Market Overview

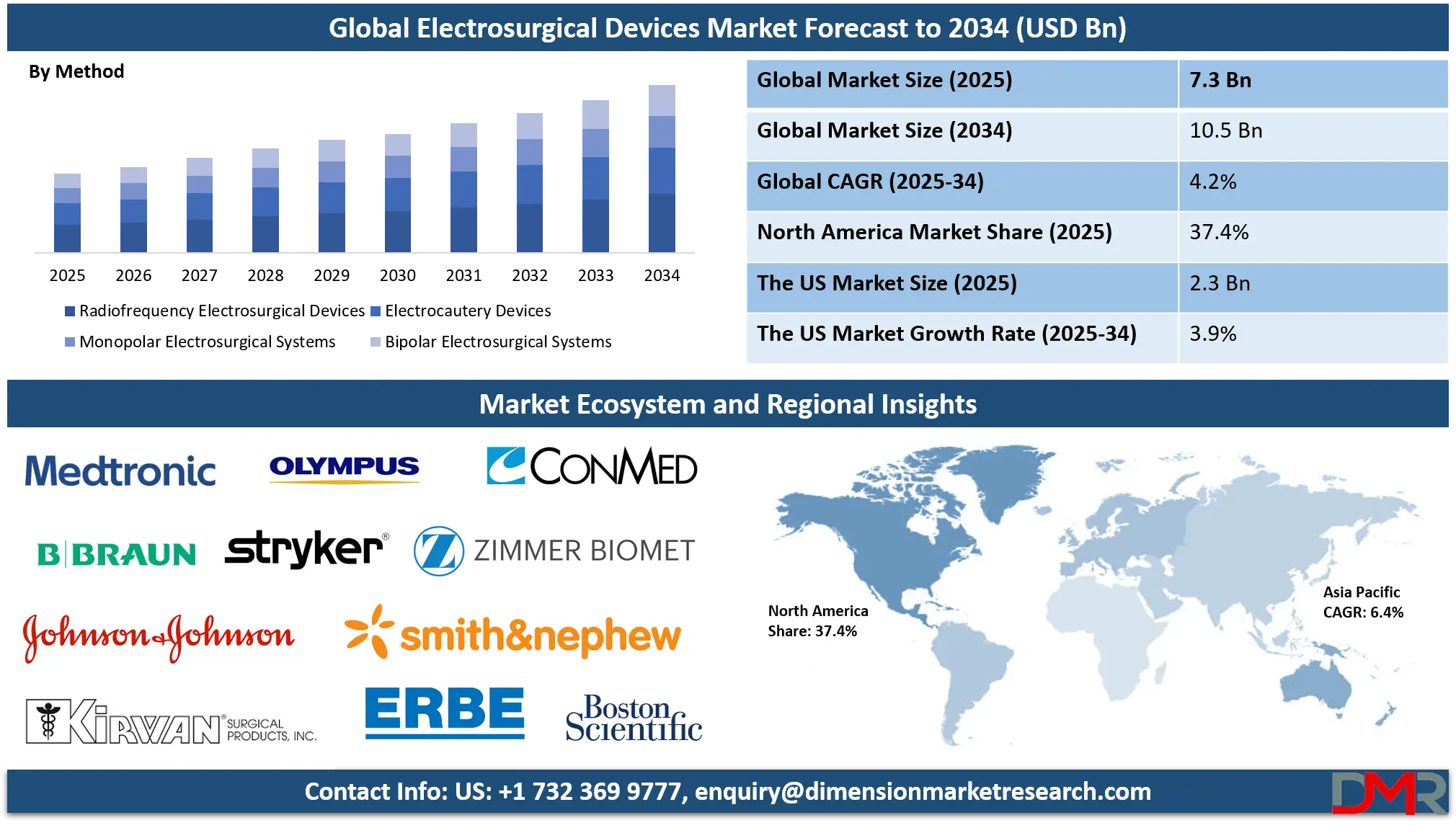

The Global Electrosurgical Devices Market is projected to reach USD 7.3 billion in 2025 and is expected to expand at a compound annual growth rate (CAGR) of 4.2% from 2025 to 2034, attaining a market value of approximately USD 10.5 billion by 2034.

The market growth is driven by the rising adoption of minimally invasive surgical procedures, increasing demand for advanced energy-based electrosurgical systems, and continuous technological innovations such as AI-assisted energy delivery, robotic-integrated electrosurgery, and real-time tissue sensing technologies. Additionally, the growing prevalence of chronic diseases, expanding hospital infrastructure, and increased utilization of electrocautery, bipolar, and ultrasonic surgical instruments are further propelling market expansion across hospitals, ambulatory surgical centers, and specialty clinics worldwide.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The global electrosurgical apparatus sector is experiencing a significant upswing, fueled by a confluence of technological progress and escalating surgical volumes. A dominant tendency is the pronounced shift towards minimally invasive surgical interventions, which heavily depend on advanced electrosurgical instruments for precise tissue dissection and hemostasis.

This movement is complemented by the integration of sophisticated technologies like radiofrequency and argon plasma coagulation, enhancing surgical safety and efficacy. The market is further energized by the development of versatile, multi-functional generators and a growing preference for bipolar instruments over traditional monopolar systems, which minimizes the risk of patient collateral injury and improves procedural outcomes in confined anatomical spaces.

