What is the Fertility Treatment Market Size?

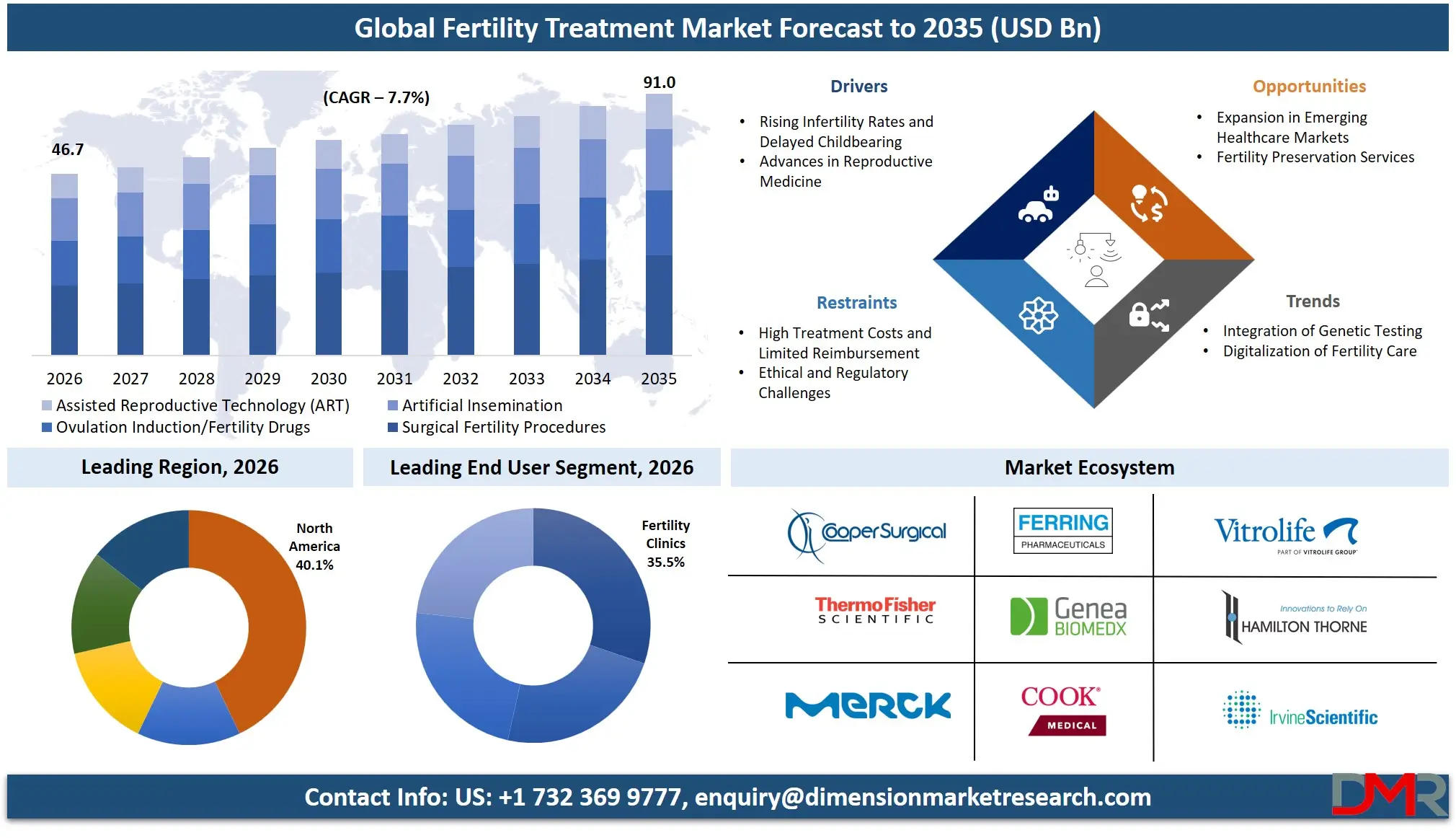

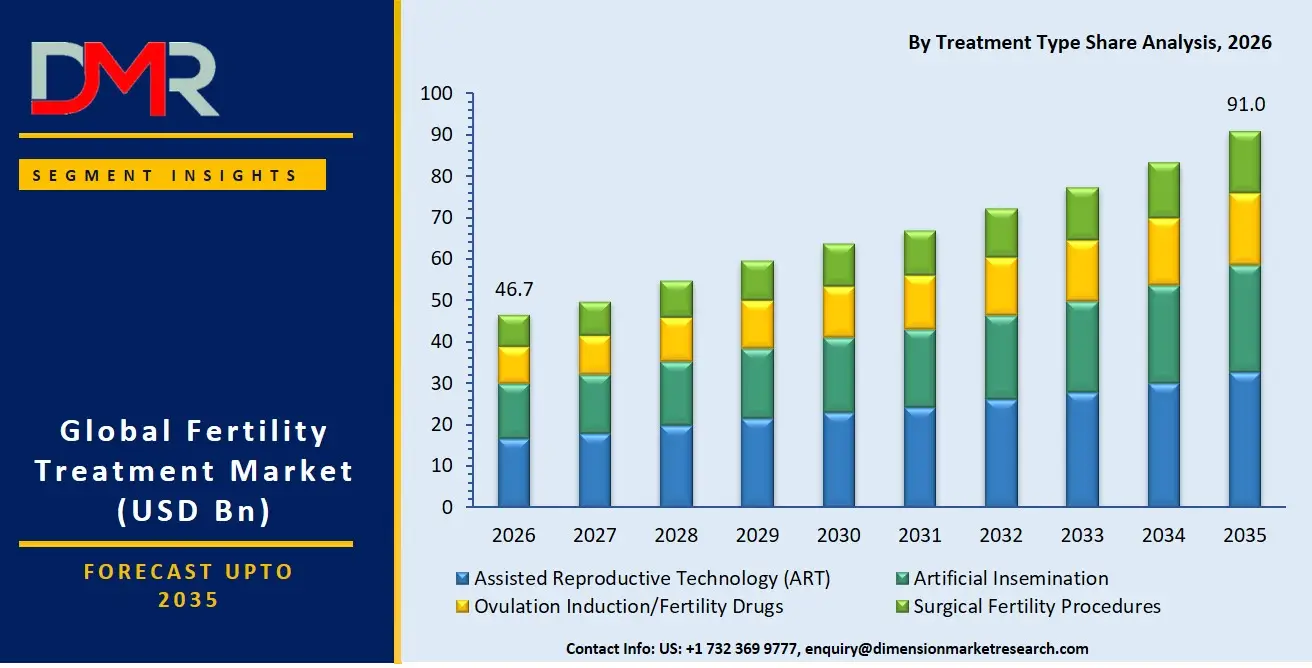

The Global Fertility Treatment Market is expected to reach a value of USD 46.7 billion in 2026, and it is further anticipated to reach USD 91.0 billion by 2035, growing at a CAGR of 7.7% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The fertility treatment market has been expanding significantly, driven by the rising global median age of first-time parents and the increasing prevalence of reproductive health disorders. The market consists of Assisted Reproductive Technology (ART) procedures, artificial insemination, pharmaceutical interventions, and surgical corrections that assist individuals and couples in achieving pregnancy. The growing societal acceptance of third-party reproduction, including donor eggs, sperm, and gestational surrogacy, alongside the trend of elective fertility preservation via Embryo or Egg Banking, is driving the necessity for specialized clinical services. Heterosexual couples facing infertility are the most frequent patients, with In Vitro Fertilization (IVF) remaining the most sought-after ART procedure due to its high success rates and technological advancements. Fertility Clinics, Hospitals, and Surgical Centers are key stakeholders as they require advanced embryology laboratories, cryopreservation facilities, and genetic screening capabilities to support complex treatment cycles.

