Market Snapshot

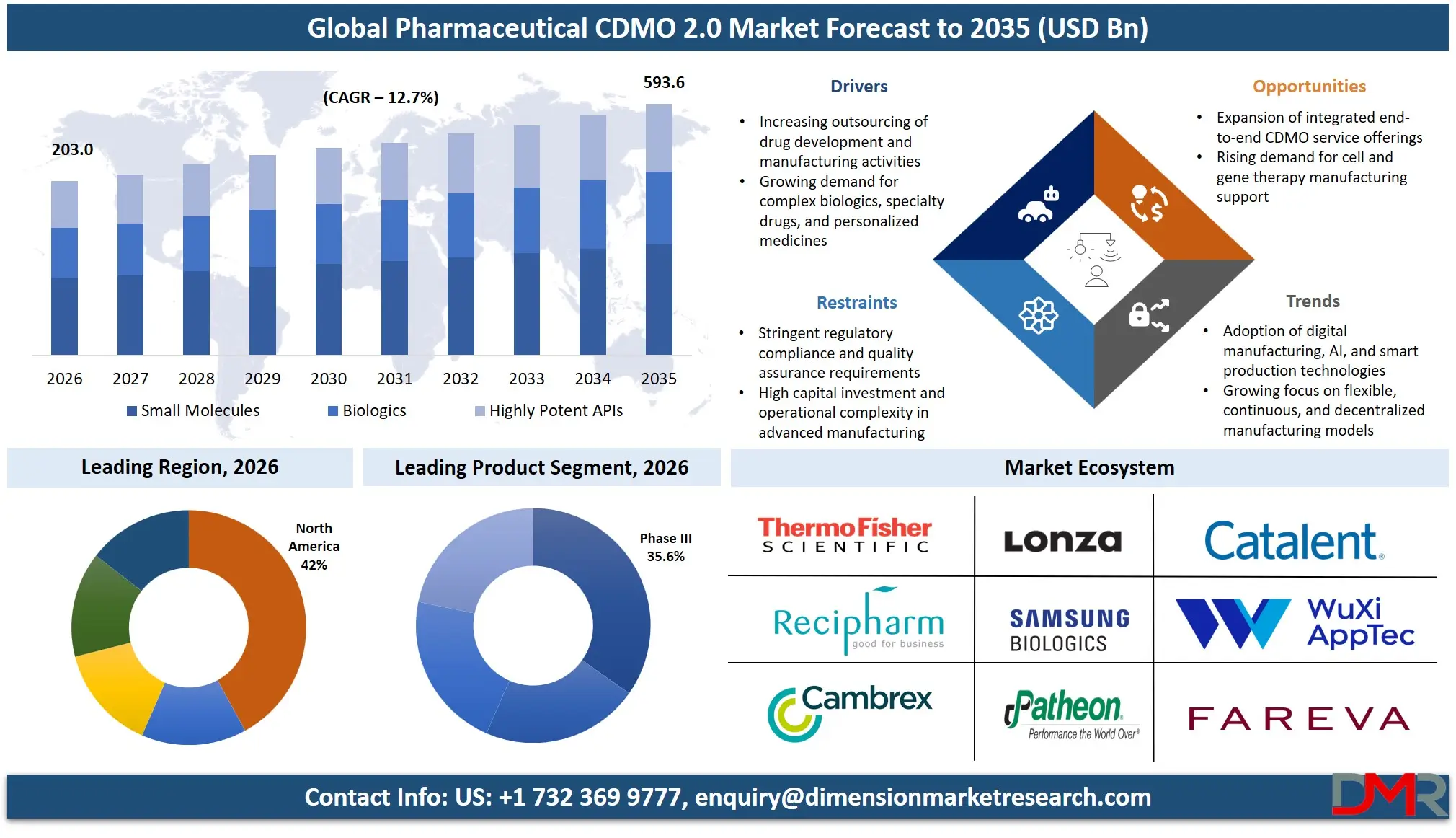

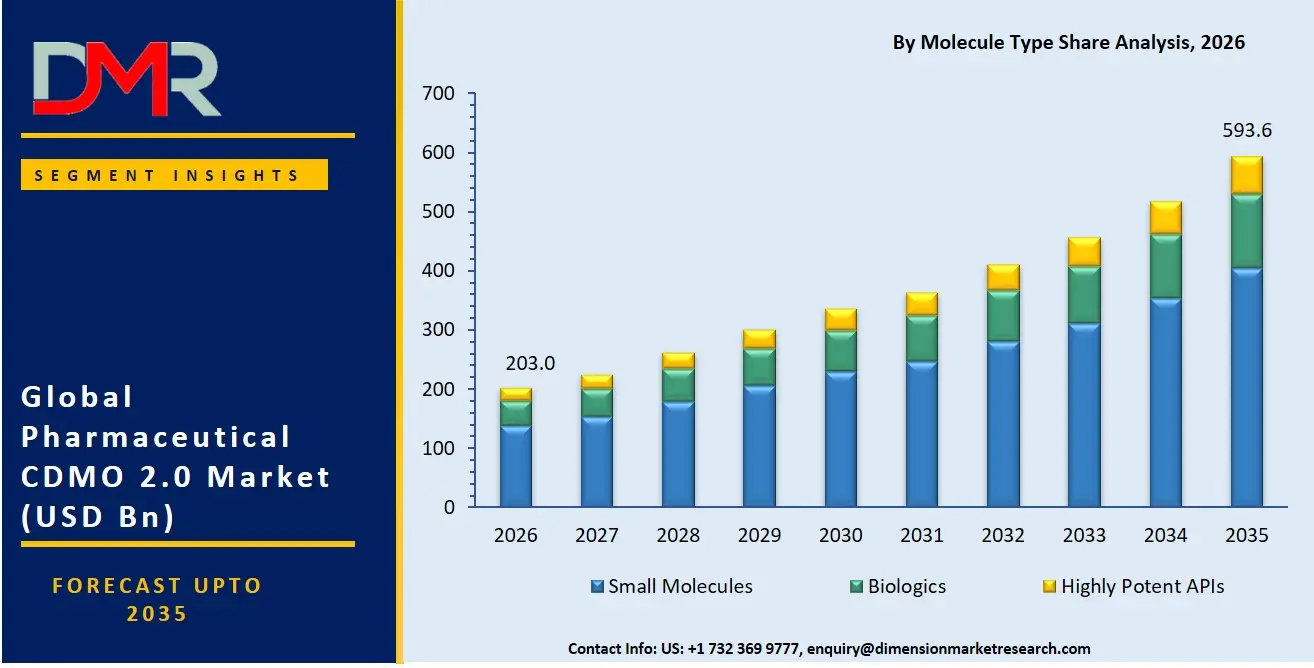

- The market size is USD 179.6 Billion in 2025, reached USD 203.0 Billion in 2026, and is projected to hit USD 593.6 Billion by 2035 at a CAGR of 12.7%.

- API Development and Manufacturing leads the By Service segment with a 63.8% revenue share in 2026.

- Small Molecules hold a 68.3% share in the By Molecule Type segment in 2026.

