The edge computing market refers to the industry focused on the deployment of computing resources toward statistics sources and end users, aiming to lessen latency, improve efficiency, and enable real-time processing of statistics. It encompasses hardware, software, and services facilitating decentralized computing at the network edge.

Key drivers include the proliferation of

Internet of Things (IoT) gadgets, rising demand for low-latency applications, and the increasing adoption of cloud computing. This marketplace serves diverse sectors which include manufacturing, healthcare, transportation, and telecommunications, among others. Key players inside the market offer edge computing solutions inclusive of aspect servers, gateways, and edge records centers. With the growing importance of records-driven insights and the need for faster processing speeds, the global edge-computing marketplace is poised for a sizable growth and innovation in the coming years.

As per Statista, the Edge Computing market is experiencing exponential growth, with global revenue projected to reach $350 billion by 2027. The research landscape underscores this momentum, as Google Scholar papers on edge computing surged from 720 in 2015 to over 42,700 in 2023, reflecting heightened innovation and investment in this domain.

Edge computing is gaining momentum with numerous events and conferences showcasing its transformative potential. Key events like Edge Computing World and IoT Solutions World Congress bring together industry leaders to discuss advancements in edge technologies.

The market is ripe with deals and partnerships, such as strategic collaborations between cloud providers and telecom companies to enhance edge infrastructure. Opportunities abound in sectors like healthcare, manufacturing, and smart cities, where edge computing drives real-time data processing and efficiency.

Edge computing in smartphones is also emerging as a key trend, enabling faster application performance, reduced latency, and enhanced user experiences by processing data closer to the device. Staying updated on edge-focused events and innovations can unlock significant growth potential in this rapidly evolving field.

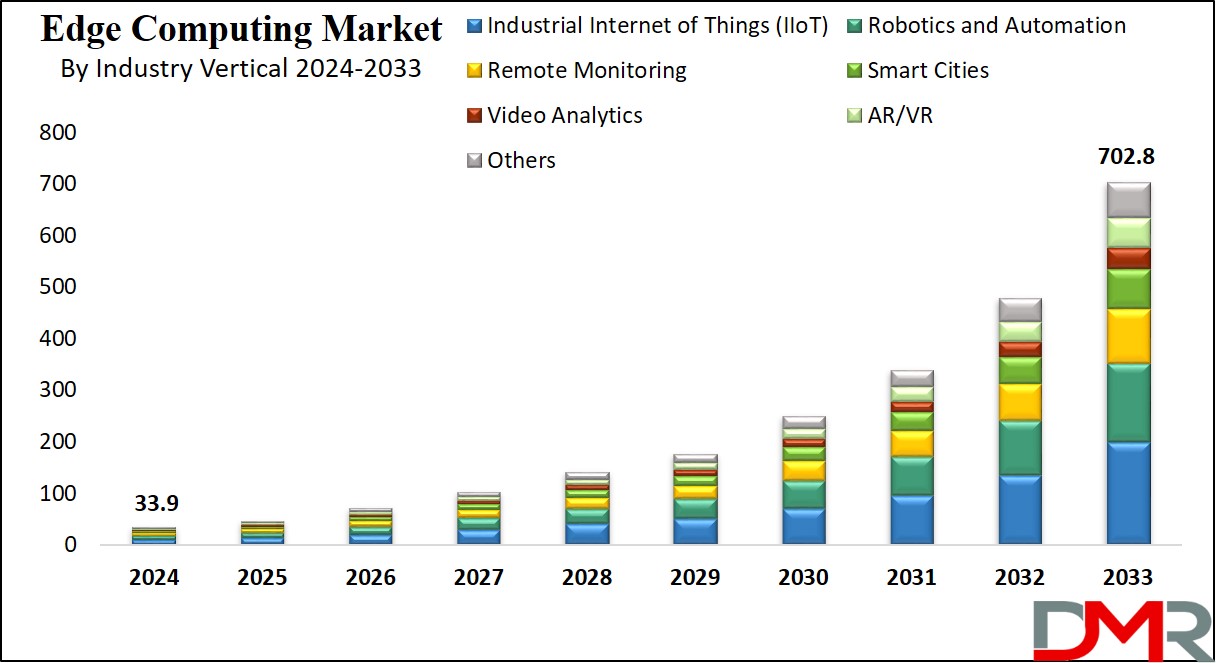

Key Takeaways

- Market Value: The market size is projected to reach a market value of USD 46.2 billion in 2025, in comparison to USD 702.8 billion in 2033 at a CAGR of 40.0%.

