What is the Medical Device Testing Services Market Size?

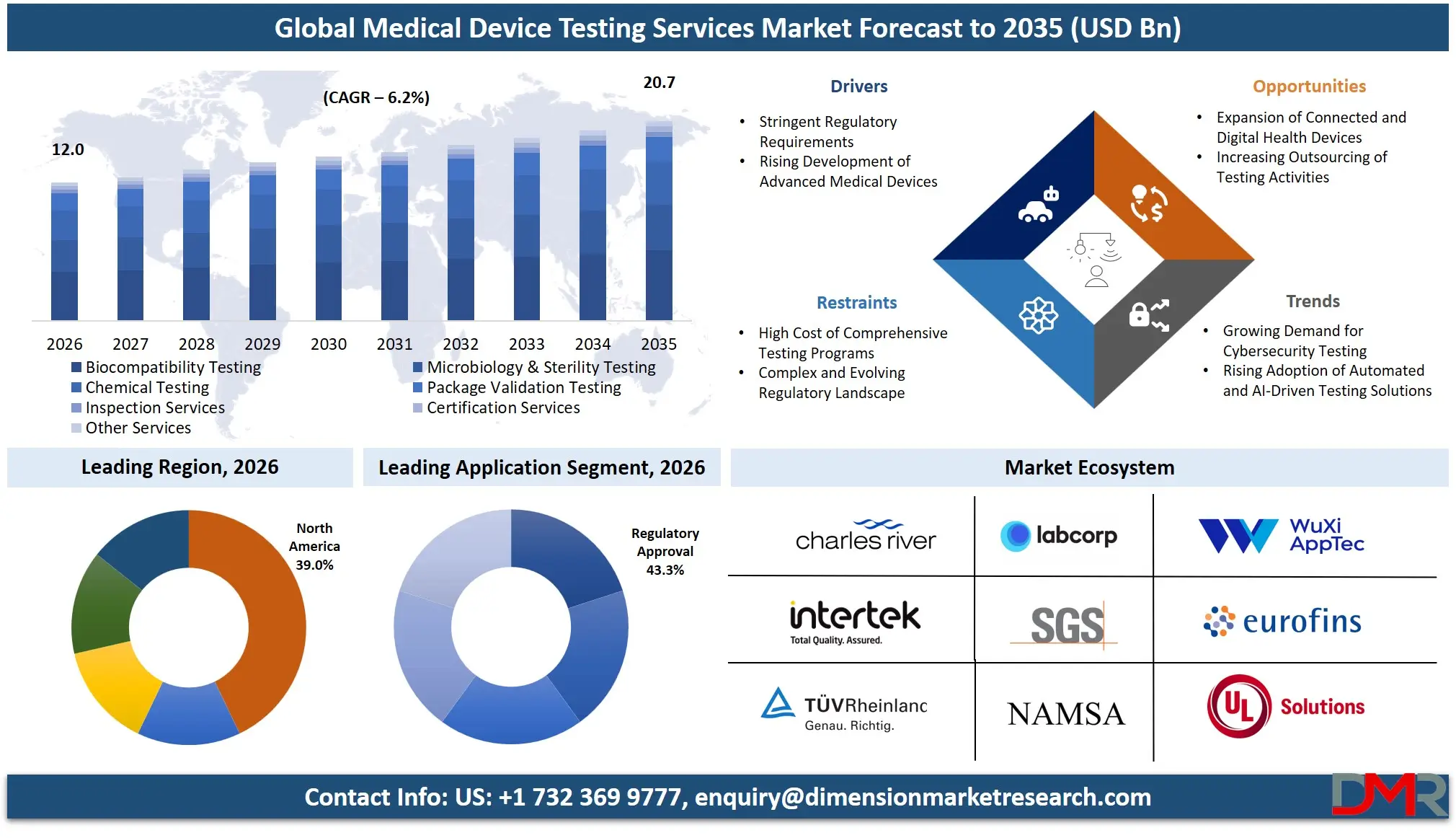

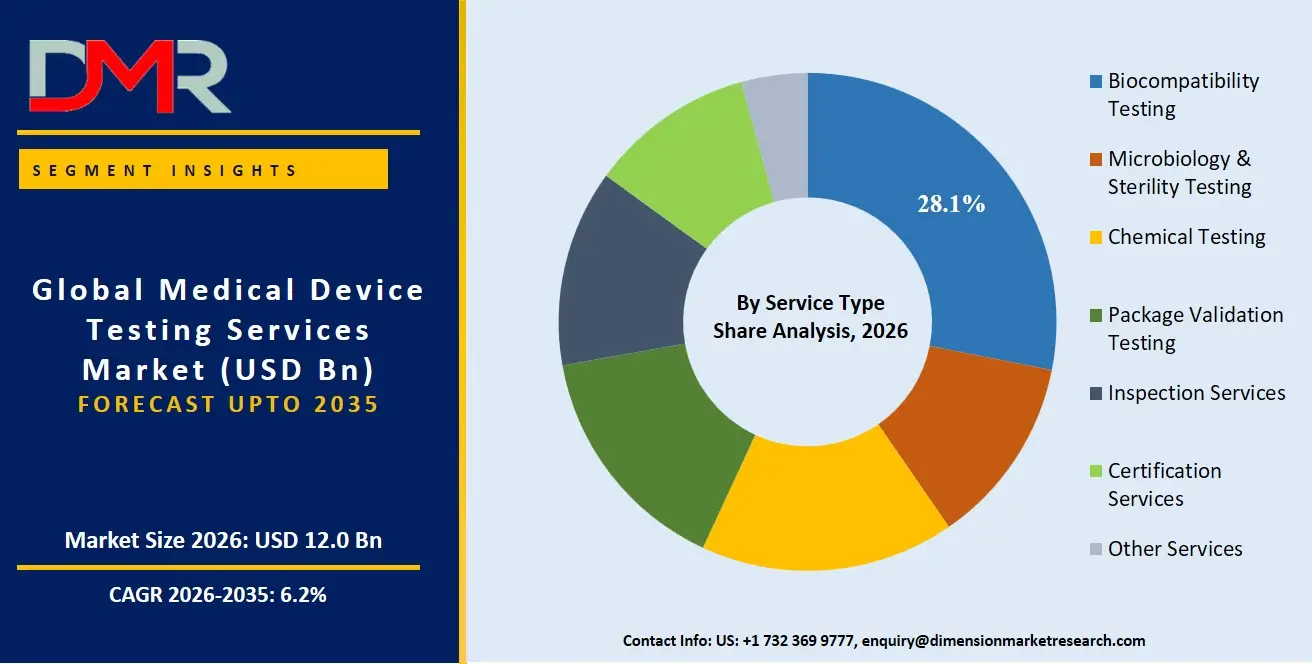

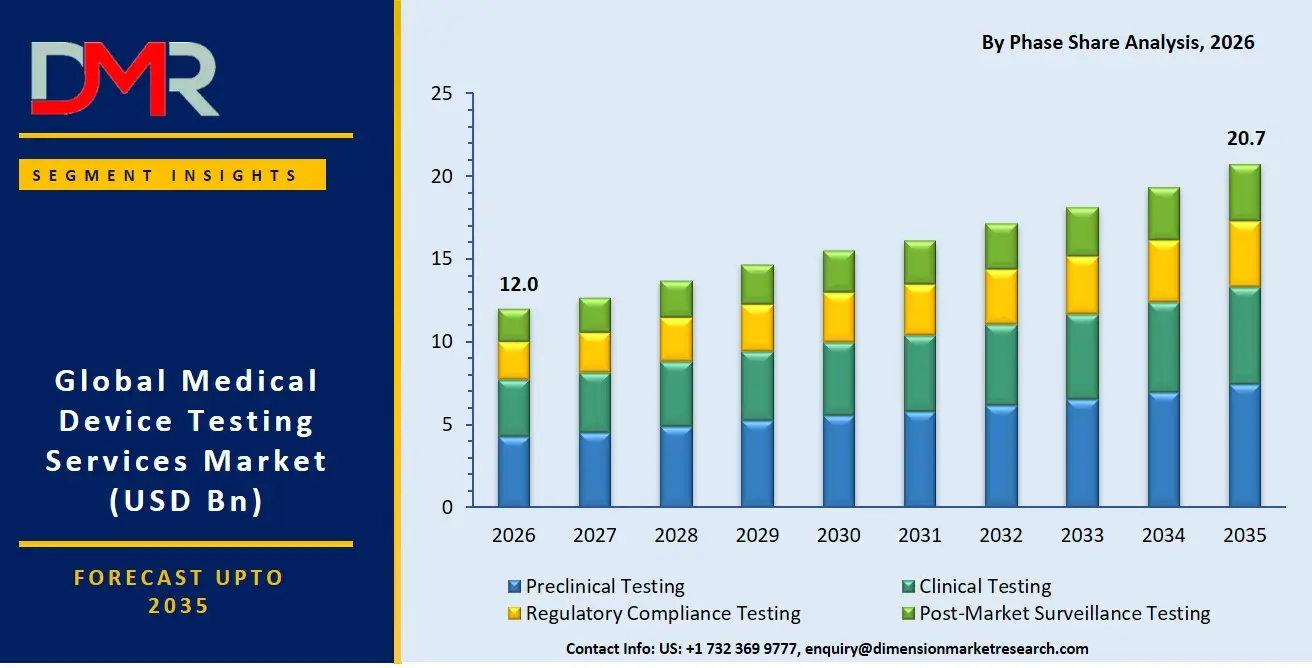

The Global Medical Device Testing Services Market is expected to reach a value of USD 12.0 billion in 2026, and it is further anticipated to reach USD 20.7 billion by 2035, growing at a CAGR of 6.2% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Medical device testing services market is witnessing considerable growth owing to the growing sophistication of medical technology as well as tightening regulations globally. Medical device testing services market includes vital service providers offering analysis and evaluation services ensuring the safety, efficacy, and quality of products from their concept until post-market phase. Biocompatibility, microbiological and sterility, chemical characterization, and package integrity testing services are included in the offerings of these companies. There is a rising need for combination products, wearable sensors, and software as a medical device (SaMD), requiring unique testing services other than the conventional ones. The main consumers of medical device testing services are the manufacturers of medical devices with ISO 10993 and ISO 13485 being the basic standards. The tough criteria set by EU Medical Device Regulation (MDR) act as an important factor for outsourced testing to CROs.