Substantial growth prospects are emerging from the expanding healthcare infrastructure in developing economies across Asia-Pacific and Latin America. The rising medical tourism industry in these regions, coupled with increasing investments in modernizing hospital surgical suites, creates a fertile environment for market penetration.

Furthermore, the escalating global prevalence of chronic conditions necessitating surgical intervention, such as cardiovascular diseases, cancers, and gastrointestinal disorders, is propelling demand. The burgeoning field of aesthetic and cosmetic surgeries also presents a lucrative avenue for specialized electrosurgical tools, opening new revenue streams for manufacturers focused on this high-growth niche.

Despite the optimistic outlook, the market expansion faces certain impediments. A primary restraint is the high capital investment associated with advanced electrosurgical units and the recurring cost of disposable components, which can be prohibitive for smaller healthcare facilities in budget-constrained settings.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Additionally, the risk of electrosurgical-related complications, including burns at the return electrode site or unintended thermal damage to adjacent tissues, remains a clinical concern. This is compounded by stringent regulatory approval processes for new devices, which can delay product launches and innovation. The need for continuous professional training to ensure the safe application of these sophisticated devices also acts as a moderating factor on unchecked growth.

The US Electrosurgical Devices Market

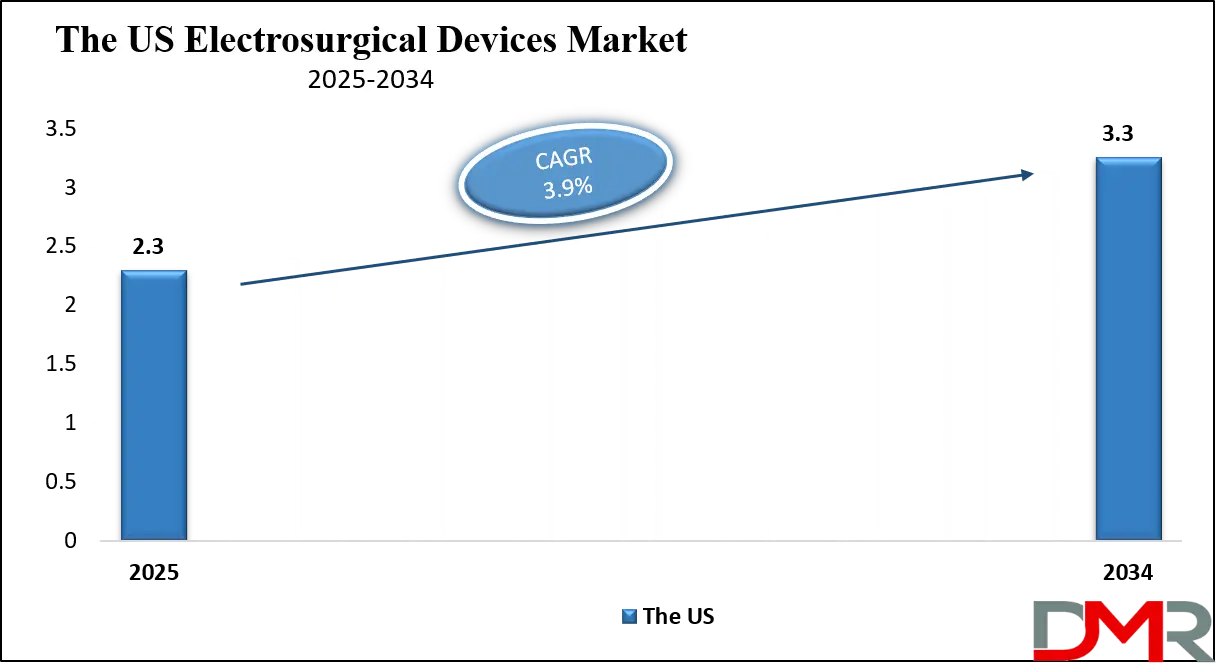

The US Electrosurgical Devices Market is projected to reach USD 2.3 billion in 2025 at a compound annual growth rate of 3.9% over its forecast period.

The United States represents the most significant national market for electrosurgical apparatus, driven by a sophisticated healthcare ecosystem and strong regulatory and demographic tailwinds. The Centers for Disease Control and Prevention (CDC) provides extensive data on public health burdens that directly influence surgical volumes.

For instance, the CDC's National Center for Health Statistics reports millions of inpatient and outpatient surgical and procedural visits annually, a substantial portion of which utilize electrosurgical technology for tasks ranging from tissue cutting to coagulation. This high procedural volume is a primary demand driver for both capital equipment and disposable instruments within the nation's hospitals and ambulatory surgical centers.

A key demographic advantage for the US market is the aging Baby Boomer population. Data from the US Census Bureau details that the population aged 65 and older is projected to expand considerably, a cohort that exhibits a higher prevalence of conditions like cancer, cardiovascular disease, and osteoarthritis, often requiring surgical intervention. This demographic shift ensures a sustained and growing patient pool for procedures dependent on electrosurgical devices.