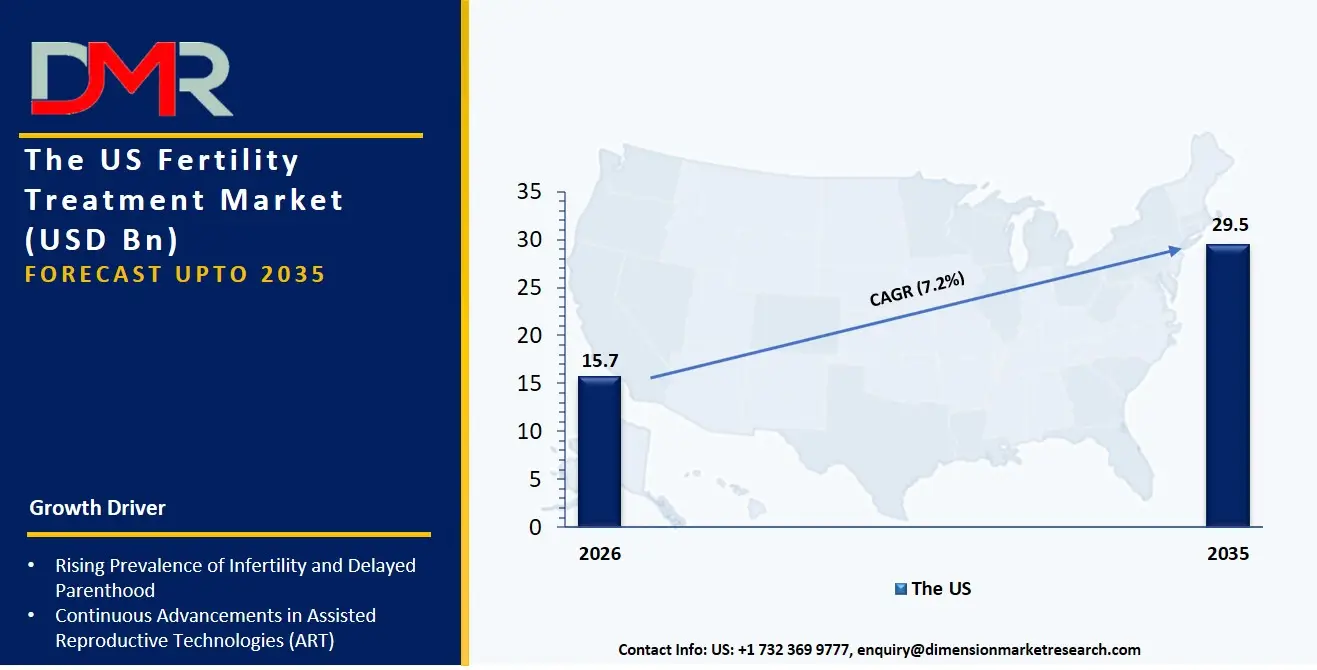

The US Fertility Treatment Market

The US Fertility Treatment Market is projected to reach USD 15.7 billion in 2026 at a compound annual growth rate of 7.2% over its forecast period, culminating in a value of USD 29.5 billion by 2035. The US remains the largest and most commercially mature market in fertility treatment globally, characterized by robust corporate insurance coverage mandates for fertility preservation and the aggressive expansion of private equity-backed fertility clinic chains.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The market has been typified by high demand for genetic testing of embryos, whereby Preimplantation Genetic Testing (PGT) is bundled with Frozen Embryo Transfer (FET) cycles to optimize single-embryo transfer outcomes. Besides, the destigmatization of Male Infertility is driving a parallel surge in demand for Intracytoplasmic Sperm Injection (ICSI) and advanced sperm retrieval technologies.

The Europe Fertility Treatment Market

The Europe Fertility Treatment Market is estimated to be valued at USD 13.5 billion in 2026 and is further anticipated to witness substantial growth, driven by progressive public health funding models in nations like Spain and the UK, alongside the rise of cross-border reproductive care (fertility tourism). The regulatory frameworks, including the European Union's Tissues and Cells Directives, significantly impact the European market and drive the need for standardized cryogenic storage protocols in Embryo or Egg Banking. Accelerated growth in the Frozen Donor segment is also being experienced in the region as single women and same-sex female couples in Scandinavia and Western Europe increasingly seek donor sperm treatments. In addition, legislative shifts toward transparency and the removal of donor anonymity in some countries are challenging service providers to create dedicated patient counseling services to navigate the psychological and legal implications of third-party reproduction.

The Japan Fertility Treatment Market

The Japan Fertility Treatment Market is projected to be valued at USD 2.8 billion in 2026. It is further expected to witness robust growth, fueled by a national demographic crisis and the government's landmark decision to expand national health insurance subsidies for IVF and ICSI treatments. The Japanese market is unique, with a cultural impetus to address declining birth rates directly through accessible Assisted Reproductive Technology (ART). Ovulation Induction and timed intercourse cycles, coupled with Intrauterine Insemination (IUI), constitute a significant portion of early-stage interventions before patients advance to more invasive treatments. There is also a strong need to integrate minimally invasive Surgical Fertility Procedures to address the high prevalence of uterine fibroids and endometriosis in the Japanese female population, forming a niche in robot-assisted laparoscopic surgery.

Key Takeaways

- Market Size & Forecast: The Global Fertility Treatment market is projected to reach USD 46.7 billion in 2026, expanding steadily to USD 91.0 billion by 2035, fueled by the dual drivers of delayed childbearing and the clinical normalization of advanced reproductive technologies like egg vitrification.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 7.7%, driven by a critical shortage of reproductive endocrinologists globally and the escalating technical complexity of managing embryology laboratories and genetic screening workflows.