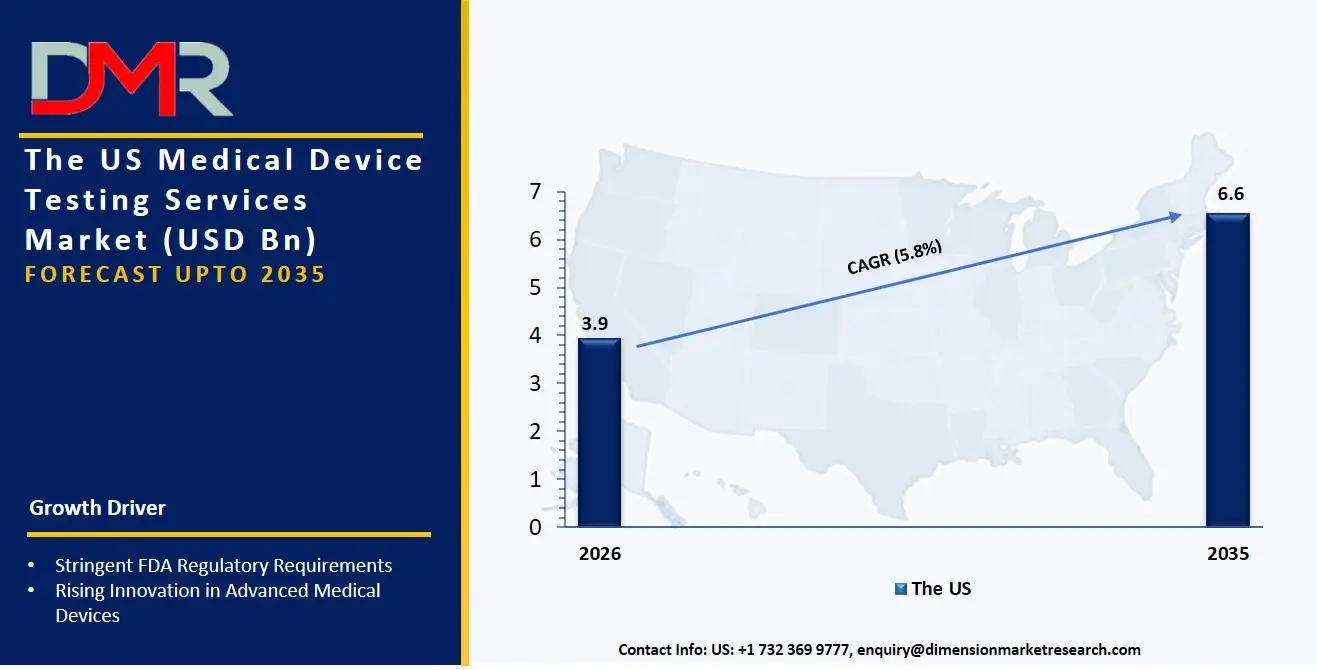

The US Medical Device Testing Services Market

The US Medical Device Testing Services Market is projected to reach USD 3.9 billion in 2026 at a compound annual growth rate of 5.8% over its forecast period, culminating in a value of USD 6.6 billion by 2035. The United States is still the biggest national market due to the PMA and 510(k) clearance pathways of premarket approval established by the FDA.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Demand for biocompatibility testing for implantable devices for cardiovascular diseases and orthopedics is very high due to the need for complete chemical characterization according to ISO 10993-18 standards, reducing patient risk. At the same time, the increased use of active medical devices with AI/ML algorithms leads to an increase in cybersecurity testing and evaluation services.

The Europe Medical Device Testing Services Market

The Europe Medical Device Testing Services Market is estimated to be valued at USD 3.5 billion in 2026 and is further anticipated to reach USD 5.9 billion by 2035 at a CAGR of 6.0%. The market in Europe is highly influenced by the complete adoption of EU MDR and In Vitro Diagnostic Regulation (IVDR), which require a considerably higher level of clinical testing as compared to their predecessors. There is an increasing demand for toxicology risk assessment and chemical characterization of existing products in light of the increased regulatory requirements. There is also an increase in the service of notified body certifications due to the rush of companies manufacturing surgical instruments and dental instruments from Germany and Switzerland to recertify their product line.

The Japan Medical Device Testing Services Market

The Japan Medical Device Testing Services Market is projected to be valued at USD 1.3 billion in 2026. It is further expected to witness robust growth, holding USD 2.2 billion in 2035 at a CAGR of 5.4%. The Japanese market is distinctive in terms of regulation, which consists of harmonizing activities undertaken by the Pharmaceuticals and Medical Devices Agency (PMDA) according to international standards, keeping in view some distinct local regulations regarding extractables and leachables testing. Biocompatibility testing and validation of in-vitro diagnostic devices account for a significant share of the cost of testing as companies in the domestic industry develop new products for neurology and respiration devices. There is a definite need for laboratories that understand the local regulatory environment to serve the purpose of a transition from traditional QA methods to performance evaluation of the novel drug-device combination.