Furthermore, federal agencies like the National Institutes of Health (NIH) invest billions of dollars annually in biomedical research, which fosters the development of next-generation surgical technologies, including advanced energy-based devices, ensuring the market remains at the forefront of innovation.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Europe Electrosurgical Devices Market

The Europe Electrosurgical Devices Market is estimated to be valued at USD 1,095 million in 2025 and is further anticipated to reach USD 1,568 million by 2034 at a CAGR of 4.0%.

The European market for electrosurgical instruments is characterized by its maturity, advanced healthcare infrastructure, and a regulatory framework guided by the stringent Medical Device Regulation (MDR). Demographic data from Eurostat, the statistical office of the European Union, highlights a pronounced and accelerating population aging trend across the continent. This demographic reality translates to a higher incidence of age-related diseases, such as malignancies and joint disorders, necessitating a greater number of surgical procedures. This creates a consistent, underlying demand for reliable and advanced electrosurgical equipment within both public and private healthcare systems throughout the European Union member states.

Government and pan-European bodies actively influence market dynamics. The European Centre for Disease Prevention and Control (ECDC) monitors healthcare-associated infections, pushing for technologies that improve patient safety, a box that modern electrosurgical systems tick by offering precise tissue management and reduced blood loss.

Moreover, initiatives from the European Commission aimed at harmonizing medical device standards and ensuring high levels of health and safety for citizens under the MDR shape product development and market entry. While this creates a high barrier for new devices, it ensures that approved products meet rigorous performance and safety benchmarks, reinforcing market stability and physician confidence in the technologies they adopt.

The Japan Electrosurgical Devices Market

The Japan Electrosurgical Devices Market is projected to be valued at USD 438 million in 2025. It is further expected to witness subsequent growth in the upcoming period, holding USD 627 million in 2034 at a CAGR of 4.2%.

Japan's electrosurgical devices sector is profoundly shaped by its status as the world's most aged society, a demographic characteristic meticulously documented by the Ministry of Internal Affairs and Communications. This super-aged demographic profile results in a high and growing prevalence of geriatric-associated medical conditions, including various forms of cancer, benign prostatic hyperplasia, and cardiovascular ailments, which are frequently managed through surgical means. Consequently, there is a persistent and robust demand for surgical interventions in the country's advanced healthcare institutions, directly fueling the need for sophisticated electrosurgical apparatus for both open and minimally invasive procedures.

National government initiatives and data from organizations like the Japan Medical Association further solidify the market's foundation. The Ministry of Health, Labour and Welfare (MHLW) oversees a universal health insurance system that provides broad coverage for surgical care, ensuring patient access to advanced medical technologies.

Furthermore, the MHLW's focus on advancing "state-of-the-art medical care" and approving new medical devices and techniques encourages the adoption of innovative electrosurgical technologies. This combination of a demographic imperative that guarantees a large patient base and a supportive, well-regulated healthcare system creates a stable and technologically advanced environment for the growth and utilization of electrosurgical devices in Japan.

Global Electrosurgical Devices Market: Key Takeaways

- Global Market Size Insights: The Global Electrosurgical Devices Market size is estimated to have a value of USD 7.3 billion in 2025 and is expected to reach USD 10.5 billion by the end of 2034.

- The Global Market Growth Rate: The market is growing at a CAGR of 4.2% over the forecasted period of 2025.

- The US Market Size Insights: The US Electrosurgical Devices Market is projected to be valued at USD 2.3 billion in 2025. It is expected to witness subsequent growth in the upcoming period as it holds USD 3.3 billion in 2034 at a CAGR of 3.9%.

- Regional Insights: North America is expected to have the largest market share in the Global Electrosurgical Devices Market with a share of about 37.4% in 2025.

- Key Players: Some of the major key players in the Global Electrosurgical Devices Market are Medtronic plc, Johnson & Johnson (Ethicon Inc.), Olympus Corporation, B. Braun Melsungen AG, Boston Scientific Corporation, CONMED Corporation, and many others.

Global Electrosurgical Devices Market: Use Cases

- Laparoscopic Cholecystectomy: Bipolar electrosurgical instruments are indispensable for precise gallbladder dissection and vessel sealing during this common minimally invasive abdominal procedure, minimizing bleeding and enhancing patient recovery.

- Transurethral Resection of the Prostate (TURP): A monopolar electrosurgical loop is used to meticulously remove obstructive prostate tissue through the urethra, providing relief from urinary symptoms with minimal invasion.

- Dermatological Lesion Excision: Electrosurgery offers dermatologists a versatile tool for shave biopsies, fulguration of benign growths, and electrodesiccation, allowing for controlled tissue removal and excellent cosmetic outcomes.

- Orthopedic Joint Replacement: Electrosurgical pencils are routinely used for cutting soft tissues and achieving hemostasis in highly vascularized areas during major joint arthroplasty, improving surgical field visibility.

- Oncological Tumor Ablation: Advanced radiofrequency ablation probes utilize electrosurgical energy to destroy malignant liver, kidney, and lung tumors percutaneously, offering a less invasive alternative to traditional surgery for selected patients.

Global Electrosurgical Devices Market: Stats & Facts

Centers for Disease Control and Prevention (CDC) / National Center for Health Statistics

- In a recent year, an estimated 48.3 million inpatient surgical and medical procedures were performed in the United States.

