Market Overview

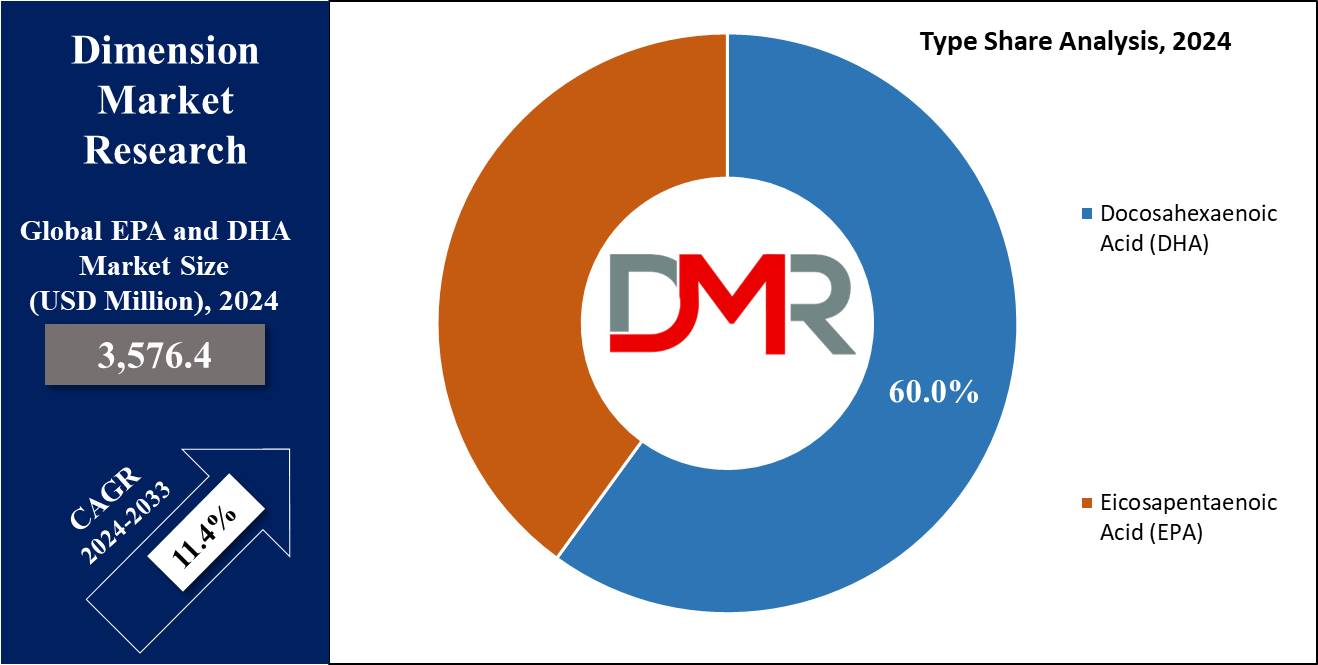

The Global EPA and DHA Market size is expected to reach a value of

USD 3,576.4 million in 2024, and it is further anticipated to reach a market value of

USD 9,463.0 million by 2033 at a

CAGR of 11.4%.

Consumer understanding of omega-3 fatty acid's benefits to health has contributed significantly to the rapid growth of the global EPA and DHA market. Eicosapentaenoic Acid or EPA and docosahexaenoic Acid or DHA are among the essential omega-3 nutrients that provide support for cardiovascular health, brain functioning, and infant development.

Fish oil, krill oil, and algae oil have traditionally been sources of omega-3 fatty acids. Currently, these fatty acids can be found in an assortment of products including dietary supplements, functional foods, pharmaceuticals, and infant formula. Due to increasing awareness of prevention over cure among consumers and increased consumer spending on omega-3 supplements and dietary products, this market growth trend will only accelerate further.