Key Takeaways

- Market Size & Forecast: The Global Medical Device Testing Services market is projected to reach USD 12.0 billion in 2026, expanding to USD 20.7 billion by 2035, mainly due to stringent implementation of EU MDRs along with advancements in active implantable medical devices.

- Growth Rate & Outlook: The global market is expected to be driven by a CAGR of 6.2% owing to an acute shortage of in-house knowledge in toxicology and increasing complexity of testing combination products.

- Primary Growth Drivers: Main drivers include a transition from generic testing to unique chemical identification, regulatory outsourcing of testing services due to the growing complexity of FDA and MDR approval requirements, and the adoption of quality assurance and quality control practices that call for specialized inspection.

- Key Market Trends: Emerging trends in the Global Medical Device Testing Services market include an increased use of unique device standards (such as ISO 18562 for respiratory devices and ISO 7405 for dental devices), use of in-silico modelling techniques during preclinical testing to avoid animal trials, and increasing focus on post-market testing.

- By Testing Standard Analysis: ISO standards testing models are anticipated to lead in the global market due to their harmonized footprint worldwide. Testing services are increasingly demanded to create comprehensive biocompatibility evaluation plans which involve connecting individual materials' level testing (ISO 10993) to final product validation and verification at device level.

- By Device Type Analysis: The cardiovascular devices and orthopedic devices is poised to hold the largest share in this market owing to strict biocompatibility standards applicable for long-lasting implanted products. In vitro diagnostic (IVD) devices hold the fastest growing segment since highly advanced assay development needs method validation and clinical performance study.

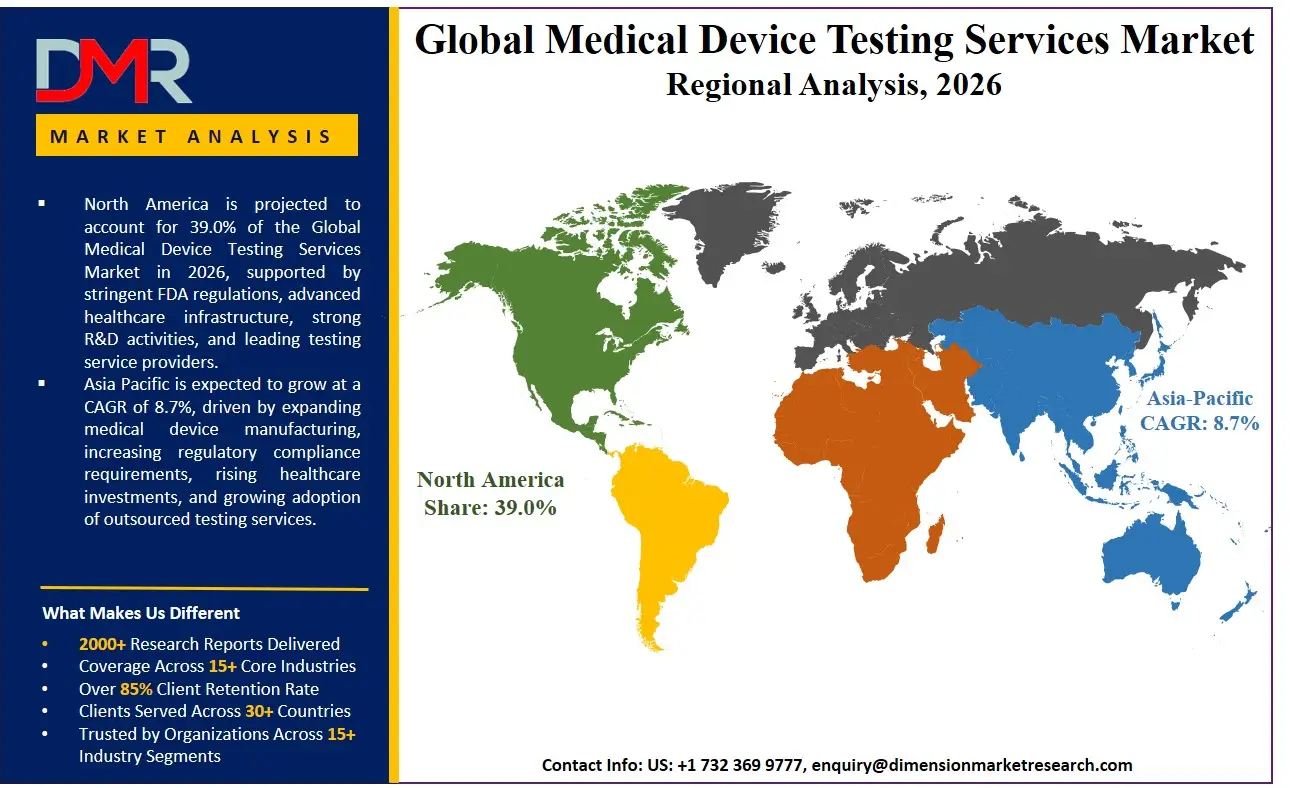

- Regional Leadership: North America is poised to hold the dominance in this market holding the largest share of 39.0% in 2026 due to the presence of a well-developed technological ecosystem in it that exploits this infrastructure to the mark and becomes the leader in this market.

