What is the Nuclear Medicine Market Size?

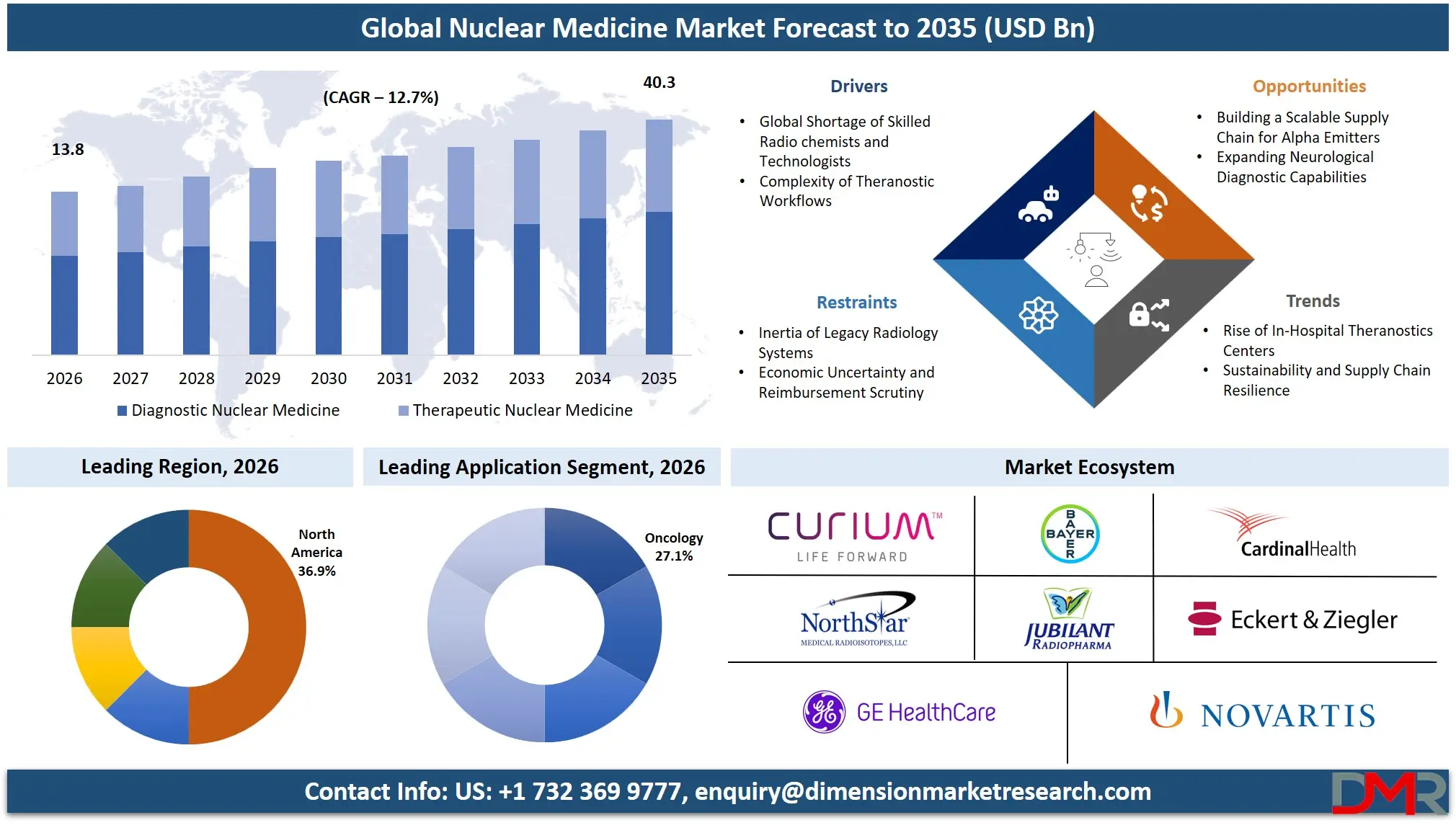

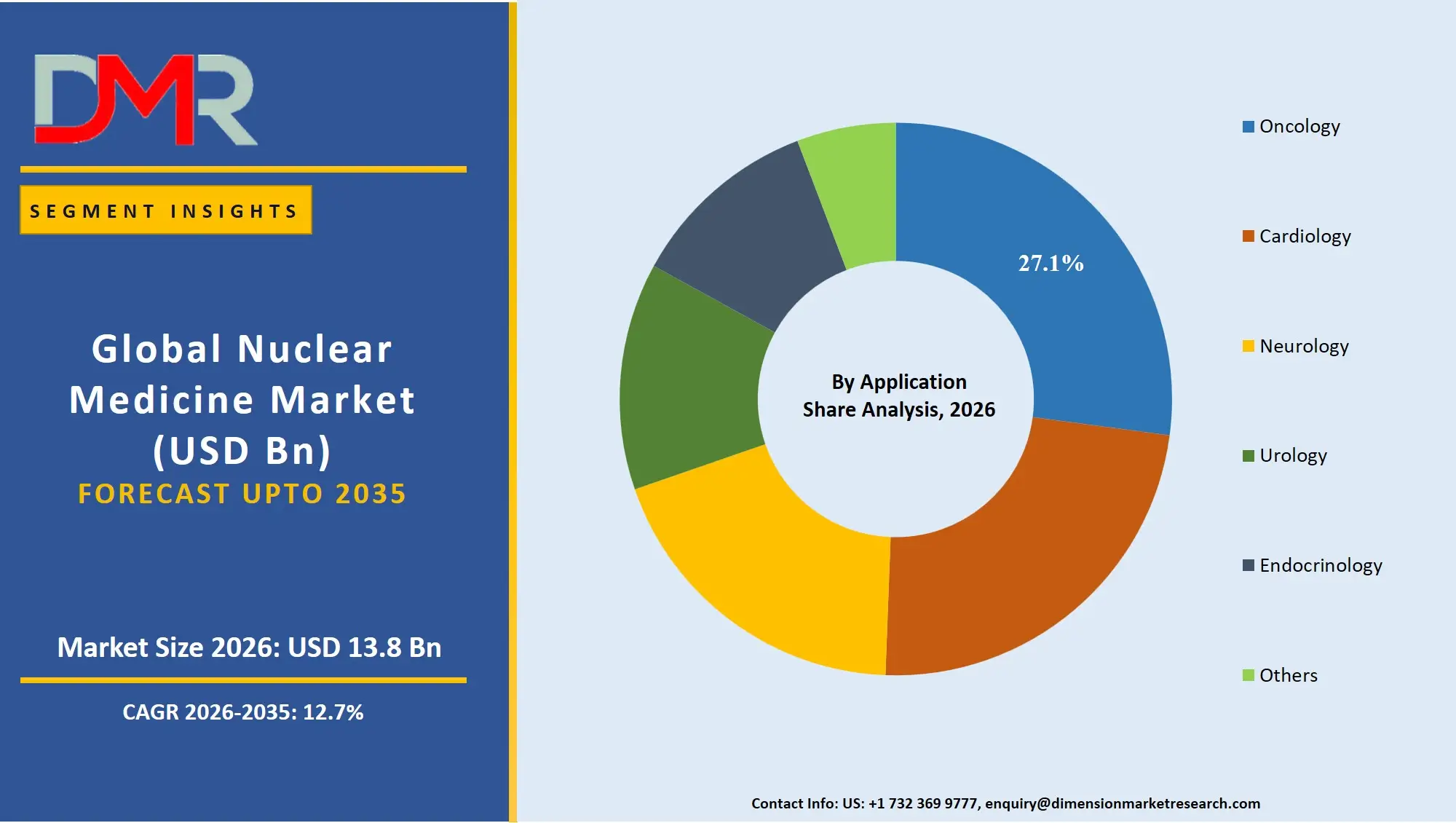

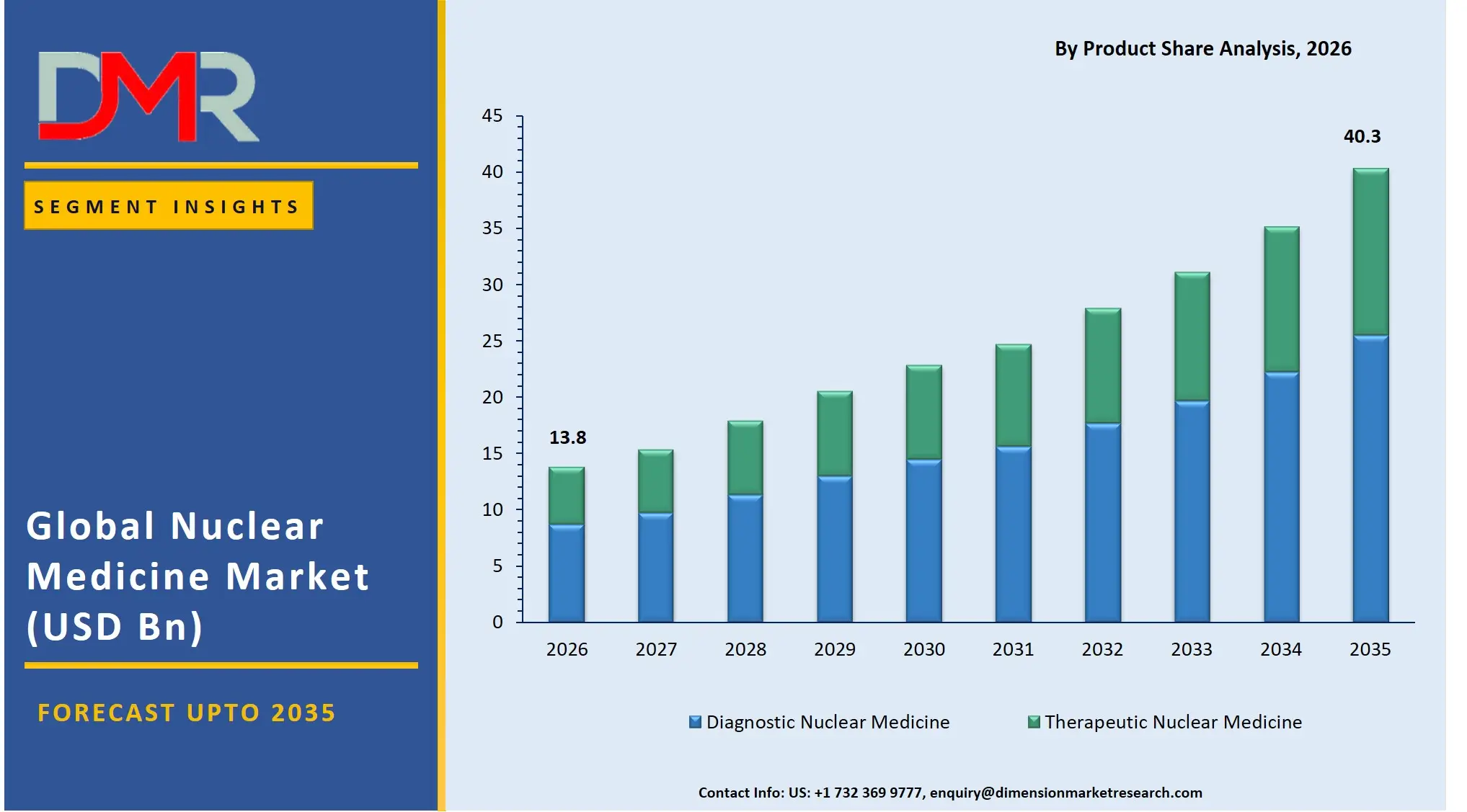

The Global Nuclear Medicine Market is expected to reach a value of USD 13.8 billion in 2026, and it is further anticipated to reach USD 40.3 billion by 2035, growing at a CAGR of 12.7% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The nuclear medicine market has been experiencing rapid growth with health systems accelerating the implementation of precision medicine and moving from traditional anatomical imaging to functional and molecular diagnosis. The market is comprised of diagnostic imaging products, therapeutic radiopharmaceuticals, and the hardware and services that help healthcare providers in the diagnosis and treatment of cancers, cardiovascular diseases, and neurological diseases. The growing need to adopt theranostic pairs, alpha-emitter therapies and AI-based image processing and analysis tools are making radiopharmaceutical products necessary.

The primary users are hospitals, with SPECT and PET diagnostic scans still being the most common due to their extensive use and coverage. The main market segments are oncology, cardiology and neurology applications as they demand targeted diagnostic and therapeutic techniques with high efficacy.