- Market Definition: Edge computing means doing computer processing closer to where data is produced, like on devices or at the edge of a network, for quicker results.

- Component Segment Analysis: Hardware is expected to exert its dominance in the component segment with a market value of 45.1% by the end of 2024.

- Organization Size Segment Analysis: Large enterprises are projected to exert their prominence in the organization size segment with the highest market share in 2024.

- Application Segment Analysis: Industrial Internet of Things (IIoT) is projected to command this market with a 28.0% market value in 2024.

- Industry Vertical Segment Analysis: The Energy and Utilities sector is expected to dominate the highest share in 2024.

- Regional Analysis: North America is predicted to dominate the edge computing market with 41.2% of the market share in 2024.

Use Cases

- Industrial IoT (IIoT) Optimization: Edge computing complements real-time statistics processing for predictive protection, high-quality manipulation, and performance in manufacturing and industrial operations.

- Autonomous Vehicles: Edge computing enables instant data analysis for self-sustaining vehicles, making sure of rapid decision-making and improved safety systems on roads.

- Smart Cities: Edge computing powers mart town programs which include visitor control, public safety, and environmental monitoring, improving urban living standards.

- Healthcare: Edge computing facilitates remote patient monitoring, telemedicine, and medical device data processing, enhancing healthcare delivery efficiency and patient outcomes.

Market Dynamic

The edge computing market dynamic provides a complete industry analysis, highlighting key market tendencies and dynamics shaping this market. With the proliferation of IoT gadgets throughout various industries, demand for side computing solutions is on the rise as an organization that aims to lessen latency and enhance operational performance through processing records toward its source. The emergence of 5G networks is predicted to further boost edge computing adoption, mainly in sectors such as telecommunications, self-reliant automobiles, and smart cities.

Rising concerns regarding data privacy, security, and regulatory compliance are also driving the adoption of edge computing for decentralized data processing and storage, by making sure that the companies in this market comply with data protection rules. Advancements in edge computing technology which include edge AI and edge analytics are expanding the market's competencies and use instances, fueling market growth. Strategic partnerships amongst technology vendors, telecom operators, and enterprise players are fostering innovation and ecosystem development in the edge computing enterprise.

Research Scope and Analysis

By Component

The edge computing market is dominated by hardware in the component segment with 45.1% of the market share in 2024. Hardware dominates the component segment of the edge computing marketplace due to its fundamental position in organizing the physical infrastructure important for deploying and operating edge computing solutions efficaciously.

Edge nodes/gateways (servers) shape the core part of computing networks, permitting data processing, storage, and management at the threshold of the network, therefore minimizing latency and facilitating actual-time decision-making.

Additionally, sensors and routers play a crucial role in collecting and transmitting facts from numerous resources, inclusive of IoT devices and industrial equipment, making sure the continuous drift of data to part computing structures for evaluation and insights. Moreover, end-point devices along with cameras, drones, head-mounted displays (HMDs), and robots serve as critical data resources and actuators in edge computing ecosystems, generating and interacting with facts that must be processed and analyzed at the edge for well-timed and informed decision-making.

While software, offerings, and edge-managed platforms are critical components of edge computing ecosystems, hardware stays the essential constructing block that underpins the distributed computing architecture and enables the seamless integration of edge computing into various industries and programs.

By Organization Size

Large enterprise in the edge computing market size was estimated to command the organization size segment with the highest market share in 2024. Large organizations dominate the edge computing market segment often because of their extensive resources, sophisticated infrastructure, and strategic recognition of innovation and digital transformation.