- Primary Growth Drivers: Key forces include the widespread societal trend of family planning postponement, the increasing medical necessity for Fertility Preservation (Egg Banking) before oncological treatments, and the rising demand for ICSI to overcome severe male factor infertility.

- Key Market Trends: Major trends include the integration of artificial intelligence (AI) for embryo selection in IVF laboratories, the use of time-lapse incubator technologies within embryology, and a significant shift toward Frozen Embryo Transfers to enhance endometrial-embryo synchrony.

- By Procedure Type Analysis: Frozen Donor and Frozen non-Donor cycles are dominating clinical protocols due to the proven safety and efficacy of vitrification. Professional services and clinic workflows are increasingly required to build seamless cryogenic chain-of-custody systems that protect gametes and embryos.

- By End User Analysis: Fertility Clinics and Hospitals are the most lucrative end-user verticals due to stringent quality control needs mandated by accrediting bodies. Clinical Research Institutes are the fastest-growing segment as pharmaceutical pipelines for novel gonadotropins and non-hormonal fertility drugs expand.

- Regional Leadership: North America is poised to dominate this market with 40.1% of the market share in 2026 due to its well-developed technological ecosystem, aggressive insurance coverage mandates, and a deep concentration of sophisticated fertility clinic chains that utilize cutting-edge ART to its fullest potential.

What is the Fertility Treatment?

Fertility Treatments are the specialized medical and surgical interventions offered by reproductive endocrinologists, embryologists, and support staff to assist individuals in achieving conception and live birth. These services, unlike standard obstetric care (which manages pregnancy after conception), are related to the diagnosis and overcoming of biological barriers to pregnancy. This involves Assisted Reproductive Technology (ART) to handle the fertilization process in a laboratory setting, Artificial Insemination to place sperm directly into the uterus, and Ovulation Induction to stimulate follicular development pharmaceutically. With global infertility rates affecting roughly 1 in 6 individuals, professional fertility services are needed to navigate complex immunological, genetic, and anatomical barriers, ensuring that clinical investments translate into tangible emotional results and healthy singleton births, as opposed to high-risk multiple gestations.

Use Cases

- Severe Male Factor Infertility Resolution: Andrology laboratories utilize Intracytoplasmic Sperm Injection (ICSI) to overcome severe oligoasthenoteratozoospermia, allowing embryologists to select a single viable sperm for direct microinjection into a mature oocyte, bypassing natural acrosome reactions.

- Oncofertility Preservation: Oncology networks refer patients to Fertility Clinics for Emergency Embryo or Egg Banking before initiating gonadotoxic chemotherapy or radiation, utilizing rapid-cycle ovarian stimulation protocols to freeze gametes without delaying cancer treatment.

- Genetic Disease Prevention: Couples with known carrier status for heritable diseases utilize ART cycles with Frozen Donor gametes or their own embryos after Preimplantation Genetic Testing for Monogenic disorders (PGT-M) to prevent the transmission of conditions like cystic fibrosis or Huntington's disease.

- Tubal Factor Infertility Bypass: Patients with severe bilateral tubal occlusion or pelvic adhesions completely bypass the fallopian tubes through In Vitro Fertilization (IVF), where oocyte retrieval and embryo transfer render tubal patency clinically irrelevant.

How AI is Transforming the Fertility Treatment Market?

AI is changing the fertility treatment landscape by accelerating the standardization of embryo selection, as well as enhancing laboratory operational efficiency. In ART procedures, AI-based computer vision tools have the potential to assess thousands of time-lapse embryo images non-invasively, algorithmically predicting ploidy status and implantation potential, significantly reducing inter-embryologist variability and selection timelines. Meanwhile, AI-powered workflow optimization in cryobanks allows clinics to better manage liquid nitrogen tank logistics by detecting temperature anomalies, predicting future storage capacity, and automating compliance tracking to reinforce chain-of-custody best practices.

Clinical decision support and patient triage are also revolving around AI. In the area of Ovulation Induction, intelligent predictive analytics are used to continuously monitor follicular tracking data and endocrine assays to suggest personalized gonadotropin dosing adjustments, keeping patients within a safe response window to avoid ovarian hyperstimulation syndrome (OHSS). Moreover, generative AI patient assistants are complementing fertility awareness by simulating treatment timelines and visualizing potential financial cost pathways, giving stakeholders a clearer visualization of the treatment burden before committing to an invasive cycle.

