What is the Global Energy Drinks Market Size?

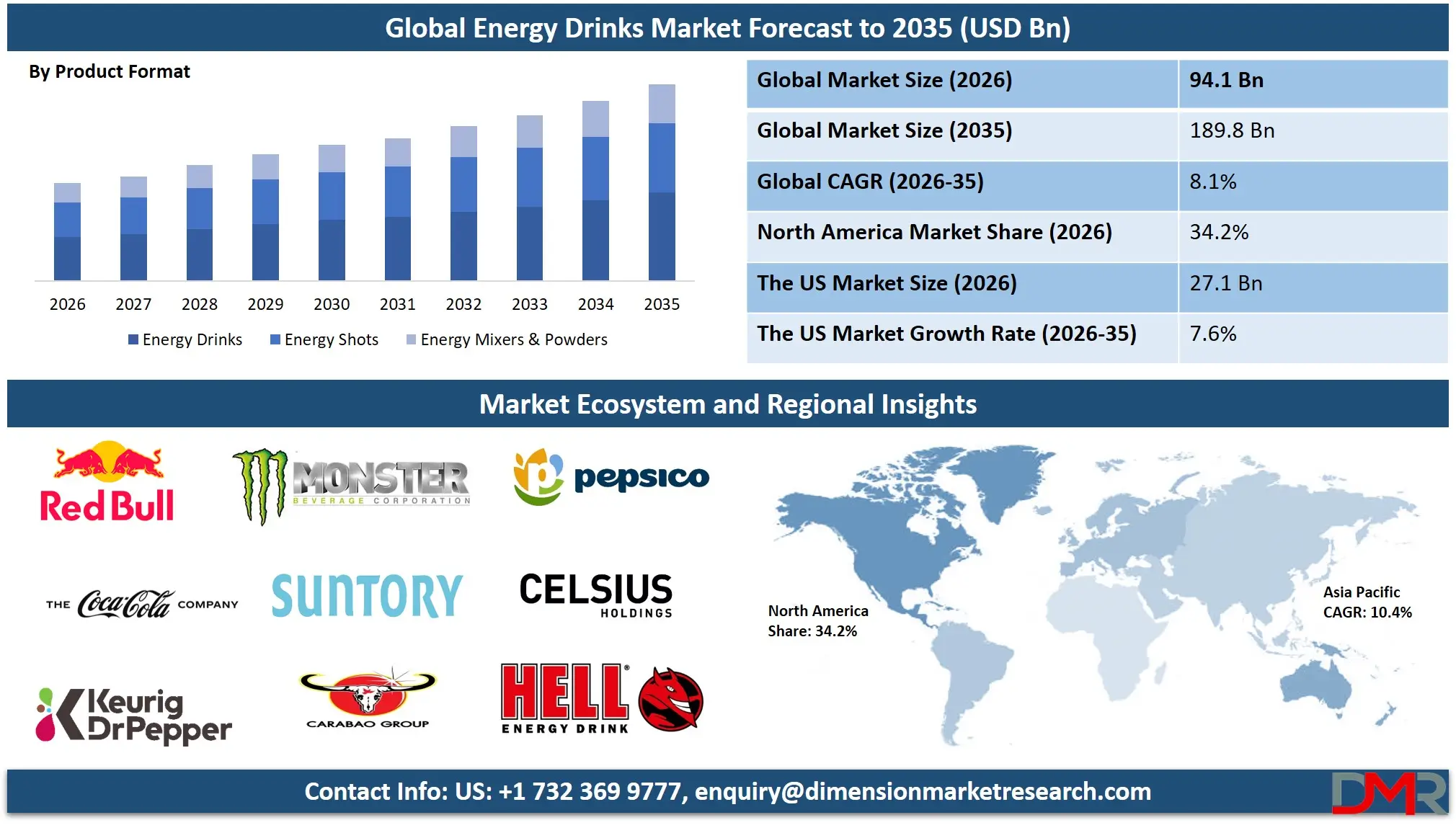

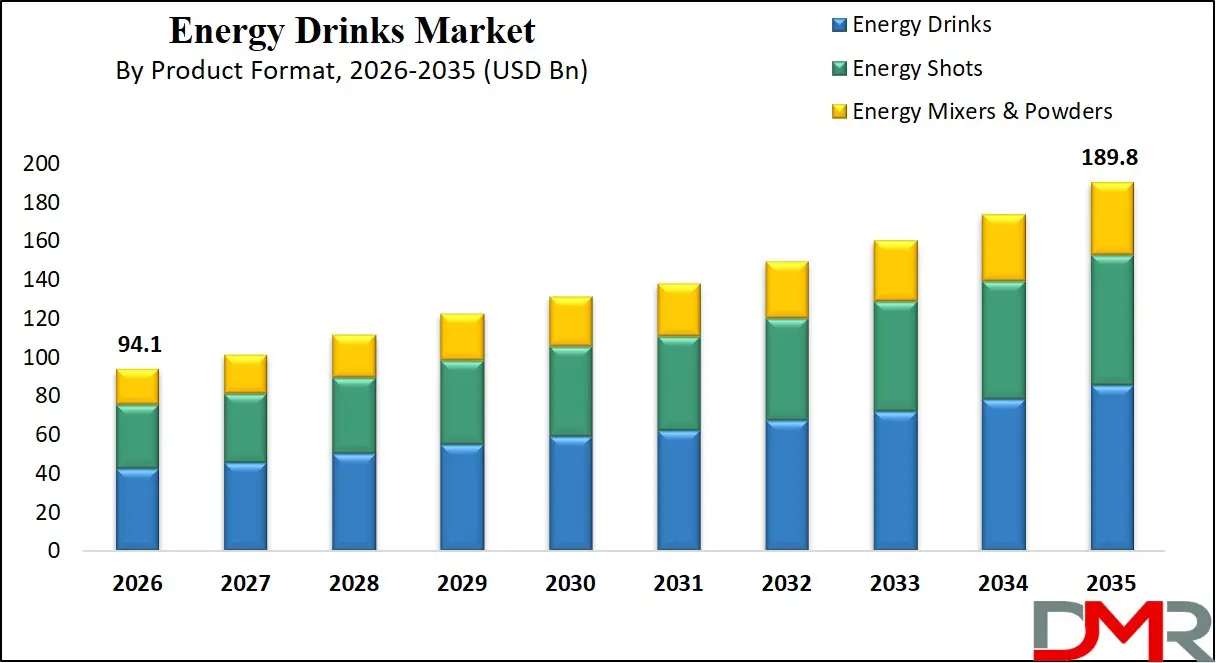

The Global Energy Drinks Market size is expected at USD 94.1 billion in 2026 and is projected to reach USD 189.8 billion by 2035, growing at a CAGR of 8.1% during the forecast period, driven by functional ingredient innovation, clean-label trends, and expanding distribution and retail integration in beverage operations.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The growth in the Global Energy Drinks market is driven by the increase in the formulation of energy drinks to offer energy and concentration, the increased emphasis from regulators in relation to packaging and labeling statements, and accelerated time to market in terms of launching new products. This is coupled with investments by private organizations in the manufacturing and distribution of products. Others are improvements in inventory management systems, sales and demand forecasting, sales maximization, product innovation, among others, which are contributing to the growth of energy drinks.

The digitization of marketing, sales, and distribution has been helping in the optimization of product offerings and processes such as time to shelf. Moreover, an increase in the consumption of energy drinks among young adults and fitness enthusiasts, alongside the increasing demand for portable beverages, has been aiding in market growth.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