Pharmaceutical and nutraceutical industries account for much of the demand that has contributed to the expansion of EPA and DHA markets globally. Forecast projections remain positive with an anticipated annual compound average growth rate exceeding

11.4% over the coming decade, as Asia Pacific countries possessing large populations, rising disposable incomes, and citizens showing greater awareness regarding

health and wellness continue to show strong potential growth potential in these nations.

Due to growing concerns and issues surrounding overfishing, algae oil represents one of the key sources for providing essential EPA and DHA lipids shaping its future market potential and helping keep fish stocks alive. DSM, BASF SE, and KD Pharma Group all play key roles in market expansion with product innovation, partnerships, and sustainability initiatives that contribute to its expansion. Market analyses clearly illustrate the fact that more product diversification and sustainability initiatives may contribute towards the long-term viability of the global EPA and DHA market.

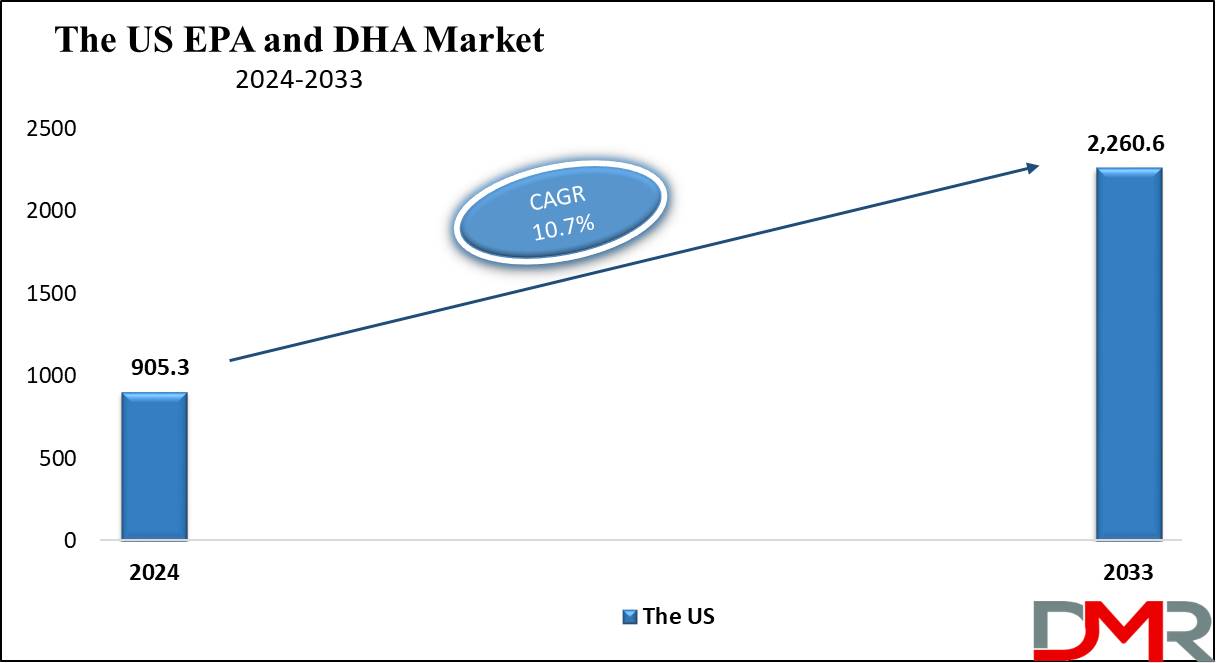

The US EPA and DHA Market

The US EPA and DHA Market is projected to be valued at USD 905.3 million in 2024. It is expected to witness subsequent growth in the upcoming period as it holds USD 2,260.6 million in 2033 at a CAGR of 10.7%. The market of EPA and DHA has proved to be developing very strongly in the U.S. due to the strengthened customer awareness of omega-3 acids as sources of health benefits.

