What is the Genetic Testing Market Size?

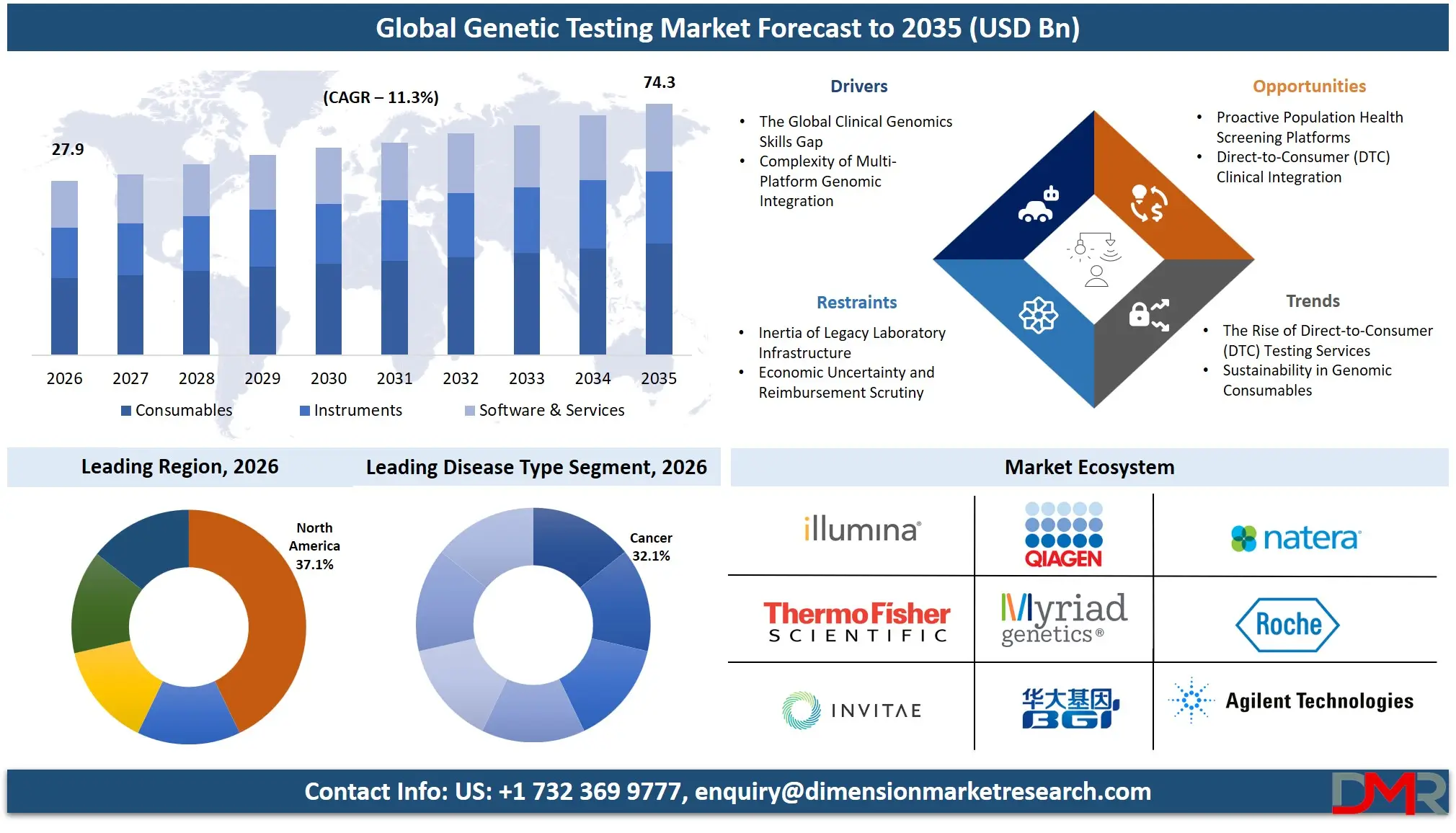

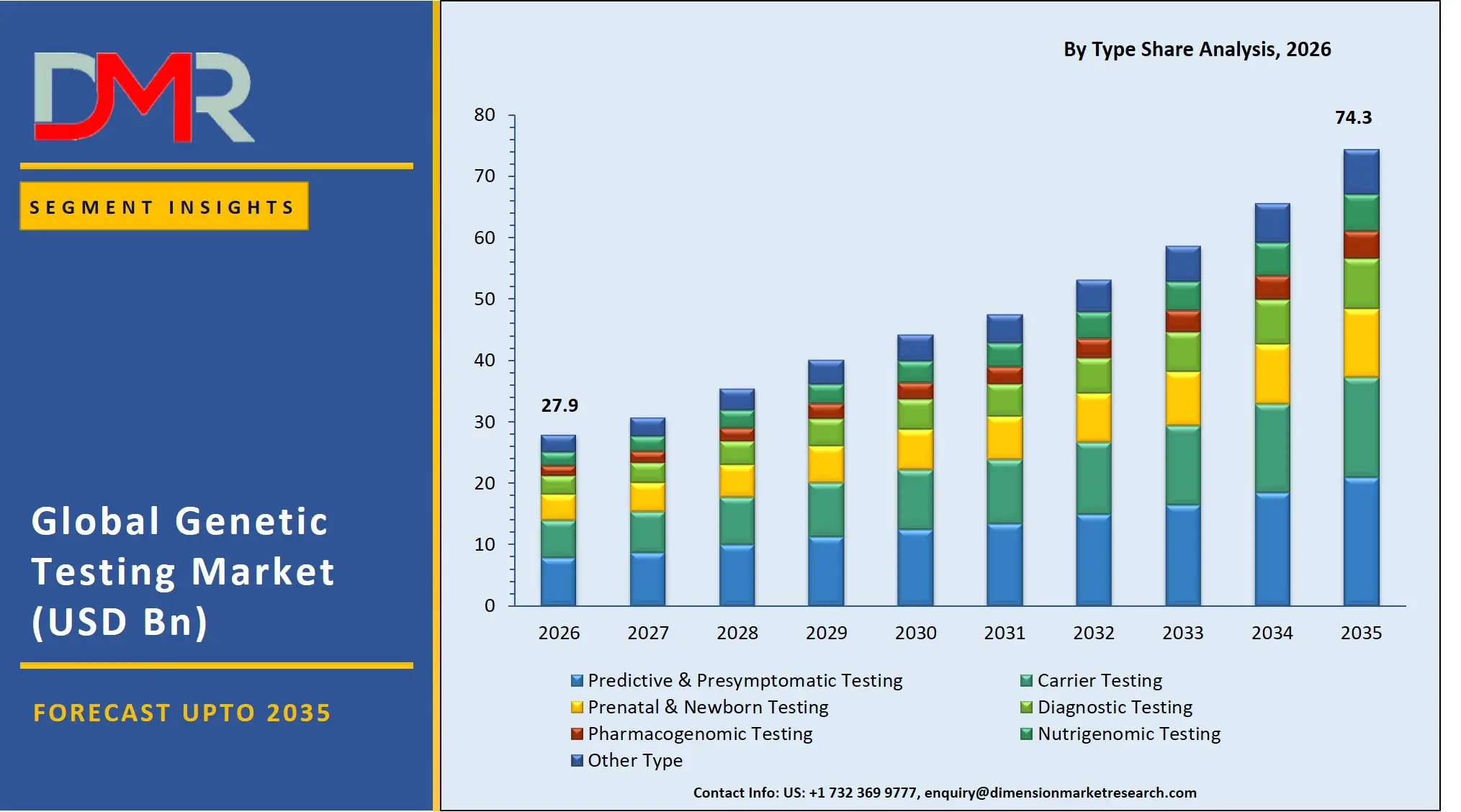

The Global Genetic Testing Market is expected to reach a value of USD 27.9 billion in 2026, and it is further anticipated to reach USD 74.3 billion by 2035, growing at a CAGR of 11.5% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The genetic testing market has been experiencing a high growth rate with the further integration of genomics into clinical care, the rising consumer interest in personalized health, and the ever-falling cost of sequencing. The market comprises of consumables, instruments, and software and services that will aid in the analysis of DNA and RNA to find diagnostic, predictive, and research uses.

The growing need to build precision medicine initiatives, comprehend intricate disease ailment dispositions, and create specific therapies is fueling the requirement of special genetic analysis solutions. The most common adopters are healthcare systems and NGS and PCR-based testing are the most popular as they are accurate and have expanding clinical utility. Hospitals & clinics, diagnostic laboratories, and research institutes are key players as they require high-throughput, accurate, and clinically validated genomic analysis ecosystems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

