient volumes, and availability of specialized breast imaging departments. Large hospitals possess the financial capacity to invest in advanced digital breast tomosynthesis systems integrated with artificial intelligence, PACS, and electronic health record platforms. They also serve as referral centers for breast cancer diagnosis, surgical planning, and multidisciplinary oncology care. Growing investments in hospital modernization, increasing breast cancer screening programs, and rising adoption of precision diagnostic technologies further reinforce hospital leadership. Their ability to provide complete diagnostic and treatment pathways supports continued market dominance.

The Global Digital Breast Tomosynthesis Market Report is segmented on the basis of the following:

By Component

- Hardware

- Digital Breast Tomosynthesis (DBT) Imaging Systems

- X-ray Tubes

- Flat Panel Detectors

- Compression Systems

- Image Acquisition Workstations

- Display Monitors

- Software

- Image Acquisition Software

- Image Reconstruction Software

- AI-Based Detection & CAD Software

- Image Visualization & Review Software

- PACS Integration Software

- Reporting & Workflow Management Software

- Services

- Installation & System Integration

- Maintenance & Repair Services

- Training & Education Services

By Product Type

- 2D/3D Combination (Integrated) Systems

- Standalone 3D Tomosynthesis Systems

- Upgrade/Retrofit Kits

- 3D Imaging Detectors

- Image Reconstruction Software

- Radiology Workstations

- Imaging Accessories

By Technology

- Wide-Angle Digital Breast Tomosynthesis

- Narrow-Angle Digital Breast Tomosynthesis

- Synthetic 2D Imaging

- Contrast-Enhanced Digital Breast Tomosynthesis (CE-DBT)

- Artificial Intelligence (AI)-Integrated Digital Breast Tomosynthesis

By Application

- Breast Cancer Screening

- Diagnostic Breast Imaging

- Follow-up Imaging

- Preoperative Assessment

- Post-Treatment Monitoring

- Other Breast Imaging Applications

By End User

- Hospitals

- Diagnostic Imaging Centers

- Specialty Breast Care Centers

- Ambulatory Surgical Centers (ASCs)

- Academic & Research Institutes

- Other End Users

Regional Analysis

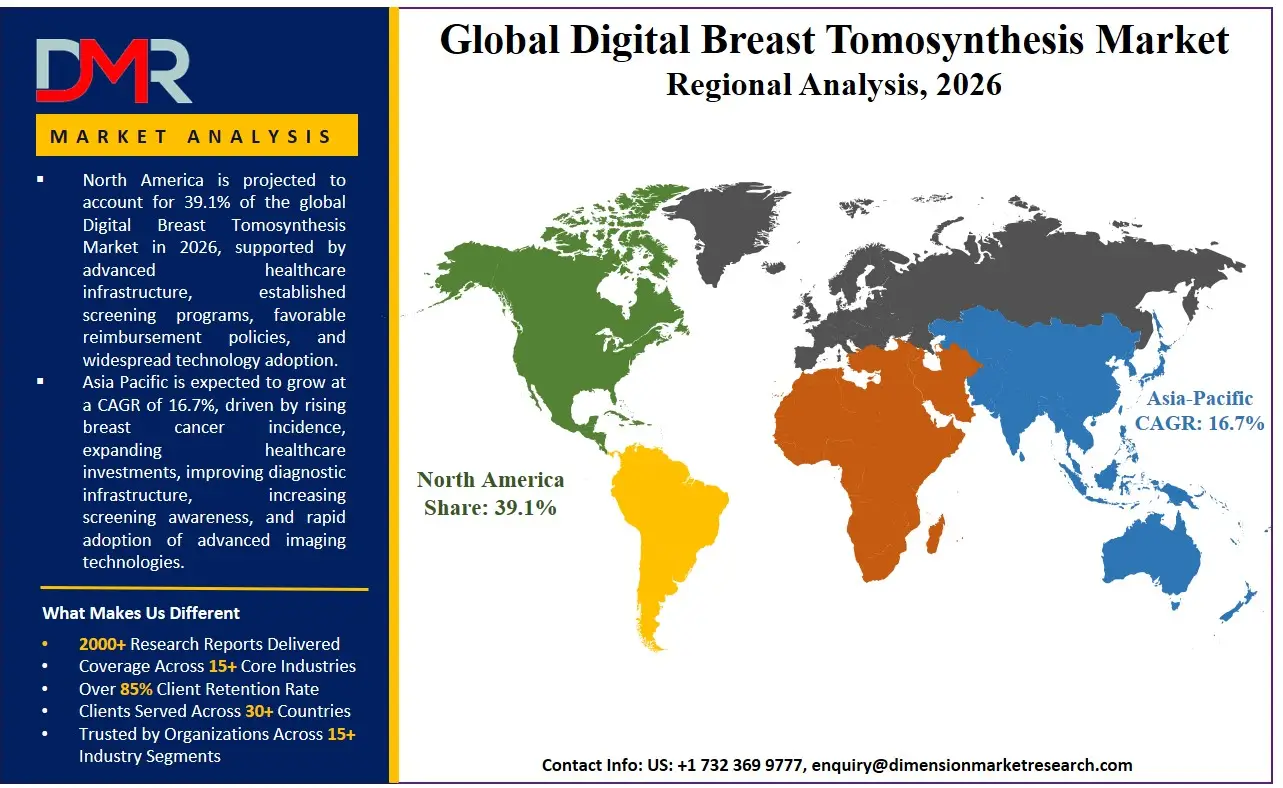

Leading Region by Market Share

ℹ

To learn more about this report –

Download Your Free Sample Report Here

North America is poised to dominate the global digital breast tomosynthesis market as it is projected to hold 39.1% of the market share by the end of 2026. The United States, which dominates North America, has the highest share in the digital breast tomosynthesis market because of the unmatched concentration of high-volume breast screening centers and the aggressive DBT and AI adoption agendas of integrated delivery networks. The area has an established ecosystem of global OEMs, specialized training consultancies, and a rich pool of fellowship-trained breast imagers and DBT-specialist technologists. Enterprise investment in artificial intelligence, advanced image reconstruction, and the overall retirement of legacy FFDM systems contribute to the continued demand for advanced hardware and software modernization along with continuous maintenance and repair services. Moreover, a robust venture capital climate persistently finances upcoming AI-CAD startups that need expert clinical integration services to achieve expeditious FDA clearance and security compliance.

Fastest-Growing Regional Market

Asia-Pacific is expected to be the most rapidly expanding digital breast tomosynthesis market, driven by government-led sweeping healthcare infrastructure modernization initiatives in India, China, Japan, and Southeast Asia. The fast-paced economic growth, the rise of a middle-class population with greater healthcare expectations, and the dynamic expansion of the private hospital sector are compelling established hospital chains and public health agencies to discard unproductive analog mammography infrastructure. Installation and system integration consulting is in high demand to help these large organizations head in the direction of advanced 3D imaging operating models. There is also a severe lack of qualified DBT-trained radiologists in the region, and it is necessary to outsource training and education services to implement, acquire, and interpret tomosynthesis studies to cover the skills gap and enable faster investments in breast imaging modernization projects.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive environment of the global digital breast tomosynthesis market has become highly dynamic with a heterogeneous array of multinational medical device OEMs, specialized AI software developers, and niche third-party service providers. The key to success will be the profound strategic alliances with leading healthcare group purchasing organizations (GPOs) and integrated delivery networks (IDNs) because they will open the necessary multi-year capital equipment contracts and early access to the new DBT screening guideline updates. The movement towards market consolidation is rapidly progressing with the traditional imaging OEMs acquiring AI-CAD engineering specialized startups to stay afloat. Proprietary intellectual property, including automated lesion segmentation frameworks and vendor-specific synthetic 2D image reconstruction algorithms, is becoming a more important basis of competitive differentiation than just spatial resolution metrics or generic detector specifications.

Some of the prominent players in the Global Digital Breast Tomosynthesis Market are:

- Hologic, Inc.