Most of the U.S. market depends on fish oil as a key sourced supply of EPA and DHA in a wide range of uses related to dietary supplements, functional food, and pharmaceutical applications. Recent trends indicate an increase in the consumption of value-added food and beverages, and among functional foods, products value-added with EPA and DHA are gaining momentum in the preference list of health-conscious consumers. This trend is based mainly on increased public awareness through campaigns regarding the cardio-protective, cognitive, and anti-inflammatory benefits of omega-3s.

One of the other growing trends in the market for U.S. EPA and DHA is innovative product development is the introduction of newer forms including beverages, snacks, and gummies in various formats with EPA and DHA, attracting younger consumers and those demanding convenience in their everyday diet. In addition, algae oil is becoming a popular plant-based, sustainable alternative to fish oil, which also provides options for vegan and ecologically aware consumers.

The U.S. market also sees significant growth in regulatory support, as the FDA is continuously approving health claims on consumption regarding omega-3, an aspect that gives consumers confidence and enhances market growth. Growing health awareness, increasing disposable incomes, and growth in demand for sustainable plant-based sources of omega-3 are some of the factors that will contribute to the US EPA and DHA market during the forecast period at an attractive growth rate.

Key Takeaways

- Global Market Value: The Global EPA and DHA Market size is estimated to have a value of USD 3,576.4 million in 2024 and is expected to reach USD 9,463.0 million in 2033.

- The US Market Value: The US EPA and DHA Market is projected to be valued at USD 2,260.6 million in 2033 from a base value of USD 905.3 million in 2024 at a CAGR of 10.7%.

- Regional Analysis: Asia Pacific is expected to have the largest market share in the Global EPA and DHA Market with a share of about 34.1% in 2024.

- By Type Segment Analysis: Docosahexaenoic Acid (DHA) is projected to dominate the type segment as it holds 60.0% of the market share in 2024.

- By Source Segment Analysis: Animal Source is anticipated to dominate this segment with 63.1% of market share by the end of 2024.

- Key Players: Some of the major key players in the Global EPA and DHA Market are Koninklijke DSM N.V., BASF SE, Croda International Plc., Corbion N.V., Golden Omega S.A., and many others.

- Global Growth Rate: The market is growing at a CAGR of 10.7% over the forecasted period.

Use Cases

- Cardiovascular Health: Dietary supplements containing EPA and DHA are normally used to avoid heart disease by reducing triglycerides and blood pressure levels. They are widely recommended for individuals with a potential risk of cardiovascular diseases.

- Infant Development: DHA is critical for brain and eye development in infants, leading to its inclusion in infant formula. The demand for DHA-enriched infant formula is rising as parents seek fortified nutrition solutions for newborns.

- Cognitive Function: Increasing numbers of EPA and DHA are also being used in these products to focus on improved cognitive functions, especially in aging populations. Supplements and foods containing omega-3 fortification make claims that they can maintain mental clarity and reduce the risk of neurodegenerative diseases.

- Pharmaceuticals: Omega-3 fatty acids are incorporated into pharmaceutical products for various conditions like hyperlipidemia and chronic inflammation. There have been many EPA or DHA based prescriptions that have received FDA approval under certain medical conditions.

Market Dynamic

Trends

Sustainable Sourcing

The shift toward EPA and DHA from sustainable and environmentally viable sources. With overfishing and the degradation of vital ecosystems gaining increased awareness, algae oil has slowly but sure become the standard for sustainability as an alternative to traditional fish oil.

Algae oil is a plant-based source of omega-3 fatty acids, with no contribution to marine depletion, pollution, or biodiversity loss. As consumers are increasingly aware of the need for sustainability and manufacturers are keen on eco-friendly production methods in their value chains, demand for algae oil is at the point of exponential growth.

Growth of Functional Foods

The inclusion of EPA and DHA in functional foods and beverages is going mainstream. Consumers are progressively seeking ways to manage their health with a minimum of supplementation and easy, natural solutions.

Foods fortified with omega-3, such as dairy products, breakfast cereals, and even beverages, have gained greater traction as people seek ingrained health-enhancing ingredients in everyday diets. This is further encouraged by growth and innovation in product formulation which the functional food industry has invested in, to meet various consumer preferences.