Market Dynamics

Key Drivers in the Global Fertility Treatment Market

Rising Infertility Rates and Delayed Childbearing

Increasing infertility prevalence, coupled with a global trend toward later parenthood, is a primary driver of the fertility treatment market. Lifestyle changes, stress, obesity, environmental exposures, and age-related declines in reproductive capacity have expanded the pool of patients seeking assistance. As more individuals postpone family formation for educational and career reasons, demand for advanced reproductive services continues to rise. Greater awareness of infertility as a treatable medical condition and improved access to specialized care further support market growth. Together, these demographic and societal shifts are sustaining robust demand for fertility treatments across both developed and emerging economies worldwide.

Advances in Reproductive Medicine

Continuous innovation in assisted reproductive technologies has significantly improved treatment success rates and patient experiences. Enhanced embryo culture systems, preimplantation genetic testing, cryopreservation techniques, and minimally invasive procedures enable more personalized and effective care. These advancements increase clinician confidence and encourage broader patient adoption. In parallel, digital tools for monitoring and treatment planning streamline clinical workflows and improve outcomes. As technology continues to reduce risks and enhance efficiency, fertility treatments are becoming increasingly accessible and acceptable, reinforcing their role as a cornerstone of modern reproductive healthcare and driving sustained expansion of the global fertility treatment market.

Restraints in the Global Fertility Treatment Market

High Treatment Costs and Limited Reimbursement

Fertility treatments, particularly ART procedures, often involve substantial out-of-pocket expenses. In many countries, insurance coverage remains limited or absent, creating financial barriers for prospective patients. Multiple treatment cycles may be required, further increasing the economic burden. These cost considerations can delay care or discourage individuals from pursuing treatment altogether. Clinics also face significant operational expenses associated with maintaining advanced laboratories and specialized staff. Consequently, affordability remains a major constraint on market penetration, especially in lower-income regions where healthcare budgets are limited and public reimbursement policies for infertility services are still evolving.

Ethical and Regulatory Challenges

The fertility treatment industry operates within a complex framework of ethical, cultural, and legal considerations. Regulations governing embryo handling, gamete donation, surrogacy, and genetic testing vary widely across jurisdictions, creating uncertainty for providers and patients. Public debates surrounding these issues can influence policy changes and affect treatment availability. Compliance with stringent standards also increases administrative burdens and operational costs for clinics. While oversight is essential for patient safety and ethical practice, inconsistent regulatory environments may slow innovation and limit the adoption of new reproductive technologies, thereby restraining overall market growth.

Growth Opportunities in the Global Fertility Treatment Market

Expansion in Emerging Healthcare Markets

Rapid improvements in healthcare infrastructure and rising disposable incomes in emerging economies are creating new opportunities for fertility service providers. Governments and private investors are increasing support for reproductive healthcare, while growing awareness encourages earlier diagnosis and treatment. Establishing clinics and training specialists in underserved regions can significantly expand patient access. Partnerships with local healthcare systems further facilitate market entry and service delivery. As cultural acceptance of fertility treatment increases and healthcare capacity improves, emerging markets are poised to become important engines of future growth for the global fertility treatment industry.

Fertility Preservation Services

Demand for fertility preservation is increasing among individuals seeking to delay parenthood, undergo cancer therapy, or safeguard reproductive options for personal reasons. Advances in egg, sperm, and embryo cryopreservation have improved reliability and broadened clinical applications. Employers and insurers in some regions are beginning to include preservation benefits, enhancing accessibility. This expanding service category provides clinics with new revenue streams and attracts younger patient populations. Continued innovation in storage and thawing techniques is expected to further strengthen the appeal of fertility preservation, making it one of the most promising growth areas within reproductive medicine.

Trends in the Global Fertility Treatment Market

Integration of Genetic Testing

Preimplantation genetic testing is increasingly being incorporated into fertility treatment protocols to improve embryo selection and reduce the risk of inherited disorders. The ability to identify chromosomally normal embryos enhances implantation success and may reduce the number of treatment cycles required. Patients and clinicians alike value the additional information provided by these technologies. As testing methods become more accurate and accessible, their use is expanding beyond high-risk cases to broader patient populations. This integration of genetics into routine fertility care is reshaping clinical decision-making and represents a defining trend in the evolving fertility treatment market.

Digitalization of Fertility Care

Telemedicine, mobile applications, and data-driven monitoring tools are transforming the delivery of fertility services. Patients can now access consultations, track treatment progress, and receive personalized guidance remotely, improving convenience and engagement. Clinics benefit from enhanced workflow efficiency and more comprehensive patient data. Artificial intelligence is also being explored for embryo assessment and treatment optimization. These digital innovations support continuity of care and broaden access to specialized services, particularly in regions with limited fertility expertise. The ongoing digital transformation of reproductive healthcare is therefore emerging as a major trend influencing the future of fertility treatment.