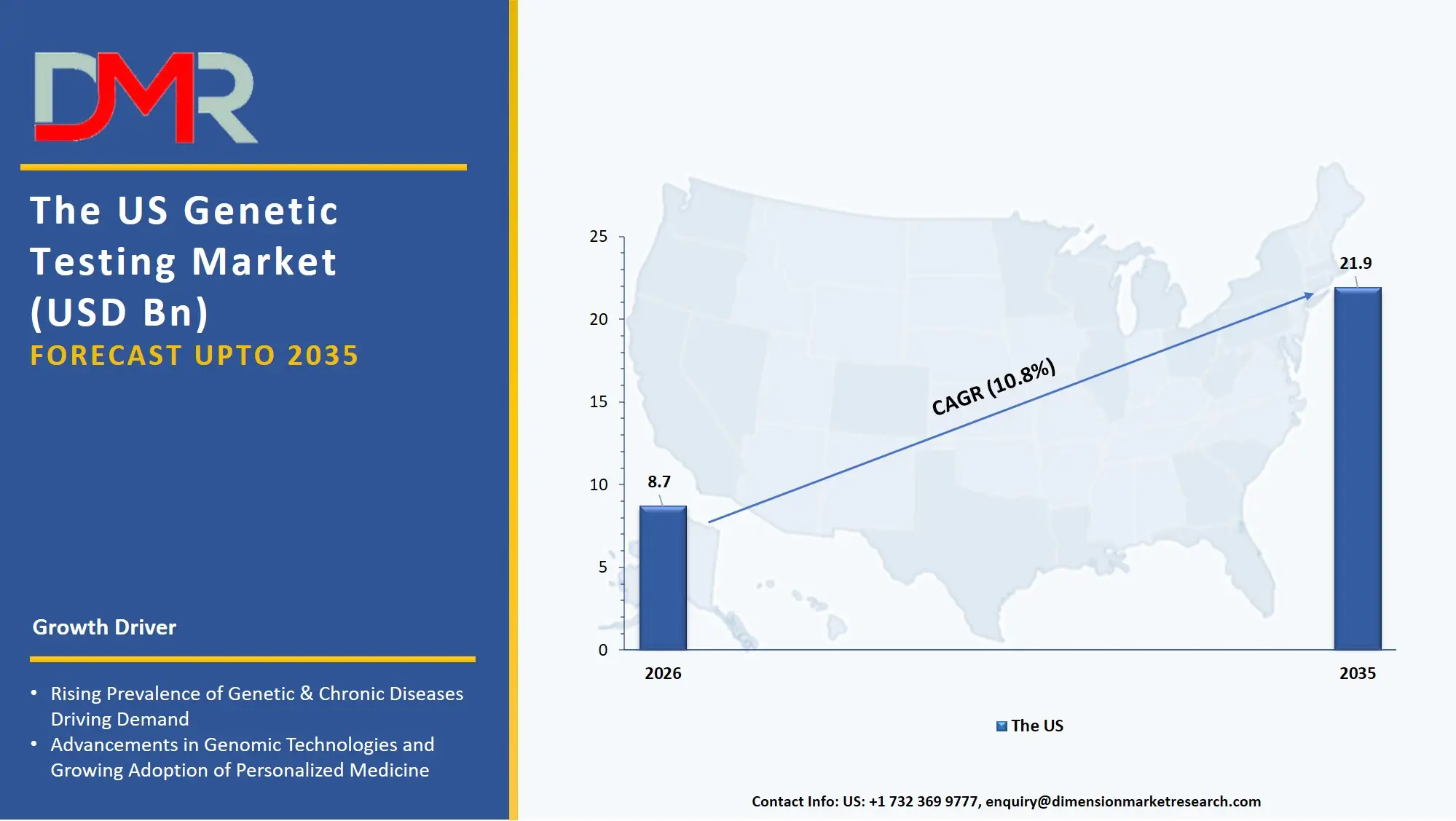

The US Genetic Testing Market

The US Genetic Testing Market is projected to reach USD 8.7 billion in 2026 at a compound annual growth rate of 10.8% over its forecast period, which is further poised to be valued at USD 21.9 billion by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US remains the largest and most advanced market in genetic testing because of the proactive modernization of national screening programs, and the increasing distribution of clinical genomic laboratories. High demand of predictive and presymptomatic testing services whereby people are targeted to comprehend their inherited risk of developing conditions such as hereditary cancer and Alzheimer disease has typified the market. In addition, the application of pharmacogenomic therapies to clinical practice workflows is generating a parallel requirement in special laboratory testing services to control drug-gene interactions and accuracy prescribing models in healthcare.

The Europe Genetic Testing Market

The Europe Genetic Testing Market is estimated to be valued at USD 8.1 billion in 2026 and is further anticipated to reach USD 21.1 billion by 2035 at a CAGR of 11.2%. The regulatory frameworks including IVDR (In Vitro Diagnostic Regulation) and the GDPR have a significant impact on the European market and drive the need to employ clinical decision support software and certified sequencing reagents. Accelerated growth of non-invasive prenatal testing (NIPT) services is also being experienced in the region as healthcare systems in Germany and France are trying to strike a balance in ethical oversight with advanced genomic diagnostics. In addition, efforts such as the 1+ Million Genomes Initiative are challenging service providers to create dedicated bioinformatics software to provide data residency and interoperability across European genomic ecosystems.

The Japan Genetic Testing Market

The Japan Genetic Testing Market is projected to be valued at USD 2.9 billion in 2026. It is further expected to witness robust growth, holding USD 7.3 billion in 2035 at a CAGR of 10.5%. The Japanese market is a special kind of market with a corporate pressure on implementing genomic medicine in the market in response to an aging population and prevalence of age related cancers. A big portion of the expenditure is comprised of diagnostic testing and laboratory testing services which are migrating towards comprehensive NGS-based panel testing. It is also strongly needed to immerse deep in the local market to bridge the gaps between the traditional cytogenetic analysis tools and new automated liquid handling systems, which is a niche in the context of laboratory automation and the automation of clinical workflows.

Key Takeaways

- Market Size & Forecast: The Global Genetic Testing market is projected to reach USD 27.9 billion in 2026, expanding dramatically to USD 74.3 billion by 2035, driven by the two drivers of adoption of clinical diagnostic and empowerment of consumers in managing their personal health.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 11.5%, due to critical expansion of clinically actionable gene panels and the growing complexity of interpreting variants of uncertain significance (VUS) and managing large-scale genomic data.

- Primary Growth Drivers: Major drivers include the pervasive shift in the paradigm of reactive to proactive health risk assessment, the necessity of the provision of the services of genetic counseling in order to contextualize the complex results, and the integration of genomics into the routine oncology care requiring special assay kits.

