What is the Managed Services Market Size?

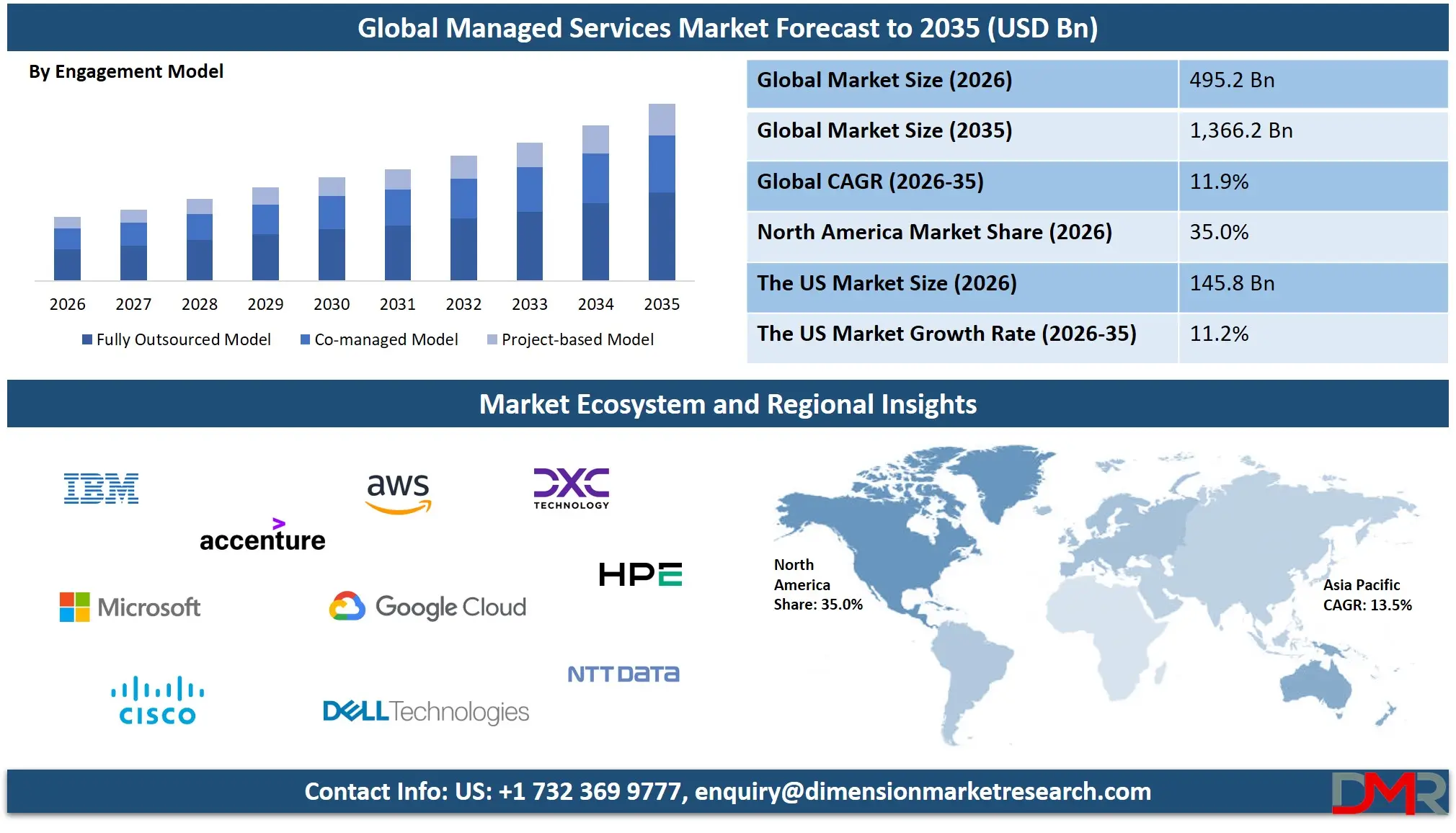

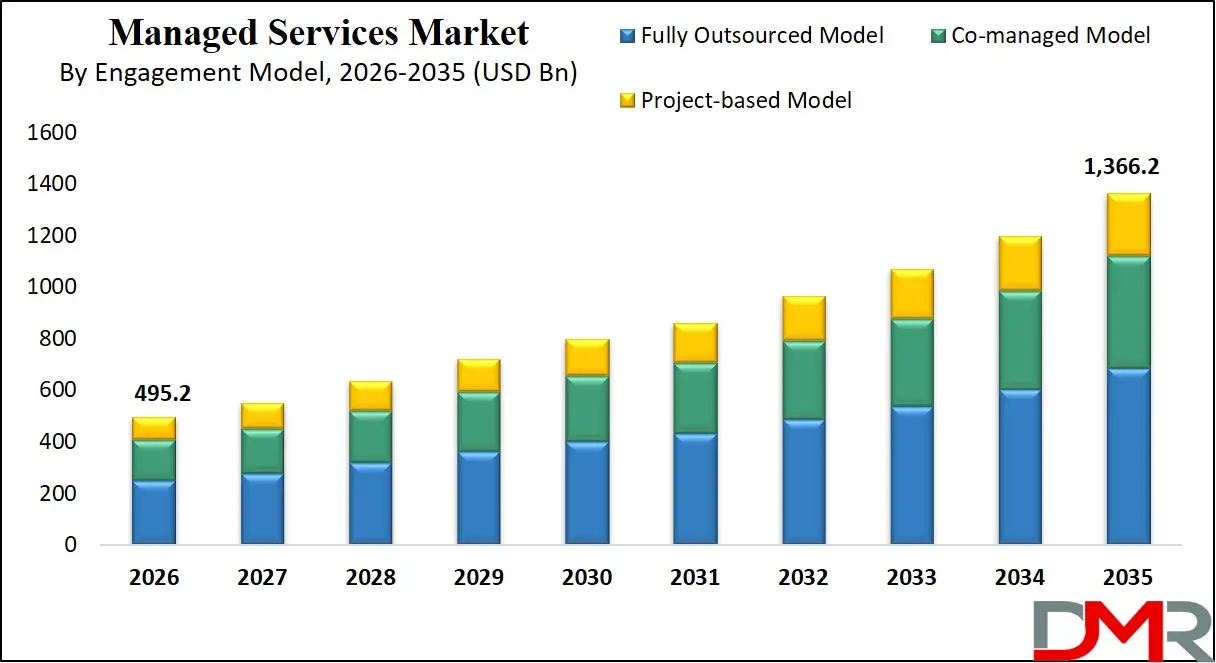

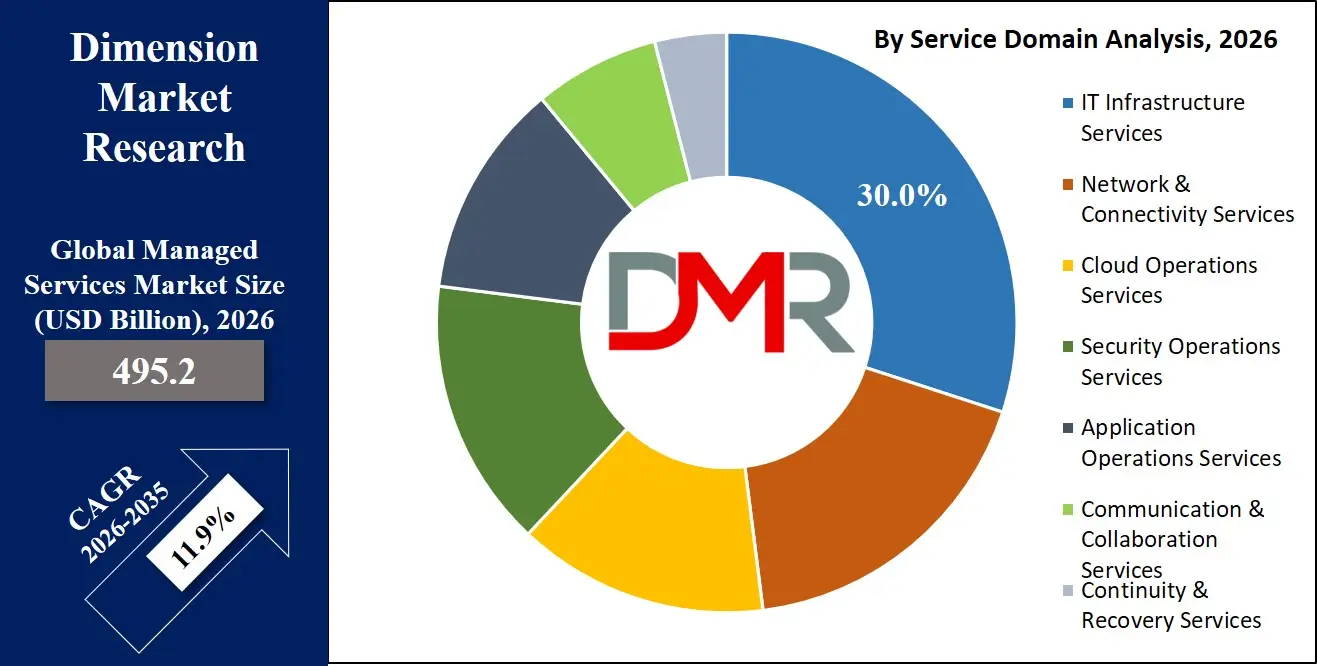

The Global Managed Services Market is projected to reach USD 495.2 billion in 2026 and grow at a CAGR of 11.9% to USD 1,366.2 billion by 2035, driven by IT outsourcing, cloud services, cybersecurity, and AI-led digital transformation.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Managed Services Market is the outsourcing of IT infrastructure, applications, and security and business operations to third party vendors in order to achieve efficiency and scalability. It is expanding as a result of the fast adoption of hybrid and multi-cloud environments