Market Overview

The Global Nuclear Imaging Market is forecasted to attain a value of USD 3,173.2 million by 2025 and is anticipated to expand at a CAGR of 5.6% from 2025 to 2034, ultimately reaching USD 5,186.1 million.

This growth trajectory reflects the increasing adoption of positron emission tomography (PET), single-photon emission computed tomography (SPECT), and hybrid imaging systems across healthcare facilities for oncology, cardiology, neurology, and precision diagnostics. Rising demand for early disease detection, advancements in radiopharmaceuticals, integration of AI in imaging, and expanding applications in personalized medicine are key factors driving market expansion during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The global nuclear imaging market is evolving rapidly as clinical demand, technological progress, and molecular science converge to create more precise diagnostic pathways. Hybrid imaging modalities like PET/CT and SPECT/CT have become indispensable because they simultaneously capture anatomical structure and physiological activity, enabling clinicians to pinpoint disease location, stage progression, and monitor treatment response with unmatched accuracy.

The growing use of specialized radiotracers such as gallium-68 for prostate cancer, fluorine-18 for neurological mapping, and technetium-99m for cardiac evaluation is widening the scope of applications beyond oncology into cardiology, neurology, endocrinology, and infectious disease imaging. Artificial intelligence is further revolutionizing this space by automating image reconstruction, reducing noise, improving lesion detection sensitivity, and integrating multimodal datasets for faster, more confident diagnoses.

The rise of theranostics, where targeted radiopharmaceuticals are used for both imaging and treatment, is shifting the paradigm from diagnosis-only approaches to integrated care models. However, challenges persist. Radioisotope shortages, particularly molybdenum-99 supply disruptions, remain a global concern, while regulatory compliance for radiopharmaceuticals can slow adoption timelines.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

High acquisition and operational costs for advanced scanners can limit accessibility in lower-resource regions. Nonetheless, emerging economies are investing heavily in nuclear medicine infrastructure, and portable PET/SPECT devices are beginning to extend access to community and rural hospitals. With global health systems prioritizing early disease detection, personalized medicine, and noninvasive functional diagnostics, nuclear imaging is positioned to be a core technology in the future of precision healthcare.

The US Nuclear Imaging Market

The US Nuclear Imaging Market is projected to reach USD 1,024.8 million in 2025 at a compound annual growth rate of 5.3% over its forecast period.

The United States nuclear imaging sector is anchored by a strong demographic driver: a growing aging population and a rising prevalence of chronic diseases that require early and precise diagnosis. A significant portion of diagnostic imaging capacity in the U.S. is dedicated to PET and SPECT applications in cancer detection, cardiac perfusion analysis, and neurological assessment.

This is supported by a large and specialized workforce of nuclear medicine technologists, physicists, and radiopharmacists. National institutions promote best practices and safety protocols, ensuring high-quality imaging while maintaining strict radiation safety standards. The U.S. leads in the integration of AI into nuclear imaging workflows, with algorithms capable of enhancing image clarity, automating quantitative analysis, and aiding in the interpretation of complex multi-parametric datasets.

Academic medical centers, research hospitals, and federal agencies are collaborating to advance the development of novel tracers and hybrid imaging techniques that combine PET/SPECT with MRI or ultrasound for more comprehensive assessments. The nation’s extensive network of cyclotron facilities ensures a reliable isotope supply for both clinical and research applications. While reimbursement policies and regulatory reviews can slow the clinical adoption of new technologies, the country’s combination of advanced infrastructure, skilled professionals, and ongoing research investment ensures it remains a leader in nuclear imaging innovation.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Europe Nuclear Imaging Market

The Europe Nuclear Imaging Market is estimated to be valued at USD 465.9 million in 2025 and is further anticipated to reach USD 737.8 million by 2034 at a CAGR of 5.0%.

Europe’s nuclear imaging landscape is defined by its highly collaborative research networks, harmonized regulations, and robust public healthcare infrastructure. The continent benefits from strong professional organizations that coordinate education, set practice guidelines, and facilitate technology adoption across member states. The integration of hybrid PET/CT and SPECT/CT systems is well established, with a growing shift toward PET/MRI for certain neurological and pediatric applications due to reduced radiation exposure.

European research programs are at the forefront of developing next-generation radiopharmaceuticals, including tracers for immunotherapy response monitoring and targeted neuroinflammation imaging. Cross-border initiatives ensure a steady supply of isotopes through coordinated production facilities and logistics frameworks.

Europe’s focus on personalized medicine aligns with the rapid adoption of theranostic protocols, particularly in oncology, where patients benefit from targeted imaging followed by receptor-specific radioligand therapy. The continent also leverages funding from pan-European projects to explore AI-enhanced imaging interpretation and automated reporting systems, helping to address radiologist shortages in certain regions. Regulatory bodies work closely with clinical institutions to fast-track the safe implementation of novel tracers and technologies while maintaining stringent radiation safety standards.

The Japan Nuclear Imaging Market

The Japan Nuclear Imaging Market is projected to be valued at USD 190.3 million in 2025. It is further expected to witness subsequent growth in the upcoming period, holding USD 310.8 million in 2034 at a CAGR of 5.6%.

Japan’s nuclear imaging sector is uniquely shaped by its demographic profile, with nearly one-third of its population aged 65 or older, creating sustained demand for early detection and monitoring of chronic diseases. The country has one of the highest per-capita deployments of PET scanners in the world, enabling widespread access to advanced diagnostic services. Nuclear imaging is a cornerstone of Japan’s cancer screening programs, particularly for gastric, lung, and prostate cancers, where precision in staging and therapy planning is critical. In neurology, PET and SPECT are routinely used for the evaluation of dementia, epilepsy, and movement disorders, often integrated into comprehensive cognitive health initiatives.

Japan is also advancing cyclotron-based isotope production, reducing dependency on imported supplies and ensuring stable availability for clinical use. Government-backed healthcare modernization programs promote the integration of AI into imaging workflows, improving lesion detection accuracy, streamlining image processing, and enhancing efficiency in high-volume hospitals. Regulatory authorities in Japan actively collaborate with academic and industry partners to accelerate the clinical adoption of novel tracers and theranostic approaches. Combined with its strong infrastructure and a culture of rapid technology uptake, Japan remains a model for the integration of advanced nuclear imaging into routine clinical practice.

Global Nuclear Imaging Market: Key Takeaways

- Global Market Size Insights: The Global Nuclear Imaging Market size is estimated to have a value of USD 3,173.2 million in 2025 and is expected to reach USD 5,186.1 million by the end of 2034.

- The Global Market Growth Rate: The market is growing at a CAGR of 5.6 percent over the forecasted period of 2025.

- The US Market Size Insights: The US Nuclear Imaging Market is projected to be valued at USD 1,024.8 million in 2025. It is expected to witness subsequent growth in the upcoming period as it holds USD 1,625.8 million in 2034 at a CAGR of 5.3%.

- Regional Insights: North America is expected to have the largest market share in the Global Nuclear Imaging Market with a share of about 38.4% in 2025.

- Key Players: Some of the major key players in the Global Nuclear Imaging Market are Siemens Healthineers, GE HealthCare, Koninklijke Philips N.V., Canon Medical Systems Corporation, Bracco Imaging S.p.A., Cardinal Health, Inc., Curium Pharma, and many others.

Global Nuclear Imaging Market: Use Cases

- Oncology Diagnostics: PET/CT enables visualization of tumor metabolism through radiotracer uptake mapping, allowing oncologists to detect malignancies at the molecular level before anatomical changes appear. This improves staging accuracy, guides biopsy targeting, and facilitates real-time monitoring of treatment response, enabling more adaptive cancer management strategies.

- Cardiac Assessment: Myocardial perfusion imaging via SPECT evaluates coronary blood flow during stress and rest, identifying ischemic regions and quantifying left ventricular function. This information informs revascularization decisions, assesses post-intervention recovery, and supports risk stratification for future cardiac events, contributing to better long-term patient outcomes.

- Neurological Disorders: Nuclear imaging using PET with amyloid, tau, or dopamine transporter tracers offers early insight into Alzheimer’s, Parkinson’s, and other neurodegenerative diseases. These scans allow for preclinical detection, differentiation between similar symptoms, and monitoring of disease progression, helping clinicians tailor patient care before irreversible damage occurs.

- Theranostic Applications: Radiopharmaceuticals such as ^177Lu-DOTATATE or ^177Lu-PSMA provide a dual function: first, enabling imaging to confirm tumor receptor presence, then delivering targeted radiation therapy directly to malignant cells. This integration enhances treatment efficacy while minimizing off-target damage, embodying the principles of precision oncology.

- Drug Development Imaging: PET and SPECT imaging in pharmaceutical research enable the visualization of drug biodistribution, receptor binding, and metabolic pathways in vivo. By providing quantifiable, noninvasive pharmacokinetic and pharmacodynamic data, nuclear imaging accelerates drug development timelines and improves the selection of candidate therapies for clinical trials.

Global Nuclear Imaging Market: Stats & Facts

International Atomic Energy Agency (IAEA)

- Technetium-99m (Tc-99m) is used in approximately 85% of diagnostic nuclear medicine procedures worldwide.

- The IAEA estimates that interruptions in molybdenum-99 (Mo-99) supply can affect the availability of Tc-99m because Mo-99 is the parent isotope used to generate Tc-99m.

- The IAEA notes that variations in global isotope production and logistics make a stable, recurring supply of short-lived isotopes (like Tc-99m) a persistent operational concern for nuclear medicine services.

IAEA / IMAGINE (IAEA Medical Imaging & Nuclear Medicine Global Resources Database) (reported in peer-reviewed articles summarizing IMAGINE)

- >140 countries have availability of SPECT or SPECT/CT systems.

- Roughly 27,000 SPECT or SPECT/CT systems are reported installed worldwide.

- 109 countries have PET/CT capability, with >5,200 PET/CT systems installed globally.

World Health Organization (WHO) / Global Health Observatory (GHO)

- WHO’s GHO tracks the density of diagnostic imaging equipment per 1,000,000 population (including PET units), providing standardized country-level metrics used for access planning and benchmarking.

- WHO data (as compiled in public datasets) are the basis for per-country indicators such as “PET units per million population,” which show very wide inter-country variation in scanner availability.

Society of Nuclear Medicine & Molecular Imaging (SNMMI) / professional body statistics

- SNMMI states that more than 20 million Americans benefit each year from nuclear medicine procedures.

- SNMMI communications and newsletters have reported that tens of millions (SNMMI has cited figures such as “over 40 million” in broader summaries) of nuclear medicine procedures are performed annually worldwide, underscoring very high procedure volumes in clinical practice.

U.S. National Academies / U.S. technical reviews on Mo-99/Tc-99m

- The United States historically performs about 50% of all Tc-99m procedures carried out worldwide (i.e., the U.S. is the single largest consumer of Tc-99m-based procedures).

- U.S. usage of Tc-99m has been described as on the order of ~40,000–50,000 Tc-99m procedures per day (as an operational benchmark used in national production planning).

U.S. Bureau of Labor Statistics (BLS) / OES / Occupational data

- May 2023 OES national estimate: Employment for Nuclear Medicine Technologists ≈ 16,560 (national estimate from OES).

- Mean annual wage for Nuclear Medicine Technologists (May 2023 OES) ≈ $95,080.

- BLS/Occupational Outlook: Employment of nuclear medicine technologists is projected to decline by ~1% from 2023 to 2033, yet there are about 800 openings per year (mostly replacement openings).

O*NET / U.S. Department of Labor summary data

- O*NET (drawing on U.S. labor statistics) reports employment ≈of 17,800 (as a close occupational estimate) and confirms the projected 1% growth and ~800 annual openings metric.

PubMed / NCBI / Peer-reviewed public research summaries

- Analyses using IAEA/IMAGINE data indicate that at least 96 countries would need to upscale PET-CT services under modeled needs; the same modeling suggested that>200 additional PET-CT scanners would be required to meet modeled demand gaps.

- Peer-reviewed reviews of the COVID period reported conventional nuclear medicine procedural volumes fell dramatically early in the pandemic (example ranges: overall reductions by ~54% in April 2020; conventional nuclear medicine reductions much higher in some months).

Eurostat (European Commission statistics)

- In 2022, Denmark reported 0.88 PET scanners per 100,000 inhabitants, while most other EU countries for which data are available reported at most 0.49 PET scanners per 100,000, highlighting intra-EU variability in PET availability.

Canadian Medical Imaging Inventory (national survey, Canada)

- National survey identified 60 PET-CT units across 9 provinces (Canada, 2022–2023 inventory).

- That inventory corresponds to ~1.5 PET-CT units per million population in Canada (2022–2023 data).

World Nuclear Association (technical information on radioisotope usage)

- In developed countries, about 1 in 50 people (≈2% of the population) use diagnostic nuclear medicine each year (reported as an estimate of population penetration in developed markets).

- Over 10,000 hospitals worldwide use radioisotopes in medicine (public technical summaries report hospital adoption in thousands worldwide).

IAEA / technical reference on isotope half-lives and logistics

- Tc-99m half-life ≈ 6 hours; Mo-99 half-life ≈ 66 hours. These short half-lives mean isotope supply is time-sensitive and distribution/logistics-dependent.

National statistics (Japan Statistics Bureau)

- Japan population data (official census release): 36,227,000 people aged 65 and over, which was 29.1% of Japan’s total population as of October 1, 2023 an important demographic driver for imaging demand.

Radiology & Nuclear Medicine Clinical Observations (public journals/reviews)

- Modeling and published service reviews indicate substantial gaps in PET-CT provision globally, with many low- and middle-income countries having far fewer scanners per million than recommended benchmarks (quantified in modeling studies that used IAEA data).

Radiation protection / clinical dose observations (public studies)

- Multi-center studies summarizing nuclear cardiology practice noted that a minority of studies achieve very low effective doses (for example, only a small percentage of PET/SPECT studies fall below specific low mSv thresholds), highlighting dose-optimization opportunities in practice.

Global Nuclear Imaging Market: Market Dynamic

Driving Factors in the Global Nuclear Imaging Market

Rising Burden of Chronic and Age-Related Diseases

The increasing global prevalence of chronic diseases, particularly cancer, cardiovascular disorders, and neurodegenerative conditions, is a major driver of the nuclear imaging market growth. The World Health Organization notes that non-communicable diseases are responsible for over 70% of deaths globally, with cancer alone accounting for nearly one in six deaths.

As life expectancy rises, especially in high-income and emerging economies, the incidence of age-related conditions requiring advanced imaging for diagnosis, staging, and treatment monitoring continues to grow. Nuclear imaging offers a unique advantage over other modalities by enabling functional and molecular-level insights before structural abnormalities appear, thereby supporting earlier and more effective interventions. In oncology, PET/CT can detect tumor activity at the cellular level, improving survival outcomes through timely therapy initiation.

Advancements in Radiopharmaceutical Development

The continual development of novel radiopharmaceuticals is significantly expanding the capabilities and clinical utility of nuclear imaging. New PET tracers, such as ^18F-fluciclovine for recurrent prostate cancer and ^18F-florbetapir for Alzheimer’s diagnosis, have broadened the range of detectable conditions. Similarly, novel SPECT agents like 99mTc-tetrofosmin are improving the evaluation of cardiac perfusion.

Radiochemistry innovations are enabling more specific targeting of disease biomarkers, improving diagnostic accuracy while minimizing radiation exposure to non-target tissues. The growth of cyclotron networks and automated synthesis units has improved the availability and scalability of short-lived isotopes, even in smaller markets. These advancements are also crucial for the success of theranostics, where a diagnostic isotope can be swapped for a therapeutic one using the same molecular ligand. As regulatory bodies streamline approval pathways for radiopharmaceuticals, adoption is accelerating in both developed and emerging regions.

Restraints in the Global Nuclear Imaging Market

High Capital and Operational Costs

One of the most significant restraints on the nuclear imaging market is the high capital and operational cost of equipment and infrastructure. PET/CT and SPECT/CT systems require multimillion-dollar investments, and operational expenses are compounded by the need for specialized facilities, such as shielded rooms and isotope handling units.

Furthermore, the short half-life of many isotopes, particularly those used in PET, necessitates proximity to cyclotron facilities or frequent isotope deliveries, increasing logistical costs. In regions with low patient volumes, achieving cost-effectiveness becomes difficult, leading to underutilization of installed systems. Even in developed markets, healthcare providers often face challenges securing reimbursement rates that adequately cover the costs of advanced nuclear imaging procedures.

Isotope Supply Chain Vulnerabilities

The nuclear imaging field is heavily dependent on a reliable supply of medical isotopes such as molybdenum-99, which decays into technetium-99m for SPECT imaging, and fluorine-18 for PET imaging. Production of these isotopes is concentrated in a small number of reactors and cyclotrons worldwide, creating vulnerability to supply disruptions from maintenance shutdowns, political instability, or transportation challenges.

Shortages can force healthcare providers to delay or cancel diagnostic procedures, directly impacting patient care. The time-sensitive nature of isotope transport due to short half-lives further complicates logistics. While efforts are underway to diversify production through non-reactor-based methods and regional cyclotron networks, these initiatives require significant investment and time to implement.

Opportunities in the Global Nuclear Imaging Market

Expansion into Emerging Markets and Rural Healthcare Systems

A major growth opportunity for nuclear imaging lies in expanding access to underserved regions, including emerging economies and rural healthcare systems in developed countries. Many low- and middle-income nations currently lack sufficient PET/CT or SPECT capacity, creating an opportunity for mobile imaging units, modular clinics, and public–private partnerships to bridge the diagnostic gap.

Portable gamma cameras and compact cyclotrons are enabling isotope production closer to point-of-care locations, reducing dependence on long-distance transport of short-lived isotopes. Governments in Asia-Pacific, Latin America, and Africa are increasingly investing in nuclear medicine infrastructure as part of broader healthcare modernization programs. Training initiatives supported by organizations like the IAEA are also helping to develop skilled nuclear medicine professionals in these regions.

Integration with Multi-Omics and AI-Driven Precision Healthcare

Another significant growth opportunity arises from integrating nuclear imaging with multi-omics data (genomics, proteomics, metabolomics) and AI-driven analytics to create comprehensive precision healthcare platforms. Molecular imaging already provides functional and metabolic insights; when combined with genomic and proteomic profiling, it can create highly personalized disease risk models and treatment plans.

AI can further synthesize these diverse datasets, revealing patterns and biomarkers that would be impossible to detect through traditional analysis alone. For example, combining PET imaging of tumor metabolism with genomic mutation profiles could predict therapy response more accurately, leading to individualized treatment protocols. Pharmaceutical companies are particularly interested in such integration for drug development, as it enables better patient stratification and more efficient clinical trial designs.

Trends in the Global Nuclear Imaging Market

Integration of AI and Hybrid Imaging Modalities

One of the most transformative trends in nuclear imaging is the growing integration of artificial intelligence (AI) with hybrid imaging modalities like PET/CT, SPECT/CT, and PET/MRI. AI algorithms enhance image reconstruction, reduce noise, and automate lesion detection, allowing for faster and more accurate interpretation. In oncology, for example, AI-assisted PET analysis can quantify tumor metabolic activity with high precision, aiding in treatment planning and monitoring.

Similarly, in cardiology, machine learning can predict perfusion deficits and risk profiles by analyzing large datasets of myocardial perfusion scans. PET/MRI, although less common, is gaining ground in neurology and pediatrics due to lower radiation exposure and high soft-tissue contrast. These technological integrations not only improve diagnostic outcomes but also streamline workflows, reduce interpretation times, and enable quantitative imaging for clinical research. This trend aligns with broader healthcare objectives of personalized medicine, as AI-enabled imaging facilitates more tailored therapeutic interventions.

Expansion of Theranostics in Precision Medicine

Theranostics, combining diagnostic imaging and targeted therapy within a single radiopharmaceutical platform, is rapidly becoming a defining trend in nuclear imaging. By using a single molecular targeting agent labeled with different isotopes, clinicians can both visualize disease sites and deliver precise radiotherapy to affected tissues. This approach has seen significant success in treating neuroendocrine tumors with ^177Lu-DOTATATE and metastatic prostate cancer with ^177Lu-PSMA-617.

Beyond oncology, theranostic research is extending into cardiology, infectious diseases, and neurodegenerative disorders. The growth of theranostics is fueled by advancements in radiochemistry, improved cyclotron and generator production of therapeutic isotopes, and expanding clinical evidence of improved patient survival rates with fewer systemic side effects. It also supports the personalized medicine model by enabling physicians to determine treatment eligibility based on imaging results, thereby minimizing unnecessary interventions.

Global Nuclear Imaging Market: Research Scope and Analysis

By Product Analysis

Imaging systems are projected to dominate the global nuclear imaging market due to their essential role in providing high-resolution, functional, and anatomical images for disease diagnosis and treatment monitoring. These systems, including SPECT and PET scanners, are integral in detecting early-stage diseases such as cancer, neurological disorders, and cardiovascular conditions.

Hospitals and diagnostic centers prioritize investing in advanced imaging systems because of their versatility in handling multiple applications and the growing demand for non-invasive diagnostic procedures. Technological innovations, such as hybrid PET/CT and PET/MRI systems, have further increased adoption by enabling simultaneous metabolic and structural imaging, thereby improving diagnostic accuracy. The aging global population and the rising prevalence of chronic diseases drive the need for precision diagnostics, which these systems deliver effectively.

Imaging systems also benefit from supportive government healthcare infrastructure funding and favorable reimbursement policies in many countries, facilitating procurement by both public and private healthcare providers. Additionally, their integration with artificial intelligence (AI) and image processing software enhances operational efficiency, workflow management, and reporting accuracy.

These advancements encourage medical professionals to shift towards newer imaging technologies that provide faster and more precise results. In research settings, imaging systems are critical tools in pharmaceutical development, enabling the tracking of drug effects on targeted organs or tissues in real-time. Their adaptability across multiple medical specialties, combined with improved affordability and longer equipment lifespans, ensures their continued dominance in the market. Overall, the versatility, diagnostic value, and technological evolution of imaging systems make them the preferred choice across the nuclear imaging landscape.

By Application Analysis

Oncology is expected to dominate the global nuclear imaging market application segment due to the rising global cancer burden and the critical role of advanced imaging modalities in early detection, staging, and monitoring treatment responses. According to the World Health Organization (WHO), cancer remains a leading cause of death globally, with approximately 20 million new cases expected annually by 2030, driving the demand for precision diagnostic solutions.

Nuclear imaging technologies such as PET, SPECT, and hybrid PET/CT systems are pivotal in detecting tumors at their earliest stages and differentiating between benign and malignant growths. Oncology applications benefit from innovations in radiopharmaceutical development, including targeted tracers for specific cancer types, which enhance image clarity and diagnostic accuracy. The growing adoption of personalized medicine further boosts oncology imaging demand, as these technologies are integral in determining individualized treatment plans, monitoring therapy progress, and detecting recurrence.

Additionally, government cancer-screening programs and rising investments in oncology research encourage the integration of nuclear imaging into clinical practice. With cancer prevalence increasing in both developed and developing economies, oncology remains the largest and fastest-growing application segment, supported by strong clinical evidence, expanding reimbursement coverage, and continuous technological advancements that improve image resolution, reduce scan times, and enable multimodal imaging for comprehensive cancer assessment.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By End User Analysis

Hospitals are poised to dominate the global nuclear imaging market end-user segment due to their extensive infrastructure, advanced diagnostic capabilities, and comprehensive patient care services. Hospitals are equipped with state-of-the-art imaging departments, enabling them to house PET/CT, SPECT, and hybrid imaging systems essential for nuclear medicine. Their ability to integrate imaging with other specialties such as oncology, cardiology, and neurology positions them as the primary providers of nuclear imaging services.

Additionally, hospitals benefit from skilled nuclear medicine physicians, radiologists, and technologists, ensuring high-quality imaging and accurate interpretations. Many hospitals, particularly in developed countries, participate in research programs and clinical trials that advance nuclear imaging technologies and radiopharmaceutical applications. Government healthcare initiatives and funding often prioritize hospital-based imaging facilities, further reinforcing their dominance. Hospitals also have the advantage of higher patient throughput, supporting the economic feasibility of expensive nuclear imaging equipment.

Furthermore, they maintain strong collaborations with radiopharmaceutical suppliers, ensuring the timely availability of isotopes necessary for scans. As patient preference shifts toward integrated diagnostic and treatment centers, hospitals remain the go-to choice for nuclear imaging procedures. Their capability to handle complex cases, emergency diagnostics, and multidisciplinary care continues to make them the leading end user in the global nuclear imaging market, with a role that is expected to strengthen further as imaging technologies evolve and hospital networks expand globally.

The Global Nuclear Imaging Market Report is segmented on the basis of the following:

By Product

- Imaging Systems

- SPECT Imaging Systems

- Hybrid SPECT Imaging Systems

- Standalone SPECT Imaging Systems

- PET Imaging Systems

- Planar Scintigraphy Imaging Systems

- Equipment

- PET/CT Scanners

- SPECT/CT Scanners

- PET/MRI Scanners

- Radioisotopes

- SPECT Radioisotopes

- Technetium-99m (Tc-99m)

- Thallium-201 (Tl-201)

- Gallium-67 (Ga-67)

- Iodine-123 (I-123)

- Other SPECT Isotopes

- PET Radioisotopes

- Fluorine-18 (F-18)

- Rubidium-82 (Rb-82)

- Other PET Isotopes

By Application

- Cardiology

- Neurology

- Thyroid

- Oncology

- Other Applications

By End User

- Hospitals

- Diagnostic Imaging Centres / Imaging Centers

- Academic & Research Institutes / R&D

- Other End User

Impact of Artificial Intelligence in the Global Nuclear Imaging Market

- Enhanced Image Reconstruction and Quality: AI-powered algorithms significantly improve image reconstruction speed and clarity in nuclear imaging modalities such as PET, SPECT, and PET/CT. By reducing noise and enhancing resolution, AI allows for more accurate lesion detection and characterization, even with lower doses of radiopharmaceuticals.

- Advanced Quantitative Analysis and Diagnostics: AI systems can process complex nuclear imaging data to provide automated, quantitative measurements, such as tumor metabolic activity or myocardial perfusion levels. These tools support clinicians in making objective, data-driven diagnoses and tracking disease progression or treatment response over time.

- Workflow Automation and Operational Efficiency: AI streamlines the nuclear imaging workflow by automating time-consuming tasks such as image segmentation, lesion detection, and report generation. This reduces the workload for radiologists and technologists, allowing them to focus more on complex cases and patient interaction.

- Predictive Analytics and Clinical Decision Support: AI integrates imaging data with electronic health records (EHRs), genetic profiles, and laboratory results to generate predictive insights about disease progression and patient outcomes. In nuclear cardiology, AI models can predict future cardiac events based on imaging biomarkers, while in oncology, they can estimate treatment response likelihood.

- Accelerated Drug Development and Radiopharmaceutical Research: AI assists pharmaceutical companies and research institutions in developing novel radiopharmaceuticals by simulating molecular interactions, predicting tracer behavior, and analyzing trial imaging data more efficiently.

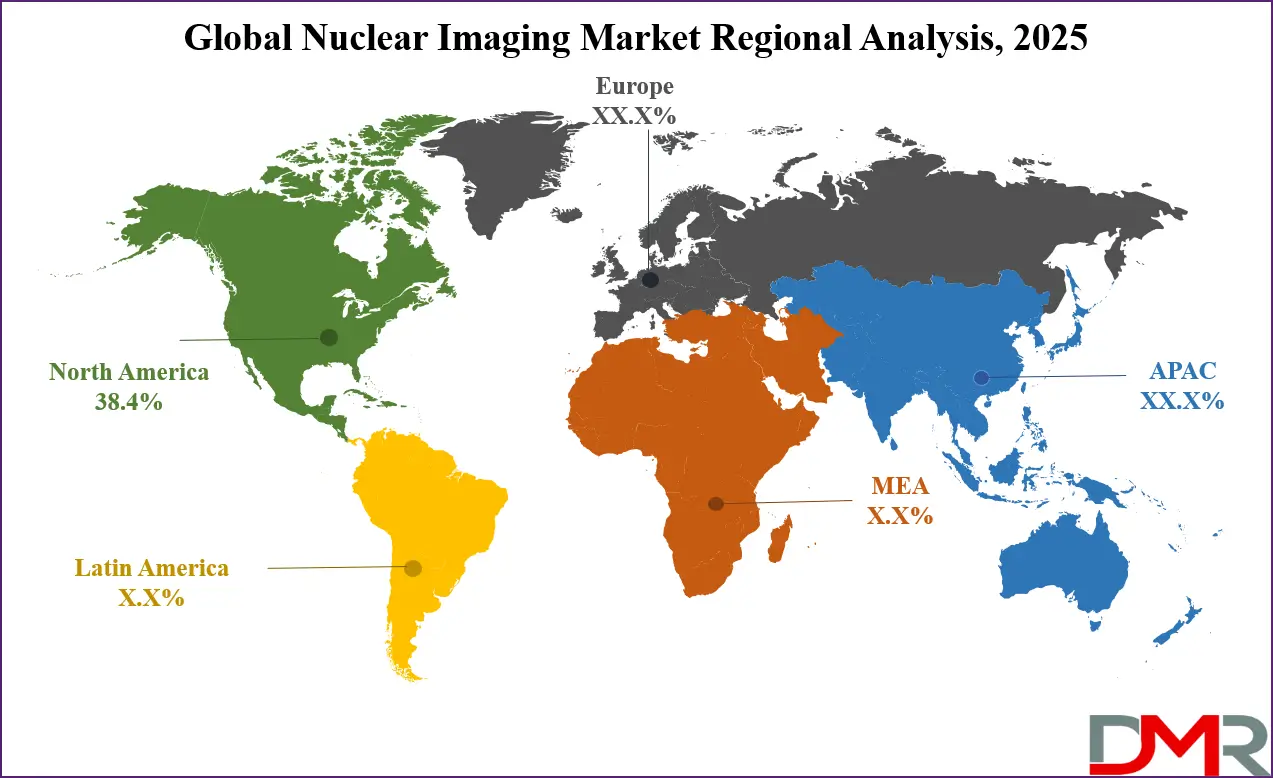

Global Nuclear Imaging Market: Regional Analysis

Region with the Largest Revenue Share

North America is projected to lead the global nuclear imaging market with 38.4% of market share in 2025, due to its robust healthcare infrastructure, high adoption of advanced imaging technologies, and strong emphasis on early disease diagnosis. The U.S. and Canada are home to some of the most advanced nuclear medicine facilities, integrating PET, SPECT, and hybrid modalities such as PET/CT and PET/MRI into routine clinical practice. Substantial investments from both government agencies and private players in healthcare modernization and medical imaging research further strengthen the region’s dominance.

The presence of leading imaging equipment manufacturers, radiopharmaceutical suppliers, and AI-driven diagnostic solution providers accelerates technological advancements. Additionally, the U.S. Food and Drug Administration (FDA) maintains a well-established regulatory framework, enabling faster approval of innovative radiopharmaceuticals and imaging systems. North America also benefits from a strong reimbursement structure for nuclear imaging procedures, making them more accessible to patients.

High prevalence rates of chronic diseases such as cancer, cardiovascular disorders, and neurological conditions drive the demand for advanced diagnostic tools. Furthermore, collaborations between academic research institutions, healthcare providers, and imaging technology companies foster innovation in image quality enhancement, quantitative diagnostics, and workflow automation. Overall, North America’s dominance is sustained by its technological leadership, favorable regulatory environment, and strong focus on precision medicine.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Region with the Highest CAGR

Asia Pacific is expected to record the highest CAGR in the global nuclear imaging market due to rapid healthcare infrastructure development, increasing healthcare expenditure, and growing awareness of advanced diagnostic technologies. Countries such as China, India, Japan, South Korea, and Australia are significantly investing in modernizing medical imaging facilities, expanding the availability of PET, SPECT, and hybrid imaging systems.

Government-led healthcare reforms, combined with private-sector investment, are enhancing access to nuclear imaging across urban and semi-urban regions. The rising incidence of cancer, cardiovascular diseases, and neurological disorders in the region, driven by aging populations and lifestyle changes, is increasing the demand for early and accurate diagnostic solutions. In addition, the expanding middle-class population with improved healthcare affordability is fueling market growth.

The Asia Pacific region is also experiencing a surge in partnerships between global imaging technology leaders and local healthcare providers, enabling the introduction of cutting-edge modalities and AI-enhanced diagnostic software. Japan and South Korea remain early adopters of nuclear imaging innovations, while China and India are emerging as high-potential markets due to large patient bases and growing medical tourism.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Global Nuclear Imaging Market: Competitive Landscape

The global nuclear imaging market is highly competitive, characterized by the presence of multinational corporations, specialized imaging equipment manufacturers, and radiopharmaceutical producers. Leading players include Siemens Healthineers, GE HealthCare, Canon Medical Systems, Philips Healthcare, Bracco Imaging, Curium, and Cardinal Health. These companies dominate the market through a combination of product innovation, strong distribution networks, and strategic collaborations.

Siemens Healthineers and GE HealthCare are at the forefront of hybrid imaging solutions such as PET/CT, PET/MRI, and SPECT/CT, incorporating AI-driven reconstruction algorithms to enhance diagnostic accuracy. Philips Healthcare continues to expand its molecular imaging portfolio, focusing on compact, high-performance systems that cater to both large hospitals and mid-sized imaging centers.

Radiopharmaceutical companies such as Curium, Bracco Imaging, and Jubilant Radiopharma play a pivotal role in supplying tracers and isotopes essential for nuclear imaging procedures. Strategic acquisitions, licensing agreements, and partnerships with hospitals and research institutions strengthen their market reach.

Emerging players and regional manufacturers are entering the market with cost-effective imaging systems, targeting price-sensitive regions in Asia Pacific and Latin America. The competitive environment is also shaped by ongoing R&D investments aimed at developing novel tracers, improving workflow efficiency, and reducing radiation dose. With AI integration and growing precision medicine adoption, competition is intensifying, pushing companies toward innovation-focused growth strategies.

Some of the prominent players in the Global Nuclear Imaging Market are:

- Siemens Healthineers

- GE HealthCare

- Koninklijke Philips N.V.