What is the Medical Device Testing Services?

Medical Device Testing Services are the specific analytical and regulatory consulting services provided by external CROs, laboratories, and notified bodies to support companies during the full product lifecycle. Unlike the medical device design and manufacturing processes, medical device testing services are concerned with the validation of safety and effectiveness. It includes Biocompatibility Testing for the analysis of material-to-host-tissue reactions, Microbiology & Sterility Testing for the detection of microorganisms' presence, Chemical Testing for the determination of toxic substances and leachables, and Package Validation for the validation of sterile barriers. Since all innovative Class III implantable devices require comprehensive biological evaluation (100%), professional medical device testing services are required to meet regulatory requirements, reduce liability risks, and shorten the time-to-market for companies to gain a competitive edge, not regulatory hurdle.

Use Cases

- Cardiovascular Stent Biocompatibility: Medical device manufacturers hire outsourced testing services to perform hemocompatibility and chronic toxicity testing on drug-eluting stents, mapping endothelialization profiles required for FDA premarket approval submissions.

- Sterility Assurance for Orthopedic Implants: Orthopedic manufacturers use sterility testing and validation services to validate ethylene oxide (EtO) sterilization cycles for complex porous-coated knee implants, ensuring a sterility assurance level (SAL) of 10⁻⁶ without compromising material integrity.

- Chemical Characterization of Dermal Fillers: Aesthetic device companies use chemical testing and toxicological risk assessment consulting to isolate and quantify 1,4-butanediol diglycidyl ether (BDDE) residuals in hyaluronic acid-based dermal fillers to comply with EU MDR Annex I general safety requirements.

- Package Validation for Surgical Instruments: Contract manufacturers use package validation testing to conduct accelerated and real-time aging studies on sterile barrier systems for surgical instruments, correlating seal strength data to maintain shelf-life claims.

How AI is Transforming the Medical Device Testing Services Market?

The implementation of AI technology in testing medical devices is bringing about major changes by making the analysis and documentation processes much faster. In the case of preclinical testing, AI algorithms for image analysis can automatically scan histopathology slides from animal implants, thereby greatly reducing time spent on the manual process and removing any kind of quantitative pathology bias. The Quality Assurance & Quality Control process, on the other hand, uses AI algorithms to detect any abnormal peaks in extractables and leachables study chromatograms as well as predicting system suitability drifts and suggesting corrections that could prevent an entire batch from failing.

Regulatory intelligence and submission-related projects are becoming increasingly AI-oriented. Natural language processing agents in certification services are used to scan regulatory databases from all over the world, find predicate device decisions, compliance issues and updates to ensure the organization complies with the ISO 13485 framework and MDSAP. In addition, the use of generative AI assistants in risk assessment consulting helps simulate toxicological endpoints and draft biological evaluation plans.

Market Dynamics

Key Drivers in the Global Medical Device Testing Services Market

Stringent Regulatory Requirements

The growing intricacy of medical devices regulations globally is one of the primary factors that propel the medical device testing services market forward. There are many regulatory bodies including the FDA of the USA, European regulatory bodies under MDR, and others that ask for thorough testing in order to check whether the products will be safe, effective, and perform well. The manufacturers have to carry out biocompatibility testing, sterility testing, electrical safety testing, software testing, and risk assessment testing among others before the launch of their products in the market.

Rising Development of Advanced Medical Devices

Innovations in medical technology have become one of the key factors that stimulate the need for testing services across the globe. There has been an increasing use of implantable devices, wearable health monitoring technologies, robotic surgery equipment, connected health devices, and advanced diagnostic technologies. All these innovative products have raised the need for thorough testing of products. These devices need rigorous testing because of the complexities involved with them. This is due to the reason that manufacturers must assure the effectiveness of their devices through different operating conditions prior to their introduction in the market.

Restraints in the Global Medical Device Testing Services Market

High Cost of Comprehensive Testing Programs

The testing cost of medical devices is one of the challenges that manufacturers face today. Medical device testing usually requires various procedures such as biocompatibility tests, microbiology, chemicals, and clinical trials, which require an expensive laboratory setup and time. Small manufacturers cannot afford to conduct thorough testing procedures since they do not have enough funding. Furthermore, the need for repeat testing when there is a modification of design or regulatory standards can increase the cost of testing. The high cost of obtaining regulatory approval will slow down the process of development of the products.

Complex and Evolving Regulatory Landscape

The dynamic nature of the regulatory landscape constitutes one of the key constraints of the medical device testing services industry. There are varying testing standards, certification requirements, and approval procedures in different nations and geographic locations. Companies trying to penetrate international markets have to cope with various regulatory regimes at once. Regular changes in the regulations force testing companies and manufacturers to change their processes and approaches. Regulatory compliance issues become particularly hard to deal with in case of new technology developments that cannot be classified within any regulation categories yet.

Growth Opportunities in the Global Medical Device Testing Services Market

Expansion of Connected and Digital Health Devices

The fast-paced development of interconnected health technologies creates major chances for the medical device testing services market. Modern medical devices use wireless technologies, cloud technologies, artificial intelligence, and remote monitoring abilities. This needs certain tests for security, software validation, interoperability, and data integrity. Connected devices are being implemented by healthcare organizations to enhance the results of treatment and improve their efficiency, which increases the need for new tests. The expansion of digital health care systems all over the world creates opportunities for test providers to create new test solutions for novel technologies.

Increasing Outsourcing of Testing Activities

Medical devices manufacturers are increasingly looking towards external firms for testing activities, which presents lucrative prospects for market expansion. Outsourcing enables firms to take advantage of testing competencies, regulatory know-how, and accreditation of laboratories without any need for capital expenditure. External testing firms can usually conduct testing more effectively and economically than internal testing units. Increasing demand to expedite time to market for products adds more impetus to outsourcing trend. Moreover, new regulatory requirements are compelling medical devices manufacturers to engage testing firms having expertise in regulatory requirements.

Trends in the Global Medical Device Testing Services Market

Growing Demand for Cybersecurity Testing

Testing related to cybersecurity is becoming a prominent trend in the medical device testing services market. With more and more medical devices being connected and the use of digital health care applications becoming common, there is an increased need for ensuring data security and protecting systems from vulnerabilities. Regulatory bodies are coming up with stronger cybersecurity measures that would help safeguard patient data and make sure that the medical devices function properly. There is an increasing investment by manufacturers in penetration testing, vulnerability assessment, software validation, and risk management.

Rising Adoption of Automated and AI-Driven Testing Solutions

Automation and artificial intelligence are rapidly gaining momentum for use in the testing process of medical devices to enhance efficiency and accuracy. Modern testing frameworks are capable of analyzing large volumes of data, spotting anomalies, and improving the validation process compared to conventional approaches. Artificial intelligence solutions provide assistance in testing software, predicting risks, and ensuring quality control while eliminating the possibility of human mistakes. Automation also helps testing companies cope with increased workload and speed up project implementation timeframes. As complexity of medical devices continues to increase, together with regulatory requirements, use of intelligent testing solutions is likely to spread even further.

Research Scope and Analysis

The Global Medical Device Testing Services Market is segmented by service type into biocompatibility, microbiology and sterility, chemical, package validation, inspection, certification, and other testing services. It is further categorized by device type, testing phase, sourcing type, testing standards, application, and end user, including manufacturers, CROs, pharmaceutical companies, research institutes, and regulatory authorities.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Service Type Analysis

Biocompatibility testing is projected to dominate the service type segment because regulatory authorities require extensive evaluation of medical devices that come into direct or indirect contact with the human body. Manufacturers must demonstrate that materials used in devices do not cause toxicity, irritation, sensitization, or adverse biological reactions. The increasing use of implantable devices, cardiovascular products, orthopedic implants, and advanced surgical instruments has significantly increased demand for biocompatibility assessments. International standards such as ISO 10993 further reinforce testing requirements before commercialization. Since nearly all implantable and patient-contacting devices require comprehensive biocompatibility validation during product development and regulatory approval processes, this segment consistently accounts for the largest share of medical device testing service revenues globally.

By Device Type Analysis

In Vitro Diagnostic devices is poised to dominate the device type segment due to the large volume of diagnostic products entering the market and the stringent testing requirements associated with ensuring accuracy, reliability, and patient safety. Diagnostic assays, molecular testing kits, laboratory analyzers, and point-of-care testing solutions require extensive analytical validation before commercialization. Rising prevalence of chronic diseases, infectious diseases, and personalized medicine initiatives has accelerated demand for diagnostic testing products worldwide. Regulatory agencies impose rigorous performance evaluation requirements for IVD products to minimize diagnostic errors. Continuous innovation in diagnostics and growing healthcare demand have made IVD devices one of the largest categories requiring specialized testing services across global healthcare markets.

By Phase Analysis

Preclinical testing is expected to dominate the phase segment because every medical device must undergo extensive safety and performance evaluations before entering human clinical studies. This stage includes biocompatibility testing, microbiological assessments, chemical characterization, toxicology evaluations, and animal studies.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Regulatory authorities require comprehensive preclinical evidence to demonstrate that devices meet safety standards and are suitable for clinical investigation. Manufacturers invest heavily in preclinical testing to identify potential risks early and avoid costly failures during later development stages. Since all medical devices, particularly implantable and high-risk products, require substantial preclinical validation prior to regulatory submission, this phase accounts for the largest share of testing expenditures within the medical device testing services market.

By Sourcing Type Analysis

Outsourced testing is projected to dominate the sourcing type segment because medical device manufacturers increasingly rely on specialized third-party laboratories and testing organizations to meet complex regulatory requirements. Outsourcing provides access to advanced testing technologies, experienced scientific personnel, and globally recognized certifications without requiring significant internal investment. Specialized testing providers offer expertise across biocompatibility, microbiology, chemical analysis, cybersecurity, and regulatory compliance testing. Additionally, outsourcing helps manufacturers reduce operational costs, accelerate product development timelines, and ensure adherence to evolving international regulations. As regulatory standards become more stringent and device technologies become increasingly sophisticated, demand for external testing expertise continues to grow, strengthening the dominance of outsourced testing services.