- Key Market Trends: Major trends include the rise of direct-to-consumer (DTC) genetic testing services, the use of AI-powered tools within bioinformatics software to auto-classify genomic variants, and the shift towards pharmacogenomic testing as payers prioritize medication efficacy and safety.

- By Product Analysis: Consumables, specifically sequencing reagents and DNA/RNA extraction and purification kits are expected to take majority share in this segment given the high throughput and recurring purchase nature of clinical and research testing.

- By Technology Analysis: Next-Generation Sequencing (NGS) and PCR-based testing are the most profitable technologies because of their high sensitivity and scalability. NGS is the fastest-growing sector as comprehensive genomic profiling for cancer diagnosis requires robust library preparation kits and data management platforms to analyze complex mutational landscapes.

- By Disease Type Analysis: Cancer is projected to dominate this segment the most significant disease segments due to the immediate clinical need for targeted therapies and diagnostic answers.

- Regional Leadership: North America is poised to dominate this market with 37.1% of the market share in 2026 due to its well-developed reimbursement ecosystem that uses this infrastructure to its fullest and makes it a leader in this market.

What is the Genetic Testing?

Genetic Testing refers to the special study of chromosomes, DNA, RNA, and proteins to identify heritable and somatic mutations, which are enabled by the products such as consumables, instruments, and software manufactured, tested, and sold by third-party manufacturers, clinical laboratories, and bioinformatics service providers. These services, unlike general wellness checks (which are lifestyle-based), are related to the biological basis of health and disease. This includes predictive and presymptomatic testing to determine an inherited risk, diagnostic testing to confirm a suspected condition physically and pharmacogenomic testing to ensure that drug therapies are effective and non-toxic. Now that 90% of all drug development programs now include genomic biomarkers, professional testing services are necessary to provide accuracy in results, clinical validity and secure data interpretation of information, rather than the raw data complexity.

Use Cases

- Comprehensive Genomic Profiling in Oncology: Oncologists outsource laboratory testing services to perform genomic profiling of tumor biopsies using NGS systems and other related sequencing reagents to identify actionable mutations such as EGFR or BRCA, and use these to select the appropriate therapy to administer to late-stage cancer patients.

- Population Carrier Screening in Healthcare: Hospital networks implement DNA/RNA extraction and purification kits and PCR reagents and master mixes to screen their prospective parentage of recessive diseases such as cystic fibrosis and thalassemia so that informed decisions regarding reproductive choices can be made on a scale.

- Pharmacogenomic Navigation in Psychiatry: Mental health clinics utilize the services of pharmacogenomic testing and clinical decision support software to predict how a patient will respond to antidepressants to ensure that the appropriate drug is prescribed in the first instance, eliminating the need to go through a trial-and-error process.

- Newborn Screening Modernization: State health departments are using automated liquid handling systems and bioinformatics software to incorporate next-generation sequencing techniques into standard newborn blood spot screening, which is used to detect many rare genetic disorders with shorter turnaround times.

How AI is Transforming the Genetic Testing Market?

The genetic testing market is transformed by AI, which makes the variant interpretation process faster, and makes the work process more efficient. In software & services, AI-based bioinformatics tools have the potential to automatically classify genetic variants from raw sequencing data into pathogenic or benign categories, greatly minimizing the amount of manual curation work done by clinical scientists and reporting timelines, and diagnostic risk. In the meantime, AI-based functions within laboratory automation platforms enable labs to gain control over testing spending, predicting maintenance requirements, indicating optimal use of reagents, and suggesting workflow modifications to entrench methods of operational efficiency.

AI is also becoming a focus of diagnosis and discovery projects. Intelligent clinical decision support agents are applied in the field of testing services to continuously screen genomic databases and new gene-disease relationships, phenotype correlations, and clinical trial matches to maintain diagnostic yield abreast with the latest medical literature. Additionally, genetic counseling services are being complemented by generative AI assistants, who simulate scenarios of patient cases, and model potential patterns of inheritance, in order to provide a visualization of the risk profile before committing to communicating with patients.

Market Dynamics

Key Drivers in the Global Genetic Testing Market

The Global Clinical Genomics Skills Gap

Global healthcare organizations are grappling to acquire skilled professionals who have the knowledge of genomic data interpretation, variant science, and genetic counseling. The skills are being demanded at a rate higher than the rate of trained talents and this has created structural deficit in the labour market. This is causing a trend which is the outsourcing of genetic counseling services and bioinformatics providers by hospitals and labs instead of relying on in-house generic personnel. These firms help with such serious procedures as the choice of tests, their interpretation, and communication with patients. By outsourcing such functions, healthcare systems will be able to accelerate their precision medicine programs and reduce the risk of misdiagnosis because of a lack of appropriate in-house genomic capabilities.