- GE HealthCare Technologies Inc.

- Siemens Healthineers AG

- Fujifilm Holdings Corporation

- Canon Medical Systems Corporation

- Koninklijke Philips N.V.

- Planmed Oy

- Metaltronica S.p.A.

- IMS Giotto S.p.A.

- Carestream Health, Inc.

- Konica Minolta, Inc.

- Delphinus Medical Technologies, Inc.

- Dilon Technologies, Inc.

- Analogic Corporation

- Allengers Medical Systems Ltd.

- Shenzhen Angell Technology Co., Ltd.

- Villa Sistemi Medicali S.p.A.

- Aurora Imaging Technology, Inc.

- iCAD, Inc.

- ScreenPoint Medical B.V.

- Other Key Players

Recent Developments

- December 2025: GE HealthCare expanded its AI imaging portfolio through a broader collaboration with NVIDIA, integrating advanced AI technologies into multiple imaging platforms, including Pristina Recon DL for breast imaging, to enhance image quality and streamline radiology workflows.

- November 2025: Hologic announced new clinical evidence at the RSNA Annual Meeting demonstrating that its Genius AI-powered mammography solutions can improve radiologists' workflow efficiency while maintaining high sensitivity for breast cancer detection, reinforcing the growing role of AI in digital breast tomosynthesis.

- September 2025: Hologic presented new research at the European Society of Breast Imaging (EUSOBI) showing that its AI-powered mammography technology can improve breast cancer detection accuracy and provide additional insights into tumor biology, supporting wider adoption of AI-enabled digital breast tomosynthesis.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 4.5 Bn |

| Forecast Value (2035) |

USD 15.2 Bn |

| CAGR (2026–2035) |

14.5% |

| The US Market Size (2026) |

USD 1.5 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Component, By Product Type, By Technology, By Application, and By End User |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Digital Breast Tomosynthesis Market?

▾ The Global Digital Breast Tomosynthesis market is poised to be valued at USD 4.5 billion in 2026 and is projected to reach USD 15.2 billion by 2035, driven by the universal need for specialized DBT systems in breast cancer screening, diagnostic imaging, and AI integration.

What is the CAGR of the Global Digital Breast Tomosynthesis Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 14.5% from 2026 to 2035, reflecting the accelerating complexity of clinical DBT environments and the persistent shortage of sub-specialized breast imaging talent.

What factors are driving the growth of the Global Digital Breast Tomosynthesis Market?

▾ Key drivers include the global radiology skills gap, the imperative to modernize legacy 2D mammography fleets, the diagnostic advantages of 3D imaging in dense breast tissue, and the surge in demand for AI-based detection & CAD software amid evolving population screening guidelines.

Which region held the largest share of the Digital Breast Tomosynthesis Market in 2026?

▾ North America is projected to hold 39.1% of market share in 2026, driven by a mature reimbursement ecosystem and aggressive healthcare enterprise investment in AI-integrated digital breast tomosynthesis and 2D/3D combination systems.

Which region is expected to grow the fastest in the Digital Breast Tomosynthesis Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid healthcare infrastructure modernization in China, India, and Japan, where installation and system integration is critical for transitioning large hospital chains to 3D imaging operations.

What are the major trends in the Global Digital Breast Tomosynthesis Market?

▾ Major trends include the integration of Generative AI into radiology reading workflows, the rise of synthetic 2D imaging and dose reduction consulting, the demand for contrast-enhanced DBT for lesion characterization, and the focus on personalized risk-adaptive screening within complex multi-vendor imaging fleets.

Who are the key players in the Global Digital Breast Tomosynthesis Market?

▾ Key players include OEMs like Hologic, Siemens Healthineers, and GE HealthCare, as well as the AI-CAD software divisions of companies like iCAD and ScreenPoint Medical, alongside specialized third-party breast imaging service providers.

How is the Global Digital Breast Tomosynthesis Market segmented?

▾ The market is segmented by Component, Product Type, Technology, Application, and End User.