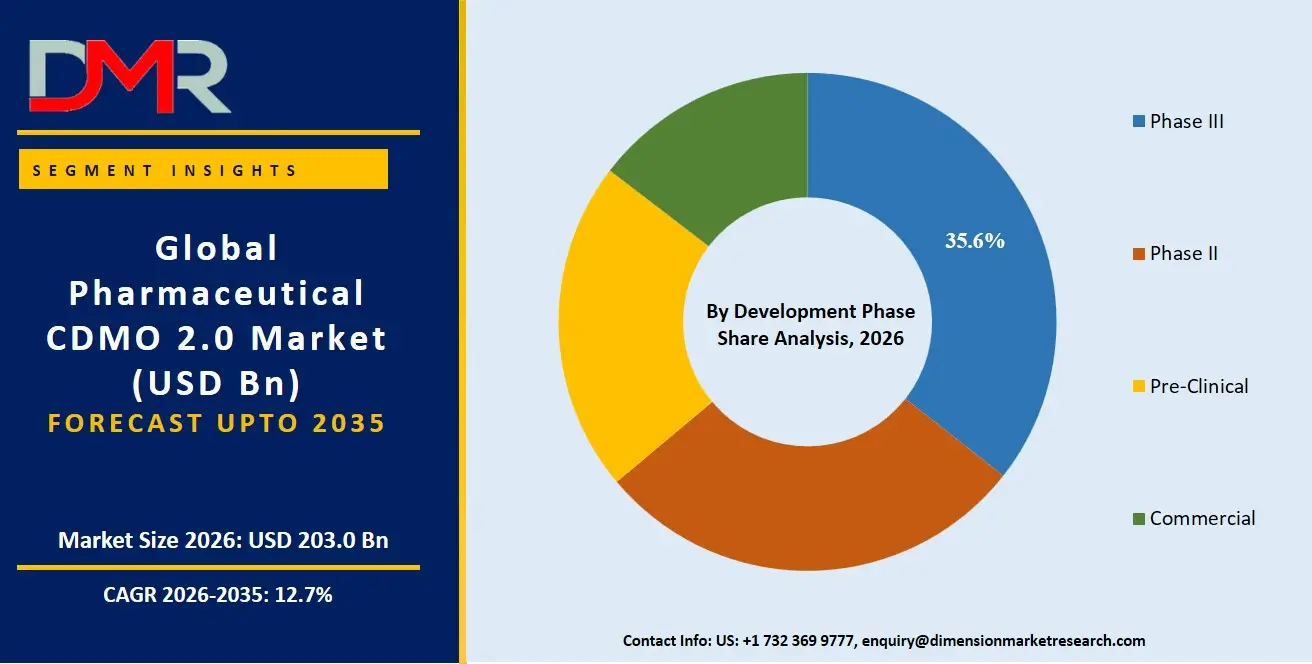

- Phase III commands a 35.6% share of the By Development Phase segment in 2026.

- Large Pharma accounts for a 48.6% share of the By End User segment in 2026.

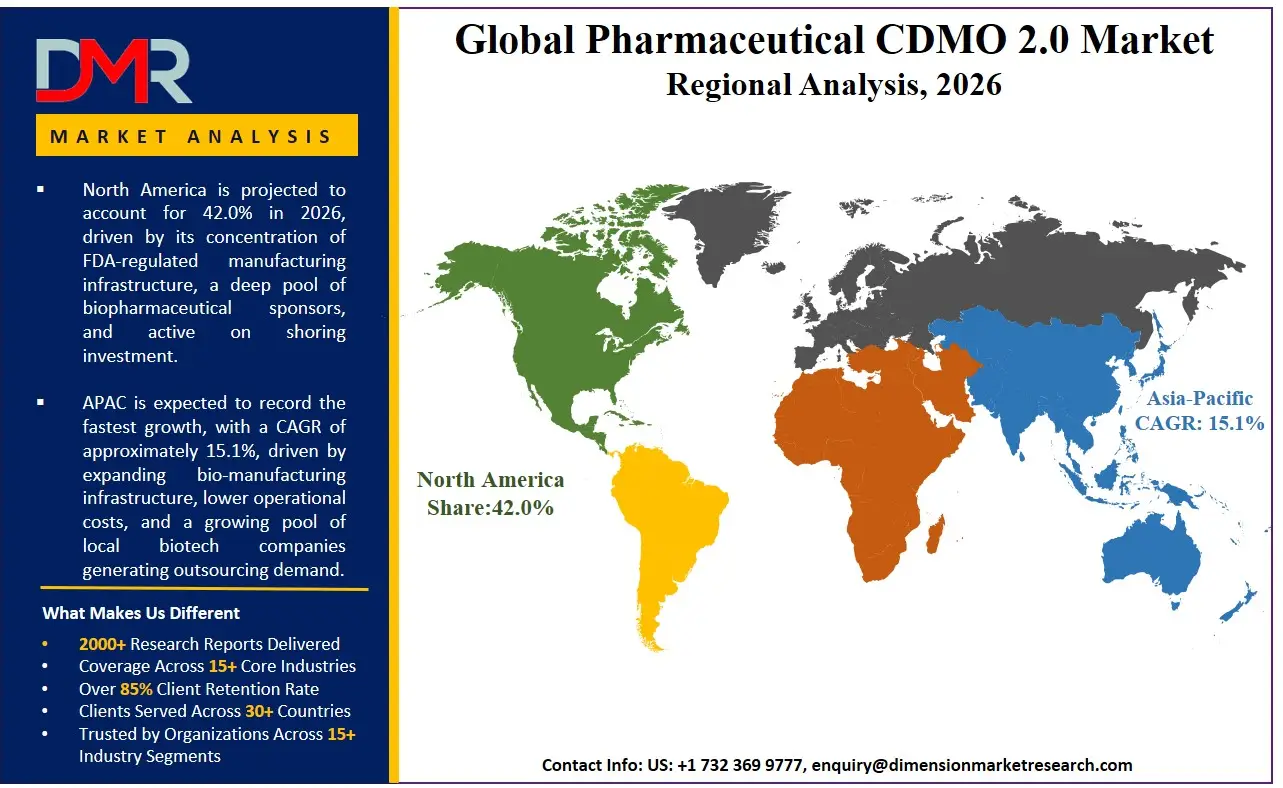

- North America leads all regions with a 42.0% revenue share; Asia Pacific is the fastest-growing region.