- Approximately 15.1 million ambulatory and outpatient surgical procedures were conducted in a recent reporting period.

- Diseases of the circulatory system accounted for nearly 4 million inpatient procedures.

- Digestive system procedures represented over 5 million inpatient interventions.

- Musculoskeletal system procedures, including joint replacements, totaled over 6 million inpatient cases.

World Health Organization (WHO)

- Cancer is a leading cause of death worldwide, accounting for nearly 10 million deaths in 2020.

- The global incidence of cancer is projected to rise by over 60% by 2040.

- An estimated 17.9 million people died from cardiovascular diseases in 2019, representing 32% of all global deaths.

- The number of people aged 60 years and older will outnumber children under 10 by 2030.

- Surgical conditions account for an estimated 30% of the global burden of disease.

Eurostat

- Over 20% of the European Union's population was aged 65 and older in 2021.

- This proportion is projected to increase to nearly 30% by 2100.

- Cancer accounted for over 1.2 million deaths in the EU in a recent year.

- Diseases of the circulatory system were responsible for approximately 1.7 million deaths in the EU.

- There were over 5 million employed health professionals in the EU, supporting surgical care delivery.

National Institutes of Health (NIH)

- The NIH budget for the fiscal year 2023 was over USD 45 billion.

- The National Cancer Institute (NCI) received approximately USD 6.9 billion in funding.

- The National Heart, Lung, and Blood Institute (NHLBI) received over USD 3.8 billion in funding.

- NIH funding has contributed to a 29% decline in the cancer death rate since the early 1990s.

- NIH research supports the development of hundreds of thousands of new medical technologies.

Ministry of Health, Labour and Welfare (Japan)

- Japan has the highest proportion of elderly citizens in the world, with over 28% of its population aged 65 or older.

- The national medical care expenditure in Japan was approximately 44 trillion yen in a recent fiscal year.

- Cancer remains the leading cause of death in Japan.

- The number of patients with lifestyle-related diseases like diabetes and hypertension remains high, often requiring surgical care for complications.

- The number of approved advanced medical technologies, including new surgical methods, continues to grow annually.

U.S. Census Bureau

- The U.S. population aged 65 and over numbered 56 million in 2020.

- By 2030, all baby boomers will be older than age 65, expanding the size of the older population.

- One in every five residents will be of retirement age by 2030.

- The number of Americans aged 65+ is projected to reach over 80 million by 2040.

- The 85+ population is projected to more than double from 6.6 million in 2020 to 14.4 million in 2040.

American Cancer Society

- The lifetime probability of being diagnosed with an invasive cancer is slightly higher for men than for women.

- The overall cancer death rate has continued to decline since the 1990s.

Global Electrosurgical Devices Market: Market Dynamic

Driving Factors in the Global Electrosurgical Devices Market

Escalating Global Burden of Chronic Diseases

The most powerful driver for the electrosurgical devices market is the relentless increase in the global prevalence of chronic conditions that necessitate surgical intervention. According to the World Health Organization, cancer and cardiovascular diseases remain leading causes of mortality worldwide, with patient numbers steadily rising. These diseases often require surgical procedures for diagnosis, treatment, or palliation, directly fueling the volume of surgeries performed.

Electrosurgical devices are fundamental tools in oncological resections, cardiovascular procedures, and other interventions, making their utilization inextricably linked to the disease burden. This creates a consistent and growing baseline demand for these devices across both developed and developing healthcare systems, as they are essential for managing the complications and primary treatments of these widespread ailments.

Demographic Shift Towards an Aging Population

A powerful and irreversible demographic driver is the global trend of population aging, meticulously documented by sources like the U.S. Census Bureau and Eurostat. Older adults have a significantly higher susceptibility to a wide range of age-related ailments, including osteoarthritis requiring joint replacement, cataracts needing extraction, and various cancers and cardiovascular conditions.

This demographic segment undergoes surgical procedures at a much higher rate than younger cohorts. As the proportion of elderly individuals in the global population expands, it creates a predictable and sustained increase in the surgical volume, which in turn generates continuous demand for the electrosurgical instruments that are staples in operating rooms for these procedures, ensuring long-term market growth.

Restraints in the Global Electrosurgical Devices Market

High Costs and Budgetary Pressures in Healthcare

A primary factor restraining market growth is the significant capital investment required for advanced electrosurgical generator consoles and the recurring expense of proprietary disposable instruments and accessories. This high cost can be a substantial barrier to adoption for smaller hospitals, clinics, and facilities in developing nations with constrained capital equipment budgets.

Furthermore, global healthcare systems are universally facing intense pressure to control and reduce overall expenditure. This environment encourages procurement departments to prioritize cost-saving measures, such as extending the life of existing equipment or opting for less expensive, sometimes refurbished, alternatives, which can slow the replacement cycle and dampen the adoption rates of newer, more expensive innovative technologies.

Risks of Complications and Stringent Regulatory Hurdles

Despite technological advancements, the risk of electrosurgery-related adverse events, such as return electrode burns, direct coupling injuries to adjacent tissues, and surgical smoke inhalation, remains a clinical concern. These potential complications necessitate comprehensive and ongoing surgeon and staff training, which adds to the total cost of ownership and can deter some facilities from upgrading.