These companies normally have large budgets, allowing them to make investments closely in current technologies like side computing to gain an aggressive gain. Large organizations frequently operate throughout numerous geographic places and have complex operational requirements, making edge computing solutions critical for optimizing their processes, enhancing performance, and turning in advanced purchaser stories.

Moreover, huge firms possess the scale and capacity to implement complete part computing architectures, consisting of deploying facet servers, side devices, and networking infrastructure throughout their networks. They additionally can increase customized edge packages tailor-made to their specific industry requirements, similarly improving their operational agility and aggressive positioning.

By Application

Industrial Internet of Things (IIoT) is anticipated to dominate the application segment in the global edge computing market with 28.0% of the market share in 2024. Industrial Internet of Things (IIoT) dominates the edge computing application segment because of its considerable adoption throughout numerous industries and its transformative effect on business operations.

IIoT leverages connected sensors, devices, and machines to gather, monitor, and analyze statistics in actual time, permitting more desirable visibility, performance, and productiveness in commercial techniques. Edge computing is instrumental in helping IIoT deployments by supplying localized information processing and analysis abilities, decreasing latency, and enabling well-timed decision-making.

Moreover, industries including manufacturing, oil and gas, transportation, and utilities increasingly depend on IIoT solutions to optimize asset utilization, enhance predictive maintenance, ensure exceptional control, and improve worker safety.

The ability of facet computing to handle massive volumes of sensor statistics and perform analytics near the statistics supply is specifically positive in Industrial Internet of Things IIoT packages, where actual-time insights are important for operational performance and competitiveness. As a result, IIoT emerges as a dominant application inside the edge computing marketplace, driving innovation and transformation across industrial sectors.

By Industry Vertical

The energy and utility sector is projected to dominate the edge computing market with the highest market share in 2024. The energy and utilities area dominates this market because of its precise operational requirements and the rising need for real-time data processing and analysis. In the energy sector, edge computing performs a vital role in optimizing operations throughout the entire value chain, which includes generation, transmission, distribution, and intake.

Edge computing permits energy companies to collect and examine statistics from sensors, meters, and IoT gadgets deployed in power plants, substations, grid infrastructure, and renewable strength installations. This real-time statistics processing helps predictive maintenance, fault detection, grid optimization, and energy management, thereby improving reliability, efficiency, and sustainability.

Furthermore, edge computing is instrumental in supporting the combination of renewable strength sources, which include solar and wind power, into the grid with the aid of allowing allotted technology, energy storage, and demand response capabilities. Additionally, within the utilities sector, edge computing enhances the monitoring and management of water and wastewater systems, smart meters, and distribution networks, leading to advanced resource allocation and customer service.

The Edge Computing Market Report is segmented on the basis of the following

By Component

- Hardware

- Hardware by Type

- Edge Nodes/Gateways (Servers)

- Sensors/Routers

- Others

- Hardware by End-Point Devices

- Cameras

- Drones

- HMD

- Robots

- Others

- Software

- Edge-Managed Platform

- Services

By Organization Size

- Large Enterprise

- Small & Medium Enterprise

By Application

- Industrial Internet of Things (IIoT)

- Robotics and Automation

- Remote Monitoring

- Smart Cities

- Video Analytics

- AR/VR

- Others

By Industry Vertical

- Energy and Utilities

- Financial and Banking Industry

- Retail

- Healthcare and Life Sciences

- Industrial

- Telecommunications

- Others

Regional Analysis

The global edge computing market was valued high as its size is expected to grow at reach a higher place in various regions globally. North America is expected to dominate the edge computing market as it

hold 41.2% of the market share in 2024. The increase in the demand for edge computation solutions in various sectors like manufacturing industries, data processing and analysis sector, and retail.

The use of edge computing solutions across various sectors in this region pushes the growth of this market further. The use of this service in cloud computing and storage solutions acts as a major driver in the growth of this market.