By Testing Standard Analysis

FDA compliance testing is anticipated to dominates the testing standard segment because the United States represents one of the largest and most regulated medical device markets globally. Manufacturers seeking access to the U.S. market must satisfy stringent requirements established by the Food and Drug Administration. These requirements often involve extensive testing related to safety, effectiveness, performance, biocompatibility, software validation, and risk management. Since many global medical device companies prioritize U.S. commercialization due to its significant market potential, FDA compliance testing receives substantial investment. The complexity and comprehensive nature of FDA regulatory pathways contribute to higher testing demand, making FDA-related testing services the largest segment within the medical device testing standards landscape.

By Application Analysis

Regulatory approval is expected to dominate the application segment because testing activities are primarily conducted to obtain authorization for product commercialization. Medical devices must undergo extensive validation, verification, and compliance assessments to satisfy regulatory agencies across major markets. Manufacturers invest heavily in testing services to demonstrate product safety, efficacy, reliability, and quality before market entry. Regulatory frameworks such as FDA regulations, EU MDR requirements, and international ISO standards require comprehensive testing documentation. Without successful regulatory approval, products cannot be legally marketed or distributed. Consequently, testing conducted specifically to support regulatory submissions represents the largest application area, accounting for a substantial share of demand within the global medical device testing services market.

By End User Analysis

Medical device manufacturers are poised to dominate the end-user segment because they are directly responsible for ensuring product safety, quality, and regulatory compliance throughout the development lifecycle. These companies invest heavily in testing services during research, development, validation, certification, and post-market monitoring activities. Increasing innovation in implantable devices, diagnostics, digital health solutions, and connected medical technologies has expanded testing requirements significantly. Manufacturers must comply with stringent international regulations while maintaining product reliability and patient safety. Since testing services are a mandatory component of device development and commercialization, manufacturers account for the majority of testing expenditures. Their continuous product development activities make them the largest consumers of medical device testing services globally.

The Global Medical Device Testing Services Market Report is segmented on the basis of the following:

By Service Type

- Biocompatibility Testing

- Cardiovascular Device Biocompatibility Testing

- Orthopedic Device Biocompatibility Testing

- Dental Implant Device Biocompatibility Testing

- Dermal Filler Biocompatibility Testing

- General Surgery Implantation Device Biocompatibility Testing

- Neurosurgical Implantation Device Biocompatibility Testing

- Ophthalmic Implantation Device Biocompatibility Testing

- Others

- Microbiology & Sterility Testing

- Bioburden Determination

- Pyrogen & Endotoxin Testing

- Sterility Testing & Validation

- Antimicrobial Testing

- Chemical Testing

- Chemical Characterization (Extractables & Leachables)

- Analytical Method Development & Validation

- Toxicological Risk Assessment & Consulting

- Package Validation Testing

- Inspection Services

- Certification Services

- Other Services

By Device Type

- In Vitro Diagnostic (IVD) Devices

- Active Medical Devices

- Implantable Medical Devices

- Cardiovascular Devices

- Orthopedic Devices

- Diagnostic Imaging Devices

- Surgical Instruments

- Dental Devices

- Ophthalmic Devices

- Neurology Devices

- Respiratory Devices

- Drug Delivery Devices

By Phase

- Preclinical Testing

- Clinical Testing

- Regulatory Compliance Testing

- Post-Market Surveillance Testing

By Sourcing Type

- In-House Testing

- Outsourced Testing

By Testing Standard

- ISO Standards Testing

- IEC Standards Testing

- FDA Compliance Testing

- EU MDR Compliance Testing

- Other Regional Regulatory Compliance Testing

By Application

- Product Development

- Quality Assurance & Quality Control

- Regulatory Approval

- Risk Assessment

- Product Validation & Verification

By End User

- Medical Device Manufacturers

- Pharmaceutical & Biotechnology Companies

- Contract Research Organizations (CROs)

- Academic & Research Institutes

- Regulatory Authorities

Regional Analysis

Leading Region by Market Share

North America is poised to dominate the global medical device testing services market, as it is projected to hold 39.0% of the market share by the end of 2026. The United States, which dominates North America, has the highest share in the testing market because of the unmatched concentration of FDA-reviewed Class III device innovators and the aggressive regulatory submission agendas of the top-tier medical technology corporations. The area has an established ecosystem of global GLP-certified CROs, specialized boutique analytical chemistry consultancies, and a rich pool of talent in toxicological pathology and regulatory affairs scientists. Enterprise investment in artificial intelligence diagnostics, smart surgical robots, and the overall shift toward bioresorbable material science contributes to the continued demand for comprehensive preclinical biological safety testing and chemical characterization. Moreover, a robust venture capital climate persistently finances upcoming neurostimulation and vascular intervention device startups that need expert outsourced testing services to achieve rapid de novo classification and compliant market entry.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Regional Market

Asia-Pacific is expected to be the most rapidly expanding medical device testing services market, driven by the government-led sweeping harmonization initiatives with ISO and GHTF (Global Harmonization Task Force) standards in China, India, Japan, and South Korea. The fast-paced economic growth, the rise of domestic medical device manufacturing, and the dynamic expansion of local regulatory testing requirements are compelling multinationals and local champions to discard unreliable in-house test methods. Biocompatibility and chemical characterization testing is in high demand to help these large organizations steer the direction of complex novel combination product evaluation. There is also a severe lack of qualified GLP-compliant laboratory capacity in the region, and it is necessary to outsource to global and emerging local CROs for extractables and leachables studies, pyrogen testing, and accelerated aging to cover the internal skill gap and enable faster registration on local regulatory bodies like the National Medical Products Administration (NMPA) and the Central Drugs Standard Control Organization (CDSCO).