Complexity of Multi-Platform Genomic Integration

Large clinical enterprises will also tend to have multiple testing platforms, mostly NGS, PCR, and microarrays, to ensure that they are able to cover a broad variety of types of variants. Nonetheless, controlling a multi-platform genomic lab is very complicated. Companies have to harmonize data formats, quality measures, reporting, and data storage solutions across a variety of instruments with different outputs. This complication can bring about inefficiencies, gaps and disjointed patient reports without the guidance of experts. Therefore, the software and services segment is increasingly in need of integrated data management platforms, which can help labs to work in such harmony.

Restraints in the Global Genetic Testing Market

Inertia of Legacy Laboratory Infrastructure

The vast majority of healthcare systems continue to operate on the old pathology workflows which were developed over a long history, and have become highly embedded in their own operations. One of the major impediments to change is these outdated processes, although genetic testing may provide more accurate diagnostics. Moving large sample archives, complicated ordering systems, highly integrated electronic health records to facilitate broad genomic profiling can be expensive and disruptive. Implementing NGS systems necessitates a lot of planning, staff training, and bioinformatics validation. The organizations are scared of interruption in the existing pathology services, loss of data and unexpected costs during the transition. As a result, the technical debt in the laboratory workflows will slow the pace of the adoption of the advanced genetic testing, and will tend to slow or even halt the larger scale investments in precision medicine.

Economic Uncertainty and Reimbursement Scrutiny

The unstable state of the economies, and the unpredictable state of the healthcare budgets environment have left payers and health systems more hesitant to reimburse new genetic tests. Although genomic medicine remains a strategic priority, laboratory directors are being put under pressure to justify all their assays on a test menu and be able to measure their clinical utility. The capital expenditure of instruments and the cost of high-value consumables to new tests are more apt to be subjected to higher scrutiny. The healthcare systems have evolved to a type of essential tests that are recommended by the guidelines and produce fast clinical actionability and lower downstream costs. New and broad tests would be more prone to be postponed until the providers can show a clear payback of health investment. This change is compelling testing companies to be more evidence-driven and health-economic-outcomes focused.

Growth Opportunities in the Global Genetic Testing Market

Proactive Population Health Screening Platforms

Among the major growth opportunities in the genetic testing market is that of helping health systems to establish secure, institutionalized population screening environments. Governments are now seeking their own custom platforms to meet their own citizen data, compliance needs, and workflows to support the health of their citizens. These advanced environments are developed with the expertise of laboratory testing service providers, genetic information storage system providers and providers of clinical decision support software. Genetic testing providers can help the public health agencies to create scalable and personalized genomic screening ecosystems that can help in the early detection of risks and preventive care. The region can generate a great demand of high specialization consumables and implementation lab services.

Direct-to-Consumer (DTC) Clinical Integration

The need to integrate both technical accuracy and consumer engagement is driving the growth of software & services as DTC genetic testing companies create solutions bridging the gap between curiosity and the clinic. These are testing solutions that are physician mediated, wellness genomic platforms and DNA relative finder tools. DTC space consumers must work through potentially severe health risk discovers. Therefore, they need genetic counseling services that have an understanding of the raw genotyping technology and clinical referral pathways. In order to add value, genetic service providers can consider integrating physician telehealth platforms with existing DTC data, in line with clinical reporting standards, and risk communication customization.

Trends in the Global Genetic Testing Market

The Rise of Direct-to-Consumer (DTC) Testing Services

Direct-to-consumer testing is becoming increasingly adopted by consumers as an alternative to traditional and siloed physician-ordered diagnostics. Businesses are building DTC genetic testing services where individuals build self-initiated health and ancestry information on their own, instead of having tests initiated, ordered and interpreted by a clinician alone. These services facilitate the convenience of collecting saliva at home, delivering the results digitally, and screening the traits. In response, genetic testing vendors are offering experience in consumer genomics, bioinformatics interpretation and regulatory compliance.

Sustainability in Genomic Consumables

Sustainability in the environment is also emerging as a key aspect in laboratory operations as institutions are under pressure to achieve ESG objectives and minimize plastic and chemical waste. The current interest of lab directors is in testing workflows which help to increase accuracy and minimise costs as well as lessen the environmental impact. This has brought about the need to have waste-reducing reagent solutions. Laboratory service providers can help organizations to choose sample collection kits with the least possible plastic, maximizing assay plates, reagent bulk-sizing, and waste reduction by switching to plate-based high-throughput formats instead of single-use formats.

Research Scope and Analysis

The Genetic Testing Market is segmented by product into consumables, instruments, and software & services, by type, by disease type, by technology, by application, and by end-users including hospitals, diagnostic laboratories, research institutes, and pharmaceutical and biotechnology companies across global markets.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Product Analysis

Consumables are dominate the product segment because they are utilized in each step of genetic testing workflows, which ensures a steady demand. In the category of consumables, sequencing reagents, PCR master mixes, and library preparation kits show the first place due to the essential role in high-throughput testing, in particular, in next-generation sequencing (NGS). Sample collection and extraction kits also play a key role with growing volumes of at-home and clinical testing. Although the tools like NGS systems and PCR machines are extremely important, they are considered to be a one-time capital investment and as such they occupy a smaller portion. Services and software are quickly catching up with consumables in terms of revenue, especially bioinformatics and cloud-based genomic platforms, but still lag in revenue generation compared to consumables because they are relatively new implementations with monetization models yet to be established.