Concurrently, the regulatory landscape for medical devices has become increasingly rigorous globally, exemplified by the European Union's Medical Device Regulation. The lengthy and costly processes for obtaining and maintaining regulatory approvals can delay product launches, increase development expenses, and act as a significant barrier to market entry for smaller innovators, thereby restraining the pace of overall market innovation and expansion.

Opportunities in the Global Electrosurgical Devices Market

Expansion in Emerging Economies

The most significant growth frontier lies in the emerging economies of Asia-Pacific, Latin America, and the Middle East. These regions are experiencing rapid economic development, leading to increased healthcare spending, expansion of private hospital chains, and government initiatives to modernize public health infrastructure. This includes building new surgical suites and equipping them with modern medical technology.

The large, underserved patient populations in these regions, combined with a growing medical tourism industry, present a massive untapped market for electrosurgical device manufacturers. Tailoring product offerings to be cost-effective and robust for these diverse healthcare settings, along with strategic local partnerships, can unlock substantial new revenue streams and drive the next phase of global market expansion.

Proliferation of Ambulatory Surgical Centers (ASCs)

There is a pronounced and persistent shift of surgical procedures from traditional inpatient hospital settings to outpatient or ambulatory surgical centers, particularly in North America and Europe. This migration is driven by the pursuit of cost-efficiency, faster patient turnover, and patient preference for convenient care.

ASCs require reliable, user-friendly, and often compact electrosurgical generators and disposable instruments to perform a high volume of same-day procedures in specialties like orthopedics, gastroenterology, and ophthalmology. This creates a dedicated and growing segment of the market with specific needs, offering a prime opportunity for manufacturers to develop and market ASC-specific electrosurgical portfolios and service contracts.

Trends in the Global Electrosurgical Devices Market

Integration with Advanced Energy Platforms and Robotics

The market is witnessing a significant convergence of electrosurgical technology with other advanced energy modalities, such as ultrasonic and advanced bipolar vessel sealing, into single, multi-functional generator platforms. This integration provides surgeons with a versatile arsenal of tools for diverse tissue types and surgical steps from a single console, enhancing procedural efficiency and operational workflow in the operating room.

Furthermore, there is a growing synergy between electrosurgical instruments and robotic-assisted surgical systems. These sophisticated platforms are increasingly being designed with proprietary electrosurgical tools that offer enhanced articulation, tremor filtration, and seamless energy delivery, controlled precisely by the surgeon from the console, thereby expanding the capabilities of minimally invasive surgery for complex oncological and reconstructive procedures.

Rise of Value-Based Healthcare and Focus on Patient Safety

A dominant trend shaping product development and procurement is the shift towards value-based healthcare models, which prioritize patient outcomes and total cost of care over simple device acquisition costs. This paradigm is driving demand for electrosurgical devices that demonstrably reduce complication rates, such as surgical site infections, unintended thermal injuries, and excessive blood loss.

Manufacturers are responding by innovating in areas like smoke evacuation systems integrated with the electrosurgical pencil to protect staff and patients from potentially hazardous plume, and by developing intelligent tissue sensing technology that automatically adjusts energy output to minimize collateral damage, thereby improving overall surgical safety profiles and contributing to better value.

Global Electrosurgical Devices Market: Research Scope and Analysis

By Product Analysis

Within the product segment, dominance is split between the foundational, high-volume consumables and the technologically advanced systems driving innovation. Electrodes, Tips & Consumables is projected to represent the undisputed volume leader in terms of pure unit sales and recurring revenue.

These components, including cutting loops, coagulation electrodes, and dispersive return electrodes, are single-use by design to ensure sterility and optimal performance. With millions of surgical procedures performed annually globally, the demand for these disposable items is relentless and non-cyclical, creating a stable and massive revenue stream for manufacturers. This segment's dominance is fueled by the sheer necessity of replenishment for every procedure, making it the engine of the market's day-to-day financial activity.

However, in terms of strategic value and growth potential, Energy-based Advanced Vessel Sealing Devices are increasingly dominating the innovation landscape and capturing value in high-margin niches. While standard bipolar and monopolar instruments are essential, these advanced devices utilize sophisticated algorithms to consistently seal blood vessels and tissue bundles with high burst strength, significantly reducing bleeding in complex surgeries like oncology and gynecology.

Their ability to replace mechanical ligatures like clips and sutures in many instances drives their adoption by improving operative efficiency and outcomes. Consequently, while consumables lead in volume, advanced energy devices are commanding premium prices and are central to competitive differentiation, making them a dominant force in shaping the market's future trajectory and technological evolution.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Method

The dominance in the method segment is a tale of entrenched incumbency versus a powerful shift towards modern surgical safety standards. Monopolar Electrosurgical Systems is anticipated to currently hold a dominant position in terms of the global installed base and their utilization in a vast array of open and minimally invasive procedures. This dominance stems from their historical precedence, exceptional cutting efficiency, and versatility for a wide range of tissue types.

They are the fundamental, widely understood tool for general surgeons, deeply embedded in surgical protocols worldwide. The extensive familiarity with monopolar techniques and the lower initial cost of the instruments ensure their continued, prevalent use, particularly in general surgery and in cost-sensitive healthcare environments.