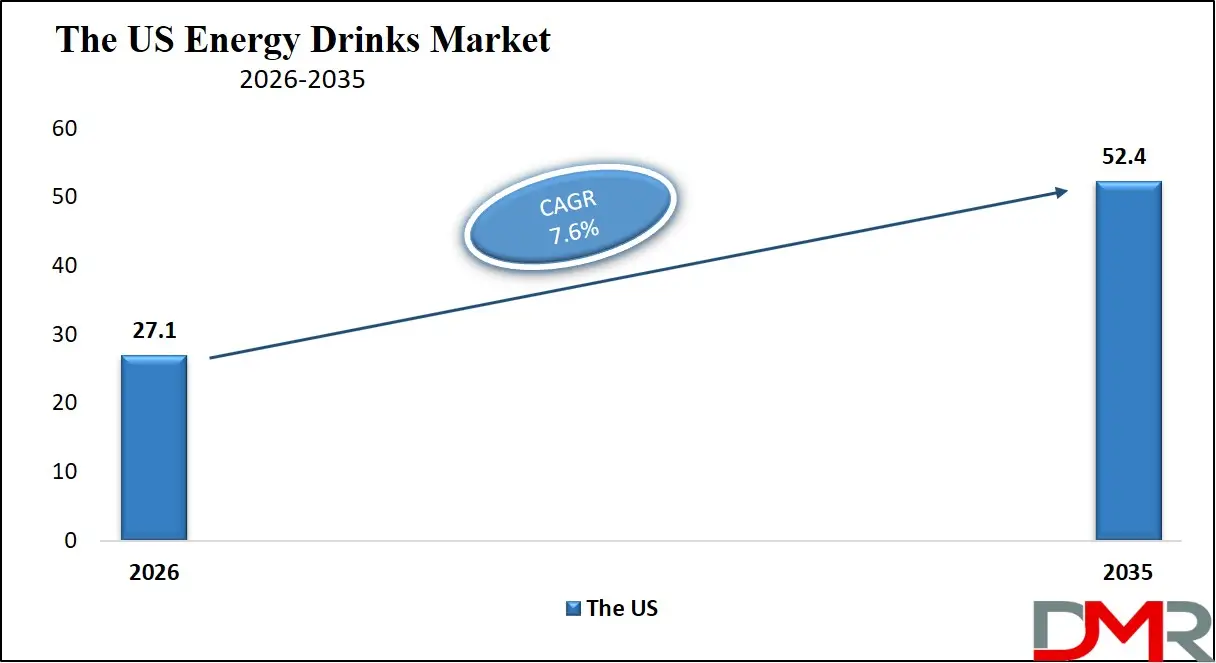

The US Energy Drinks Market

The US Energy Drinks Market is estimated to grow to USD 27.1 billion in 2026 with a compound annual growth rate of 7.6% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US market is defined by the existence of significant federal digital transformation schemes like the National AI in Beverage Initiative, the FDA's modernized dietary supplement and beverage guidance, and USDA-supported AI/ML-enabled compliance pathways for functional drinks and sports nutrition products, all of which will help the development of AI-driven flavor intelligence, real-time inventory tracking of automated distribution workflows, and predictive energy drink software. Automated energy drink management systems continue to be more rapidly adopted in the region, and the US needs highly developed interoperability frameworks, integration of real-world consumption data using sales repositories and energy drink analytics, and verifiable AI assurance for regulatory compliance. Also, service providers are being pressured by initiatives like the National Strategic Reserve for critical ingredients and national AI in digital commerce strategies to create dedicated integration and deployment services to guarantee data interoperability, safety, and compliance across a variety of marketing departments, sales operations, and distribution teams.

Europe Energy Drinks Market

The Europe Energy Drinks Market is estimated to be valued at USD 24.9 billion in 2026, witnessing growth at a CAGR of 5.9%, during the forecast period.

The Energy Drinks Market is mature in Europe, and it has a strong effect on the regulatory specifications and regional policies including the EU Farm to Fork Strategy, the European Blockchain and Data Infrastructure initiatives, and national digital transformation programs (e.g., France Numérique and Germany's Digitalwirtschaft 2030 strategy). Another area that countries are working towards is smart energy drink modularization in order to align production and distribution workload demands and interoperability of cross-border ingredient supply chains. It is driven by advanced technologies, such as real-time flavor intelligence engines and high-reliability compliance scoring systems with built-in predictive algorithms for the development of product risk profiles. Adoption is facilitated by the use of public-private partnerships and the harmonization of energy drink data standards. Technologies like real-time production workload balancing and smart packaging-based data sharing are commonly practiced as research-centric programs, and Europe is a frontrunner in terms of the digital transformation of safe and efficient energy drink-enabled enterprise operations.

Japan Energy Drinks Market

The Japan Energy Drinks Market is projected to be valued at USD 6.1 billion in 2026, progressing at a CAGR of 8.3%, during the period spanning from 2026 to 2035.

Japan boasts a mature energy drinks market supported by high-performance automated formulation systems, diagnostic compliance integration technology, and a wide network of robotic process automation and AI innovations. Automation, precision, and process integrity are the priorities in the country and are achieved by predictive product risk progression models and intelligent workflow management systems for enterprise distribution and retail. Growth is stimulated by government actions under the Society 5.0 initiative and constant investment in digital business infrastructure. The high volume of safety and compliance review, industrial product development for supply chain and retail agreements, and energy drink automation requires efficient AI for real-time evidence-based inference. The difficulties are high validation costs for new energy drink automation architectures and integration with legacy production systems, yet the prospects are in exporting developed energy drink technologies to Asian and Pacific markets.

Key Takeaways

- Market Size & Forecast: The Global Energy Drinks Market is estimated to be valued at USD 94.1 billion in 2026 and is expected to grow to USD 189.8 billion by 2035.

- Growth Rate & Outlook: The market is expected to witness growth at a compound annual growth rate of 8.1% in the forecast period.

- Primary Growth Drivers: Growing consumer demand for functional and performance beverages, increasing consumption of energy drinks among young adults, sportspeople, and professionals, and demand for sugar-free and clean energy drinks are the major factors driving the growth in the market.

- Key Market Trends: Growing popularity of natural and organic energy drinks, growth of low-calorie and sugar-free energy drinks, increased product innovation in taste and ingredients, and influence of online marketing and sponsorships in esports in the energy drinks market are some of the key market trends.

- By Product Format: The Energy Drinks segment is anticipated to get the majority share of the market in 2026.

- By Nature: The Conventional segment is expected to occupy the largest revenue share in 2026 in the market.

- By Distribution Channel: The Supermarkets/Hypermarkets segment is expected to get the largest revenue share in 2026 in the energy drinks market.

- Regional Leadership: North America is predicted to dominate the market with an estimated 34.2% share in 2026, driven by high consumption levels and strong brand presence.

What are Energy Drinks?

Energy drinks are functional drinks that include caffeine, taurine, B-vitamins, amino acids, and natural and artificial sweeteners to stimulate the brain, stamina, and metabolism. These products use standardized formulation guidelines, libraries of flavors, inventory, and analytics technologies to attain quick turnaround, enhanced safety and accuracy, and quick prototyping and scale-up manufacturing operations. Athletes, students, workers, and night shift employees are now using energy drinks to enhance alertness, performance, and further facilitate the design of compliant and efficient functional drinks.

Use Cases

- Product Formulation for Retail Launches: The manufacturers of energy drinks can establish high-throughput formulation systems that can identify the optimal combinations of ingredients in caffeinated blends, sugar-free, and all-natural lines with response times of days and weeks, compared to formulation development times of months when formulating by hand.

- Inventory & Distribution Optimization: Businesses are using historical consumption and sales data, including re-order rates and out-of-stock events, to provide replenishment advice and product portfolio management without downtime to ensure smooth production and sales.

- Compliance Monitoring & Control: Enterprise-scale deployments are using quality analytics to conduct real-time safety surveillance, compliance anomaly detection, and alerting with accurate measures.

- Public Health & Government Programs: More efficient energy drink systems support regulatory compliance in functional beverages and supply chain monitoring, facilitate adherence to food safety policies, contribute to operational reliability, and help implement standards such as food safety regulations and digital commerce practices.

How AI Is Transforming the Global Energy Drinks Market?

Artificial intelligence is transforming the energy drinks market, enabling predictive modeling of product demand and sales performance, automatic detection of anomalies in consumption patterns, and optimization of flavor development parameters in a market-specific scenario. Sales data and consumer insights can be processed using AI algorithms to identify performance trends and optimize product outcomes at scale. This saves time, improves decision-making, and is more efficient than manual data analysis.

Moreover, AI enhances operational efficiency through adaptive demand planning, anticipating distribution challenges, and intelligent prioritization of production and supply chain processes. It is also involved in reducing the cost of product testing and ongoing performance tracking, allowing companies to reduce operational costs and improve the reliability of production and distribution outcomes and their financial returns.

Market Dynamics

Key Drivers of the Global Energy Drinks Market

Product Innovation and Consumer-Centric Formulation Development

The market is being driven by the rapid introduction of new product formulations, efficient consumer data utilization, integration with retail and distribution systems, and enhanced analytics from sales repositories. Such factors make it possible for firms to keep track of the performance of their products, spot any consumption patterns, and facilitate both the development and commercialization of the products efficiently. This leads to enhanced productivity and improved decision-making, all without placing undue stress on manual evaluation. The heightened emphasis placed on developing unique flavors is also increasing the necessity for product strategies, as firms embrace the use of data and optimization of workflow.

Rising Regulatory Compliance Requirements

With increased emphasis on safety and quality, more stringent systems have been developed by government agencies that outline the framework for the use of ingredients, proper labeling, and approval process. This need is fostering the development of manufacturing processes that ensure that compliance standards are met. In parallel, global initiatives promoting formulation transparency and workforce development are encouraging the adoption of standardized production practices. The increasing focus on ingredient disclosure and reduction in compliance risks is also enhancing the necessity of reliable and scalable operational frameworks across both developed and emerging markets.

Restraints in the Global Energy Drinks Market

High Development and Operational Costs

Energy drink product development and market expansion can be expensive and time-intensive, requiring extensive testing in production settings, validation of formulation consistency, and long-term performance evaluation of new product variants. Moreover, the regulatory needs and data protection issues associated with consumer insights contribute to the complexity and expense of operations. All these have the potential to create entry barriers, extend the commercialization cycle, and raise the initial capital requirements.

Lack of Standardization Across Product Offerings

The industry has remained dependent on varying formulation strategies, ingredient profiles and branding strategies across geographic areas. Nevertheless, the absence of standard product positioning and formulation benchmark is among the major challenges. The products of the energy drinks lack universal frameworks across markets, so the process of product alignment can be complicated, and the uniformity of consumer perception and distribution in different markets and retail markets can be limited.

Growth Opportunities in the Global Energy Drinks Market

Expansion in Emerging Markets

Developing markets such as Brazil, Indonesia, Nigeria, the UAE, and Vietnam are witnessing increasing investment in retail infrastructure and consumer product accessibility. These regions present strong growth potential due to rising demand for energy drinks, increasing urbanization, and evolving consumer lifestyles. With relatively lower market penetration, they provide opportunities for the introduction of new product variants optimized for local preferences and regulatory environments.

Growing Shift Toward Advanced Distribution and Retail Channels

The rise of organized retail, the development of e-commerce platforms, and the changing consumer buying behavior are influencing the increased need to be efficient in distribution. The channels are crucial in enhancing accessibility of the products, with real-time visibility of the inventory, and wider market coverage. As the trend of quicker availability of a product and efficient supply chains increases, enhanced distribution strengths will probably become the key to future market growth.

Global Energy Drinks Market Trends

Increasing Adoption of Data-Driven Sales and Marketing Strategies

Sales performance is becoming highly monitored with advanced analytics identified by the energy drink companies to identify consumption patterns. Distribution planning, product positioning, and general market responsiveness are improving through the use of data-driven insights. This is changing decision-making from a more manual process to a more organized and constantly optimized strategy. Also, firms are utilizing consumer information to narrow down the targeted marketing campaigns and enhance brand appeal among important demographics.

Advancement in Centralized Distribution Monitoring and Management

Digital tools and centralization are becoming relevant in the management of distribution networks of energy drinks. These platforms allow tracking sales performance in real-time, better management of portfolios, and better coordination within supply chains. These strategies enhance transparency, minimize inefficiencies in operations and offer faster reaction to demand fluctuations in retail channels.

Research Scope and Analysis

The global energy drinks market is driven by strong demand for ready-to-drink caffeinated beverages, conventional formulations, and can packaging. Growth is further supported by rising health-conscious consumption, tropical flavor innovations, expanding online retail channels, and increasing preference for functional and performance-enhancing beverages worldwide.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Product Format Analysis

The Energy Drinks segment is expected to remain the largest in 2026, accounting for about 62.5% share of the global energy drinks market. This dominance is driven by high consumer demand for ready-to-drink formulations, widespread availability across retail channels, and continuous innovation in flavors and functional ingredients such as nootropics and adaptogens. Meanwhile, the Energy Shots segment is witnessing strong growth, driven by rising demand for concentrated, low-volume products that deliver rapid energy boosts for on-the-go consumers, particularly in workplace and travel settings. The Energy Mixers & Powders segment, while smaller, is gaining traction among fitness enthusiasts and home mixologists who value customization and portion control.

By Nature Analysis

The Conventional segment is expected to account for the largest share in 2026 with around 66.4% share, as conventional energy drinks remain the mainstream choice due to established brand loyalty, lower price points, and widespread distribution in supermarkets and convenience stores. However, the Organic segment is the fastest-growing, driven by increasing health consciousness, clean label trends, and consumer preference for natural caffeine sources (e.g., green tea, guarana) and absence of artificial sweeteners and preservatives. Organic energy drinks are particularly popular in North America and Europe among premium retail and wellness-focused consumers.

By Product Type Analysis

The Caffeinated Beverages segment dominates the market, accounting for an estimated 78.5% share in 2026, as caffeine remains the primary functional ingredient for mental alertness and physical endurance. Nearly all mainstream energy drinks fall into this category. The De-caffeinated Beverages segment represents a small but growing niche, catering to consumers sensitive to caffeine or those seeking energy from alternative ingredients like B-vitamins, taurine, and coenzyme Q10. This segment is gaining traction in evening consumption occasions and among health professionals recommending reduced stimulant intake.

By Packaging Analysis

The Cans segment is expected to hold the largest share in 2026 with approximately 71.2% share, driven by aluminum's durability, superior barrier properties against light and oxygen, rapid cooling capability, and high recyclability. Cans are the preferred packaging for on-the-go consumption and are strongly associated with leading brands like Red Bull and Monster. The Bottles segment follows, primarily used for premium products, resealable formats, and larger multi-serve sizes. The Others segment (including pouches, cartons, and glass) is growing steadily, driven by sustainability initiatives and brand differentiation strategies, particularly in the organic and natural energy drink sub-segments.

By Flavor Analysis

The Citrus segment is expected to dominate with approximately 34.8% share in 2026, as citrus flavors are universally recognized, refreshing, and effectively mask the bitterness of caffeine and other functional ingredients. The Berry segment follows closely, appealing to consumers seeking sweeter, fruit-forward profiles. Tropical flavors are the fastest-growing, driven by consumer interest in exotic taste experiences and successful product launches from brands like Monster's "Pipeline Punch" and Red Bull's "Summer Edition." The Herbs segment (ginseng, ginger, turmeric) remains smaller but is growing rapidly within the functional and organic sub-markets.

By Categories Analysis

The Functional Beverages segment is expected to dominate with around 37.8% market share in 2026, driven by the critical need for rapid and accurate assessment of ingredient efficacy, health benefit communication, and regulatory adherence. Energy drink platforms support compliance scenarios due to their ability to rapidly prototype approval workflows, delivering rapid turnaround times while maintaining product data within enterprise systems. The Sports Drink segment holds a significant share, supported by electrolyte and performance ingredient innovations targeted at athletes and fitness enthusiasts. The Non-Alcoholic Beverage segment benefits from the broader shift away from alcohol among younger demographics, while Non-Carbonated Packaged Drinks appeal to consumers preferring still, juice-based, or tea-based energy options.

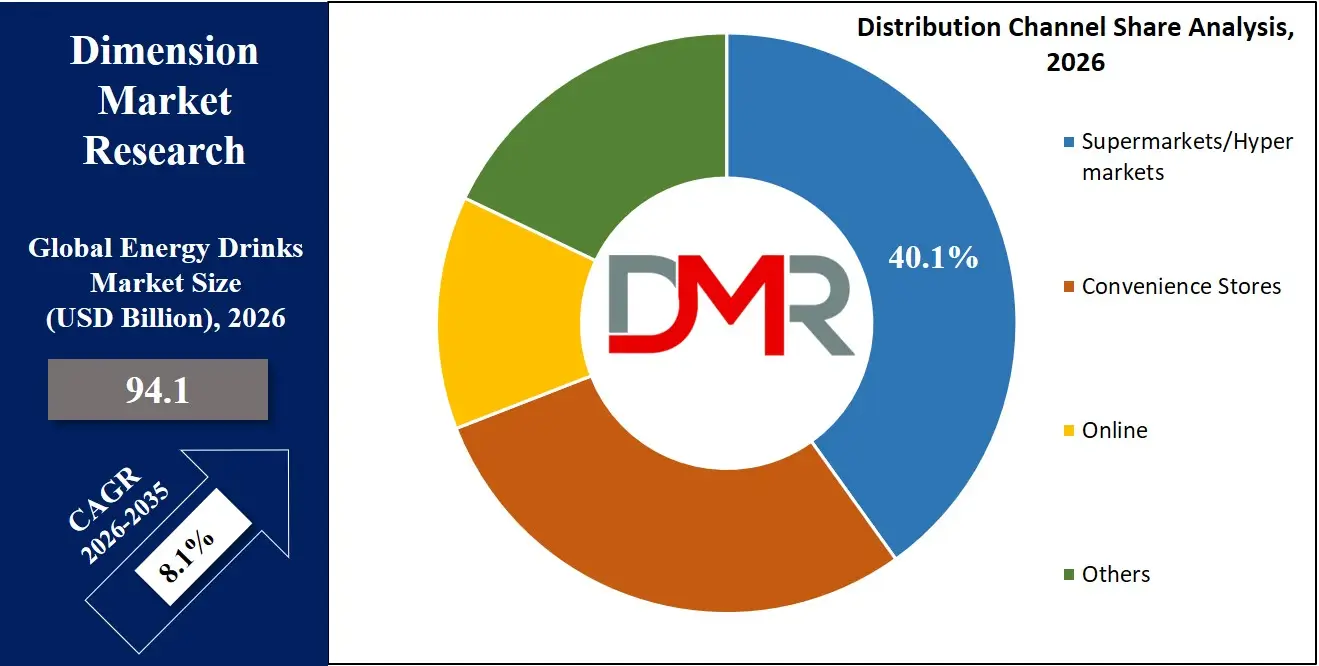

By Distribution Channel Analysis

The Supermarkets/Hypermarkets segment is expected to dominate with approximately 40.1% share in 2026, driven by the critical need for shelf space allocation, volume sales, and one-stop shopping convenience. These large-format retailers offer the widest assortment of brands, flavors, and pack sizes. The Convenience Stores segment follows closely, as these outlets capture high-margin impulse purchases and single-serve transactions, particularly from commuters and young adults. Online retail is the fastest-growing channel, driven by direct-to-consumer brand strategies, subscription models, bulk purchasing discounts, and the convenience of home delivery. The Others segment accounts for the remainder, representing important niche channels for targeted consumer segments.

The Global Energy Drinks Market Report is segmented based on the following:

By Product Format

- Energy Drinks

- Energy Shots

- Energy Mixers & Powders

By Nature

By Product Type

- Caffeinated Beverages

- De-caffeinated Beverages

By Packaging

By Flavor

- Citrus

- Berry

- Tropical

- Herbs

- Others

By Categories

- Natural Energy Drink

- Sports Drink

- Non-Alcoholic Beverage

- Functional Beverages

- Non-Carbonated Packaged Drinks

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online

- Others

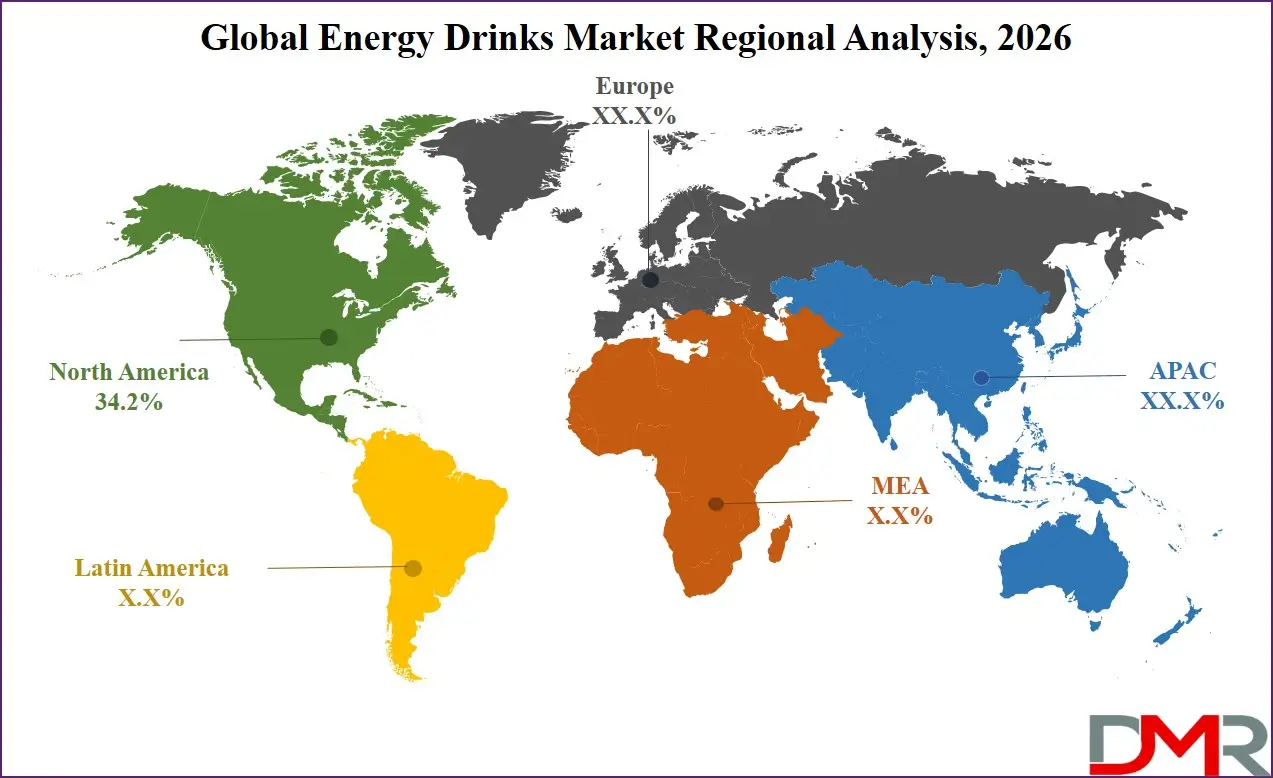

Regional Analysis

Leading Region in the Energy Drinks Market

It is projected that North America will take the lead in the global energy drinks market (by value), covering a market share of about 34.2% in the year 2026. The region's dominance is driven by strong retail digital transformation cadence (US-based National AI in Beverage Initiative and FDA digital commerce programs), high product and distribution prices relative to other regions, a mature retail IT supply chain for advanced interoperability and high-speed data exchange, and the presence of key energy drink vendors and digital transformation consultancies. The widespread adoption of advanced machine learning and workflow-based automation for marketing, sales, distribution, and compliance further strengthens North America's leading position in the market. Additionally, continuous investments in AI-enabled process logic monitoring and interoperability capabilities are further reinforcing regional technological leadership.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Region in the Energy Drinks Market

Asia-Pacific is the fastest-growing region, supported by strong digital transformation deployment targets (China, India, Japan), increasing data sovereignty initiatives, rising investments in domestic production capabilities, and growing adoption of automated beverage management systems. The region benefits from well-established manufacturing capacity for automated workflows, increasing commercial participation, and alignment with national digital economy roadmaps. Countries across the region are actively deploying energy drink platforms to enhance operational productivity-per-dollar and strengthen retail digital infrastructure. Growing emphasis on R&D and structured process logic development further accelerates market expansion in the region. Moreover, increasing government support and commercial enterprise commitments are expected to sustain high growth momentum.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The energy drinks market is highly competitive, with innovation and strategic alliances shaping the competitive environment. In order to achieve a competitive advantage, companies are focused on the development of advanced automation architectures (e.g., AI-based flavor intelligence, workflow automation for distribution, and machine learning for risk optimization), AI-powered consumer analytics, and digital twin-enabled compliance monitoring platforms. There are high barriers to entry due to capital-intensive process validation infrastructure, specialized formulation and compliance expertise, and the need for mature retail ecosystems and enterprise regulatory and procurement compliance.

Strategic approaches in the market to increase market presence include partnerships with retailers and digital transformation centers, mergers between automation solution providers and system integrators, and long-term supply contracts with marketing departments, distribution teams, and academic institutions. Moreover, research and development in interoperability frameworks and scalable software architectures are important factors in maintaining competitiveness and addressing the evolving needs of the digital retail community.

Some of the prominent players in the Global Energy Drinks Market are:

- Red Bull GmbH

- Monster Beverage Corporation

- PepsiCo, Inc.

- The Coca-Cola Company

- Suntory Holdings Limited

- Keurig Dr Pepper Inc.

- Celsius Holdings, Inc.

- T.C. Pharmaceutical Industries Co., Ltd.

- Osotspa Public Company Limited

- Carabao Group Public Company Limited

- Taisho Pharmaceutical Holdings Co., Ltd.

- Otsuka Holdings Co., Ltd.

- Amway Corp.

- Living Essentials, LLC

- AriZona Beverages USA LLC

- HELL ENERGY Magyarország Korlátolt Felelősségű Társaság

- AJE Group

- National Beverage Corp.

- Nutrabolt, Ltd.

- Congo Brands, LLC

- Other Key Players

Recent Developments

- October 2025: The Coca-Cola Company expanded its distribution and bottling investments across emerging markets, particularly in Asia and Latin America, to enhance its energy drink market penetration and strengthen its global supply chain network.

- August 2025: Keurig Dr Pepper Inc. announced the acquisition of JDE Peet's for approximately USD 18.0 billion, aiming to restructure its portfolio into separate beverage and coffee businesses, strengthening its strategic focus on high-growth segments including energy drinks.

- August 2025: Celsius Holdings, Inc. entered a major strategic partnership with PepsiCo, Inc., under which PepsiCo invested USD 585 million to increase its stake to around 11%, while becoming the exclusive distribution partner for Celsius' portfolio across the U.S. and Canada.

- March 2025: Red Bull GmbH expanded its long-term partnership with Riot Games, extending its role as the official energy drink partner for global esports events, strengthening brand visibility and consumer engagement across younger demographic.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 94.1 Bn |

| Forecast Value (2035) |

USD 189.8 Bn |

| CAGR (2026–2035) |

8.1% |

| The US Market Size (2026) |

USD 27.1 Bn |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimated Year |

2026 |

| Segments Covered |

By Product Format (Energy Drinks, Energy Shots, Energy Mixers & Powders), By Nature (Organic, Conventional), By Product Type (Caffeinated Beverages, De-caffeinated Beverages), By Packaging (Cans, Bottles, Others), By Flavor (Citrus, Berry, Tropical, Herbs, Others), By Categories (Natural Energy Drink, Sports Drink, Non-Alcoholic Beverage, Functional Beverages, Non-Carbonated Packaged Drinks), By Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Online, Others) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Energy Drinks Market?

▾ The Global Energy Drinks Market size is estimated to have a value of USD 96.2 billion in 2024 and is expected to reach USD 192.3 billion by the end of 2033.

Which region accounted for the largest Global Energy Drinks Market?

▾ North America is expected to be the largest market share in the Global Energy Drinks Market with a share of about 33.3% in 2024.

Who are the key players in the Global Energy Drinks Market?

▾ Some of the major key players in the Global Energy Drinks Market are Coca-Cola Company, PepsiCo. Inc., Red Bull, and many others.

What is the growth rate in the Global Energy Drinks Market?

▾ The market is growing at a CAGR of 8.0 percent over the forecasted period.