By Type Analysis

This segment is projected to dominated by diagnostic testing as it is widely used during the process of identifying genetic conditions, cancers and inherited diseases in clinical settings. The fact that it is used in confirming diseases and in making decisions regarding treatment make it very important and demand is always high. Predictive and presymptomatic testing also finds more favor, especially where there is growing knowledge of preventive medicine, such as chronic and hereditary diseases, like cancer and neurological disorders. Prenatal and newborn testing is a major segment as it has government-sponsored screening programs, early disease detection programs, etc. Pharmacogenomic testing is increasing steadily with the increase in personalized medicine, but remain immature compared to diagnostic testing, which is the primary source of revenue because of its direct clinical application.

By Disease Type Analysis

Cancer is expected to hold the majority proportion to the disease type segment, mainly because of the massive application of genetic tests in oncology to diagnose, prognose and select targeted therapy. This dominance is largely spurred by the increasing global cancer burden and adoption of precision oncology. Rare genetic disorders also constitute a significant segment, which is supported by the development of the sequencing technology, which makes it possible to precisely identify the previously undiagnosed conditions. Cystic fibrosis, sickle cell anemia, and thalassemia are diseases with a steady demand because of the hereditary nature of the disease and the existence of screening programs. Nevertheless, oncology remains in the vanguard as genetic testing becomes part of the cancer care trajectories and treatment customization.

By Technology Analysis

Next-Generation Sequencing (NGS) is poised to dominate the technology segment because it has a high throughput, scalability, and is able to analyze multiple genes simultaneously with high accuracy. Its leadership has been cemented by its cost efficiency per base, and its expanding applications in oncology, rare diseases, and large-scale studies of the genome. Testing based on PCR is still commonly used to perform targeted and rapid diagnostics, particularly, in routine clinical practice, but it does not have the comprehensive capabilities of NGS. The array technologies and FISH are essential in certain applications like chromosomal studies but have relatively small areas of application. With the growing interest in precision medicine, NGS will keep winning over the other technologies, being the place of choice when it comes to advanced genetic analysis.

By Application Analysis

The application segment is expected to be led by cancer diagnosis due to the growing integration of genetic testing into oncology to achieve early detection, tumor profiling, and treatment selection. Its dominance is further enhanced by the emergence of targeted therapies and companion diagnostics. Another critical area is genetic disease diagnosis which is aided by the increasing awareness and the development of testing capabilities to diagnose inherited diseases. Newborn screening programs are also significant particularly in developed areas where there is mandatory policies on screening. Direct-to-consumer testing patterns have led to a rapid increase in the number of applications in the field, but primarily clinical applications, and in particular cancer, are the largest contributors to the number of applications.

By End-User Analysis

The end-user segment is projected to be dominated by diagnostic laboratories, due to their large volumes of genetic tests, with specialized infrastructure, advanced equipment, and skilled personnel. They are at the center of the genetic testing ecosystem because they are efficient in processing high-throughput testing. Hospitals and clinics also constitute a large portion, especially in sample collection and initial examination, but tend to outsource complex examinations to external labs. The research and academic institutes will help in innovation and testing at the earlier stages but will also generate relatively less revenue. The rising outsourcing of genetic testing services and the rising need to accurately and large-scale analyze genomic data across healthcare systems, reinforce the dominance of diagnostic laboratories.

The Global Genetic Testing Market Report is segmented on the basis of the following:

By Product

- Consumables

- Sample Collection Kits (Saliva, Blood, Buccal Swabs)

- DNA/RNA Extraction & Purification Kits

- Library Preparation Kits

- PCR Reagents & Master Mixes

- Sequencing Reagents

- Microarray Chips & Reagents

- Assay Kits

- Quality Control & Validation Reagents

- Instruments

- Next-Generation Sequencing (NGS) Systems

- PCR Instruments

- Microarray Scanners & Hybridization Systems

- DNA Extraction & Purification Systems

- Electrophoresis Systems

- Automated Liquid Handling Systems

- Cytogenetic Analysis Instruments

- Laboratory Automation Platforms

- Software & Services

- Bioinformatics Software

- Genetic Data Management Platforms

- Clinical Decision Support Software

- Cloud-based Genomic Analysis Solutions

- Direct-to-Consumer (DTC) Genetic Testing Services

- Laboratory Testing Services

- Genetic Counseling Services

- Data Storage & Security Solutions

By Type

- Predictive & Presymptomatic Testing

- Carrier Testing

- Prenatal & Newborn Testing

- Diagnostic Testing

- Pharmacogenomic Testing

- Nutrigenomic Testing

- Other Type

By Disease Type

- Cancer

- Alzheimer’s Disease

- Cystic Fibrosis

- Sickle Cell Anemia

- Thalassemia

- Huntington’s Disease

- Rare Genetic Disorders

- Others

By Technology

- Next-Generation Sequencing (NGS)

- PCR-based Testing

- Array Technology

- Fluorescence In Situ Hybridization (FISH)