Research Scope and Analysis

The global fertility treatment market is segmented by treatment type into assisted reproductive technology including IVF, ICSI, and frozen embryo transfer, artificial insemination comprising IUI and ICI, ovulation induction and fertility drugs, and surgical procedures. Additional segments include female and male infertility, procedure type, and end users comprising fertility clinics, hospitals, surgical centers, and clinical research institutes.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Treatment Type Analysis

Assisted Reproductive Technology is projected to dominate the fertility treatment market due to its high success rates and broad applicability to both male and female infertility. Within ART, IVF is the leading procedure, supported by continuous improvements in embryo culture, cryopreservation, and genetic testing.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

ART is increasingly favored by clinicians and patients because it offers personalized treatment options and reliable outcomes, particularly for complex infertility cases. Delayed parenthood, rising infertility prevalence, and expanding insurance coverage in select markets further strengthen demand. The growing availability of specialized fertility centers and ongoing technological innovation continue to reinforce ART's position as the largest and most influential treatment segment.

By Gender/Patient Type Analysis

Female infertility is poised to represent the dominant patient segment, reflecting the high frequency of diagnoses involving ovulatory disorders, age-related fertility decline, and reproductive tract conditions. Women are also the primary recipients of most fertility interventions, including ovulation induction, IVF, and embryo transfer procedures. Increased awareness, improved access to reproductive healthcare, and a societal trend toward delayed childbearing have contributed to greater utilization of fertility services among female patients. Comprehensive diagnostic pathways and established treatment protocols further support this segment's leadership. Consequently, female infertility remains the principal focus of clinical practice and research within the global fertility treatment market.

By Procedure Type Analysis

Fresh non-donor cycles are expected to dominate procedure volumes owing to their longstanding clinical acceptance and use of patients' own gametes, which many individuals prefer for personal and ethical reasons. These procedures benefit from well-established protocols and widespread availability across fertility clinics. Although frozen and donor cycles are expanding rapidly, fresh non-donor treatments remain a foundational option, particularly for first-time patients with favorable prognoses. Advances in ovarian stimulation and embryo selection have further improved outcomes, sustaining their popularity. As a result, fresh non-donor procedures maintain the largest share of activity in the global fertility treatment market.

By End User Analysis

Fertility clinics are projected to dominate the end-user landscape because they offer specialized expertise, dedicated laboratory infrastructure, and comprehensive reproductive services under one roof. Their focus on assisted reproductive technologies enables high procedure volumes and consistent clinical outcomes. Many clinics invest heavily in advanced equipment, embryology capabilities, and patient support programs, enhancing treatment success and satisfaction. The increasing preference for specialized centers over general hospitals for infertility care further reinforces their leadership. Expanding clinic networks and partnerships with research institutions continue to strengthen this segment, ensuring that fertility clinics remain the primary setting for fertility diagnosis and treatment worldwide.

The Global Fertility Treatment Market Report is segmented on the basis of the following:

By Treatment Type

- Assisted Reproductive Technology (ART)

- In Vitro Fertilization (IVF)

- Intracytoplasmic Sperm Injection (ICSI)

- Frozen Embryo Transfer (FET)

- Artificial Insemination

- Intrauterine Insemination (IUI)

- Intracervical Insemination (ICI)