Simultaneously, Bipolar Electrosurgical Systems are the dominant force in terms of growth momentum and are the preferred choice for an expanding range of modern surgeries. Their key advantage is safety; the electrical current flows only between the tips of the instrument, eliminating the need for a patient return electrode and drastically reducing the risk of alternate-site burns.

This makes them indispensable for procedures in sensitive, confined, or fluid-filled anatomical areas, such as in neurosurgery, otolaryngology, and laparoscopic gynecological surgery. As the global surgical trend overwhelmingly shifts towards minimally invasive techniques, the inherent safety and precision of bipolar systems have made them the dominant and often mandatory method for these advanced procedures, positioning them to eventually supersede monopolar systems in many applications.

By Application

The application segment is expected to led by the field that encompasses the broadest and most frequent surgical needs. General Surgery is the dominant application area for electrosurgical devices, a status driven by the immense and diverse volume of procedures it performs. This specialty includes a vast spectrum of interventions, from routine hernia repairs and cholecystectomies to complex laparotomies and oncological resections of the digestive system.

In nearly all these procedures, electrosurgical instruments are the primary tools for making incisions, dissecting tissue, and achieving hemostasis. The sheer universality and indispensability of electrosurgery across this wide procedural portfolio, coupled with the high global incidence of conditions requiring general surgical intervention, cement its position as the largest and most dominant application segment by a significant margin.

A highly significant and rapidly advancing segment is Oncology Surgery, which, while sometimes categorized under general or specialty surgery, deserves recognition as a dominant driver of innovation and complex device utilization. Cancer resections demand extreme precision, meticulous hemostasis in highly vascularized tissues, and the ability to operate in confined spaces near critical structures.

This makes advanced bipolar and vessel sealing devices absolutely critical. The escalating global cancer burden, as documented by the World Health Organization, ensures a growing volume of these technically demanding procedures. The need for optimal outcomes in oncology pushes the adoption of the most sophisticated energy-based devices, making this application a dominant force in driving the development and procurement of high-value, advanced electrosurgical platforms.

By End User

The end-user landscape is unequivocally is poised to dominated by centralized healthcare institutions that handle the bulk of surgical care. Hospitals, encompassing both public and private entities, are the dominant consumers of electrosurgical devices. This dominance is rooted in their role as the primary hubs for inpatient and complex surgical care.

Hospitals house the majority of operating rooms, perform the widest range of procedures from emergency trauma surgery to scheduled major oncological resections and have the infrastructure and capital budgets to invest in multiple, high-end electrosurgical generator consoles and large inventories of instruments. Their high patient throughput and central role in healthcare systems make them the most critical customer segment for market players, accounting for the largest share of both capital equipment and disposable sales.

The segment exhibiting the most rapid growth and increasingly influencing device design and procurement is Ambulatory Surgical Centers (ASCs) and Outpatient Facilities. This segment's growing influence is driven by the global healthcare policy shift towards moving appropriate procedures out of expensive hospital settings.

ASCs specialize in same-day surgeries that do not require overnight hospitalization, creating a high-volume, efficiency-focused environment. For electrosurgical device manufacturers, this has spawned a dominant and specific demand for reliable, user-friendly, and cost-effective generators and disposables tailored for high-turnover workflows in specialties like orthopedics, pain management, and gastroenterology. The proliferation of ASCs makes them a dominant force in shaping product development for the outpatient market and a key growth engine for the industry.

The Global Electrosurgical Devices Market Report is segmented on the basis of the following:

By Product

- Electrodes, Tips & Consumables

- Disposable Electrodes

- Reusable Electrodes and Tips

- Electrodes for Laparoscopic and Endoscopic Procedures

- Energy-based Advanced Devices

- Ultrasonic (Harmonic) Devices

- Bipolar Vessel Sealing Systems

- Radiofrequency Ablation Devices

- Electrosurgical Generators

- Monopolar Generators

- Bipolar Generators

- Multi-Mode / Advanced Energy Generators

- Electrosurgical Instruments

- Monopolar Handpieces

- Bipolar Forceps

- Vessel Sealers

- Electrocautery Pencils

- Accessories & Support Equipment

- Footswitches

- Cables and Connectors

- Smoke Evacuators and Filters

- Return Pads (Grounding Pads)

By Method

- Radiofrequency Electrosurgical Devices

- Electrocautery Devices

- Monopolar Electrosurgical Systems

- Bipolar Electrosurgical Systems

By Application

- General Surgery

- Gynecology

- Urology

- Orthopedic & Cardiovascular

- Other Application

By End User

- Hospitals (Public & Private)

- Ambulatory Surgical Centers (ASCs) / Outpatient Facilities

- Clinics & Specialty Centers

- Diagnostic & Research Centers

- Home Healthcare

Impact of Artificial Intelligence in the Global Electrosurgical Devices Market

- Enhanced Surgical Precision: AI-powered electrosurgical devices can analyze real-time tissue feedback, automatically adjusting energy delivery to minimize thermal damage, improve accuracy, and reduce post-operative complications.