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive environment of global medical device testing services has become highly dynamic with a heterogeneous array of global full-service CROs, specialized analytical chemistry laboratories, and notified body testing divisions. The key to success will be the profound scientific credibility and regulatory partnerships with notified bodies like TÜV SÜD and BSI, because they will open the necessary co-submission pathways and early access to the new interpretation of EU MDR guidance documents. The movement towards market consolidation is rapidly progressing with the traditional laboratory outsourcing companies acquiring niche extractables and leachables and antimicrobial testing specialists to stay afloat. Proprietary intellectual property, including automated analytical method development protocols and in-silico toxicological prediction databases, is becoming a more important basis of competitive differentiation than just labor arbitrage or generic GLP compliance management.

Some of the prominent players in the Global Medical Device Testing Services Market are:

- Eurofins Scientific

- Charles River Laboratories

- SGS SA

- Intertek Group plc

- TÜV SÜD

- TÜV Rheinland

- UL Solutions

- NAMSA

- WuXi AppTec Medical Device Testing

- Element Materials Technology

- Nelson Laboratories

- Pace Analytical Services

- North American Science Associates (NAMSA)

- Laboratory Corporation of America Holdings (Labcorp)

- ICON plc

- IQVIA Laboratories

- Sterigenics International

- Medical Device Testing Services (MDTS)

- Kiwa NV

- BSI Group

- Other Key Players

Recent Developments

- February 2026: Charles River Laboratories announced a major expansion of its Medical Device Testing Innovation Center, a professional services initiative to assist clients in the Neuromodulation and Ophthalmic Implantation sectors to create highly sensitive chemical characterization profiles through high-resolution accurate mass spectrometry and GLP-compliant expertise in ISO 10993-18 toxicological risk assessment.

- December 2025: SGS SA strengthened its strategic alliance with a leading dental implant consortium and introduced a dedicated practice called Endotoxin & Pyrogen Testing and Th17-biased immunotoxicity profiling aimed at supporting Dental Device manufacturers in testing novel titanium-zirconium alloys for peri-implantitis endpoints and maintaining compliance with global dental material standards.

- October 2025: Eurofins Scientific purchased a specialized German medical device CRO to further its Biocompatibility Testing and certification services for absorbable cardiovascular stent manufacturers, to support the complicated requirements of degradation product mapping and local tissue tolerance testing required by European notified bodies.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 12.0 Bn |

| Forecast Value (2035) |

USD 20.7 Bn |

| CAGR (2026–2035) |

6.2% |

| The US Market Size (2026) |

USD 3.9 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Service Type, By Device Type, By Phase, By Sourcing Type, By Testing Standard, By Application, and By End User |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Medical Device Testing Services Market?

▾ The Global Medical Device Testing Services market is poised to be valued at USD 12.0 billion in 2026 and is projected to reach USD 20.7 billion by 2035, driven by the universal need for specialized evaluations in chemical characterization, biocompatibility, and microbiology for global regulatory submissions.

What is the CAGR of the Global Medical Device Testing Services Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 6.2% from 2026 to 2035, reflecting the accelerating complexity of novel biomaterials and the persistent shortage of internal toxicological risk assessment expertise.

What factors are driving the growth of the Global Medical Device Testing Services Market?

▾ Key drivers include the divergence in global regulatory standards, the imperative to generate clinical evidence for high-risk implantable devices, the management complexity of extractables and leachables chemical characterization, and the surge in demand for EU MDR-specific certification and re-certification services.

Which region held the largest share of the Medical Device Testing Services Market in 2026?

▾ North America, specifically the United States, is expected to hold 39.0% of the market share in 2026, driven by a mature FDA-regulatory ecosystem and aggressive medical technology enterprise investment in biocompatibility testing and AI-driven diagnostic device validation.

Which region is expected to grow the fastest in the Medical Device Testing Services Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid regulatory modernization in China, India, and Japan, where Preclinical Testing and Chemical Characterization are critical for transitioning local manufacturers to meet global ISO and MDR standards.

What are the major trends in the Global Medical Device Testing Services Market?

▾ Major trends include the integration of in-silico toxicology into biological evaluation plans, the rise of green chemistry and sustainability in material selection, the demand for device-type-specific standards compliance, and the focus on in vitro alternative methods within biocompatibility testing.

Who are the key players in the Global Medical Device Testing Services Market?

▾ Key players include global CROs like Charles River Laboratories, Eurofins Scientific, and SGS, as well as the testing divisions of notified bodies like TÜV SÜD, alongside specialized pure-play analytical chemistry laboratories and biocompatibility consultancies like NAMSA and Nelson Labs.

How is the Global Medical Device Testing Services Market segmented?

▾ The market is segmented by Service Type, Device Type, Phase, Sourcing Type, Testing Standard, Application, and End User.