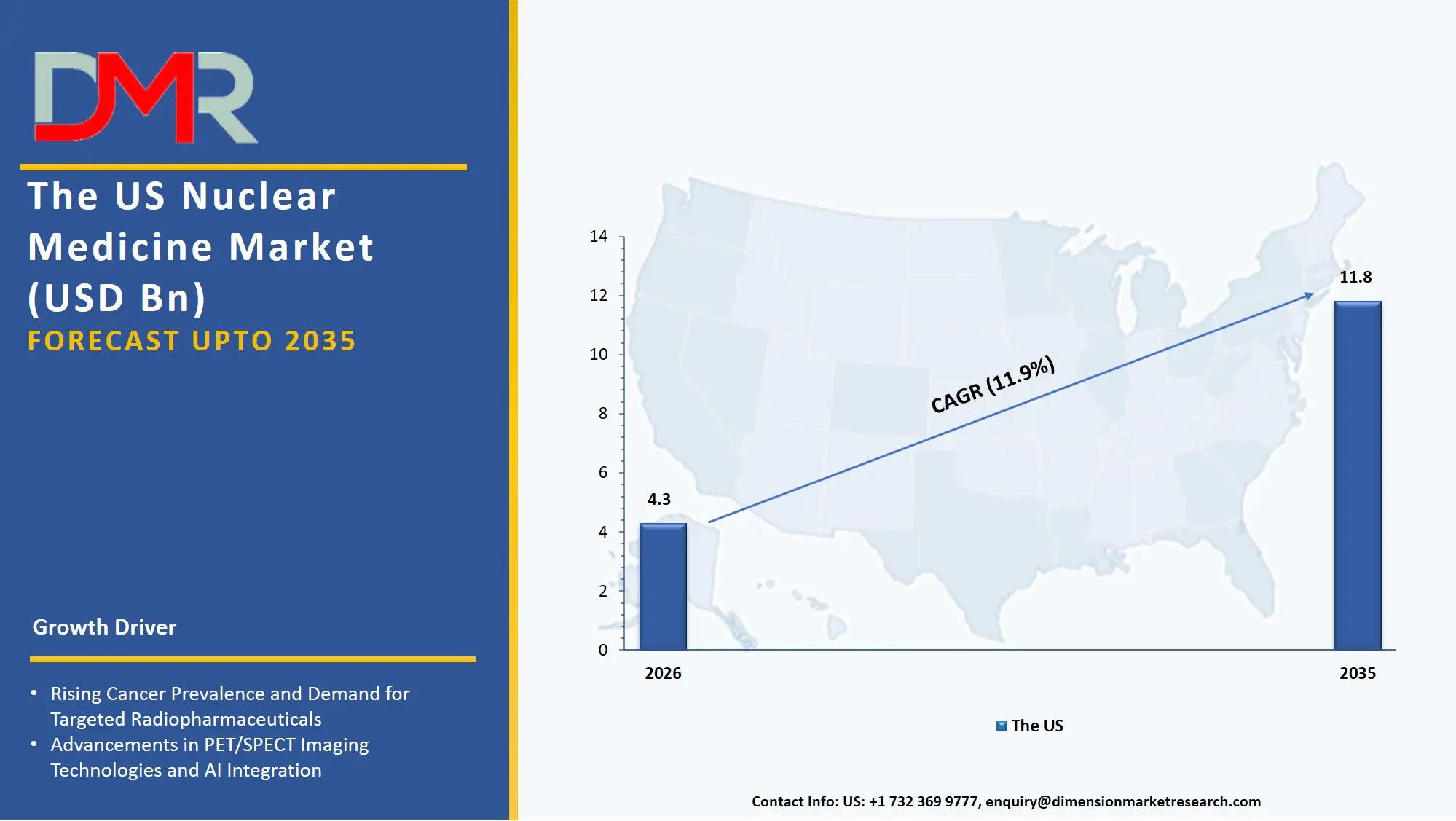

The US Nuclear Medicine Market

The US Nuclear Medicine Market is projected to reach USD 4.3 billion in 2026 at a compound annual growth rate of 11.9% over its forecast period, which is further expected to be reach a value of USD 11.8 billion by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

In nuclear medicine, the US remains the biggest and most advanced market because of the productive clinical research of academic medical centers and the increasing distribution of networks of radiopharmacy. High demand of PET diagnostics has characterized the market where providers are progressively adopting new F-18 and Ga-68 labeled tracers in oncologic and neurologic imaging. In addition, the clinical translation of therapeutic alpha emitters is generating an analogous demand in special radiopharmaceuticals and managing protocols to control targeted alpha therapy of metastatic disease.

The Europe Nuclear Medicine Market

The Europe Nuclear Medicine Market is estimated to be valued at USD 3.9 billion in 2026 and is further anticipated to reach USD 11.2 billion by 2035 at a CAGR of 12.4%. The regulatory frameworks, such as the European Medical Device Regulation (MDR) and certain directives on radiation protection, greatly influence the European market and are the force behind the necessity to establish stringent quality assurance and a safe and domestic supply of medical radioisotopes. The region is also undergoing accelerated development of therapeutic nuclear medicine with oncology institutes in Germany and France leading the way in the use of beta emitters such as Lu-177 in neuroendocrine tumors and prostate cancer. Moreover, efforts like the European Radioisotope Valley (ERV) are putting pressure on suppliers to establish committed production and logistics chains to ensure consistent access and supply chain resilience to European healthcare ecosystems.

The Japan Nuclear Medicine Market

The Japan Nuclear Medicine Market is projected to be valued at USD 1.5 billion in 2026. It is further expected to witness robust growth, holding USD 4.1 billion in 2035 at a CAGR of 11.6%. The Japanese market is distinct, and the national healthcare initiative is to respond to the super-aging population and the resulting increase in oncological and neurodegenerative conditions. A significant portion of the expenditure is on diagnostic nuclear medicine, especially with neurology SPECT imaging, and therapeutic beta emitters as specified cancer hospitals expand their facilities to include targeted radionuclide therapy. The necessity to be closely integrated with the local clinical infrastructure is also high to seal the gaps between old single-photon imaging systems and new theranostic workflows that take niche in the advanced hybrid SPECT/CT and PET/MRI systems.

Key Takeaways

- Market Size & Forecast: The Global Nuclear Medicine market is projected to reach USD 13.8 billion in 2026, expanding dramatically to USD 40.3 billion by 2035, fueled by the dual drivers of theranostic adoption and the mandatory modernization of oncology care infrastructure.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 12.7%, given the severe lack of specialized nuclear medicine physicians and the increasing complexity of dealing with new radiopharmaceutical supply chains and just-in-time patient dosing.

- Primary Growth Drivers: The major drivers are the prevalence of clinical adoption of anatomic to molecular imaging, the necessity to identify diagnostic SPECT and PET to prevent expensive late-stage cancer diagnoses, and the coordination of theranostic pairs needing a coordinated pipeline of diagnostic and therapeutic nuclear medicine products.

- Key Market Trends: The major trends involve the emergence of new alpha emitters to targeted therapy, the adoption of AI-based solutions in nuclear medicine diagnostics to auto-quantify tumor burden, and transitioning to therapeutic nuclear medicine, with oncology boards increasingly focused on precision radioligand therapies.

- By Product Analysis: Diagnostic nuclear medicine is poised to dominate this segment is dominated by SPECT and PET because both are used by clinicians to conduct accurate molecular imaging, which allows them to stage diseases accurately, select patients, minimize treatment risks, accelerate workflow, and enhance their integration with theranostic solutions in clinical practice.

- By Application Analysis: Oncology prevails this segment because of the need to handle urgent care and the capability of nuclear medicine to measure whole tumor burden without needing invasive procedures, monitor early therapies, provide personalized treatment, and spur biomarker imaging innovations and the development of theranostic radiopharmaceuticals.

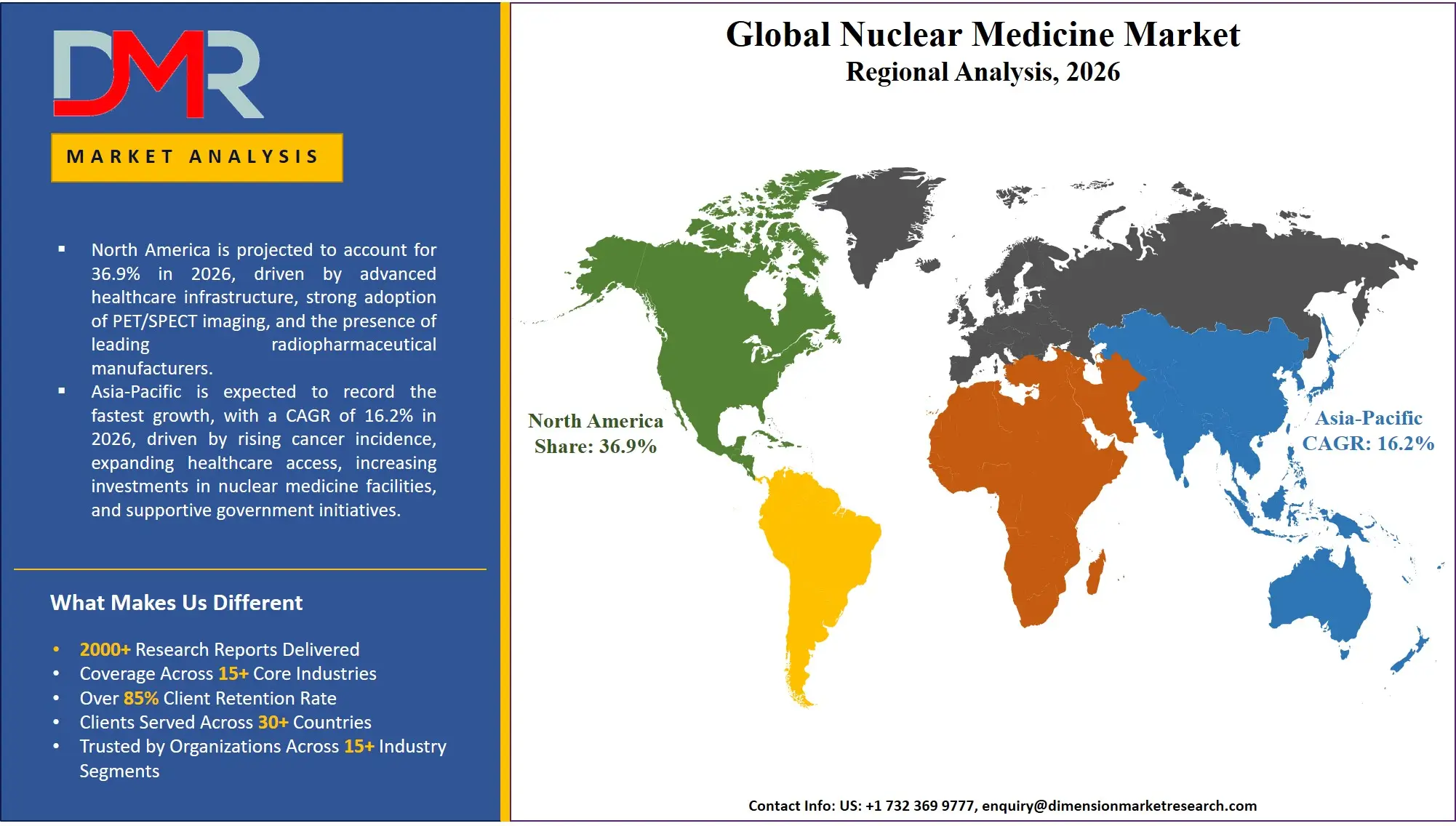

- Regional Leadership: North America is poised to dominate this market with 36.9% of the market share in 2026 because its clinical research ecosystem is well-developed and leverages this infrastructure to its maximum capacity and makes it a leader in this market.

What is the Nuclear Medicine?

Nuclear medicine is a branch of medical imaging and treatment that involves the utilization of minute quantities of radioactive substances, or radiopharmaceuticals, to perform disease diagnosis and treatment. These products are not connected to the where (anatomy) but the what of the molecular activity of a disease (in comparison to conventional radiology). This includes Diagnostic Nuclear Medicine to image organ activity and determine pathology, including SPECT to image cardiac perfusion and PET to determine where metastatic cancer is located. It also incorporates Therapeutic Nuclear Medicine to release the targeted radiation that destroys diseased cells with beta emitters and alpha emitters to treat medical conditions such as thyroid cancer and metastatic prostate cancer without affecting the large mass of surrounding normal tissue. Each year in the US alone, more than 20 million nuclear medicine procedures are done to reach precise oncology, cardiac management and precise neurological examination, which necessitates the translation of molecular data into clinical results, rather than strictly anatomical data.

Use Cases

- Theranostic Applications in Prostate Cancer: Oncology centers implement a coordinated product approach, where Ga-68 PSMA PET diagnostics are used to determine the specific location of the disease and then Lu-177 PSMA therapeutic beta emitters are used to provide specific radioligand therapy, which is a personalized treatment loop.

- Alzheimer's Disease Diagnosis: Neurology departments perform special PET diagnostics, including amyloid and tau imaging agents to ensure the presence of the Alzheimer pathology in living patients, going beyond the symptomatic evaluation to a molecular diagnosis.

- Precision Imaging in Cardiology: Hospitals are implementing SPECT diagnostics with Technetium-99m tracers to make critical decisions about revascularization and medical therapy of patients with coronary artery disease by non-invasively assessing myocardial perfusion and ventricular function.

- Targeted Alpha Therapy for Bone Metastases: Radiation oncology centers are exploiting therapeutic alpha emitters like Radium-223 to treat the symptomatic bone metastases of castration-resistant prostate cancer alongside systemic therapies to manage the disease holistically.

How AI is Transforming the Nuclear Medicine Market?

AI is transforming the nuclear medicine market by speeding up the image interpretation process, in addition to improving the efficiency of the operations. In Diagnostic Nuclear Medicine, AI-based reconstruction systems can automatically create high-definition PET and SPECT of low-count faster scans to significantly reduce radiation exposure and scan time and enhance patient comfort. In the meantime, clinicians can make superior predictions of organ-specific absorbed doses with AI-powered features in therapeutic nuclear medicine by examining imaging prior to therapy, anticipating biodistribution, and recommending the best dosing to maximize the therapeutic ratio.

AI is also becoming the center of product development and clinical research. Intelligent algorithms are also applied in the domain of research institutes where they are utilized to constantly screen immense chemical libraries and discover new tumor-targeting vectors, speeding up the development of new diagnostic and therapeutic radiopharmaceuticals. In addition, treatment planning is being supplemented by generative AI assistants simulating the biological effect of alpha emitters and model the likelihood of tumor control to provide stakeholders with a visual representation of the possible efficacy of the therapy before investing clinical resources.

Market Dynamics

Key Drivers in the Global Nuclear Medicine Market

The Global Shortage of Skilled Radiochemists and Technologists

Healthcare systems around the world are struggling to obtain qualified professionals with the expertise of cyclotron use, radiopharmaceutical production, clinical dosimetry and radiation safety. The demand on the specialized skills is growing faster than the number of trained talents and has created a structural shortage in the labor market. This is creating a tendency to outsource radiopharmacy services to hospitals and imaging centers instead of relying on the in-house production. These suppliers help in important activities such as daily delivery of radioisotopes, quality control and regulatory compliance. The outsourcing of these functions enables organizations to have access to quality nuclear medicine products of reliable quality and reduces the risks of delays in operations caused by lack of in-house capacities.

Complexity of Theranostic Workflows

Medical institutions of considerable size are adopting theranostic pairs, primarily a diagnostic PET agent and a corresponding therapeutic beta or alpha emitter, to ensure a truly personalized oncologic approach. Nonetheless, managing a theranostic workflow is very complicated. Organizations need to coordinate radiopharmaceutical procurement, patient scheduling, radiation safety protocols, and reimbursement across multiple departments using various clinical and logistical standards. This complexity may cause inefficiencies, safety risks, and unnecessary cost without the guidance of dedicated programs. Thus, there is a growing need for fully integrated radiopharmaceutical product solutions and supportive logistics that can assist hospitals to operate in such advanced treatment paradigms.

Restraints in the Global Nuclear Medicine Market

Inertia of Legacy Radiology Systems

The majority of hospital networks continue running imaging and treatment protocols that have a long history of development, and which have become deeply integrated into their own clinical processes. These are some of the traditional radiology practices that present a serious challenge to change even though nuclear medicine will provide deeper insights in terms of the molecules. Shifting the purely anatomical imaging to hybrid SPECT/CT, PET/CT and theranostic procedures can be expensive and logistical. Implementation of new radiopharmaceuticals requires extensive planning, exercise, and investment in special scanners. The organizations fear workflow obstructions, excessive initial equipment expenses, and absence of distinct reimbursement during the shift. Clinical inertia will, therefore, slow the uptake of the advanced nuclear medicine and is likely to delay or even prevent the proliferation of the new radiopharmaceutical products.

Economic Uncertainty and Reimbursement Scrutiny

Payers are more reluctant to pay new, high-priced radiopharmaceuticals and related procedures due to unstable economies and unpredictable healthcare budget conditions. Although nuclear medicine is strategic to the oncology, department heads are under pressure to prove the value of each product expenditure and to deliver quantifiable benefits to patient outcomes. The economics, as well as the complicated logistics of new therapeutic nuclear medicine products, such as alpha emitters, would face a greater examination by the hospital formulary committees. Clinicians have turned to brief, pre-established diagnostic processes which yield fast operating benefits or cost saving. Investment in new therapeutic infrastructure and products is more likely to be postponed in the long-term until the suppliers can prove an evident pharmacoeconomic payoff. This transformation is forcing the radiopharmaceutical manufacturers to become more performance oriented and results oriented.

Growth Opportunities in the Global Nuclear Medicine Market

Building a Scalable Supply Chain for Alpha Emitters

Helping global healthcare networks develop a safe, scalable supply chain of therapeutic alpha emitters is one of the key growth opportunities in nuclear medicine market. Many businesses have explored the idea of single-center production, but are currently seeking a powerful, decentralized manufacturing and distribution paradigm that fulfills their own clinical reach, regulatory needs, and patient timetables. These sophisticated targetry, chemical separation, purification, and just-in-time logistics skills are part of the expansion of these complex networks. The suppliers of radiopharmaceuticals can help cancer centers to develop reliable and on-demand access to alpha-emitter therapies that can benefit oncology programs. The region can generate a large demand in high value, highly specialized therapeutic products.

Expanding Neurological Diagnostic Capabilities

The necessity to integrate both the conclusive diagnostic devices and the knowledge of certain neurodegenerative pathologies is contributing to the development of the new PET products as the world burden of dementia increases. These include tau agents, amyloid PET tracers, and synaptic density biomarkers. Clients in neurology and psychiatry clinics must be provided with accurate and prompt differential diagnosis with specific operational needs. Therefore, they need imaging products that can deliver clear molecular data and fit into the routine clinical processes. The developers of radiopharmaceuticals can think of adding value, such as creating companion diagnostic agents, meeting payer requirements of anti-amyloid agents, and personalizing imaging protocols.

Trends in the Global Nuclear Medicine Market

The Rise of In-Hospital Theranostics Centers

Theranostics is gaining popularity in oncology institutes as an alternative to conventional and isolated care in different radiology and oncology centers. Hospitals are building In-Hospital Theranostics Centers, which provide an integrated, patient-focused service, instead of diagnosis and treatment being provided by different, dyscoordinated teams. These platforms facilitate the easy transfer between a PET diagnostic scan to a targeted beta or alpha emitter therapy. In response, radiopharmaceutical suppliers are offering product design knowledge, dosimetry aids, and automation of workflow.

Sustainability and Supply Chain Resilience

The sustainability of the environment in the production of radioisotopes is also becoming a major consideration during the decision of nuclear medicine as the institutions are pressured to achieve their corporate social responsibility and to reduce medical waste effect on the environment. Companies are now concerned with the production processes that enhance productivity and reduce the cost and the dependence on the old and highly enriched uranium-based reactors. This has led to the requirement of the cyclotron- and generator-based supply solutions. Radiopharmaceutical providers help organizations to choose isotopes that are produced locally, maximize the yield of generators and minimize waste of short-lived byproducts.

Research Scope and Analysis

The global nuclear medicine market is segmented by product into diagnostic and therapeutic nuclear medicine, by application across oncology, cardiology, neurology, and others, and by end users including hospitals, diagnostic imaging centers, research institutes, and other healthcare facilities worldwide.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Product Analysis

Diagnostic Nuclear Medicine is poised to dominate the product market in the nuclear medicine industry globally because clinicians require transparent information about the molecules before making critical therapeutic choices. Treatment plans in most situations cannot be optimized without the functional knowledge which SPECT and PET represents, which graphically depict the physiological activity of disease.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Diagnostic products have the potential to help clinicians in stage the tumors, measuring the viability of the myocardia, and distinguishing between dementias, which addresses the underlying clinical questions of where and what the disease is. SPECT and PET are in high demand. As a result of the increased utilization of theranostic pairs, by oncologists, there is an increasing need to utilize an identical diagnostic product. These products reduce the risks of treatment, enhance the choice of patients, accelerate clinical processes, and increase the returns on the investment in therapeutic nuclear medicine in the long term.

By Application Analysis

Oncology projected to remain the dominant application owing to the clinical urgency and the versatility of nuclear medicine products. Nuclear medicine is preferred by organizations, as it enables them to characterize the whole tumor burden, in a non-invasive manner, which removes blind-treatment decisions and sampling error risks. The segment allows the quick monitoring of therapy, which is why a change in the treatment regimen can be activated by the clinician within weeks of its commencement. Thereby, nuclear medicine product ecosystem flourishes on oncology, addressing critical adjacent activities such as novel cancer biomarker imaging, theranostic matching of prostate and neuroendocrine tumors, and tailored synthesis of targeted agents to ensure that radiopharmaceuticals respond to the genetic and molecular profile of the specific cancer of the individual patient.

By End-User Analysis

Hospitals are expected to dominate nuclear medicine because of the magnitude and complexity of their clinical operations. They have large capital budgets and extensive portfolios of programmed patient care pathways, which in most cases are comprised of more intricate oncological and cardiovascular programs that demand careful diagnostic and treatment coordination. As compared to smaller clinics which can quickly implement off-the-shelf diagnostic equipment, large hospitals have complicated departmental silos and rigid in-patient radiation safety regulations. Their nuclear medicine missions demand product portfolios of high volume SPECT diagnostics of emergency departments, targeted PET diagnostics of comprehensive cancer staging, and therapeutic alpha and beta emitters of in-patient radioligand therapy program, integrating care across multiple disciplines at once.

The Global Nuclear Medicine Market Report is segmented on the basis of the following:

By Product

- Diagnostic Nuclear Medicine

- Therapeutic Nuclear Medicine

- Alpha Emitters

- Beta Emitters

- Brachytherapy Isotopes

By Application

- Oncology

- Cardiology

- Neurology

- Urology

- Endocrinology

- Others

By End-User

- Hospitals

- Diagnostic Imaging Centers

- Research Institutes

- Others

Regional Analysis

Leading Region by Market Share

North America is poised to dominate the global nuclear medicine market as it is projected to hold 36.9% of the market share by the end of 2026. The United States, which dominates The largest share of the nuclear medicine market is held by the United States, which dominates North America due to the unrivalled presence of top cancer hospitals and the ambitious precision medicine programs of major academic institutions. The region has a supporting infrastructure of leading global radiopharmaceutical companies, nuclear pharmacies and nuclear medicine physicians and scientists. Corporate investment in new theranostic pairs, state-of-the-art alpha emitters, and overall replacement of old gamma cameras with hybrid SPECT/CT and PET/MRI technologies ensure that the demand for diagnostic and therapeutic nuclear medicine products, and innovation, continues to be strong. In addition, a strong venture capital environment continues to fund emerging biotech companies that require strong supply chains to allow rapid clinical trials and FDA approval.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Regional Market

Asia-Pacific is expected to be the most rapidly expanding nuclear medicine market, given the large-scale government driven healthcare infrastructure reform programs in India, China, Japan and Southeast Asia. The rapid economic development, emergence of a large ageing population and the rapid growth of private sector hospitals is forcing existing hospital conglomerates and government agencies to upgrade facilities with cutting-edge diagnostic imaging equipment. Nuclear medicine therapeutic products are highly sought after to enable these large hospital systems to move in the direction of integrated cancer care models. There is also a dire shortage of nuclear medicine physicians in the region, and it is imperative to engage with international vendors to ensure product supply, training, and quality control to fill the gap and accelerate uptake of new theranostic products.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive environment of the global nuclear medicine market has become highly dynamic with a heterogeneous array of multinational pharmaceutical giants, specialized pure-play radiopharmaceutical companies, and emerging clinical stage biotechs. The ability to build intense partnerships with cyclotron networks, hospital conglomerates, and logistics companies will be crucial for success as they will open the essential channels to market and provide efficient just-in-time supply of short-lived isotopes. Consolidation of the market is rapidly taking place, with established diagnostic imaging vendors buying theranostics-focused biotech start-ups that focus on new targets and alpha-emitter products to remain competitive. Intellectual property in the form of albumin-binder conjugates to prolong tumor retention and site-specific conjugation methods is gaining more relevance than simple generic isotope provision or radiolabeling technologies.

Some of the prominent players in the Global Nuclear Medicine Market are:

- GE HealthCare

- Cardinal Health

- Siemens Healthineers

- Novartis

- Curium Pharma

- Bayer AG

- Bracco Imaging

- Lantheus Holdings

- Jubilant Radiopharma

- Eckert & Ziegler

- Telix Pharmaceuticals

- NorthStar Medical Radioisotopes

- SOFIE Biosciences

- Spectrum Dynamics Medical

- IBA Molecular

- Isotopia Molecular Imaging

- BWXT Medical

- Blue Earth Diagnostics

- Cerveau Technologies

- Actinium Pharmaceuticals

- Other Key Players

Recent Developments

- January 2026: Novartis announced it will invest in significantly expanding its radioligand therapy (RLT) manufacturing network, a strategic move to support Oncology and Neurology patients with its proprietary therapeutic nuclear medicine products through a global network of production sites and expertise with targeted alpha and beta emitters.

- November 2025: GE HealthCare deepened its partnership with a major pharmaceutical company and launched a dedicated practice for theranostic PET diagnostic and therapeutic alpha emitters to support oncology treatment facilities in the easy incorporation of new diagnostic products into prostate cancer treatment protocols and to stay compliant with international pharmaceutical regulations.

- October 2025: Telix Pharmaceuticals bought a European radiochemistry company to expand its diagnostic nuclear medicine and therapeutic product solutions for urological cancers, to address the complex needs of hospitals and specialist imaging centers to deliver next-generation theranostic services.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 13.8 Bn |

| Forecast Value (2035) |

USD 40.3 Bn |

| CAGR (2026–2035) |

12.7% |

| The US Market Size (2026) |

USD 4.3 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Product, By Application, and By End-Use |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Nuclear Medicine Market?

▾ The Global Nuclear Medicine market is poised to be valued at USD 13.8 billion in 2026 and is projected to reach USD 40.3 billion by 2035, driven by the universal need for specialized products in precision oncology, cardiac viability assessment, and neurological differential diagnosis.

Which region held the largest share of the Nuclear Medicine Market in 2026?

▾ North America is poised to dominate this market with 36.9% of market share in 2026, driven by a mature clinical ecosystem and aggressive hospital investment in nuclear medicine diagnostics and AI-enhanced molecular imaging capabilities.

Who are the key players in the Global Nuclear Medicine Market?

▾ Key players include global healthcare giants like Siemens Healthineers, GE HealthCare, and Novartis, as well as specialized pure-play radiopharmaceutical companies like Curium, Lantheus Holdings, and Telix Pharmaceuticals, alongside a growing field of clinical-stage biotech firms.

What is the CAGR of the Global Nuclear Medicine Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 12.7% from 2026 to 2035, reflecting the accelerating complexity of radiopharmaceutical theranostics and the persistent shortage of specialized clinical talent and radioisotope supply.

What factors are driving the growth of the Global Nuclear Medicine Market?

▾ Key drivers include the global shift to targeted alpha and beta emitter therapies, the imperative to clinically validate new disease biomarkers with PET diagnostics, the management complexity of radioisotope supply chains, and the surge in demand for theranostic pairs amid evolving precision oncology guidelines.

Which region is expected to grow the fastest in the Nuclear Medicine Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid healthcare modernization in India, China, and Japan, where therapeutic nuclear medicine products are critical for transitioning large hospital networks to comprehensive cancer care models.

What are the major trends in the Global Nuclear Medicine Market?

▾ Major trends include the clinical translation of targeted alpha emitters, the rise of in-hospital theranostics centers, the demand for novel neurological diagnostics, and the focus on production and supply chain resilience within complex radiopharmaceutical networks.

How is the Global Nuclear Medicine Market segmented?

▾ The market is segmented by Product, Application, and End-User.