- Integration with Robotic Surgery Systems: Artificial Intelligence enables electrosurgical tools to seamlessly integrate with robotic-assisted surgical platforms, enhancing minimally invasive procedures and enabling predictive motion control for better outcomes.

- Predictive Maintenance and Device Monitoring: AI algorithms can monitor device performance, predict component wear, and schedule maintenance proactively, reducing downtime in hospitals and ensuring operational efficiency.

- Data-Driven Clinical Decision Support: By analyzing historical surgical data, AI can provide recommendations for energy settings, instrument selection, and procedural workflow optimization, assisting surgeons in complex or high-risk procedures.

- Personalized and Adaptive Energy Delivery: AI allows devices to adapt energy modes based on patient-specific factors (e.g., tissue type, vascular density), leading to more personalized surgery and improved safety for diverse patient populations.

Global Electrosurgical Devices Market: Regional Analysis

Region with the Largest Revenue Share

North America, led by the United States, is projected to commands the 37.4% of the global market share by the end of 2025 for electrosurgical apparatus, a position solidified by a confluence of economic, technological, and regulatory factors. The region possesses a highly developed and well-funded healthcare infrastructure, with significant hospital and ambulatory surgical center (ASC) spending on advanced medical technologies.

This financial capacity allows for the rapid adoption of premium-priced, innovative devices, including integrated electrosurgical generators and advanced bipolar energy platforms. Furthermore, the presence of a robust regulatory framework through the U.S. Food and Drug Administration (FDA), while stringent, provides a clear pathway for commercialization and fosters physician confidence in the safety and efficacy of approved devices, creating a stable environment for market leaders.

The demographic and disease profile of the region further entrenches its dominance. A high and growing prevalence of chronic conditions such as cancer, cardiovascular diseases, and obesity, detailed by sources like the CDC and NIH, drives an immense volume of surgical procedures annually.

This established patient base creates consistent, high demand for electrosurgical instruments. Compounding this is the early and widespread adoption of minimally invasive surgical techniques and robotic-assisted surgery, which are heavily dependent on sophisticated electrosurgical tools for precision. Coupled with the presence of major global market players within the region who drive intensive research, development, and marketing, these elements create a self-reinforcing cycle of innovation and utilization that is difficult for other regions to match in scale.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Region with the Highest CAGR

The Asia Pacific region is projected to exhibit the highest Compound Annual Growth Rate (CAGR) in the electrosurgical devices market, fueled by transformative economic expansion and healthcare modernization. Nations including China, India, South Korea, and those in Southeast Asia are experiencing rapid increases in healthcare expenditure, enabling massive investments in upgrading public and private hospital infrastructure.

This includes equipping new operating rooms with modern surgical technologies, creating a vast new addressable market for both basic and advanced electrosurgical units. Government initiatives aimed at achieving universal health coverage and improving access to surgical care are pivotal, directly stimulating domestic demand for medical devices that were previously underutilized.

A powerful demographic tailwind and a growing medical tourism industry further accelerate this growth. The region contains a massive population with a rising middle class that can increasingly afford private healthcare and demands higher-quality surgical interventions. Simultaneously, the prevalence of lifestyle-related diseases requiring surgery is escalating.

To capture this potential, both international corporations and burgeoning local manufacturers are intensifying their focus on the region, often tailoring products to be cost-effective for local markets. This strategic focus, combined with the establishment of local manufacturing, improves affordability and availability. The convergence of a large underserved patient population now gaining access to care, government support, and strategic market investments creates an exceptionally fertile ground for exponential market growth unmatched by more mature regions.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Global Electrosurgical Devices Market: Competitive Landscape

The global electrosurgical devices market is characterized by a high degree of fragmentation and intense competition, featuring a mix of well-established multinational medtech giants and agile specialized players. Dominant entities, including Medtronic plc, Johnson & Johnson (Ethicon Inc.), and Becton, Dickinson and Company (BD), maintain their leadership through extensive product portfolios that span from basic electrosurgical generators to advanced vessel sealing platforms.

Their strength lies in robust global distribution networks, significant investment in research and development for technological innovation, and strong brand loyalty built over decades. These industry titans often compete by integrating electrosurgery into broader digital surgery and robotic platforms, creating ecosystem lock-in that secures long-term contracts with large hospital systems.

The competitive dynamics are further shaped by the presence of strong second-tier players, such as B. Braun Melsungen AG, Olympus Corporation, and CONMED Corporation, who compete effectively in specific regional markets or clinical niches like minimally invasive or endoscopic surgery. The landscape also includes numerous smaller and regional manufacturers that often compete on price, particularly in cost-sensitive emerging markets, by offering reliable generics and disposables.

This intense rivalry compels all participants to continuously innovate, focusing on enhancing surgical outcomes, improving user ergonomics, and reducing overall procedural costs. Key competitive strategies observed include aggressive portfolio diversification, strategic mergers and acquisitions to acquire novel technology, and a heightened focus on providing value-based solutions and comprehensive service contracts to key end-users like Ambulatory Surgical Centers.

Some of the prominent players in the Global Electrosurgical Devices Market are:

- Medtronic plc

- Johnson & Johnson (Ethicon Inc.)