Growth Drivers

Rising Health Awareness

Growing awareness regarding health benefits associated with EPA and DHA, particularly in the prevention of cardiovascular diseases, improving cognitive functions, and decreasing inflammation. These factors act as a significant driver for market growth.

Omega-3s have scientific evidence that proves their benefits, which has helped increase adoption among health-conscious consumers. Public health campaigns, medical endorsements, and the growing pervasiveness of chronic diseases are driving more consumers to take omega-3s as part of their regimen, further driving demand for EPA and DHA products.

Aging Population

A growing aging population across the world is another major growth factor in the EPA and DHA market. With graying, the populations increasingly depend on preventive health to fight age-related diseases like Alzheimer's, heart disease, and arthritis.

Omega-3 fatty acids, DHA are known to be helpful for cognitive functions and cardiovascular health, hence these fatty acids are highly in demand with aging populations. The rise in consumption due to the exponentially increasing elderly population worldwide, especially in regions like North America, Europe, and Asia, increases dietary supplements and omega-3 fortified food consumption.

Growth Opportunities

Emerging Markets

There are immense growth opportunities for the EPA and DHA market in emerging economies, especially from the Asia Pacific and Latin America regions. As the urbanization in these regions is increasing per se, higher disposable incomes, and awareness about health are in demand for omega-3 products at a faster rate.

Similarly, demand for dietary supplements and EPA DHA food fortification formulation is expected to see phenomenal growth due to the reason that consumers are gradually drifting toward preventive health care and healthy lifestyles. This, in turn, sets an attractive opportunity for the manufacturers to increase their presence in order to tap these fast-growing markets.

Plant-Based Omega-3s

The increasing demand for plant-based diets and vegan alternatives has opened up great avenues in the development of plant-based omega-3 products. Algae oil is becoming one of the key sources of EPA and DHA for these consumers who avoid animal-based products. This demand for plant-based omega-3 dietary supplements and foods with fortification is expected to further rise due to increasing vegan and vegetarian consumers, hence being a growth opportunity for firms offering sustainable and plant-based omega-3 solutions.

Restraints

High Costs of Omega-3 Products

One of the key restraints facing the EPA and DHA market is that premium omega-3 supplements and fortified foods are not cheap. Because the process of extraction and production is so complicated, products made with high-quality fish oil and algae oil usually command a premium price.

It will automatically reduce the accessibility to those oils, especially in sensitive markets during periods when consumers are unwilling or unable to pay a premium for health supplements. The main problem is still the very high cost of raw materials and sophisticated production technologies, which makes it really hard for a manufacturer to provide quality omega-3 products at relatively low prices.

Supply Chain Challenges

EPA and DHA markets experience disruption, mainly in the supply chain of fish oil, krill oil, and algae oil. Supplies of raw materials can fluctuate due to overfishing, environmental legislation, and climate change cause temporary shortages and altering prices.

In addition, logistics regarding maintaining freshness and potency during transportation and storage are critical since the omega-3 oils are susceptible to oxidation. The ability to manage such supply-chain challenges without compromising product quality or availability remains one of the key issues for omega-3 manufacturers.

Research Scope and Analysis

By form

Triglycerides are projected to dominate the form segment of the EPA and DHA market as they hold 60.0% of the market share in 2024 as are the formed in which omega-3 fatty acids naturally occur in fish oil. Humans are more capable of absorbing and utilizing omega-3s if they are taken in the triglyceride form. This makes it a superior choice for nutraceutical supplements and functional food products.

Further, this makes triglycerides even more bioavailable in other words, their absorption is more efficient in the body compared to other forms like ethyl esters. The higher the bioavailability, the better the delivery of EPA and DHA into the body's tissues, implying better health value of the omega-3 supplements.

Apart from that, triglycerides are more stable and resistant to oxidation than other forms of omega-3. This stability is very crucial because it sustains the potency and effectiveness of the EPA and DHA through storage and transportation. This means that your product will be health-wise effective throughout its shelf life. Generally speaking, supplements made of triglycerides are a little better embraced by the consumer, with them bearing fewer side effects, as compared to those others based upon ethyl ester.

This continued demand for natural, high-quality omega-3 supplements pushes the dominance of triglycerides. As consumer preferences shift regarding naturalness and lack of processing, the triglyceride form has increasingly become the favored form when it comes to both forms of EPA and DHA in the marketplace. Companies marketing in the space continue to focus on delivering high-purity triglyceride products to meet that demand, a factor ensuring triglycerides keep their leading position in the form segment.

By Source

Animal sources are anticipated to dominate this market at 63.1% of the market share in the source segment in 2024. Animal sources, particularly fish oil and krill oil, remain the dominant sources because of their high composition of omega-3 fatty acids, EPA and DHA. Fish oil, in particular, is an extremely good source of both EPA and DHA, hence one of the most efficient and cost-effective sources for the extraction of these two important nutrients.

Decades of scientific research have proven the established efficacy of omega-3-s sourced from animals, thereby establishing consumer trust in fish oil-based products. That historical trust led to fish oil maintaining the market share even when faced with emerging alternative sources such as algae oil.

Due to their high composition of nutrients, fish oil-based products still have a high demand in the global market. These animal sources, provide a higher unit concentration of EPA and DHA compared to plant-based alternatives; thus, they are very popular with dietary supplement and functional food manufacturers, as they would want to be able to deliver an effective product.

Moreover, in general, fish oil is relatively inexpensive, and the supply chains are very well developed for steady supplies. Extraction processes for omega-3 from animal sources are, on the other hand, efficient and scalable, which is one of the major factors ensuring their leading position in the source segment of the EPA and DHA market.

While the issues of sustainability are dragging the market towards other available alternatives, such as algae oil, fish oil remains the main source due to its relative cheapness, availability, and scientifically proven health benefits. Krill oil, on the other hand, has superior bioavailability over other products and comes with added antioxidant properties, hence gaining traction in the market but still lower than that of fish oil.

By Type

DHA represents the dominant position in the type segment of the EPA and DHA market because it is considered essential role in brain and eye development at an early age. DHA is a major constituent of the cerebral cortex and retina hence; it is highly important for neurological and visual function.

Infant formula and maternal supplements are the two major applications of DHA since it is widely recognized that pregnant and lactating mothers require a higher intake to support the growth of the infant's brain and eyes. Demand from the infant nutrition segment has been one of the mainstays driving its leadership position. DHA also finds extensive applications in products for the improvement of cognitive health, particularly among aging populations.

Many believe DHA increases memory retention, aids in mental clarity, and can prevent neurodegenerative diseases such as Alzheimer's with the recent interest in mental health and cognitive functions, there is a surge in demand for DHA supplements. This makes DHA, highly concentrated in the brain compared to the amounts present in EPA, more viable within products catering to the application of cognitive health and further solidifies its dominant position in the type segment of the EPA and DHA market.

Scientific studies that have steadily emerged to support the benefits of DHA have been sweetened further with strong recommendations by healthcare professionals, raising consumer awareness and demand for DHA-enriched products. For this reason, DHA dominates in application in infant formula, cognitive health supplements, and functional foods.

The demand for DHA is expected to remain high during the forecast period because of its increasing use for health applications-from prenatal supplements to cognitive function products intended for aging adults.

By Application

The application segment of the EPA and DHA market is led by nutritional dietary, as consumers growing more aware of health benefits from omega-3 fatty acids, including cardiovascular, cognitive functionality, and reduced inflammation. Omega-3 dietary supplements that contain sufficient amounts of EPA and DHA are an easy way to get daily nutrition from these nutrients, especially in regions where fish intake is low.