- Ovulation Induction/Fertility Drugs

- Surgical Fertility Procedures

By Gender/Patient Type

- Female Infertility

- Male Infertility

By Procedure Type

- Fresh non-Donor

- Frozen non-Donor

- Fresh Donor

- Frozen Donor

- Embryo or Egg Banking

By End User

- Fertility Clinics

- Hospitals

- Surgical Centers

- Clinical Research Institutes

Regional Analysis

Leading Region by Market Share

ℹ

To learn more about this report –

Download Your Free Sample Report Here

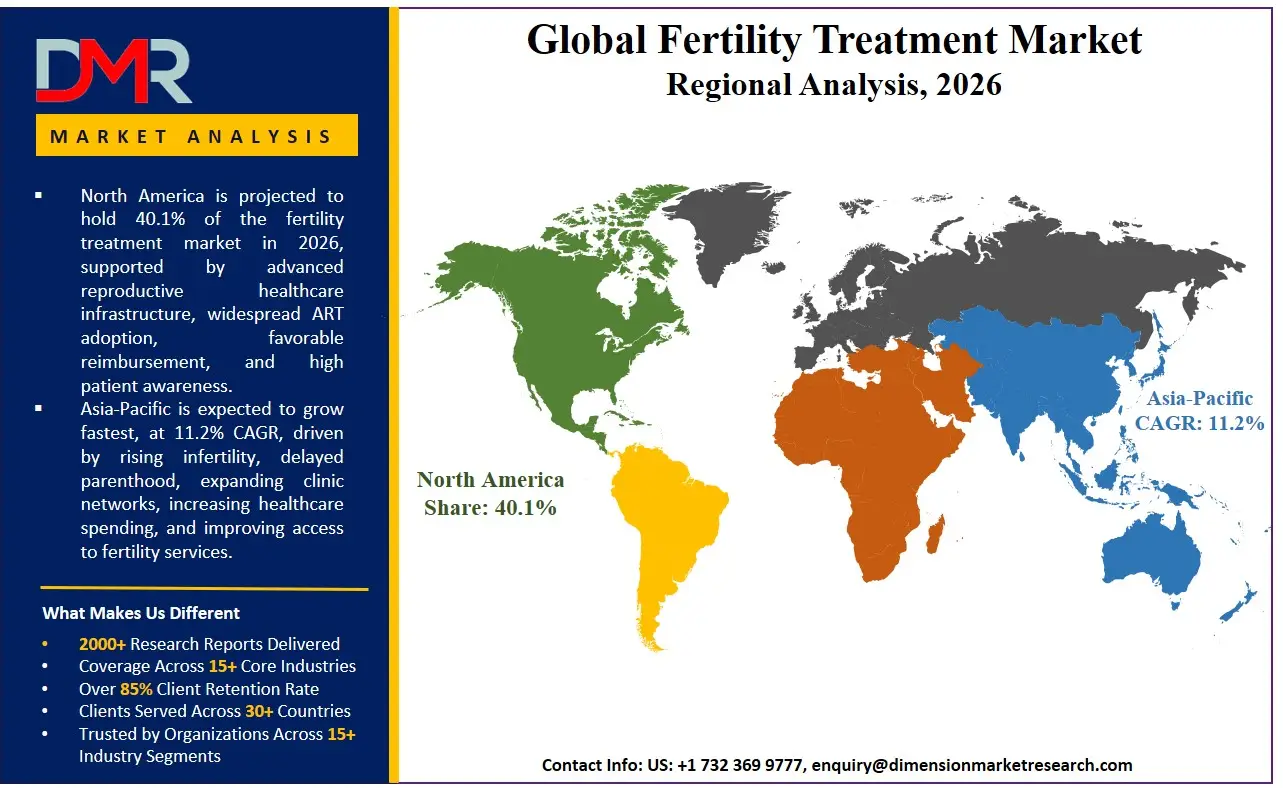

North America is poised to dominate the global fertility treatment market as it is projected to hold 40.1% of the market share by the end of 2026. The United States, which dominates North America, has the highest share in the fertility treatment market because of the unmatched concentration of venture-funded private fertility chains and the aggressive family-building mandates of Fortune 500 employee benefit packages. The region has an established ecosystem of global reproductive tissue banks, high-complexity reference andrology labs, and a rich pool of Board-Certified Reproductive Endocrinologists and embryologists. Enterprise investment in genetic testing, advanced blastomere biopsy, and the general transition to single-embryo transfer protocols contribute to the continued demand for Frozen Donor and non-Donor cycles along with continuous genetic counseling. Moreover, a favorable regulatory climate under the FDA and ASRM guidelines persistently finances upcoming fertility-tech startups that require expert professional services to achieve rapid patient acquisition and CLIA compliance.

Fastest-Growing Regional Market

Asia-Pacific is expected to be the most rapidly expanding fertility treatment market, driven by the government-led sweeping pro-natalist policies to reverse collapsing birth rates in China, India, Japan, and South Korea. The fast-paced relaxation of ART regulations, the rise of a medical tourism middle-income population, and the dynamic expansion of the digital health economy is compelling established corporate hospital chains and state agencies to discard outdated low-throughput insemination protocols. Fertility Clinics specializing in IVF and ICSI are in high demand to help these large demographic transitions head in the direction of high-throughput, automation-driven embryology operating models. There is also a severe lack of qualified senior embryologists in the region, and it is necessary to outsource professional training and laboratory design services to cover the technical skills gap and enable faster investments in complex ART projects.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive environment of the global fertility treatment market has become highly dynamic with a heterogeneous array of multinational fertility clinic networks (IVF chains), specialized andrology diagnostics providers, and niche laboratory automation manufacturers. The key to success will be the profound strategic alliances with gynecologic referring physicians and large self-insured employers because they will open the necessary direct-to-consumer awareness channels and early access to the new at-home diagnostic capabilities. The movement towards market consolidation is rapidly progressing with the traditional hospital-based reproductive departments acquiring independent boutique clinics specializing in reproductive immunology and Male Infertility microsurgery to stay afloat. Proprietary intellectual property, including automated vitrification devices and AI-based embryo annotation algorithms, is becoming a more important basis of competitive differentiation than just standard blastocyst grading or generic 3D transvaginal ultrasound imaging.

Some of the prominent players in the Global Fertility Treatment Market are:

- Merck KGaA

- Ferring Pharmaceuticals

- CooperSurgical

- Vitrolife

- Cook Medical

- FUJIFILM Irvine Scientific

- Thermo Fisher Scientific

- Hamilton Thorne

- Genea Biomedx

- Esco Medical

- Kitazato Corporation

- IVFtech

- Progyny

- Monash IVF Group

- Virtus Health

- The Prelude Network

- IVIRMA Global

- OvaScience

- EMD Serono

- Organon & Co.

- Other Key Players

Recent Developments

- January 2026: Vitrolife AB expanded deployment of its AI-enabled embryo assessment platforms across IVF clinics, strengthening data-driven embryo selection and supporting improved treatment outcomes.

- October 2025: Monash IVF Group continued expanding its clinic network in the Asia–Pacific region to address rising demand for assisted reproductive technologies.

- July 2025: CooperSurgical, Inc. broadened the availability of advanced vitrification solutions for oocyte and embryo cryopreservation, enhancing post-thaw viability.

- March 2025: Progyny, Inc. expanded employer-sponsored fertility benefits programs, increasing access to IVF and fertility preservation services for covered employees.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 46.7 Bn |

| Forecast Value (2035) |

USD 91.0 Bn |

| CAGR (2026–2035) |

7.7% |

| The US Market Size (2026) |

USD 15.7 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Treatment Type, By Gender/Patient Type, By Procedure Type, and By End User |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Fertility Treatment Market?

▾ The Global Fertility Treatment market is poised to be valued at USD 46.7 billion in 2026 and is projected to reach USD 91.0 billion by 2035, driven by the universal trend of delayed childbearing, rising infertility prevalence, and the growing societal acceptance of Assisted Reproductive Technology (ART) and elective fertility preservation.

What is the CAGR of the Global Fertility Treatment Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 7.7% from 2026 to 2035, reflecting the accelerating demand for advanced embryology techniques, genetic testing integration, and the persistent shortage of reproductive endocrinologists globally.

What factors are driving the growth of the Global Fertility Treatment Market?

▾ Key drivers include the sociocultural shift toward advanced maternal age, the global shortage of specialized fertility clinicians, the management complexity of multi-cycle ART protocols, the rising incidence of male factor infertility, and the surge in demand for Egg and Embryo Banking amid expanding employer-sponsored fertility preservation benefits.

Which region held the largest share of the Fertility Treatment Market in 2026?

▾ North America, specifically the United States, held 40.1% of the market share in 2026, driven by a mature private equity-backed fertility clinic ecosystem, aggressive corporate insurance coverage mandates, and deep enterprise investment in Frozen Embryo Transfer (FET) and Preimplantation Genetic Testing (PGT) capabilities.

Which region is expected to grow the fastest in the Fertility Treatment Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by pro-natalist government subsidies expanding IVF access in Japan, China, and South Korea, where Fertility Clinics and ART procedures are critical for transitioning large patient populations to high-throughput embryology operating models.

What are the major trends in the Global Fertility Treatment Market?

▾ Major trends include the integration of AI for non-invasive embryo selection and annotation, the rise of planned Freeze-All cycles and Frozen Embryo Transfer (FET) protocols, the demand for lab automation and microfluidic technologies, and the growing clinical focus on Male Infertility specialization through advanced Intracytoplasmic Sperm Injection (ICSI) and surgical sperm retrieval.

Who are the key players in the Global Fertility Treatment Market?

▾ Key players include multinational fertility clinic networks such as Virtus Health, IVI-RMA Global, and Monash IVF Group; specialized andrology diagnostics and equipment providers like Hamilton Thorne and CooperSurgical (The Cooper Companies); reproductive tissue cryobanks such as California Cryobank and Fairfax EggBank; and niche laboratory automation manufacturers including Vitrolife and Cook Medical.

How is the Global Fertility Treatment Market segmented?

▾ The market is segmented by Treatment Type, by Gender/Patient Type, by Procedure Type, and by End User.