which necessitates constant management. OECD studies on the digital economy show that the world is moving to an outsourced IT model in an effort to enhance productivity and resilience.

The World Bank data of digital development demonstrates an increase in digitization and internet penetration as the primary drivers of demand, particularly in developing economies. The rising cybersecurity threats are also driving the growth in demand of managed security services. The AI automation, cloud-native adoption, and multi-cloud orchestration will drive future growth. On the whole, it is one of the enablers of enterprise digital transformation and continuity of operations.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

US Managed Services Market

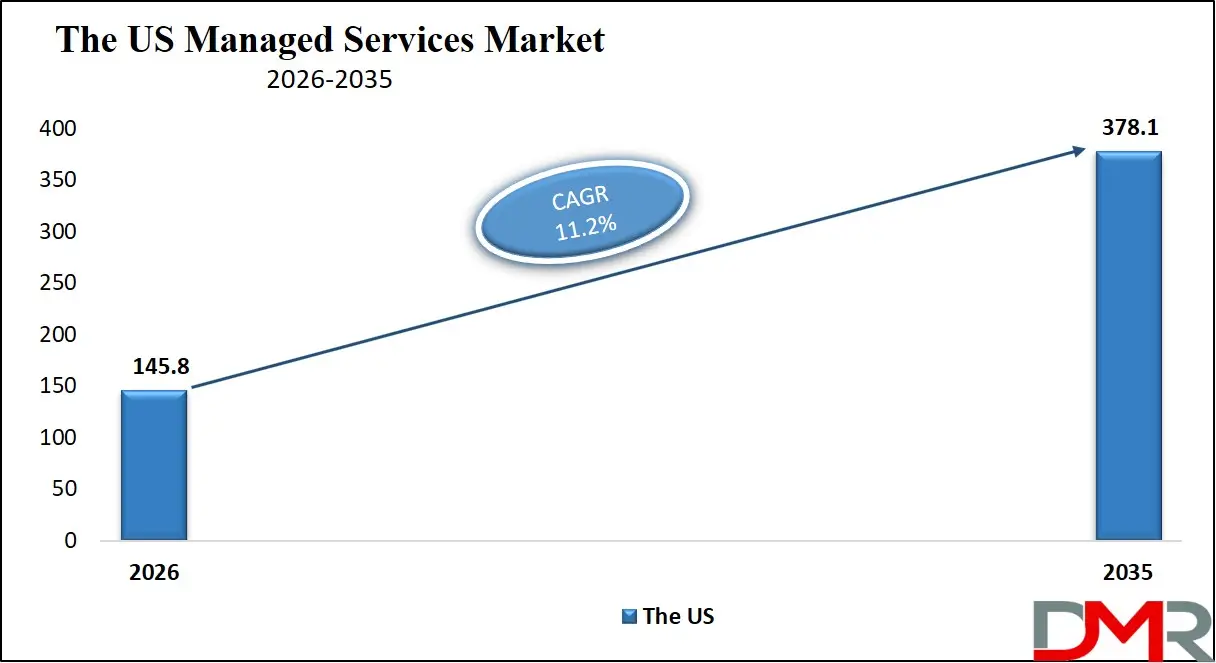

The US Managed Services Market is projected to reach USD 145.8 billion in 2026 and grow at a compound annual growth rate of 11.2%, reaching USD 378.1 billion by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US Managed Services Market is the largest globally, driven by IT outsourcing, cloud managed services, cybersecurity demand, and strong enterprise digital transformation. It is supported by advanced digital infrastructure, hybrid cloud adoption, and rising AI-based IT operations across enterprises. Increasing regulatory compliance requirements and growing cyber threats are further accelerating demand for managed security and governance services.