The growing trend of preventive health has also explained the rising consumption of dietary supplements, as more and more people are getting involved in ways through which they can benefit their health in the long run. Among the primary reasons that dietary supplements are leading this segment is their ability to provide concentrated doses of EPA and DHA to ensure that consumers can receive adequate health benefits without complete dependence on their diet.

This demand is also driven by the rise in the elderly population due to increasing life spans. As people grow older, they seek remedies through supplements that can prevent or mitigate the severity of age-related health conditions such as cognitive decline and heart disease. Omega-3 fatty acids are well associated with improved mental clarity, anti-inflammation, and cardiovascular protection and, hence, provide a comprehensive complement to the dietary needs of aging consumers.

The extension towards a greater requirement for these supplements of EPA and DHA in different formats- such as soft gels, gummies, powders, and liquid formulations been invented by manufacturers. Such diversification of the offer increased the desirability of omega-3 supplementation among various consumer demographics, especially among younger generations with specific dietary preferences.

Major players in the market, like DSM, BASF SE, and KD Pharma Group, are some of the companies that have made considerable investments in research and product development. For these reasons, the dietary supplement segment has become a growth segment. Dietary supplements are, therefore, likely to retain the market share in the segment for EPA and DHA during the forecast period.

The EPA and DHA Market Report is segmented on the basis of the following

By Type

- Eicosapentaenoic Acid (EPA)

- Docosahexaenoic Acid (DHA)

By Source

- Animal Source

- Anchovy Oil

- Sardine Oil

- Tuna Oil

- Cod Liver Oil

- Salmon Oil

- Krill Oil

- Menhaden Oil

- Plant Source

- Algal Oil

- Other Marine Algae

By Form

- Triglyceride (TG) Form

- Ethyl Ester (EE) Form

- Free Fatty Acid (FFA) Form

- Phospholipid Form

By Application

- Dietary Supplements

- Soft gels

- Tablets

- Powders

- Infant Formula

- Functional Foods and Beverages

- Fortified Food Items

- Omega-3 Enhanced Beverages

- Pharmaceuticals

- Prescription Drug

- Medical Nutrition

- Animal Feed

- Pet food

- Livestock and Aquaculture Feed

- Personal Care and Cosmetics

- Other Applications

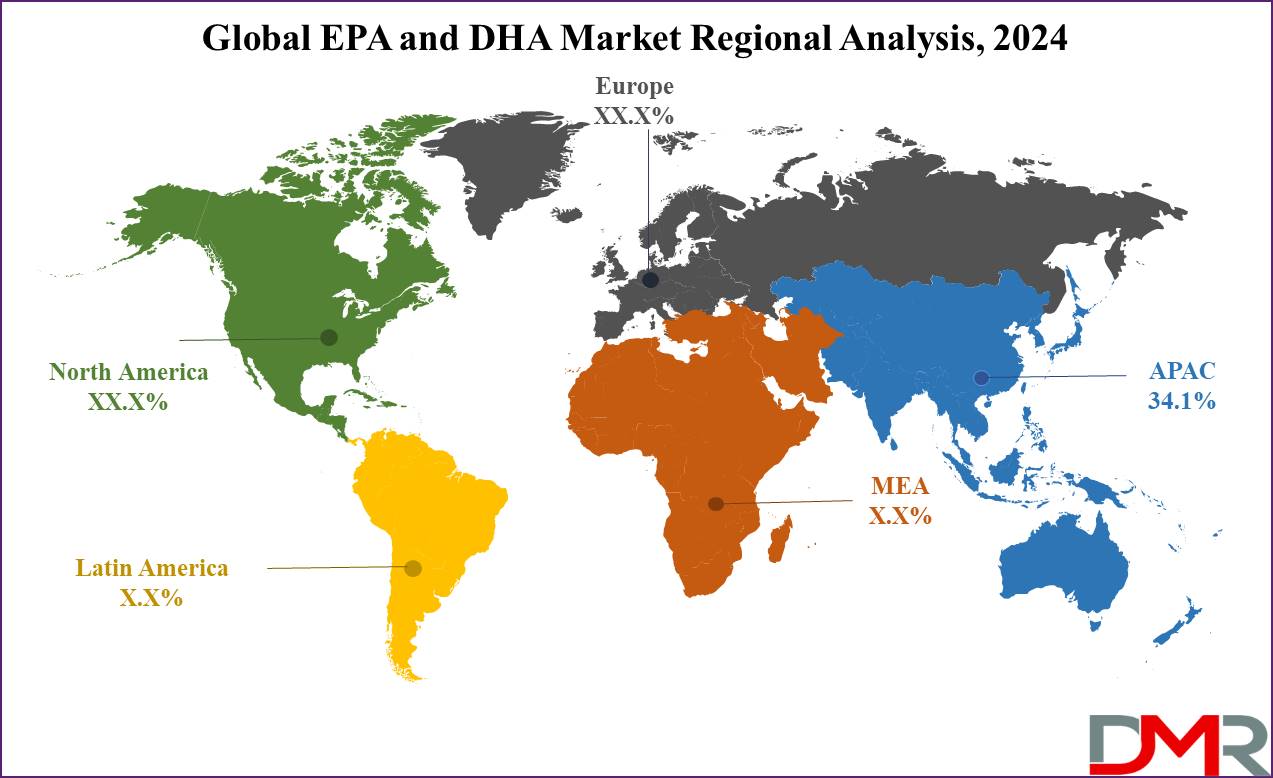

Regional Analysis

Asia Pacific is projected to be the largest and fastest-growing region in the global EPA and DHA market as it

will hold 34.1% of the market share by the end of 2024. The Asia Pacific currently is the biggest and fastest growing geographical region in the global EPA and DHA market, due to the huge population base, increasing disposable incomes of the people, and rising health awareness.

This demand will be driven by countries such as China, Japan, India, and South Korea due to consumer awareness related to health benefits associated with EPA and DHA. The high consumption of fish and seafood in the region, being natural sources of EPA and DHA, has been one of the factors that have contributed to its dominance. For instance, in countries like Japan, where the consumption of fish has traditionally formed part of their diet, there already exists a strong cultural emphasis on omega-3 intake.

This leads to increased consumer demand for fish oil supplements and fortified foods. Of late, China has emerged as a major hub globally for omega-3 products, "primarily in the infant formula category." In fact, encouragement by the Chinese government to improve maternal and infant health has triggered demand for DHA-enriched infant formulas, considered essential for the neurological and visual development of newborns. Fast urbanization and the growth of the middle class in China have also driven consumer preference for more value-added health products.

Government initiatives and regulatory approvals on the use of omega-3s in dietary supplements and functional foods also encourage increased demand for EPA and DHA. The growth in the peanut industries, particularly the pharmaceutical and nutraceutical industries, within the region is also a driving force in the dominance of Asia Pacific. Many local producers get with omega-3 products concurrently, their prices being competitive, hence getting close to the big population.

Additionally, influential players in the global EPA and DHA market, including DSM and BASF SE, are expanding their business processes in Asia Pacific owing to the growth potential of the region. These factors are likely to favor continuation of regional dominance in the global EPA and DHA market during the forecast period, since the regulatory environment in the region supports the same and there is a surge in demand among consumers for preventive health solutions.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The market of EPA and DHA is fiercely competitive, wherein the key leading players in the market, DSM, BASF SE, KD Pharma Group, and Archer Daniels Midland Company, are focusing on innovation, strategic partnership development, and expansion.

The two leading companies, DSM and BASF SE are well-positioned within the value chain of omega-3 ingredients, offering products ranging from dietary supplements to pharmaceutical-grade solutions in food fortification. With growing concerns over sustainability, these two companies are popular for substantial venture investments in algae oil production as a means of reducing dependency on fish oil.