- Olympus Corporation

- B. Braun Melsungen AG

- Boston Scientific Corporation

- CONMED Corporation

- Erbe Elektromedizin GmbH

- Stryker Corporation

- Smith & Nephew plc

- Zimmer Biomet Holdings, Inc.

- Kirwan Surgical Products LLC

- Apyx Medical Corporation

- Bovie Medical Corporation

- CooperSurgical, Inc.

- KLS Martin Group

- Utah Medical Products, Inc.

- Meyer-Haake GmbH

- Karl Storz SE & Co. KG

- Ellman International (part of Cynosure LLC

- XcelLance Medical Technologies Pvt. Ltd

- Other Key Players

Recent Developments in the Global Electrosurgical Devices Market

- May 2024: Becton, Dickinson and Company (BD) announces a strategic collaboration with a leading academic medical center to co-develop next-generation intelligent energy algorithms for its advanced vessel sealing devices.

- March 2024: Medtronic plc receives U.S. FDA clearance for the latest software upgrade to its Valleylab FT10 Energy Platform, introducing new tissue sensing features for general surgery procedures.

- October 2023: Johnson & Johnson's Ethicon division showcases its next-generation bipolar dissection and vessel sealing device, the ENSEAL X1, at the American College of Surgeons Clinical Congress.

- July 2023: B. Braun Melsungen AG acquires a minority stake in a start-up specializing in pulsed electron ablation technology, aiming to expand its oncology surgery portfolio.

- April 2023: The International Society for Electrosurgery & Energy Devices (ISEED) holds its annual symposium in Munich, Germany, featuring keynotes on the integration of energy devices with robotic surgical systems.

- November 2022: CONMED Corporation completes the acquisition of In2Bones Global, Inc., a move that significantly expands its portfolio in extremities surgery, complementing its existing electrosurgical offerings for orthopedics.

- September 2022: Olympus Corporation launches its new "Gymny" 3-mm electrosurgical resection electrode in European markets for advanced urological procedures.

- June 2022: A major strategic partnership is formed between AngioDynamics and a distribution partner to expand the market reach of its NanoKnife ablation system in the Asia Pacific region.

Report Details

| Report Characteristics |

| Market Size (2025) |

USD 7.3 Bn |

| Forecast Value (2034) |

USD 10.5 Bn |

| CAGR (2025–2034) |

4.2% |

| The US Market Size (2025) |

USD 2.3 Bn |

| Historical Data |

2019 – 2024 |

| Forecast Data |

2026 – 2034 |

| Base Year |

2024 |

| Estimate Year |

2025 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors, etc. |

| Segments Covered |

By Product (Electrosurgical Generators, Electrosurgical Instruments, Energy-based Advanced Devices, Electrodes, Tips & Consumables, Accessories & Support Equipment), By Method (Radiofrequency Electrosurgical Devices, Electrocautery Devices, Monopolar Electrosurgical Systems, Bipolar Electrosurgical Systems), By Application (General Surgery, Gynecology, Urology, Orthopedic & Cardiovascular, Other Applications), By End User (Hospitals (Public & Private), Ambulatory Surgical Centers (ASCs) / Outpatient Facilities, Clinics & Specialty Centers, Diagnostic & Research Centers, Home Healthcare)

|

| Regional Coverage |

North America – US, Canada; Europe – Germany, UK, France, Russia, Spain, Italy, Benelux, Nordic, Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, Rest of MEA |

| Prominent Players |

Medtronic plc, Johnson & Johnson (Ethicon Inc.), Olympus Corporation, B. Braun Melsungen AG, Boston Scientific Corporation, CONMED Corporation, Erbe Elektromedizin GmbH, Stryker Corporation, Smith & Nephew plc, Zimmer Biomet Holdings Inc., Kirwan Surgical Products LLC, Apyx Medical Corporation, Bovie Medical Corporation, CooperSurgical Inc., KLS Martin Group, Utah Medical Products Inc., Meyer-Haake GmbH, Karl Storz SE & Co. KG, Ellman International (Cynosure LLC), XcelLance Medical Technologies Pvt. Ltd., and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users), and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days, and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Electrosurgical Devices Market?

▾ The Global Electrosurgical Devices Market size is estimated to have a value of USD 7.3 billion in 2025 and is expected to reach USD 10.5 billion by the end of 2034.

What is the growth rate in the Global Electrosurgical Devices Market in 2025?

▾ The market is growing at a CAGR of 4.2 percent over the forecasted period of 2025.

What is the size of the US Electrosurgical Devices Market?

▾ The US Electrosurgical Devices Market is projected to be valued at USD 2.3 billion in 2025. It is expected to witness subsequent growth in the upcoming period as it holds USD 3.3 billion in 2034 at a CAGR of 3.9%.

Which region accounted for the largest Global Electrosurgical Devices Market?

▾ North America is expected to have the largest market share in the Global Electrosurgical Devices Market with a share of about 37.4% in 2025.

Who are the key players in the Global Electrosurgical Devices Market?

▾ Some of the major key players in the Global Electrosurgical Devices Market are Medtronic plc, Johnson & Johnson (Ethicon Inc.), Olympus Corporation, B. Braun Melsungen AG, Boston Scientific Corporation, CONMED Corporation, and many others.