Hyperautomation is an advance form of automation distinctive from traditional automation by integrating technologies like AI and ML to allow systems to learn from data, adapt to new situations, & make informed decisions.

Further, greater automation penetration, enhanced precision, increased return on investment (ROI), & accuracy across different industries present potential opportunities for growth. Hyper Automation's ability to provide enhanced analytics data allows enterprises to achieve timely & accurate ROI.

However, challenges, like a lack of trained labor & improper deployment due to a low understanding of automation's application in different industries. In addition, the deployment of advanced tools like AI,

natural language processing, and

machine learning requires skilled labor and proper training. The absence of these elements could restrain industry progress.

Moreover, the shortage of reliable data for AI & decision-making poses a major challenge to the growth of the Global Hyper Automation Market. Similarly, the lack of training among personnel remains a key obstacle to the widespread adoption of Hyper Automation

Research Scope and Analysis

By Component

Regarding components, the industry has been segmented into hardware, software, & services, each playing a different role in the hyper-automation ecosystem. Within the hardware category, hyper-automation services include activities like controlled power delivery installation & the maintenance of machinery and equipment.

Primarily, the hardware segment secures the largest share of revenue in 2023. This dominance can be said owing to the benefits offered by automation hardware in industries, like increased efficiency, improved quality, & lower errors in manufacturing processes. These advantages stem from the inherent mobility, scalability, & adaptability of automation solutions.

Moreover, the software segment is anticipated to see a fast growth rate throughout the forecast period, as automation software plays a critical role in improving efficiency by creating solutions customized to streamline repetitive administrative tasks & data processing. These software solutions are created to reduce the need for human intervention & can be effectively implemented across different business domains.

The dynamics between these components demonstrate how hardware-driven efficiency & quality gains complement the software's role in automating routine tasks, ultimately contributing to the broader landscape of hyper-automation.

By Technology

In terms of technologies, the global hyper-automation industry can be segmented into several categories, each contributing to the overall advancement of automation & efficiency. These technologies include Robotic Process Automation (RPA), Machine Learning (ML), Natural Language Generation (NLG), context-aware computing, biometrics, chatbots, & computer vision. Each of these technologies plays a unique role in improving various aspects of automation & business processes.

Among these categories, the RPA technology segment majorly dominates in 2023, capturing a significant share of the total industry revenue. Robotic Process Automation includes the use of software bots to automate routine & rule-based tasks, enabling businesses to streamline operations & limit human intervention.

With the proliferation of complex business tools like data analytics & big data, companies are struggling with the challenge of managing large volumes of data generated daily, which led to a growing need for efficient data handling & processing. Multinational companies, in particular, are opting for corporate data centers that offer advanced data security measures, driving the development of the RPA segment as they seek to optimize data management processes. All these tends & factors are anticipated to the future growth of the market as well

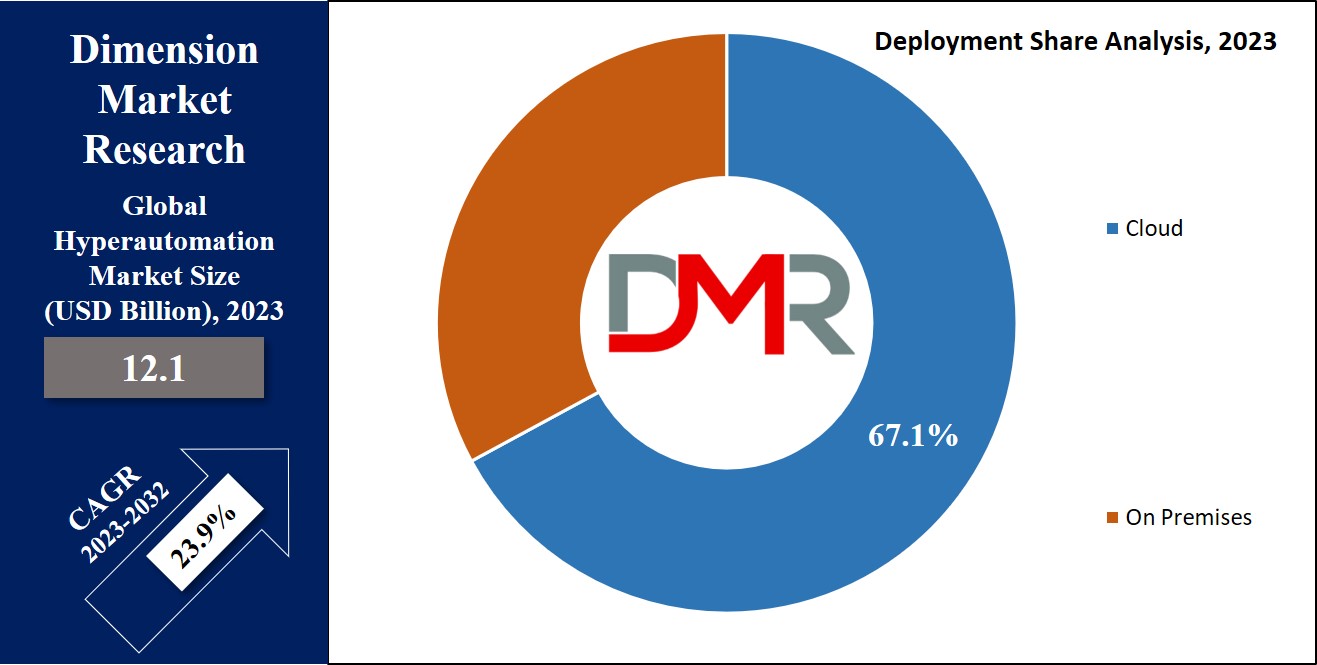

By Deployment

The global hyper-automation industry is divided into on-premise and cloud categories in terms of deployment mode. The cloud deployment segment emerged as the major factor in 2023, claiming the majority share of the total revenue.

This segment is anticipated to maintain its leading position throughout the forecast period while expanding steadily. Cloud deployment offers businesses better efficiency & flexibility by allowing the delivery of features & functions in a streamlined manner. Organizations can tap into a large network of data centers & cloud platforms to facilitate analysis & mapping using cloud-based solutions.

Simultaneously, the on-premise deployment segment is anticipated to experience significant growth over the forecast period. This growth is driven by the increased demand from SMEs On-premise deployment holds the potential for large revenue contribution in the future.

It also grants customers full access to their data, applications, & infrastructure while simultaneously reducing operational costs & bettering security measures. As SMEs increasingly seek customized & localized solutions, the on-premise segment is expected to witness significant expansion.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Function

In terms of functions, the global hyper-automation industry is segmented into Human Resources (HR), Information Technology (IT), marketing & sales, finance & accounting, and operations & supply chain. Among these segments, the finance & accounting function segment emerged as the dominant force in 2023, capturing the largest share of revenue and is expected to maintain its dominance throughout the forecast period.

The growth of the finance & accounting segment can be said owing to the growing demand for error reduction, improved collaboration, & enhanced overall productivity. Businesses are attaining these objectives by integrating hyper-automation technology into numerous financial processes like financial analysis, payroll administration, invoicing, collections, & financial statement preparation.

Standardizing & automating these processes through hyper-automation contributes to enhanced efficiency & accuracy, driving growth within the finance & accounting function segment.

In addition, the marketing & sales function is anticipated to exhibit quick growth, during the forecast period. This growth is driven by the growing dependence of marketing firms on automation to improve campaign accuracy, deliver better leads to sales teams, & yield higher returns on investment (ROI). These factors collectively contribute to the growth of the market within the marketing & sales segment.

By Enterprise

Categorizing based on enterprises, the global hyper-automation industry is divided into two segments, that are large-size enterprises and Small- and Medium-sized Enterprises or SMEs. The large-size enterprise segment emerges as the major driving factor in the global hyper-automation market in 2023.

This segment is expected to maintain its leading position & continue expanding at a significant growth rate throughout the forecast period. As the business landscape becomes highly complex with the integration of data analytics & big data, companies are noticing the challenge of managing large volumes of daily data.

In response, multinational firms are choosing corporate data centers that provide advanced data security measures, supporting the growth of the large enterprise segment. This choice of data centers with higher security provisions contributes to the segment's expansion.

Moreover, the SMEs segment is also anticipated to register noteworthy growth during the forecast period. This growth is driven by the increasing demand for quickly deployable & scalable data centers. The need for agility & adaptability in data management is driving the adoption of hyper-automation solutions among SMEs.

Additionally, the increasing adoption of cloud services by SMEs is a significant driver for market growth within this segment. As SMEs acknowledge the benefits of cloud-based solutions, the hyper-automation market is poised to flourish within this sector.

By End User

Segmented by the end user, the global hyper-automation market is divided into various sectors, like manufacturing, automotive,

healthcare analytics, aerospace & defense, retail, BFSI (Banking, Financial Services, & Insurance), IT & telecommunication, transportation & logistics, and others. Among these, the IT & telecommunication sector emerges as the dominant force in the global hyper-automation industry in 2023, capturing the maximum share of the overall global market.

This segment is anticipated to maintain its position & expand steadily throughout the forecast period. The integration of Robotic Process Automation (RPA) is proving favorable for telecom companies as it eases operational tasks & creates a way to generate consistent revenue streams through the provision of fast, high-quality, & cost-effective services.

This trend contributes to the segment's constant growth, as telecom companies leverage RPA for improved efficiency & customer service, cementing their market position.

Moreover, the retail end-use segment is also anticipated to experience significant growth during the forecast period. Automation is proving transformative for the retail sector, making it easier for efficient inventory management, reducing the workload of store managers, & improving delivery timelines. These advantages are driving the adoption of hyper-automation solutions in the retail domain, enhancing its operational efficiency & customer experience.

The Hyperautomation Market Report is segmented on the basis of the following:

By Component

- Hardware

- Software

- Services

By Technology

- Robotic Process Automation

- Machine Learning

- Biometrics

- Chatbots

- Context-Aware Computing

- Natural Language Generation

- Computer Vision

By Deployment

By Function

- Marketing & Sales

- Finance & Accounting

- Human Resources

- Operations & Supply Chain

- Information Technology

By Enterprise

- Large-size Enterprises

- Small & Medium-size Enterprises

By End User

- Manufacturing

- Automotive

- BFSI

- Healthcare

- IT & Telecommunication

- Retail

- Transportation & Logistics

- Others

Regional Analysis

In 2023, the North American region dominates the market by capturing a

significant 35.2% share of the global hyper-automation market's total revenue. This commanding position is owing to the rapid advancement of digitization, which has steeped various sectors, & the increase in demand for growing operational efficiency & low business costs. Notably, the region's industries are actively embracing hyper-automation to support their supply chains' resilience, thereby driving the region's market growth.

Further, the Asia Pacific region is anticipated to see a fast growth rate during the projected period.

Major economies like Japan, China, & India are making significant investments in supporting their IT infrastructure & establishing new data centers to establish the ever-expanding volumes of data generated in their respective domains.

Additionally, a significant number of SMEs in the region are eagerly adopting cloud computing solutions. This extensive adoption of cloud technology contributes to a highly encouraging growth prospect for the Asia Pacific market segment.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive landscape of the market is experiencing fragmentation, mainly due to the presence of various global & regional players. In order to flourish within this fiercely competitive environment & extend their market reach, leaders in the industry are using a range of strategic approaches including forming partnerships, establishing collaborations, & launching new products that help them grow along with growing their market positioning & share.

For instance, in September 2022, UiPath, a leader in enterprise automation software, & OutSystems, a global player in fast application development, announced a partnership, through which the companies combine UiPath's powerful Business Automation Platform with OutSystems' efficient low-code capabilities.

As together, they offer clients the opportunity to intelligently & securely automate important business processes and applications. Further, the collaboration results in time savings, improved productivity, & the creation of transformative app experiences for businesses.

Some of the prominent players in the Global Hyperautomation Market are

- UiPath

- Wipro Ltd.

- Tata Consultancy Services Ltd.

- Mitsubishi Electric Corporation

- OneGlobe LLC

- SolveXia

- Appian

- Automation Anywhere

- Other Key Players

Recent Developments

- February 2025: Swimlane announces 107% year-over-year adoption growth of its Turbine AI hyperautomation platform, showcasing its growing traction as a leading security automation solution.

- May 2024: Trellix introduces “Trellix Wise”, a GenAI-powered hyper-automation suite within its XDR platform that delivers up to five times the efficiency for threat detection and response.

- July 2025: Capgemini announces acquisition of WNS for approximately $3.3 billion, integrating WNS’s AI, analytics, and hyperautomation capabilities into Capgemini’s intelligent operations ecosystem.

- November 2022: Roboyo acquired Procensol, adding low-code application development expertise and expanding its hyperautomation services across global markets.

- June 2025: Swimlane secures $45 million in growth funding, led by Energy Impact Partners and Activate Capital, to support global expansion and product innovation in AI hyperautomation for security operations.

Report Details