- Cytogenetic Testing

- Biochemical Testing

By Application

- Cancer Diagnosis

- Genetic Disease Diagnosis

- Cardiovascular Disease Diagnosis

- Ancestry & Ethnicity Testing

- Traits Screening

- Newborn Screening

- Health & Wellness / Risk Assessment

- Forensic & Relationship Testing

By End-User

- Hospitals & Clinics

- Diagnostic Laboratories

- Research & Academic Institutes

- Others

Regional Analysis

Leading Region by Market Share

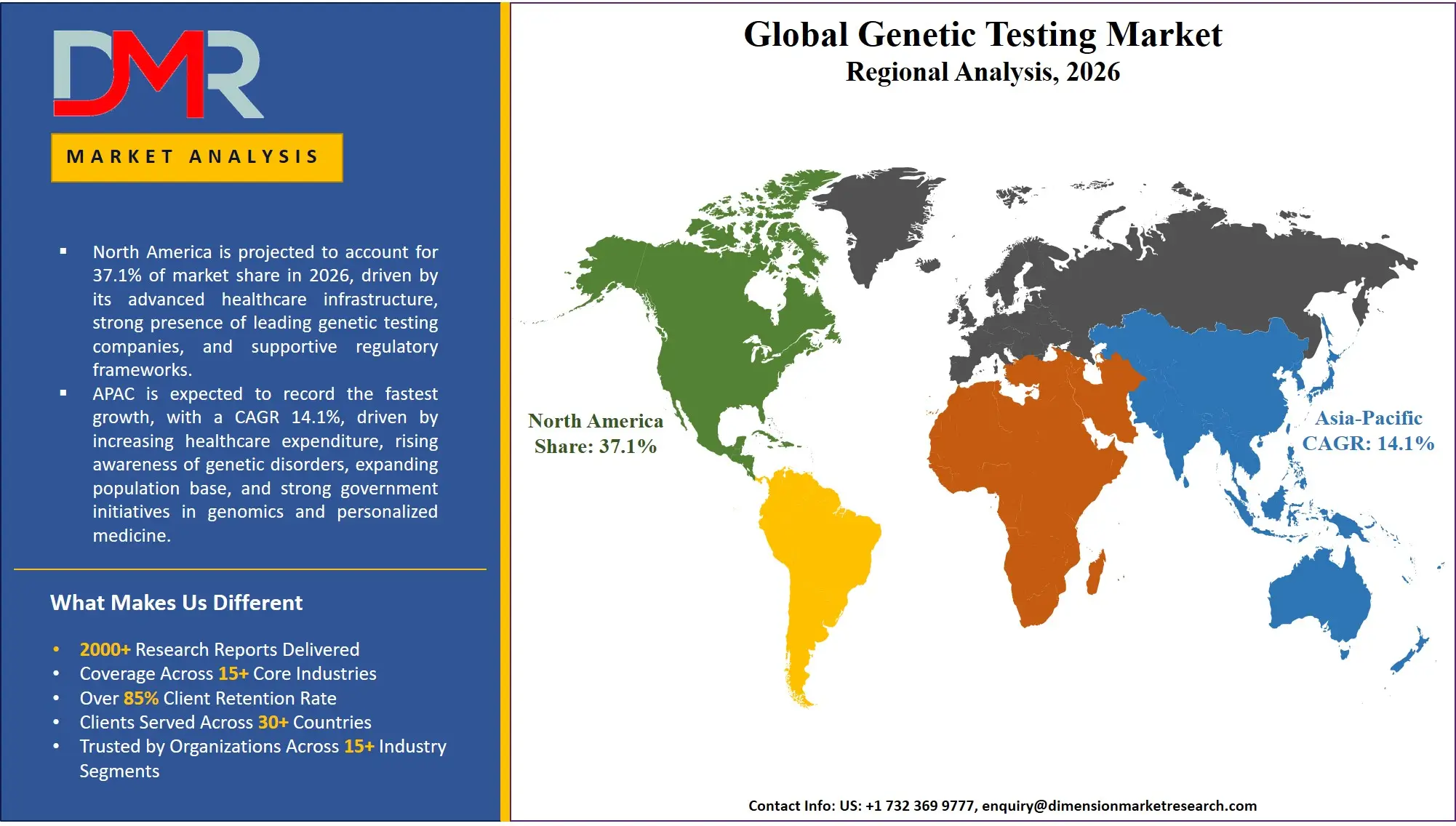

North America is poised to dominate the global genetic testing market as it is projected to hold 37.1% of the market share by the end of 2026. The largest share of genetic testing market belongs to the United States, which controls the largest part of North America, due to the unparalleled concentration of commercial diagnostic laboratories and aggressive precision medicine agendas of major academic medical Centres. The region boasts a proven ecosystem of international testing corporations, specialty bioinformatics companies and an immensely talented pool of genetic counseling and molecular pathology. The ongoing need of NGS systems and consumables as well as scalable genetic data management platforms is supported by enterprise investment in comprehensive cancer genomics, advanced AI-driven interpretation and the overall inclusion of healthy population screening programs. In addition, a highly advanced but complex reimbursement climate continues to fund future innovative genetic testing that requires highly skilled laboratory testing service to gain regulatory approval and payer coverage.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Regional Market