The other major players are like KD Pharma Group, recognized, especially for developing high-purity omega-3 oils. The company has developed innovative technologies of extraction applied to the preparation of highly concentrated products with a high content of EPA and DHA. It produces high-concentration EPA/DHA products for the nutraceutical and pharmaceutical market segments. Its focus on product purity and bioavailability made KD Pharma Group a key player in the high-end omega-3 supplement market.

The competitive landscape also features regional players, especially in the Asia Pacific region, where local manufacturers, with their cost-effective methods of production and strong distribution networks, are posting gains in market share.

This is because regional players can sell their omega-3 products at cheaper prices and hence make them more accessible to the rising middle class in emerging markets. As demand for omega-3 grows globally, it will become increasingly competitive, a space in which companies have to strategize on product differentiation and sustainability in addition to technological enhancements.

Some of the prominent players in the Global EPA and DHA Market are

- Archer Daniels Midland Company

- Koninklijke DSM N.V.

- BASF SE

- Croda International Plc.

- Corbion N.V.

- Golden Omega S.A.

- Novasep Holding SAS

- Arctic Nutrition AG

- Organic Technologies

- Pelagia AS

- Other Key Players

Recent Developments

- March 2024: DSM announced a strategic partnership with a leading nutraceutical company to develop a new range of algae oil-based omega-3 supplements. This collaboration aims to address the growing demand for sustainable and plant-based health solutions, particularly among vegan and environmentally conscious consumers.

- January 2024: BASF SE expanded its omega-3 production capacity by opening a new state-of-the-art facility in Asia Pacific. The new plant is designed to meet the rising regional demand for EPA and DHA supplements, particularly in emerging markets like China and India.

- December 2023: KD Pharma Group launched a new line of high-purity omega-3 supplements, targeting the pharmaceutical market. The new product line is designed to address specific health concerns such as hyperlipidemia and chronic inflammation, with higher concentrations of EPA and DHA to deliver enhanced therapeutic benefits.

- October 2023: Archer Daniels Midland Company announced the development of a new encapsulation technology that improves the stability and shelf life of fish oil supplements. This technology reduces oxidation, ensuring that EPA and DHA retain their potency over time.

Report Details

| Report Characteristics |

| Market Size (2024) |

USD 3,576.4 Mn |

| Forecast Value (2033) |

USD 9,463.0 Mn |

| CAGR (2024-2033) |

11.4% |

| Historical Data |

2018 – 2023 |

| The US Market Size (2024) |

USD 905.3 Mn |

| Forecast Data |

2025 – 2033 |

| Base Year |

2023 |

| Estimate Year |

2024 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Type (Eicosapentaenoic Acid (EPA), and Docosahexaenoic Acid (DHA)), By Source (Animal Source, and Plant Source), By Form (Triglyceride (TG) Form, Ethyl Ester (EE) Form, Free Fatty Acid (FFA) Form, and Phospholipid Form), By Application (Dietary Supplements, Infant Formula, Functional Foods and Beverages, Pharmaceuticals, Animal Feed, Personal Care and Cosmetics, and Other Applications) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia- Pacific– China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA

|

| Prominent Players |

Archer Daniels Midland Company, Koninklijke DSM N.V., BASF SE, Croda International Plc., Corbion N.V., Golden Omega S.A., Novasep Holding SAS, Arctic Nutrition AG, Organic Technologies, Pelagia AS, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

The Global EPA and DHA Market size is estimated to have a value of USD 3,576.4 million in 2024 and is expected to reach USD 9,463.0 million by the end of 2033.

The US EPA and DHA Market is projected to be valued at USD 905.3 million in 2024. It is expected to witness subsequent growth in the upcoming period as it holds USD 2,260.6 million in 2033 at a CAGR of 10.7%.

Asia Pacific is expected to have the largest market share in the Global EPA and DHA Market with a share of about 34.1% in 2024.

Some of the major key players in the Global EPA and DHA Market are Koninklijke DSM N.V., BASF SE, Croda International Plc., Corbion N.V., Golden Omega S.A., and many others.

The market is growing at a CAGR of 10.7 percent over the forecasted period.