- Canon Medical Systems Corporation

- Bracco Imaging S.p.A.

- Cardinal Health, Inc.

- Curium Pharma

- Jubilant Radiopharma

- NTP Radioisotopes SOC Ltd.

- Advanced Accelerator Applications (Novartis AG)

- Mediso Medical Imaging Systems

- Digirad Corporation

- Spectrum Dynamics Medical

- Positron Corporation

- Blue Earth Diagnostics (Bracco Group)

- SOFIE Biosciences

- Lantheus Holdings, Inc.

- Eckert & Ziegler Radiopharma GmbH

- Nordion (Canada) Inc.

- IsoTherapeutics Group LLC

- Other Key Players

Recent Developments in the Global Nuclear Imaging Market

- July 2025: The U.S. Department of Energy (DOE) announced a strategic initiative to enhance domestic production of medical isotopes, particularly molybdenum-99, to reduce reliance on foreign imports and improve supply chain stability for nuclear imaging.

- May 2025: GE HealthCare unveiled an advanced PET/CT system with AI-powered motion correction technology, improving image clarity and reducing scan times for oncology and neurology applications.

- March 2025: The European Association of Nuclear Medicine (EANM) launched an updated set of clinical guidelines for nuclear imaging procedures to standardize quality and improve diagnostic accuracy across EU member states.

- December 2024: Siemens Healthineers received CE Mark approval for its new hybrid SPECT/CT scanner designed for high-resolution cardiac imaging, enabling earlier detection of coronary artery disease.

- September 2024: Japan’s Ministry of Health, Labour and Welfare (MHLW) announced expanded reimbursement policies for PET/CT scans in early cancer screening programs to promote broader adoption.

- June 2024: Bracco Imaging introduced an innovative theranostic radiopharmaceutical platform to integrate diagnosis and therapy in a single nuclear medicine workflow.

- April 2024: Philips Healthcare partnered with the University of Toronto to develop next-generation AI algorithms for real-time nuclear imaging reconstruction.

- January 2024: NorthStar Medical Radioisotopes completed the expansion of its Wisconsin production facility to increase the supply of non-uranium-based molybdenum-99 for nuclear medicine applications.

Report Details

| Report Characteristics |

| Market Size (2025) |

USD 3,173.2 Mn |

| Forecast Value (2034) |

USD 5,186.1 Mn |

| CAGR (2025–2034) |

5.6% |

| The US Market Size (2025) |

USD 1,024.8 Mn |

| Historical Data |

2019 – 2024 |

| Forecast Data |

2026 – 2034 |

| Base Year |

2024 |

| Estimate Year |

2025 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors, etc. |

| Segments Covered |

By Product (Imaging Systems, Equipment, Radioisotopes), By Application (Cardiology, Neurology, Thyroid, Oncology, Other Applications), By End User (Hospitals, Diagnostic Imaging Centres/Imaging Centers, Academic & Research Institutes/R&D, Other End Users) |

| Regional Coverage |

North America – US, Canada; Europe – Germany, UK, France, Russia, Spain, Italy, Benelux, Nordic, Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, Rest of MEA |

| Prominent Players |

Siemens Healthineers, GE HealthCare, Koninklijke Philips N.V., Canon Medical Systems Corporation, Bracco Imaging S.p.A., Cardinal Health, Inc., Curium Pharma, Jubilant Radiopharma, NTP Radioisotopes SOC Ltd., Advanced Accelerator Applications (Novartis AG), Mediso Medical Imaging Systems, Digirad Corporation, Spectrum Dynamics Medical, Positron Corporation, Blue Earth Diagnostics (Bracco Group), SOFIE Biosciences, Lantheus Holdings, Inc., Eckert & Ziegler Radiopharma GmbH, Nordion (Canada) Inc., IsoTherapeutics Group LLC., and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users), and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days, and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Nuclear Imaging Market?

▾ The Global Nuclear Imaging Market size is estimated to have a value of USD 3,173.2 million in 2025 and is expected to reach USD 5,186.1 million by the end of 2034.

What is the growth rate in the Global Nuclear Imaging Market in 2025?

▾ The market is growing at a CAGR of 5.6 percent over the forecasted period of 2025.

What is the size of the US Nuclear Imaging Market?

▾ The US Nuclear Imaging Market is projected to be valued at USD 1,024.8 million in 2025. It is expected to witness subsequent growth in the upcoming period as it holds USD 1,625.8 million in 2034 at a CAGR of 5.3%.

Which region accounted for the largest Global Nuclear Imaging Market?

▾ North America is expected to have the largest market share in the Global Nuclear Imaging Market with a share of about 38.4% in 2025.

Who are the key players in the Global Nuclear Imaging Market?

▾ Some of the major key players in the Global Nuclear Imaging Market are Siemens Healthineers, GE HealthCare, Koninklijke Philips N.V., Canon Medical Systems Corporation, Bracco Imaging S.p.A., Cardinal Health, Inc., Curium Pharma, Jubilant Radiopharma, NTP Radioisotopes SOC Ltd., and many others.