North America undeniably dominates the global facet computing market, due to its sturdy infrastructure, technological advancements, and early adoption of edge computing solutions. Major players such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform (GCP) have their headquarters in North America and leverage the assets of the region to offer comprehensive edge computing services.

Additionally, the presence of a thriving tech ecosystem, abundant investment possibilities, and a fairly professional group of workers further solidify North America's function as a workforce in part computing innovation. Furthermore, North American enterprises throughout various sectors, such as telecommunications, healthcare, production, and finance, are increasingly embracing aspect computing to decorate operational efficiency, deliver low-latency services, and offer new sales streams. As a result, North America continues to drive considerable growth and funding within the global edge computing market, cementing its dominance in this market.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The global computing marketplace is highly competitive with major players including Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform (GCP) dominating by offering product catalogs with a wide range of products. These corporations provide complete computing solutions, consisting of AWS Wavelength, Azure Edge Zones, and Anthos, respectively.

Other significant competitors in this market encompass IBM, Cisco Systems, Dell Technologies, Hewlett Packard Enterprise (HPE), NVIDIA, Intel, and Huawei, where each of these companies present their computing structures and offerings tailor-made solutions to numerous industries. Startups and regional corporations in this market additionally make contributions to the competitive landscape with an area of interest services focused on precise facet computing use instances.

The marketplace is characterized by using ongoing innovation, partnerships, and strategic alliances to enhance aspect computing abilities and deal with evolving consumer needs. With the proliferation of Internet of Things (IoT) devices and the growing demand for low-latency processing, the competition within the global area computing marketplace is predicted to remain high as groups vie for market share and differentiation.

Some of the prominent players in the Global Edge Computing Market are

- ABB

- Amazon Web Services (AWS), Inc.

- Aricent, Inc.

- Atos

- Cisco Systems, Inc.

- General Electric Company

- Hewlett Packard Enterprise Development

- Honeywell International Inc.

- Huawei Technologies Co., Ltd.

- IBM Corporation

- Intel Corporation

- Microsoft Corporation

- Rockwell Automation, Inc

- SAP SE

- Other Key Players

Recent Development

- In February 2024, Synadia secured USD 25.0 million Series B funding led by Forgepoint Capital for NATS.io development, catering to edge AI and multi-cloud applications amidst the growing edge computing market.

- In January 2024, G42 invests in Analog, an edge computing startup focusing on AI solutions for human needs. Analog emphasizes partnership and innovation. Launch announced at Davos.

- In September 2023, T-Mobile Ventures launched a second fund to invest in AI and edge computing for the 5G network, aiming to enhance consumer products and business services.

- In August 2023, ABB invested in Pratexo, enhancing edge computing solutions for decentralized electrical networks. The partnership aims to improve security, autonomy, and resilience.

- In August 2023, OVHcloud is set to acquire German edge computing specialist grid-scale, aiming to enhance its presence in Europe and enter the rapidly growing edge computing market.

Report Details

| Report Characteristics |

| Market Size (2023) |

USD 33.9 Bn |

| Forecast Value (2032) |

USD 702.8 Bn |

| CAGR (2023-2032) |

40.0% |

| Historical Data |

2018 – 2023 |

| Forecast Data |

2024 – 2033 |

| Base Year |

2023 |

| Estimate Year |

2024 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Component (Hardware, Software, Services, and Edge-Managed Platform), By Organization Size (Large Enterprise, and Small & Medium Enterprise), By Application (Industrial Internet of Things (IIoT), Robotics and Automation, Remote Monitoring, Smart Cities, Video Analytics, AR/VR, and Others), By Industry Vertical (Energy and Utilities, Financial and Banking Industry, Retail, Healthcare and Life Sciences, Industrial, Telecommunications, and Others) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia- Pacific– China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

ABB, Amazon Web Services (AWS) Inc., Aricent Inc., Atos, Cisco Systems Inc., General Electric Company, Hewlett Packard Enterprise Development, Honeywell International Inc., Huawei Technologies Co. Ltd., IBM Corporation, Intel Corporation, Microsoft Corporation, Rockwell Automation Inc, SAP SE, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users), and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |