Market Overview

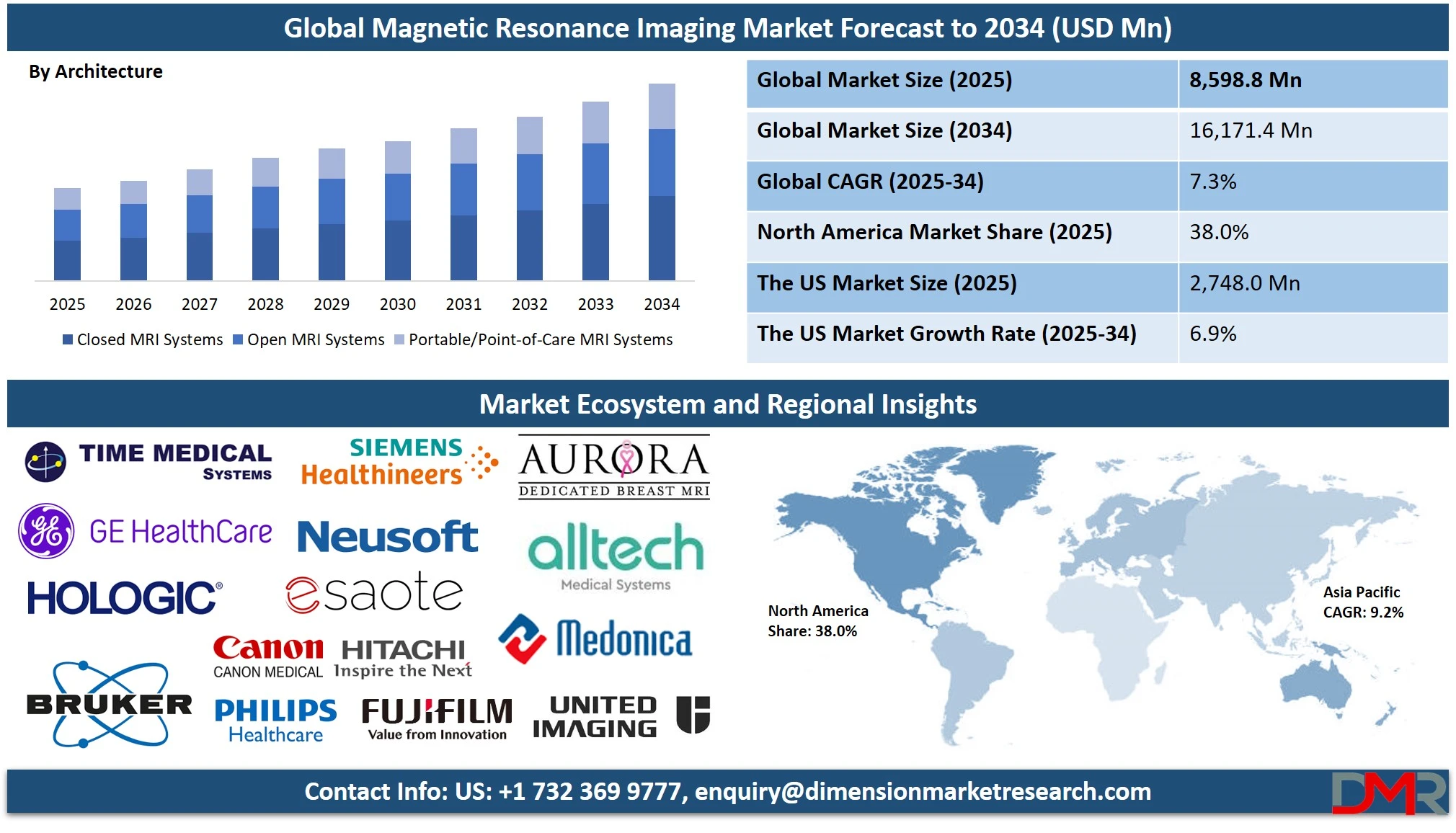

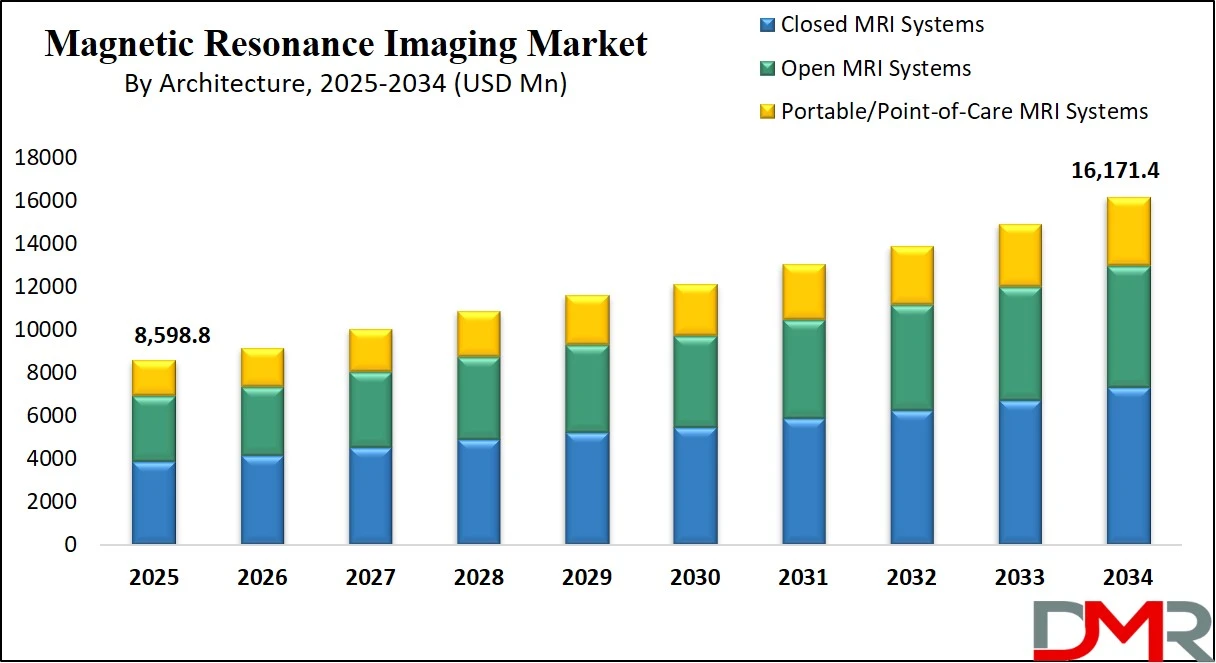

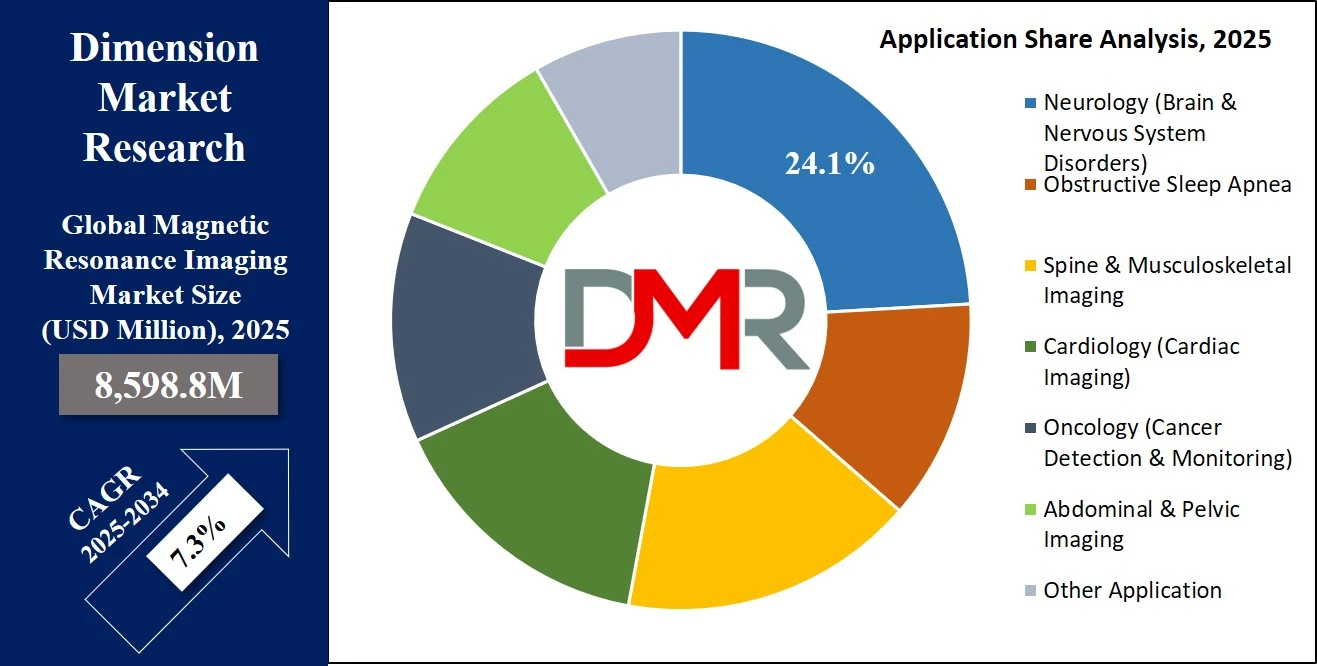

The Global Magnetic Resonance Imaging Market is projected to reach USD 8,598.8 million in 2025 and grow at a compound annual growth rate of 7.3% from there until 2034 to reach a value of USD 16,171.4 million.

The global magnetic resonance imaging (MRI) market is poised for sustained expansion, driven by the increasing prevalence of chronic disorders such as neurological conditions, musculoskeletal disorders, cardiovascular diseases, and cancer. MRI systems are increasingly favored for their non-invasive, radiation-free imaging capabilities, offering high-resolution anatomical and functional details. Advancements in coil design, machine learning-enabled image reconstruction, and 7T and ultra-high-field MRI systems have significantly enhanced diagnostic precision across clinical applications.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

A key trend shaping the MRI industry is the development of portable and point-of-care MRI systems. These compact devices, now more accessible due to AI-based image processing and cost-efficient hardware, are revolutionizing brain and trauma imaging in emergency and critical care settings. Another trend is the growing adoption of hybrid imaging modalities like PET/MRI and MRI-guided interventions, enabling real-time visualization during surgeries and therapy.

An important growth opportunity lies in emerging economies with underdeveloped diagnostic infrastructure. Government-funded healthcare expansion and initiatives to improve early diagnosis rates are creating demand for affordable and efficient imaging systems. Moreover, research collaborations between academic institutes and imaging manufacturers are accelerating the development of AI-enhanced radiology workflows and patient-specific AI imaging.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

However, challenges persist. MRI scanners remain capital-intensive investments, often exceeding the budgetary limits of smaller hospitals and diagnostic centers. Additionally, compatibility limitations for patients with metallic implants and long scan durations hinder widespread use, especially in pediatric and geriatric populations.

Despite these restraints, the global MRI market is forecasted to grow steadily, supported by rising geriatric demographics, expanding clinical applications, and ongoing technological innovation. With the integration of deep learning algorithms for faster acquisition and interpretation, MRI is evolving from a diagnostic tool to a predictive and precision-medicine enabler, unlocking new dimensions in preventive healthcare and personalized treatment planning.

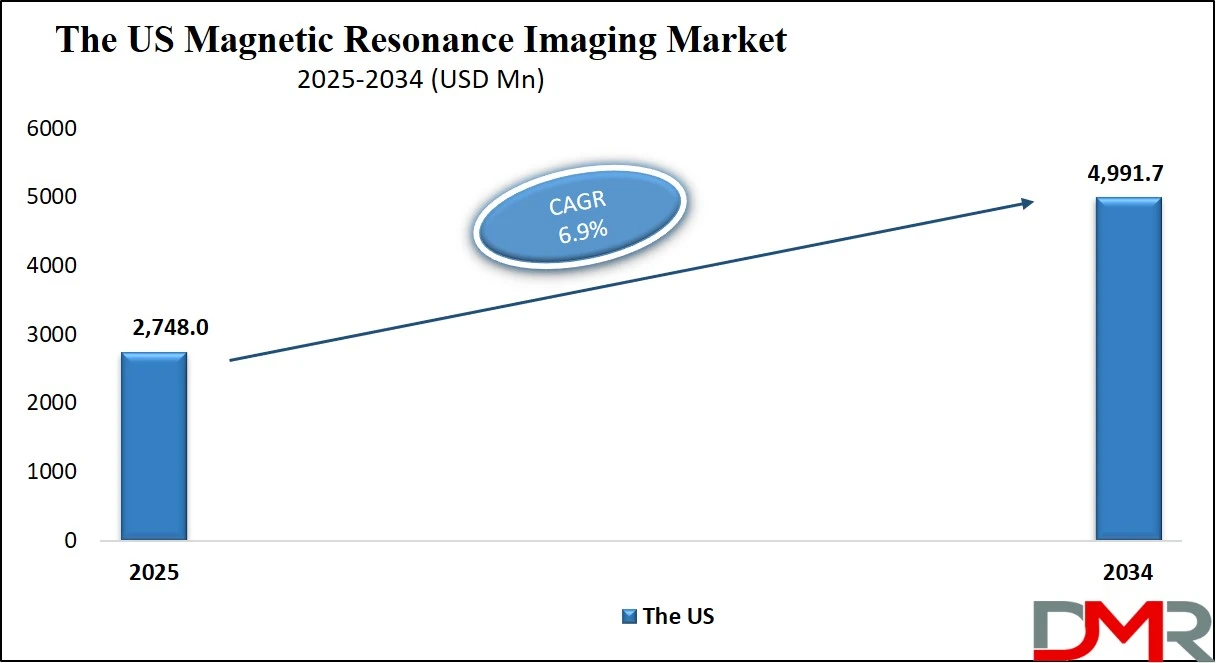

The US Magnetic Resonance Imaging Market

The US Magnetic Resonance Imaging Market is projected to reach USD 2,748.0 million in 2025 at a compound annual growth rate of 6.9% over its forecast period.

The U.S. magnetic resonance imaging (MRI) market benefits from robust healthcare infrastructure, strong academic research, and rising chronic disease prevalence. According to the U.S. Centers for Disease Control and Prevention (CDC), nearly 60% of American adults suffer from at least one chronic condition, reinforcing the need for advanced imaging in diagnostics and disease management. MRI has become integral in neurology, orthopedics, cardiology, and oncology due to its detailed soft-tissue visualization and absence of ionizing radiation.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Demographically, the aging population is a critical driver. The U.S. Census Bureau projects that by 2034, older adults will outnumber children for the first time in U.S. history. This shift contributes to the growing volume of MRI procedures for degenerative disorders, spinal conditions, and brain imaging. In addition, increasing obesity and diabetes rates continue to push demand for cardiovascular and abdominal imaging.

The U.S. Food and Drug Administration (FDA) plays a pivotal role in regulating MRI devices and facilitating innovation through programs like the Breakthrough Devices Program. Furthermore, the National Institutes of Health (NIH) supports extensive imaging research, including funding AI-integrated MRI platforms and radiomics studies, boosting both clinical and technological advancement.

The Veterans Health Administration and the Centers for Medicare & Medicaid Services (CMS) provide reimbursement frameworks that help expand MRI accessibility across the public healthcare system. Meanwhile, private insurers are increasingly covering MRI procedures, particularly for preventive screening and early-stage diagnostics.

Collectively, favorable reimbursement policies, rising disease burden, academic innovation, and demographic transitions contribute to the steady advancement of the U.S. MRI market in both clinical and research domains.

The Europe Magnetic Resonance Imaging Market

The Europe Magnetic Resonance Imaging Market is estimated to be valued at USD 1,289.8 million in 2025 and is further anticipated to reach USD 2,371.6 million by 2034 at a CAGR of 7.0%.

Europe’s magnetic resonance imaging (MRI) market benefits from comprehensive public healthcare systems, early adoption of medical technology, and an aging demographic. According to Eurostat, over 21% of the EU population is aged 65 or older, amplifying demand for diagnostic imaging services related to neurodegenerative, orthopedic, and cardiovascular conditions. MRI is widely adopted in Germany, France, the UK, and the Nordics, where hospitals are equipped with high-field and mid-field MRI systems for clinical and academic use.

Public health systems in countries such as Germany (GKV), France (Assurance Maladie), and the UK (NHS) support full or partial reimbursement for MRI procedures, making the modality accessible across economic classes. The European Medicines Agency (EMA) and the European Commission further support the safe deployment of MRI technologies, especially in conjunction with pharmaceutical imaging agents and emerging AI-based radiology tools.

The European Commission has funded numerous research initiatives under the Horizon Europe framework to advance imaging science, including projects focusing on AI-driven segmentation, MRI-guided robotic surgery, and portable MRI systems for rural outreach. In addition, the WHO Europe regional office promotes imaging infrastructure equity through digital health transformation across underserved areas in Eastern and Southern Europe.

Regulatory harmonization through the European Medical Device Regulation (MDR) also ensures safety and innovation. Moreover, multilingual academic collaborations across universities and hospitals foster MRI innovation in specialized applications like fetal MRI, epilepsy detection, and tumor characterization.

The Japan Magnetic Resonance Imaging Market

The Japan Magnetic Resonance Imaging Market is projected to be valued at USD 515.9 million in 2025. It is further expected to witness subsequent growth in the upcoming period, holding USD 963.4 million in 2034 at a CAGR of 7.1%.

Japan’s magnetic resonance imaging (MRI) market stands out due to its high scanner density, technologically advanced healthcare ecosystem, and a demographic profile heavily skewed toward the elderly. According to the Statistics Bureau of Japan, over 29% of the population is aged 65 or older, the highest proportion among developed nations. This aging demographic is a significant driver of MRI utilization for neurodegenerative diseases, musculoskeletal disorders, and cardiac conditions.

Japan holds one of the world’s highest numbers of MRI machines per capita, as reported by the Ministry of Health, Labour and Welfare (MHLW), which has led to faster diagnosis and efficient clinical workflows. Hospitals and diagnostic centers widely deploy 1.5T and 3T systems, while academic institutions are pioneers in developing next-generation imaging techniques, such as diffusion tensor imaging and functional MRI (fMRI) for brain mapping.

Government policies under the Japan Revitalization Strategy and the Health and Medical Strategy Promotion Act prioritize digital health and AI integration in imaging, further strengthening the MRI landscape. The Pharmaceuticals and Medical Devices Agency (PMDA) ensures rapid but safe device approvals, while the Japan Agency for Medical Research and Development (AMED) actively funds collaborative imaging research involving AI, radiomics, and quantum computing.

Reimbursement policies under Japan’s universal healthcare system incentivize routine and advanced MRI scans. The efficiency of the NHI (National Health Insurance) scheme allows high MRI penetration in both urban and rural settings, improving access and equity.

Global Magnetic Resonance Imaging Market: Key Takeaways

- Global Market Size Insights: The Global Magnetic Resonance Imaging Market size is estimated to have a value of USD 8,598.8 million in 2025 and is expected to reach USD 16,171.4 million by the end of 2034.

- The Global Market Growth Rate: The market is growing at a CAGR of 7.3 percent over the forecasted period of 2025.

- The US Market Size Insights: The US Magnetic Resonance Imaging Market is projected to be valued at USD 2,748.0 million in 2025. It is expected to witness subsequent growth in the upcoming period as it holds USD 4,991.7 million in 2034 at a CAGR of 6.9%.

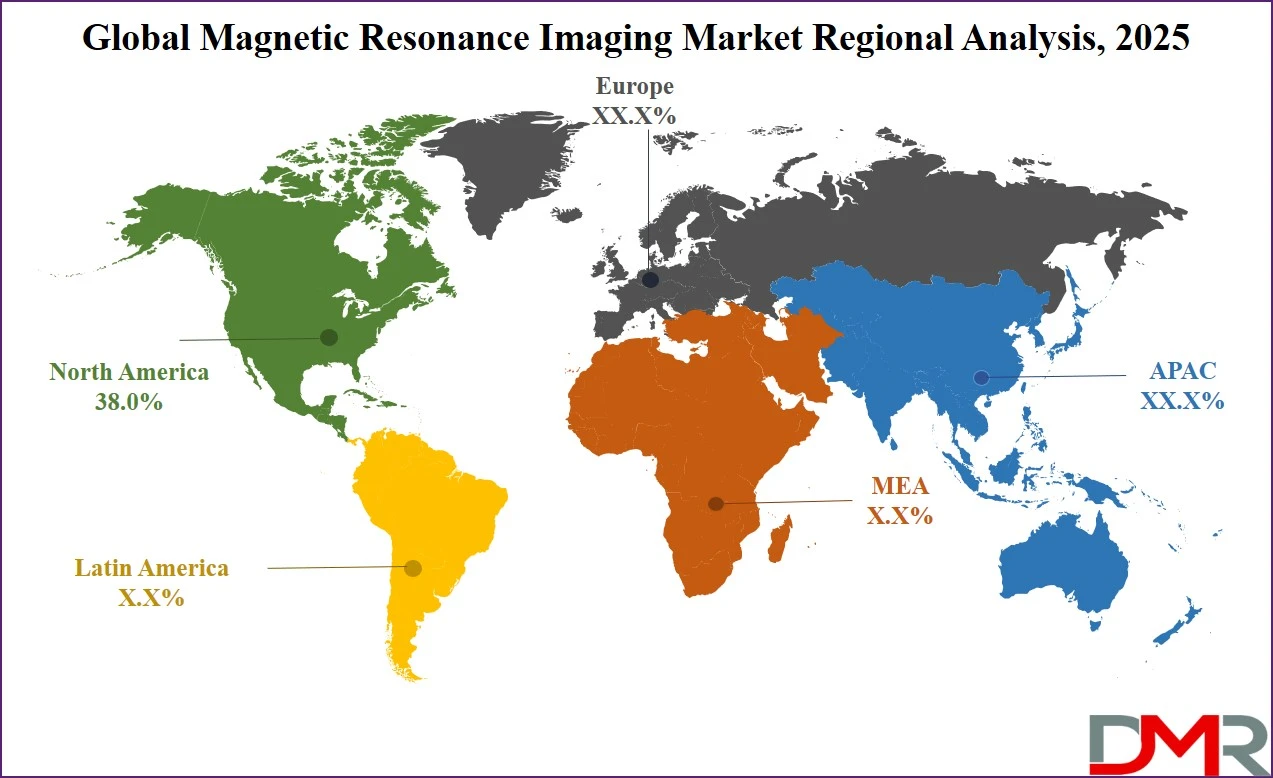

- Regional Insights: North America is expected to have the largest market share in the Global Magnetic Resonance Imaging Market with a share of about 38.0% in 2025.

- Key Players: Some of the major key players in the Global Magnetic Resonance Imaging Market are Siemens Healthineers, GE HealthCare, Philips Healthcare, Canon Medical Systems, Fujifilm (including Hitachi), United Imaging, and many others.

Global Magnetic Resonance Imaging Market: Use Cases

- Neurological Disease Diagnosis: MRI is pivotal in diagnosing conditions like multiple sclerosis, Alzheimer’s disease, and brain tumors. High-resolution 3D imaging and functional MRI (fMRI) help visualize brain lesions, structural abnormalities, and neural activity.

- Oncology Imaging and Monitoring: MRI plays a critical role in tumor detection, staging, and treatment planning across cancers such as prostate, breast, and brain. Unlike CT, MRI provides detailed contrast in soft tissues without ionizing radiation.

- Cardiovascular Imaging: Cardiac MRI (CMR) is essential for evaluating myocardial viability, congenital heart disease, and perfusion abnormalities. It offers precise imaging of cardiac anatomy, function, and tissue composition.

- Musculoskeletal Disorders: Orthopedic specialists use MRI to diagnose joint injuries, ligament tears, spinal disc herniation, and bone marrow edema. High-field MRI systems produce detailed images of soft tissue and cartilage, helping avoid unnecessary surgeries and improving rehabilitation outcomes.

- Pediatric and Fetal Imaging: MRI is increasingly used for pediatric brain imaging and fetal diagnostics due to its safety profile and detailed resolution. Fetal MRI helps detect congenital abnormalities when ultrasound results are inconclusive.

Global Magnetic Resonance Imaging Market: Stats & Facts

OECD / International Bodies

- 66% of the world’s population lacks access to MRI scanners.

- Low- and middle-income countries (LMICs) average 1.12 MRI units per million population, compared with 26.53 units per million in high-income countries (HICs).

- Japan has the highest MRI density globally, with 55.21 MRI units per million population.

- In 2011, MRI density was 46.9 per million in Japan, 31.5 in the U.S., and an OECD average of 13.3 per million.

Eurostat / European Public Health Data

- Europe has approximately 7,736 MRI scanners.

- The average across Europe is 16 MRI scanners per million inhabitants.

- Greece, Italy, and Finland have the highest densities with 34, 31, and 30 per million, respectively.

- Portugal has the lowest MRI density in Europe at 10 units per million people.

Canada (Canadian Medical Imaging Inventory – CIHI, Health Canada)

- MRI units in Canada increased by 14.3%, from 378 to 432 units between 2019–2023.

- MRI scanner density grew from 10.0 to 10.8 units per million people over the same period.

- Ontario and Quebec saw MRI growth of 18.8% and 15.8%, respectively.

- Average of 7 full-time MRI technologists (MRTs) per MRI site across Canada.

- National average: 22 MRTs per million population; highest in Manitoba (54.7), Yukon (45), and British Columbia (38.8).

- Total number of MRI-operating MRTs increased by 18.4%, from 748 to 886.

- MRT density rose by 12.7% during this period; Yukon saw an 84.4% increase.

- MRI scanner usage ranged from 37.5 to 113.2 hours weekly.

- 14.5% of MRI units operated under 20 hours/week, 34.1% operated 80–120 hours, and 18.5% exceeded 120 hours/week.

- Annual planned downtime averaged 33.9 hours, while unplanned downtime averaged 78.6 hours.

- 92.9% of MRI scans were non-cardiac, 2.7% cardiac, and 1.3% research-based.

- Scans by purpose: 98.7% diagnostic, 0.6% interventional, 0.6% research.

- Exam distribution: 28.8% neurological, 28.7% musculoskeletal, 18.4% oncology, and 12.3% hepatobiliary.

- Only 18% of sites reported using clinical decision support tools.

- 62.5% of MRI sites participated in peer-review image interpretation; Alberta led with 95% participation.

International Safety / Technical Observations

- An estimated 50,000 MRI scanners are in use globally.

- MRI machines can emit noise levels up to 120 dB(A), requiring protective measures for patients.

- In Pennsylvania (2004-2008), 27 reported projectile incidents involved ferromagnetic objects in MRI suites.

- Average MRI exam duration ranges between 20 to 40 minutes, depending on exam type and field strength.

Global Magnetic Resonance Imaging Market: Market Dynamics

Driving Factors in the Global Magnetic Resonance Imaging Market

Rising Prevalence of Chronic Diseases

A primary growth driver for the Magnetic Resonance market is the escalating global burden of chronic diseases, particularly neurological, cardiovascular, and oncological disorders. MRI is a non-invasive, radiation-free imaging modality that is ideal for diagnosing and monitoring these conditions. According to the World Health Organization (WHO), chronic diseases account for over 70% of global deaths, with increasing incidence driven by aging populations, sedentary lifestyles, and dietary shifts.

MRI plays a critical role in early detection, disease staging, and treatment planning, making it indispensable for managing chronic illnesses. For example, multiple sclerosis, stroke, Alzheimer’s disease, and brain tumors rely heavily on MRI for accurate diagnosis and follow-up imaging. In cardiology, cardiac MRI is now a gold-standard tool for assessing myocardial infarction, cardiomyopathies, and congenital heart defects. As more healthcare systems prioritize chronic disease management through preventive and precision medicine, demand for high-resolution, functional MRI solutions will continue to rise.

Technological Advancements in MRI Systems

The Magnetic Resonance market is significantly propelled by continuous technological advancements that enhance imaging capabilities, patient comfort, and clinical utility. Innovations such as ultra-high-field MRI (7T), silent scan technology, diffusion tensor imaging, and real-time functional MRI (fMRI) are transforming diagnostic outcomes. High-field MRI systems provide superior resolution and contrast, enabling clinicians to detect microstructural changes in tissues crucial for early-stage cancer detection and neuroimaging.

Moreover, developments in parallel imaging and compressed sensing algorithms are drastically reducing scan times, making procedures more tolerable for patients and efficient for operators. Silent MRI, pioneered by players like GE Healthcare, addresses the discomfort of loud scan noises, improving patient compliance, especially in pediatric and geriatric segments.

Simultaneously, AI-powered automation is streamlining workflow and interpretation, making MRI more accessible to low-resource settings. Technological convergence with wearable sensors and tele-radiology platforms also supports remote diagnostics and mobile imaging services. Furthermore, cryogen-free MRI systems are lowering installation and maintenance costs, making them viable for smaller facilities.

Restraints in the Global Magnetic Resonance Imaging Market

High Cost and Operational Complexity

One of the most prominent restraints in the Magnetic Resonance market is the high capital and operational cost associated with MRI systems. High-field MRI scanners (1.5T and above) can cost anywhere from USD 1.2 million to over USD 3 million, not including expenses related to installation, shielding, and facility remodeling.

Additionally, operating these systems requires a constant supply of liquid helium for superconducting magnets, specialized maintenance, and trained radiologic technologists. The cost of siting and shielding an MRI suite is often prohibitive for smaller clinics and rural healthcare centers.

Furthermore, the need for high bandwidth data storage, dedicated PACS infrastructure, and trained radiologists for interpretation adds to the total cost of ownership. These economic constraints limit adoption, especially in emerging economies and smaller practices. Insurance reimbursements for MRI procedures are also under pressure, particularly in regions like Europe and the U.S., where payers are encouraging use of lower-cost imaging modalities like ultrasound or CT when appropriate.

Limited Availability of Skilled Workforce

The Magnetic Resonance market also faces a critical bottleneck in terms of human resources. Operating and interpreting MRI scans require specialized skills not easily acquired without rigorous training. According to the World Health Organization (WHO), many low- and middle-income countries have fewer than one radiologist per 100,000 population, with even fewer MRI-trained technicians.

In advanced economies, the situation is only marginally better, with radiologist burnout and workforce shortages frequently cited in healthcare surveys. The complexity of MRI procedures, including protocol selection, image acquisition, and contrast agent administration, demands a high level of expertise to avoid diagnostic errors.

Furthermore, subspecialties like neuroimaging or cardiac MRI require advanced training not commonly available in standard radiology programs. While some automation tools are emerging, they are not yet capable of replacing skilled personnel entirely. Regulatory bodies like the U.S. FDA and EMA require trained operators for diagnostic imaging, which limits the scale-up of MRI services.

Opportunities in the Global Magnetic Resonance Imaging Market

Expanding Healthcare Access in Emerging Markets

Emerging economies present a significant untapped opportunity for the Magnetic Resonance market. Countries in Asia-Pacific, Latin America, and Africa are witnessing rapid healthcare it infrastructure development fueled by rising incomes, urbanization, and government-led health reforms. These regions still face limited access to advanced diagnostic imaging technologies like MRI due to high equipment costs and a lack of trained personnel. However, public and private sector initiatives are changing this dynamic.

For instance, India’s Ayushman Bharat scheme and China’s Healthy China 2030 agenda are actively promoting access to quality diagnostic services, including imaging. Vendors are responding by developing cost-effective, easy-to-maintain MRI systems tailored for low- and middle-income markets.

Compact MRI units and refurbished systems are gaining traction in rural and tier-2 cities. Furthermore, local manufacturing incentives and public-private partnerships are accelerating adoption. The World Bank and WHO also support diagnostic infrastructure projects in Africa, presenting a pipeline for MRI penetration.

Growing Application in Research and Drug Development

Magnetic Resonance systems are increasingly being adopted in clinical research and pharmaceutical development, offering lucrative opportunities for market growth. MRI’s ability to provide detailed anatomical and functional imaging without ionizing radiation makes it ideal for studying disease progression, evaluating drug efficacy, and conducting safety assessments in both animals and humans. Academic medical centers and CROs (Contract Research Organizations) are using MRI in neurological, cardiovascular, and musculoskeletal studies.

Advanced techniques like functional MRI (fMRI), magnetic resonance spectroscopy (MRS), and diffusion-weighted imaging (DWI) are enabling researchers to quantify biomarkers and track treatment responses in real time. The U.S. National Institutes of Health (NIH) and the European Union’s Horizon Europe program provide significant funding for MRI-based research. Additionally, MRI is being incorporated into Phase I–III clinical trials to obtain non-invasive endpoints for regulatory submission.

Trends in the Global Magnetic Resonance Imaging Market

Integration of AI in MRI Imaging

One of the defining trends in the Magnetic Resonance (MR) market is the growing integration of artificial intelligence (AI) in MRI technology. AI is increasingly used for improving image reconstruction, reducing scan times, and enhancing diagnostic accuracy.

Deep learning algorithms are being trained to interpret MRI scans faster and more accurately, helping radiologists make precise diagnoses in less time. Vendors are also embedding AI capabilities into MRI systems to automate routine tasks like organ segmentation, tumor detection, and scan protocol optimization. This trend is leading to more personalized and predictive medicine, which is critical for value-based healthcare.

Additionally, AI-driven noise reduction and motion correction algorithms are significantly improving image clarity in patients who cannot stay still during scans, such as children or elderly individuals. Companies like Siemens Healthineers and GE Healthcare have incorporated AI-based solutions into their MRI platforms, indicating a broader industry movement. Hospitals and imaging centers are increasingly adopting AI-assisted MRI tools to improve operational efficiency and patient throughput.

Shift Towards Outpatient and Point-of-Care MRI Solutions

The Magnetic Resonance market is experiencing a significant trend towards decentralization of imaging services, with a focus on outpatient and point-of-care MRI solutions. Traditionally confined to large hospitals due to size, cost, and infrastructure needs, MRI technology is now being adapted for smaller, more flexible setups. Manufacturers are developing compact, portable, and energy-efficient MRI systems that can be installed in outpatient centers, specialty clinics, and even rural facilities with limited resources.

This shift is driven by the increasing demand for accessible diagnostic services and faster patient turnaround without compromising image quality. Open and ultra-low-field MRI systems are being deployed in orthopedic, sports medicine, and rehabilitation clinics, addressing specific clinical needs with minimal operational complexity.

Additionally, innovations in cryogen-free technology and lightweight superconducting magnets are allowing broader adoption outside traditional settings. Healthcare policies emphasizing patient-centric care and cost reduction are further reinforcing this trend. For instance, the U.S. Centers for Medicare & Medicaid Services (CMS) encourages outpatient diagnostic services to reduce hospital burden.

Global Magnetic Resonance Imaging Market: Research Scope and Analysis

By Architecture Analysis

Closed MRI systems are projected to dominate the MRI market due to their superior image resolution, higher magnetic field strength, and broad clinical applicability. These systems are enclosed cylindrical machines that offer a controlled environment, ideal for high-precision imaging. Closed MRI scanners typically operate in the 1.5T to 3T field strength range, which provides a greater signal-to-noise ratio, enabling detailed visualization of organs, tissues, and abnormalities.

These systems are widely used in hospitals and large diagnostic centers, especially in applications like neurology, cardiology, oncology, and musculoskeletal imaging, where clarity and accuracy are paramount. Their ability to generate clearer, more detailed images supports earlier and more reliable diagnoses, which is critical in time-sensitive conditions like strokes or tumors.

Despite concerns over patient discomfort due to claustrophobia or size limitations, advancements such as noise reduction, larger bore diameters, and faster scanning times have significantly improved the patient experience in recent years. Moreover, the high utilization rate of closed MRI systems in developed countries, coupled with increasing adoption in emerging economies, further strengthens their market dominance.

Additionally, reimbursement policies in regions like North America and Europe tend to favor the use of high-performance imaging systems, giving closed MRI systems a further edge over open or portable alternatives. While open systems offer comfort, they often sacrifice image quality, particularly in high-detail scans. As such, the clinical superiority and broader diagnostic range of closed MRI systems have made them the go-to choice for comprehensive medical imaging, positioning them as the dominant architecture in the global MRI market.

By Field Strength Analysis

High field MRI systems, specifically those operating between 1.5T and 3T, are poised to represent the dominant segment in the MRI market due to their optimal balance of image quality, scan speed, and diagnostic versatility. These systems produce high signal-to-noise ratios, allowing for detailed and accurate imaging across a wide array of clinical applications, including neurology, cardiology, musculoskeletal, oncology, and abdominal scans.

The 1.5T systems are considered the clinical standard, particularly in developed markets, as they are cost-effective while still delivering excellent image resolution. Meanwhile, 3T systems, which offer twice the field strength of 1.5T, provide even sharper images and faster scan times, making them ideal for advanced imaging needs such as functional MRI (fMRI) or complex neurological assessments.

Healthcare providers prefer high-field systems because they support a wide range of coil configurations and advanced imaging techniques like spectroscopy and diffusion tensor imaging (DTI). These features help physicians detect disease earlier and plan treatments more effectively, which is essential in value-based care environments.

In comparison, low field systems (<0.5T) are primarily used in niche applications due to their limited imaging power, and very high field systems (>3T) are largely confined to research and academic settings due to regulatory and cost constraints. High field MRI systems hit the sweet spot, combining clinical efficacy with economic viability.

The global rise in chronic disease prevalence, increasing investment in advanced diagnostic infrastructure, and growing demand for minimally invasive diagnostic tools are expected to keep this segment at the forefront of MRI adoption worldwide.

By Mobility Analysis

Fixed room MRI systems are anticipated to dominate the MRI mobility segment due to their widespread use in hospitals and imaging centers where high patient throughput, clinical precision, and comprehensive diagnostic capabilities are required. These systems are permanently installed in controlled environments that are specially constructed with appropriate shielding, HVAC systems, and power infrastructure to ensure optimal system performance and patient safety.

Fixed systems are primarily associated with high-field MRI units (1.5T and 3T), which are used for complex diagnostic procedures such as neurological, musculoskeletal, cardiovascular, and oncological imaging. Their ability to accommodate a wide range of coils, support contrast-enhanced imaging, and integrate with Picture Archiving and Communication Systems (PACS) makes them indispensable in full-scale diagnostic settings.

Hospitals prefer fixed MRI systems because they can be used around the clock without the logistical constraints of mobility. Their integration with other radiological services enhances workflow efficiency and ensures faster diagnosis, which is critical for emergency cases. The high return on investment from consistent patient volumes further justifies the capital expense.

In contrast, mobile trailer-based systems, while useful in rural or underserved areas, face limitations such as lower image quality (typically with mid or low field systems), logistical challenges in transportation and setup, and restricted use of advanced imaging techniques. These systems serve as supplements rather than replacements for fixed installations.

As global healthcare systems continue to scale diagnostic capabilities, especially in urban and tertiary care centers, the demand for fixed room MRI systems is expected to maintain dominance, supported by technological innovation, rising chronic disease incidence, and expanded hospital infrastructure.

By Application Analysis

Neurology is expected to represent the dominant application segment in the MRI market, primarily due to the unmatched capabilities of MRI in visualizing the brain and central nervous system (CNS) with high-resolution, non-invasive imaging. MRI is the gold standard for diagnosing and monitoring a wide range of neurological conditions, including strokes, brain tumors, multiple sclerosis, epilepsy, traumatic brain injuries, and neurodegenerative disorders such as Alzheimer’s and Parkinson’s disease.

The ability of MRI to differentiate between gray and white matter, detect minute structural abnormalities, and evaluate cerebral blood flow makes it indispensable for neurologists. Advanced modalities like functional MRI (fMRI), diffusion-weighted imaging (DWI), and magnetic resonance angiography (MRA) further enhance diagnostic precision by mapping brain activity, identifying acute ischemia, and assessing vascular structures.

The rising global incidence of neurological disorders driven by aging populations, sedentary lifestyles, and increased awareness has significantly fueled demand for MRI in this segment. Additionally, the growing use of MRI in psychiatric evaluations and pre-surgical planning (especially in epilepsy and brain tumor surgeries) has expanded its clinical relevance.

Unlike other applications, such as musculoskeletal or abdominal imaging, neurological conditions often require repeat scans over time to monitor disease progression or treatment response. This increases the per-patient utilization rate of MRI systems in neurology, boosting its market share.

Investment in neuroscience research, along with integration of AI-driven brain mapping and real-time monitoring technologies, continues to elevate the role of MRI in neurology. This firmly positions it as the leading application segment within the global MRI market.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By End User Analysis

Hospitals are expected to dominate the end-user segment of the MRI market due to their comprehensive diagnostic infrastructure, high patient volume, and financial capacity to invest in advanced imaging technologies. Most hospitals, especially tertiary care and multi-specialty institutions, are equipped with fixed high-field MRI systems (1.5T or 3T) that support a wide spectrum of clinical applications, from routine screening to complex diagnostics.

Hospitals often act as referral centers for smaller clinics and rural health facilities, further increasing MRI utilization rates. They cater to both inpatients and outpatients and frequently require MRI imaging for pre-surgical planning, post-operative assessments, and emergency diagnostics, especially for neurology, cardiology, trauma, and oncology cases.

Unlike standalone imaging centers or ambulatory surgical centers, hospitals often participate in government-funded health programs, clinical research, and academic collaborations, increasing the demand for advanced MRI features like spectroscopy, fMRI, and real-time image guidance. Their integrated radiology departments also enable efficient PACS management, multi-modality comparison, and immediate physician consultation.

Hospitals are also at the forefront of adopting next-generation MRI systems with AI integration, reduced scan times, enhanced resolution, and improved patient comfort (such as wide-bore systems). These advancements support their strategic goals of improving diagnostic accuracy, reducing patient wait times, and enhancing outcomes.

In contrast, imaging centers and ASCs often focus on cost-efficiency and volume, limiting the adoption of premium technologies. As healthcare infrastructure expands, particularly in emerging markets, hospitals will continue to be the primary purchasers and users of MRI systems, securing their position as the dominant end-user in the global market.

The Global Magnetic Resonance Imaging Market Report is segmented on the basis of the following:

By Architecture

- Closed MRI Systems

- Open MRI Systems

- Portable/Point-of-Care MRI Systems

By Field Strength

- Low Field MRI Systems (<0.5T)

- Mid Field MRI Systems (0.5T–1.5T)

- High Field MRI Systems (1.5T–3T)

- Very High Field MRI Systems (3T–7T and above)

By Mobility

- Fixed Room Systems

- Mobile Trailer-based Systems

By Application

- Neurology (Brain & Nervous System Disorders)

- Obstructive Sleep Apnea

- Spine & Musculoskeletal Imaging

- Cardiology (Cardiac Imaging)

- Oncology (Cancer Detection & Monitoring)

- Abdominal & Pelvic Imaging

- Other Application

By End User

- Hospitals

- Imaging Centers

- Ambulatory Surgical Centers (ASCs)

- Academic & Research Institutes

Impact of Artificial Intelligence in the Global Magnetic Resonance Imaging Market

- Accelerated Scan Times: AI algorithms optimize image acquisition by predicting and reconstructing high-quality images from fewer raw data inputs. This significantly reduces scan time, improving patient throughput and comfort while lowering operational costs.

- Enhanced Image Quality & Precision: AI enhances image clarity by reducing noise and correcting artifacts, enabling more accurate detection of lesions, tumors, and structural abnormalities. This is especially beneficial in neurology, oncology, and cardiovascular MRI applications.

- Automated Image Analysis & Reporting: AI-driven software enables automatic detection, segmentation, and quantification of anatomical structures. It reduces radiologist workload, minimizes human error, and provides faster, more consistent reporting across imaging centers.

- Workflow Optimization & Scheduling: AI streamlines the entire MRI workflow from patient scheduling and protocol selection to image post-processing by using predictive analytics and adaptive protocols. This leads to reduced waiting times and improved operational efficiency.

- Personalized & Predictive Diagnostics: AI integrates imaging data with patient records to support personalized diagnosis and treatment planning. Machine learning models can predict disease progression, treatment response, and recurrence, elevating the clinical utility of MRI in precision medicine.

Global Magnetic Resonance Imaging Market: Regional Analysis

Region with the Largest Revenue Share

North America is projected to lead the global Magnetic Resonance (MR) market as it holds 38.0% of the total market revenue by the end of 2025, due to its strong healthcare infrastructure, early adoption of medical technologies, and a high volume of advanced diagnostic procedures. The United States, in particular, has a dense network of tertiary care hospitals, academic research centers, and specialized imaging clinics equipped with high-field and ultra-high-field MRI systems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Supportive reimbursement policies under Medicare and Medicaid, coupled with private insurance coverage, promote higher MRI utilization rates across various clinical segments such as neurology, oncology, cardiology, and musculoskeletal imaging. The region also benefits from a well-established medical device regulatory framework led by the FDA, which facilitates the timely approval of innovative MRI technologies and upgrades.

Moreover, the prevalence of chronic diseases such as Alzheimer’s, stroke, cancer, and cardiovascular conditions is significantly high in North America, driving demand for precise and early diagnosis using MRI. The U.S. Census Bureau projects a rise in the aging population, with adults aged 65 and over expected to reach over 80 million by 2040, fueling demand for non-invasive diagnostic imaging.

Academic institutions and research organizations across the U.S. and Canada continue to play a pivotal role in clinical trials and advancements in MRI applications, including functional and molecular imaging. These factors collectively strengthen the region’s leadership in both demand and innovation.

Region with the Highest CAGR

Asia Pacific is expected to register the fastest CAGR in the global Magnetic Resonance market due to increasing healthcare investments, growing disease burden, and rapid technological diffusion. Countries like China, India, South Korea, and Japan are investing heavily in healthcare infrastructure development, especially in underserved rural and tier-2 cities.

The rising middle class and improved healthcare access are significantly expanding the patient base eligible for MRI diagnostics. Moreover, national health policies such as India’s Ayushman Bharat and China’s Healthy China 2030 are increasing insurance coverage and public hospital funding, indirectly boosting MRI adoption.

The region is also witnessing rapid urbanization and lifestyle shifts, leading to a surge in chronic diseases such as diabetes, cardiovascular conditions, and neurological disorders, all of which require advanced imaging for effective diagnosis and treatment planning. According to the Ministry of Health, Labour and Welfare in Japan and the National Health Commission of China, imaging volumes have increased substantially over the last decade.

In addition, domestic manufacturers in China and Japan are developing cost-effective MRI systems that meet local needs while maintaining quality standards, improving affordability, and adoption across the public and private sectors.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Global Magnetic Resonance Imaging Market: Competitive Landscape

The Magnetic Resonance market features an intensely competitive landscape marked by innovation, global expansion, and increasing partnerships. Leading players include Siemens Healthineers, GE HealthCare, Philips Healthcare, Canon Medical Systems, and Fujifilm Holdings.

These companies continuously invest in product upgrades, including compact MRI systems, silent scanning technology, AI-driven image processing, and portable MRI devices to differentiate their offerings in a saturated market. For instance, Siemens and GE have launched 1.5T and 3T systems that deliver faster scans with reduced noise and improved clarity, targeting outpatient clinics and diagnostic centers.

Emerging players such as Hyperfine and United Imaging are disrupting the space with cost-effective and mobile MRI solutions, targeting developing regions and smaller facilities that lack access to conventional MRI infrastructure. Competitive intensity is also heightened by collaborations with academic institutions and hospitals to develop specialized MR applications for neurology, oncology, and pediatric imaging.

Companies are also focusing on software integration and workflow automation as key differentiators. AI-based imaging reconstruction, automated scan protocols, and cloud-based PACS (Picture Archiving and Communication Systems) are increasingly being bundled with MRI systems.

Furthermore, after-sales services, training programs, and financing packages are critical strategic levers, especially in cost-sensitive regions like Asia and Latin America. Regulatory approvals and compliance with international safety standards further shape the competitive dynamics, as companies aim for faster market penetration and broader global reach in a tightly regulated medical imaging environment.

Some of the prominent players in the Global Magnetic Resonance Imaging Market are:

- Siemens Healthineers

- GE HealthCare

- Philips Healthcare

- Canon Medical Systems Corporation

- Hitachi Ltd. (now part of Fujifilm Healthcare)

- Fujifilm Holdings Corporation

- United Imaging Healthcare

- Esaote SpA

- Neusoft Medical Systems

- Hologic Inc.

- Bruker Corporation

- Aurora Imaging Technology

- Time Medical Systems

- Hyperfine Inc.

- IMRIS

- Aspect Imaging

- Medonica Co. Ltd.

- AllTech Medical Systems

- MR Solutions Ltd.

- Other Key Players

Recent Developments in the Global Magnetic Resonance Imaging Market

- January 2025: Quibim raised USD 50 million in Series A funding to advance AI-powered imaging biomarker technology. The funds will be used to expand globally and enhance clinical decision-making tools in MRI diagnostics.

- December 2024: Hyperfine Inc. expanded its distribution network by partnering with medical device companies in Europe and the Middle East, aiming to accelerate the global adoption of its portable point-of-care MRI systems.

- December 2024: Siemens Healthineers introduced AI-enabled upgrades to its Magnetom Flow 1.5T MRI platform, significantly enhancing image quality and reducing scan time through deep learning-based reconstruction technologies.

- December 2024: Philips launched its next-generation BlueSeal MRI system, a helium-free 1.5T scanner with sustainable design and reduced operational costs, introduced during RSNA 2024 to meet increasing demand for eco-friendly imaging systems.

- November 2024: GE Healthcare introduced the SIGNA Champion 1.5T MRI system, incorporating advanced AI features like AIR Recon DL and Sonic DL to enhance scan speed, image clarity, and overall patient experience.

- November 2024: Philips expanded its collaboration with SyntheticMR, launching SyMRI 3D to improve quantitative brain imaging. This strategic alliance supports more accurate assessments in neurological and psychiatric applications.

- May 2024: Siemens Healthineers launched the Magnetom Terra 7T, the first ultra-high-field MRI system approved for clinical use, delivering unmatched spatial resolution for detailed brain, spine, and musculoskeletal imaging.

- May 2024: GE Healthcare installed a prototype high-end neuroimaging MRI scanner at Brigham and Women’s Hospital, targeting FDA clearance for advanced clinical research in neurological disorders and cognitive mapping.

- May 2024: Fischer Medical Ventures began local MRI production in India, marking the country's first domestically manufactured MRI units, aimed at reducing import dependence and promoting self-reliance in medical imaging technologies.

Report Details

| Report Characteristics |

| Market Size (2025) |

USD 8,598.8 Mn |

| Forecast Value (2034) |

USD 16,171.4 Mn |

| CAGR (2025–2034) |

7.3% |

| Historical Data |

2019 – 2024 |

| The US Market Size (2025) |

USD 2,748.0 Mn |

| Forecast Data |

2025 – 2033 |

| Base Year |

2024 |

| Estimate Year |

2025 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors, etc. |

| Segments Covered |

By Architecture (Closed, Open, and Portable/Point-Of-Care MRI Systems), By Field Strength (Low, Mid, High, and Very High Field MRI Systems), By Mobility (Fixed Room, and Mobile Trailer-Based Systems), By Application (Neurology, Obstructive Sleep Apnea, Spine & Musculoskeletal Imaging, Cardiology, Oncology, Abdominal & Pelvic Imaging, and Other Application), and By End User (Hospitals, Imaging Centers, Ambulatory Surgical Centers, and Academic & Research Institutes). |

| Regional Coverage |

North America – US, Canada; Europe – Germany, UK, France, Russia, Spain, Italy, Benelux, Nordic, Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, Rest of MEA |

| Prominent Players |

Siemens Healthineers, GE HealthCare, Philips Healthcare, Canon Medical Systems, Fujifilm (including Hitachi), United Imaging, Esaote, Neusoft, Hologic, Bruker, Aurora Imaging, Time Medical, Hyperfine, IMRIS, Aspect Imaging, Medonica, AllTech Medical Systems, and MR Solutions Ltd., and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users), and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days, and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Magnetic Resonance Imaging Market?

▾ The Global Magnetic Resonance Imaging Market size is estimated to have a value of USD 8,598.8 million in 2025 and is expected to reach USD 16,171.4 million by the end of 2034.

What is the growth rate in the Global Magnetic Resonance Imaging Market in 2025?

▾ The market is growing at a CAGR of 7.3 percent over the forecasted period of 2025.

What is the size of the US Magnetic Resonance Imaging Market?

▾ The US Magnetic Resonance Imaging Market is projected to be valued at USD 2,748.0 million in 2025. It is expected to witness subsequent growth in the upcoming period as it holds USD 4,991.7 million in 2034 at a CAGR of 6.9%.

Which region accounted for the largest Global Magnetic Resonance Imaging Market?

▾ North America is expected to have the largest market share in the Global Magnetic Resonance Imaging Market with a share of about 38.0% in 2025.

Who are the key players in the Global Magnetic Resonance Imaging Market?

▾ Some of the major key players in the Global Magnetic Resonance Imaging Market are Siemens Healthineers, GE HealthCare, Philips Healthcare, Canon Medical Systems, Fujifilm (including Hitachi), United Imaging, and many others.