Europe Managed Services Market

Europe Managed Services Market is expected to grow to USD 128.2 billion in 2026, with a CAGR of 11.1%. The high rate of enterprise adoption of cloud computing, IT outsourcing and managed cybersecurity services in major industries leads to the growth of the market. The need to comply with more regulation, including GDPR, is further catalyzing the need to seek secure and compliant managed solutions. An increase in digital transformation projects and uptake of hybrid IT is also enhancing the managed services ecosystem of the region.

Japan Managed Services Market

The Japan Managed Services Market is expected to grow to USD 34.6 billion in 2026 with a CAGR of 10.5%. The market is motivated by growing enterprise attention to IT modernization, cloud integration and managed services based on automation. The increasing need to have cybersecurity and data protection solutions is also contributing to market growth. The aging workforce in Japan is also increasing, and this is pushing the outsourcing of IT operations to enhance efficiency and continuity of operations.

Key Takeaways

- Market Size: The Global Managed Services Market is projected to be valued at USD 495.2 billion in 2026 and is expected to reach USD 1,366.2 billion by 2035.

- Growth Rate and Outlook: The market is projected to grow at a CAGR of 11.9% during the forecast period, driven by rising IT outsourcing, cloud adoption, and cybersecurity demand.

- Primary Growth Drivers: Key drivers include rapid enterprise digital transformation, increasing hybrid and multi-cloud adoption, growing cybersecurity risks, and rising demand for cost-efficient IT operations and AI-driven automation.

- By Service Domain Analysis: IT Infrastructure Services are expected to dominate with around 30.0% share in 2026, driven by demand for compute, storage, data center, and endpoint management in hybrid IT environments.

- By Service Function Analysis: Business Process Services are anticipated to lead with approximately 42.0% share in 2026, supported by outsourcing of customer operations, finance, HR, and procurement functions for cost efficiency.

- By Deployment Architecture Analysis: On-premises Managed Services are projected to hold about 44.0% share in 2026, driven by enterprise preference for control, security, and compliance in managing critical IT systems.

- Regional Leadership: North America is expected to lead the market in 2026 due to strong cloud adoption, advanced IT infrastructure, and high enterprise spending on managed services solutions.

What are Managed Services?

Managed Services are outsourcing IT infrastructure, security, applications and operations to third-party vendors to maintain continuous monitoring and optimization using a subscription model. It substitutes reactive IT support with proactive, managed delivery. OECD digital economy indicators observe that there is greater use of outsourced digital services to enhance efficiency and resilience. World Bank figures show an increasing globalization that is leading to demand, particularly in the emerging economies. Some of the major services are cloud management, cybersecurity and network monitoring. The model saves money on IT and enhances scalability. All in all, it helps businesses to concentrate on business core and at the same time, it provides secure and efficient IT operations.

Use Cases

- Cloud Infrastructure Management: Managed services are used to monitor, optimize, and maintain cloud environments across public, private, and hybrid platforms. Providers handle workload balancing, resource scaling, and uptime management to ensure high availability. This helps enterprises reduce infrastructure complexity and improve operational efficiency.

- Cybersecurity Operations: Organizations use managed security services for continuous threat monitoring, detection, and response. Providers manage SOC operations, vulnerability assessments, and compliance enforcement. This reduces exposure to cyber risk while ensuring real-time protection against evolving threats.

- IT Support and Service Desk: Managed services support enterprise IT operations through centralized service desks and incident management systems. They handle user requests, troubleshooting, and system maintenance. This improves response time, reduces downtime, and enhances end-user productivity.

- Data Backup and Disaster Recovery: Enterprises rely on managed services for automated data backup, recovery planning, and disaster recovery execution. Providers ensure data integrity and rapid restoration during system failures or cyber incidents. This strengthens business continuity and minimizes operational disruption.

How AI is transforming the Managed Services Market?

The Managed Services Market is being transformed by AI to make predictive monitoring, automated incident resolution, and intelligent workload optimization optimizations across IT environments possible. It minimizes the need to use manual processes by automating IT with AI and self-healing infrastructure.

Managed security services improve the speed of cybersecurity threat detection and response with machine learning-based analytics. In sum, AI is transforming the managed services into autonomous, intelligent and highly efficient digital operations rather than reactive support models.