Asia-Pacific is projected to become the fastest growing genetic testing market, fueled by sweeping precision medicine programs led by the government in India, China, Japan and Southeast Asia. The rapid economic development, the emergence of a new middle-income group, and the active development of the sphere of private healthcare delivery is forcing the established hospital conglomerates and state agencies to implement new advanced genomic technologies to manage inherited diseases. There is a great need to be able to head these large health systems toward the direction of proactive neonatal screening and pathogen genomics. There is also a severe shortage of qualified bioinformaticians and variant scientists in the region, and a need to outsource specialized software and services to implement, interpret and securely store genomic data to overcome the skills gap and enable faster clinical genomic investment.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The global genetic testing market is a highly dynamic competitive environment with a heterogeneous mix of multinational genetic testing service providers, specialized genetic testing instrument manufacturers and niche bioinformatics software firms. Profound strategic alliances with large reference laboratories and health systems since they will give the requisite test access points and early incorporation into clinical guidelines. The trend of market consolidation is gaining momentum with conventional diagnostic testing firms acquiring AI and bioinformatics-centric startups to keep afloat. Proprietary intellectual property, such as novel reagent formulations, automated variant curation frameworks, and proprietary genetic risk scores, are increasingly becoming an increasingly important basis of competitive differentiation than simply raw sequencing output or generic assay design strategies.

Some of the prominent players in the Global Genetic Testing Market are:

- Illumina, Inc.

- F. Hoffmann-La Roche Ltd

- Thermo Fisher Scientific Inc.

- QIAGEN N.V.

- Myriad Genetics, Inc.

- Natera, Inc.

- BGI Genomics

- Invitae Corporation

- Guardant Health, Inc.

- Eurofins Scientific

- Agilent Technologies, Inc.

- Abbott Laboratories

- Laboratory Corporation of America Holdings (LabCorp)

- Quest Diagnostics Incorporated

- PerkinElmer, Inc.

- Oxford Nanopore Technologies

- Pacific Biosciences of California, Inc.

- 23andMe, Inc.

- AncestryDNA

- Color Genomics, Inc.

- Other Key Players

Recent Developments

- January 2026: Illumina announced a significant expansion of its bioinformatics partnership ecosystem, a software and services initiative to help diagnostic laboratories in Healthcare and Life Sciences create proprietary curation models of AI variants through its Cloud-based Genomic Analysis Solutions and expertise in data storage and security.

- November 2025: Thermo Fisher Scientific intensified its partnership with clinical networks and introduced a particular practice known as Pharmacogenomic & Diagnostic Testing and Laboratory Automation, aimed to help hospital labs migrate to comprehensive NGS panel testing and keeping in compliance to IVDR and FDA regulations on quality control.

- October 2025: 23andMe will have acquired a telehealth provider to further its DTC Genetic Testing Services as well as Genetic Counseling Services bridge to clinical care, to support the complicated needs of consumers and healthcare system partners to navigate clinically actionable genetic information.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 27.9 Bn |

| Forecast Value (2035) |

USD 74.3 Bn |

| CAGR (2026–2035) |

11.5% |

| The US Market Size (2026) |

USD 8.7 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Product, By Type, By Disease Type, By Technology, By Application, and By End-User |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Genetic Testing Market?

▾ The Global Genetic Testing market is poised to be valued at USD 27.9 billion in 2026 and is projected to reach USD 74.3 billion by 2035, driven by the universal need for specialized tools in genomic analysis, clinical diagnostics, and AI-driven interpretation.

What is the CAGR of the Global Genetic Testing Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 11.5% from 2026 to 2035, reflecting the accelerating complexity of genomic data and the persistent integration of sequencing into standard-of-care clinical pathways.

Which region held the largest share of the Genetic Testing Market in 2026?

▾ North America is poised to lead this market with 37.1% of the market share in 2026, driven by a mature clinical laboratory ecosystem and aggressive investment in diagnostic testing and AI-driven genomic interpretation capabilities.

Who are the key players in the Global Genetic Testing Market?

▾ Key players include instrument and reagent manufacturers like Illumina, Thermo Fisher Scientific, and Roche, as well as clinical genetic testing providers like Quest Diagnostics, Labcorp, and Natera, alongside specialized pure-play DTC genotyping and bioinformatics companies.

What factors are driving the growth of the Global Genetic Testing Market?

▾ Key drivers include the clinical genomics skills gap, the imperative to move from reactive to proactive population screening, the management complexity of multi-platform lab operations, and the surge in demand for DTC genetic testing services amid evolving consumer health awareness.

Which region is expected to grow the fastest in the Genetic Testing Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid precision medicine adoption in India, China, and Japan, where diagnostic testing is critical for transitioning large hospital systems to comprehensive genomic profiling.

What are the major trends in the Global Genetic Testing Market?

▾ Major trends include the integration of Generative AI into bioinformatics software, the rise of DTC genetic testing services, the demand for liquid biopsy-based assays, and the focus on cloud-based genomic analysis solutions within complex NGS data environments.

How is the Global Genetic Testing Market segmented?

▾ The market is segmented by Product, Type, Disease Type, Technology, Application, and End-User.