Market Dynamics

Key Drivers in the Global Managed Services Market

Quick Enterprise Digital Transformation

The number of industries where organizations are using digital-first operating models is growing, and it is greatly increasing the need to use managed IT services. Legacy infrastructure is being updated by enterprises, using cloud, automation, and virtualization technologies. This transition needs to be constantly monitored, optimized, and integrated. MSSPs assist in minimizing the complexity of operations and providing scalability and performance. Consequently, the market is experiencing a significant growth driver of digital transformation initiatives.

Increasing Cybersecurity Threat Environment

The increasing rate and intricacy of cyberattacks are compelling businesses to enhance their security stance. Managed security services are being implemented by organizations to maintain round the clock threat detection, incident response, and compliance management. This encompasses security at both endpoint, network and cloud levels. Businesses do not have native capability to deal with advanced threats, and they grow more reliant on third parties. Security-based outsourcing therefore is emerging as a major motivator towards adoption of managed services.

Restraints in the Global Managed Services Market

Data security and compliance issues.

The tough regulatory environment is making enterprises more wary of outsourcing IT and data-intensive processes. The BFSI and the healthcare industry have stringent compliance standards in the data sovereignty and privacy legislation. The perception of risk of data exposure is higher when sensitive workloads are transferred to third parties. This restricts the complete adoption of the managed services in some areas and industries. Subsequently, compliance complexity is a significant inhibitor of market growth.

Vendor Lock-in and Dependency Risks.

Organizations tend to encounter issues of excessive dependence on one managed service provider in the long run. The process of moving providers may be complicated, expensive, and time-consuming. This raises issues of flexibility, control of prices and technological flexibility. Businesses could also have restrictions in tailoring services outside vendor-prescribed models. These reasons decrease the confidence of buyers and limit the decision of outsourcing on large scale. Therefore, vendor lock-in is still a serious inhibitor in the market.

Growth Opportunities in the Global Managed Services Market

AI-powered Managed Services Growth

Incorporating artificial intelligence in managed services is establishing powerful chances of smart automation and forecasting IT functions. AI facilitates real-time analytics, automated troubleshooting, and self-healing infrastructure in enterprise settings. This lowers the operating costs and enhances service efficiency and uptime. MSPs are starting to provide AI-driven cloud, security, and application management platforms. With the increasing desire among businesses to have more intelligent IT operational processes, AI-powered managed services are emerging as a major growth pathway to market expansion.

Quick Multi-cloud Environment Proliferation

The use of multi-cloud strategies is gaining popularity among enterprises to eliminate reliance on the vendor and enhance flexibility. This brings a pressure on the need to have single management platforms that would be able to monitor and optimize numerous cloud environments at the same time. The managed service providers are placed to provide orchestration, cost-reduction, and monitoring of performance in a variety of cloud ecosystems. The difficulty in managing distributed cloud infrastructure is increasing the demand of outsourcing. Consequently, the development of multi-clouds is a significant opportunity to service providers in the managed services market.

Trends in the Global Managed Services Market

Narrow Competition in the market and pressure on the prices

The competitive environment of the managed services market is quite strong featuring both global IT powerhouses and small and specialized service providers. This would result in price wars and low profit margins of service providers. Clients usually require cost efficiency and demand high service capability. Big box vendors can provide bundled services, which are difficult to compete with by smaller providers. Such pricing pressure restricts differentiation and affects the long-term profitability in the industry.

Rapid Technological Obsolescence

Managed service providers are facing challenges in keeping up with the rapid change in technology in cloud, cybersecurity and AI. The constant investment is needed to modernize tools, platforms, and competencies. Inability to stay abreast with new technologies may result in a loss of customers to the more modernized competition. Businesses are turning into strong requests of next-generation functionalities like automation and zero-trust security. This is continuous change which poses a significant threat to the long term market performance.

Research Scope and Analysis

By Service Domain Analysis

The service domain segment of the Managed Services Market is likely to be dominated by IT Infrastructure Services with a 30.0% market share in 2026 due to the need to outsource the management of compute, storage, data centers, and endpoint systems to facilitate hybrid IT environments.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Network and connectivity services are also on the rise steadily and allow safe and smooth communication within the enterprise via WAN, SD-WAN and network monitoring systems. Increasing the need of high-performance and always-on connectivity and cloud-based networks is also increasing the pace of adoption in organizations around the world.

By Service Function Analysis

The service function segment of the Managed Services Market is anticipated to be overtaken by Business Process Services with a 42.0% share in 2026 owing to the high rates of enterprise outsourcing of its customer operations, financial, human resource, and procurement functions to enhance efficiency and lower operational expenses. This segment is advantaged by increased demand of scalable and standardized business processes in diverse industries. In conjunction to this, the IT Operations Services are concerned with management of core IT environment such as service desks, incident management, asset tracking and system maintenance. These services guarantee IT uptime, quicker problem fixes, and better operational management.

By Deployment Architecture Analysis

The on-premises Managed Services are projected to dominate the deployment architecture segment with 44.0% share in 2026, as enterprise control, security, and compliance requirements in the management of critical IT infrastructure and legacy systems are likely. The model is commonly used in regulated markets that need data sovereignty. The cloud-native Managed Services are expanding at a high rate because organizations are moving towards scalable and flexible clouds. They allow automated workload management, real-time monitoring, and multi-cloud system integration, which can be used to accelerate digital transformation and enhance operational efficiency.

By Enterprise Size Analysis

It is projected that Large Enterprises will hold the enterprise size segment of the Managed Services Market at 65.0% share in 2026 due to their complex IT infrastructures, multi-location operations, and increased ability to spend on advanced managed services, including cloud, cybersecurity and IT operations. Outsourcing is becoming more important in these organizations to enhance efficiency, scalability, and the results of digital transformation. Conversely, SMEs are also becoming a rapidly developing segment by embracing managed services that enable them to get access to affordable IT skills without extensive infrastructure investments. Advanced IT and security services are becoming more affordable to SMEs through cloud-based delivery models and subscription pricing, which help them in their digital adoption and efficient operation.

By Engagement Model Analysis

It is projected that Fully Outsourced Model will be the leading engagement model segment of the Managed Services Market with a 50.0% share in 2026 as businesses will outsource all the responsibility of their IT infrastructure, applications, and business operations to third-party providers to save costs, achieve scalability, and offload internal workloads. The model is popular among organizations that require end-to-end managed expertise and 24/7 service. Conversely, Co-managed Model is also becoming popular as a partnership model where in-house IT departments collaborate with service providers to run particular operations. It provides more control, flexibility and sharing of knowledge and also uses external experience to perform complicated IT functions and specialized services.

By Pricing Structure Analysis

The Subscription Model will take the largest portion of the pricing structure segment of the Managed Services Market at 60.0% in 2026 due to the predictability of recurring expenses and longer-term contracts of IT, cloud, and security services. It assists with consistent budgeting and uninterrupted provision of services to businesses. Conversely, the Usage-based Model is increasing with organizations implementing flexible, pay-as-you-go pricing, basing it on the actual consumption of resources. It is also extensively deployed in the cloud, allowing to be cost-efficient, scale and have greater financial control over dynamic loads.

By Technology Orientation Analysis

Technology orientation segment will be dominated by Legacy IT Managed Services with a 40.0% share in 2026 due to the continued use of on-premise systems and traditional enterprise IT that needs continuous support and maintenance. Cloud-native Managed Services on the other hand are increasing fast, with organizations moving towards scalable, containerized and automated cloud environments. These services assist microservice, continuous deployment and multi-cloud management, allowing increased agility, quicker innovation and enhanced operational efficiency across contemporary digital infrastructures.

By Industry Vertical Analysis

In 2026, BFSI will take over the industry vertical segment of the Managed Services Market with a 20.0% share due to the high demand of secure, compliant, and scalable IT infrastructure to facilitate banking operations, digital payments, and management of financial data. The industry has a high dependence on managed services in terms of cybersecurity, cloud adoption and regulatory compliance. By contrast, IT & Telecom has been a significant user of managed services because of the large network infrastructure, heavy traffic of data, and constant service demands. This sector relies on network operations, cloud management, and cybersecurity solutions, which would secure uninterrupted connectivity, service availability, and effective digital service provision.

The Global Managed Services Market Report is segmented on the basis of the following:

By Service Domain

- IT Infrastructure Services

- Compute & Server Management

- Storage & Data Infrastructure

- Data Center Operations

- Workplace & Endpoint Infrastructure

- Network & Connectivity Services

- WAN/LAN Operations

- SD-WAN Management

- Network Monitoring & Control

- Edge Connectivity Management

- Cloud Operations Services

- Public Cloud Operations

- Private Cloud Operations

- Multi-cloud Management

- Security Operations Services

- Security Operations Center SOC

- Threat Monitoring & Response

- Identity & Access Operations

- Endpoint Security Operations

- Application Operations Services

- Application Support & Maintenance

- DevOps Operations

- Middleware Operations

- Communication Collaboration Services

- Unified Communications Operations

- Collaboration Platform Management

- Continuity & Recovery Services

- Data Backup Operations

- Disaster Recovery Operations

By Service Function

- Business Process Services

- IT Operations Services

- Data Operations Services

- Industry Process Services

- Customer Experience Services

By Deployment Architecture

- On-Premises Managed Services

- Cloud-native Managed Services

- Hybrid Managed Architecture

By Enterprise Size

By Engagement Model

- Fully Outsourced Model

- Co-managed Model

- Project-based Model

By Pricing Structure

- Subscription Model

- Usage-based Model

- Outcome-based Model

By Technology Orientation

- Legacy IT Managed Services

- Cloud-native Managed Services

- Automation-driven Managed Services

By Industry Vertical

- BFSI

- IT & Telecom

- Healthcare

- Manufacturing

- Retail & E-commerce

- Government & Public Sector

- Energy & Utilities

- Others

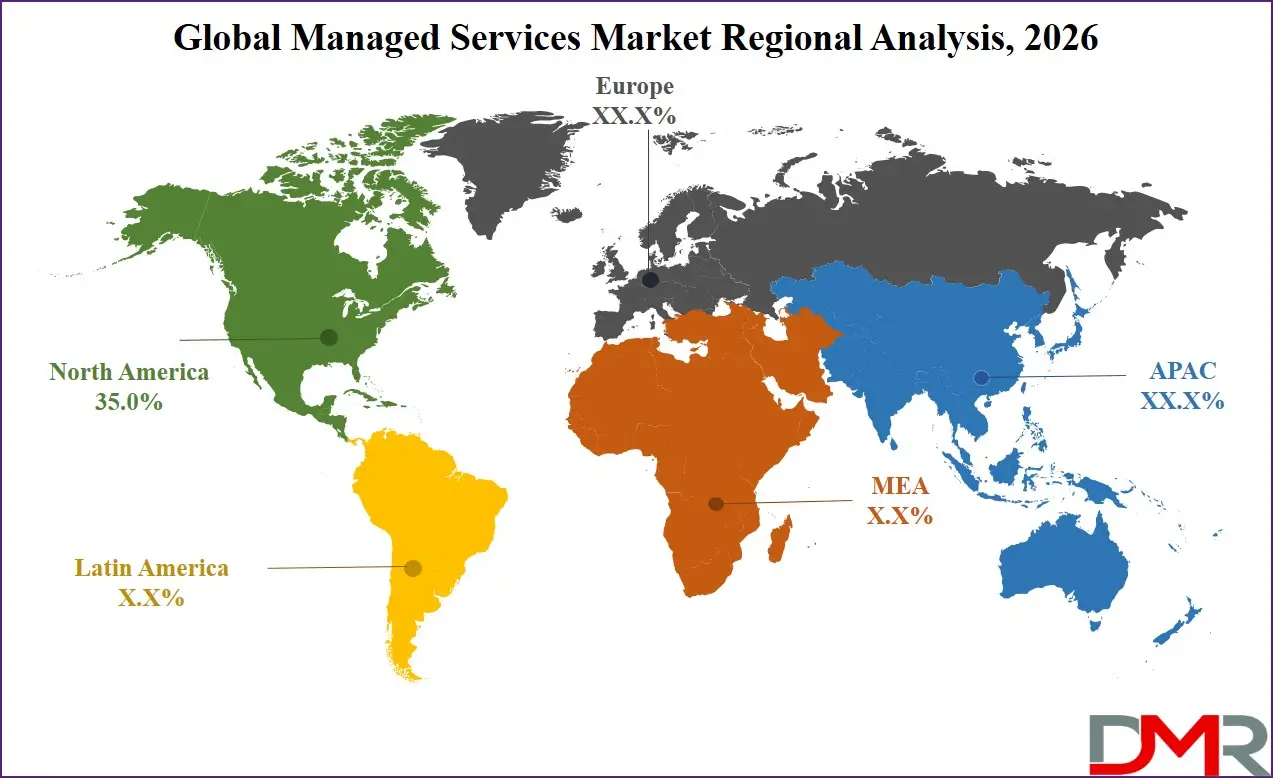

Regional Analysis

Leading Region by Market Share

North America is expected to lead the Managed Services Market with a 35.0% share in 2026, driven by strong adoption of cloud computing, IT outsourcing, and advanced cybersecurity solutions across enterprises. The region benefits from a highly developed digital infrastructure and early adoption of AI-driven IT operations. Strong presence of global technology providers and high enterprise IT spending further reinforce its market dominance.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Regional Market

Asia Pacific is expected to be the fastest-growing regional market in Managed Services due to rapid digital transformation and expanding cloud adoption across enterprises. Increasing SME digitization, rising IT outsourcing demand, and strong government support for digital infrastructure are key growth drivers. The region is also witnessing rapid expansion of cybersecurity and cloud-native service adoption across industries.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive landscape of the Managed Services Market is highly fragmented with the presence of global IT service providers, cloud vendors, and specialized managed service firms. Competition is driven by innovation in cloud management, cybersecurity solutions, and AI-enabled IT operations. Players are focusing on strategic partnerships, mergers, and service expansion to strengthen market position. Pricing pressure and demand for end-to-end integrated solutions are intensifying rivalry across the industry.

Some of the prominent players in the Global Managed Services Market are:

- IBM

- Accenture

- Microsoft

- Cisco

- Amazon Web Services

- Google Cloud

- DXC Technology

- Hewlett Packard Enterprise

- Dell Technologies

- NTT DATA

- Tata Consultancy Services

- Infosys

- Wipro

- HCLTech

- Capgemini

- Cognizant

- Atos

- Kyndryl

- Rackspace Technology

- Fujitsu

- Other Key Players

Recent Developments

- June 2025: Barracuda launched an AI-powered Managed XDR platform integrated with global SOC capabilities to enhance threat detection and automated response for enterprises.

- June 2025: Tech Mahindra introduced a managed multicloud defense service with Cisco to deliver secure cloud operations and unified cybersecurity across hybrid environments.

- June 2025: Netgear acquired cybersecurity startup Exium to strengthen its managed security services portfolio for MSP ecosystems and enterprise networking solutions.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 495.2 Bn |

| Forecast Value (2035) |

USD 1,366.2 Bn |

| CAGR (2026–2035) |

11.9% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Service Domain (IT Infrastructure Services, Network & Connectivity Services, Cloud Operations Services, Security Operations Services, Application Operations Services, Communication Collaboration Services, Continuity & Recovery Services), By Service Function (Business Process Services, IT Operations Services, Data Operations Services, Industry Process Services, Customer Experience Services), By Deployment Architecture (On-Premises Managed Services, Cloud-native Managed Services, Hybrid Managed Architecture), By Enterprise Size (Large Enterprises, SMEs), By Engagement Model (Fully Outsourced Model, Co-managed Model, Project-based Model), By Pricing Structure (Subscription Model, Usage-based Model, Outcome-based Model), By Technology Orientation (Legacy IT Managed Services, Cloud-native Managed Services, Automation-driven Managed Services), By Industry Vertical (BFSI, IT & Telecom, Healthcare, Manufacturing, Retail & E-commerce, Government & Public Sector, Energy & Utilities, Others) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Managed Services Market?

▾ The Global Managed Services Market is projected to be valued at USD 495.2 billion in 2026 and is expected to reach USD 1,366.2 billion by 2035.

What is the CAGR of the Managed Services Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 11.9% during the forecast period.

What factors are driving the growth of the Managed Services Market?

▾ Growth is driven by enterprise digital transformation, rising hybrid and multi-cloud adoption, increasing IT outsourcing demand, and growing cybersecurity threats. Cost optimization needs and AI-driven IT automation are also key drivers.

What are the major trends in the Managed Services Market?

▾ Key trends include AI-enabled IT operations, zero-trust security adoption, multi-cloud orchestration, subscription-based pricing models, and automation-led service delivery.

Which region held the largest share of the Managed Services Market in 2026?

▾ North America held the largest market share of 35.0% in 2026 due to advanced IT infrastructure and high cloud adoption.

Which region is expected to grow the fastest in the Managed Services Market?

▾ Asia Pacific is expected to grow at the fastest rate due to rapid digitalization, increasing SME adoption, and expanding cloud ecosystems.

Who are the key players in the Managed Services Market?

▾ IBM, Accenture, Microsoft, Cisco, Amazon Web Services, Google Cloud, DXC Technology, Hewlett Packard Enterprise, Dell Technologies, NTT DATA, Tata Consultancy Services, Infosys, Wipro, HCLTech, Capgemini, Cognizant, Atos, Kyndryl, Rackspace Technology, Fujitsu, and other key players.

How is the Managed Services Market segmented?

▾ The market is segmented By Service Domain, By Service Function, By Deployment Architecture, By Enterprise Size, By Engagement Model, By Pricing Structure, By Technology Orientation, and By Industry Vertical.