- The U.S. market is valued at USD 69.9 Billion in 2026, growing at a CAGR of 11.5%.

- Key players include Lonza, Samsung Biologics, Thermo Fisher Scientific (Patheon), Catalent (Novo Holdings), WuXi AppTec, Fujifilm Diosynth, Recipharm, AGC Biologics, Piramal Pharma Solutions, and Siegfried.

Market Overview

The Pharmaceutical CDMO 2.0 market covers outsourced contract development and manufacturing services across API production, finished-dosage manufacturing, analytical testing, and packaging. Internal manufacturing by integrated pharmaceutical companies that do not offer third-party services sits outside this boundary. That exclusion defines where commercial risk and capital have migrated away from pharma balance sheets toward specialized operators who now bear the operational burden and capture the pricing premium.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Pharma companies are choosing to pay for capacity rather than build it. Drug pipelines shifting toward biologics and advanced therapies carry complexity that most internal facilities cannot support cost-efficiently. As reported by BioPlan Associates, 56.7% of CDMOs were testing new upstream platforms in 2026, compared to 45.1% of internal pharma facilities. CDMOs are outpacing pharma's own manufacturing teams in technology adoption, which strengthens the outsourcing case for every new molecule entering development.

Concentration at the end-user level creates a structural tension for CDMO operators. Large Pharma holds a 48.6% end-user share, meaning revenue depends heavily on a small number of high-value clients. Emerging biotech and virtual pharma are growing fast but bring smaller deal sizes and higher clinical attrition. CDMOs that balance these two client types manage revenue risk more effectively than those anchored to either segment alone.

Market Size and Forecast

The Global Pharmaceutical CDMO 2.0 Market size is estimated at USD 203.0 Billion in 2026 from USD 179.6 Billion in 2025, and is projected to reach USD 593.6 Billion by 2035, exhibiting a CAGR of 12.7% during the forecast period.

The U.S. market, valued at USD 69.9 Billion in 2026, grows at a slower CAGR of 11.5%, confirming that global growth velocity will increasingly come from outside North America. The top 10 CDMOs generated combined revenue of USD 31.8 Billion in 2024, up 5% year-over-year as reported by GEN. That demand base provides the foundation for the compound trajectory through 2035. Resilience secured up to USD 825 Million in long-term financing in October 2025, directed at sterile and complex biologics manufacturing, signaling that private capital is pricing in sustained outsourcing acceleration well ahead of the forecast window.

Samsung Biologics completed its acquisition of GSK's Rockville, Maryland facility in March 2026, adding approximately 60,000L of capacity for its first U.S. manufacturing presence. If similar facility acquisitions continue at this pace, the market could absorb outsourced volume ahead of the base case. A downside scenario exists if BIOSECURE Act compliance timelines, enacted in late 2025, stall tech transfers and compress growth below the 12.7% CAGR base, particularly between 2026 and 2028.

Service Analysis

API Development and Manufacturing accounted for a 63.8% share of service demand in 2026, the highest of any category.

API manufacturing requires specialized chemistry expertise, controlled-environment infrastructure, and regulatory-grade quality systems that most pharma companies prefer to outsource rather than maintain internally. This segment's lead is structural, not cyclical. CDMOs that hold validated API capacity across multiple chemistry platforms capture the widest range of client programs and face the least competitive pressure from generalist operators.

Finished-Dosage Development and Manufacturing is gaining commercial relevance as CDMOs expand fill-finish capacity for sterile injectables. Analytical and Testing Services underpin every other category: without validated testing capabilities, CDMOs cannot release batches or satisfy regulatory requirements.

Batch record automation at a global CDMO handling over 10,000 batches annually cut average review time by 60%, as confirmed by an Acodis 2025 case study, shortening time from batch completion to product release by several days. Packaging and Logistics closes the value chain from manufacturing to market-ready product, and CDMOs treating it as a margin-generating service layer rather than an afterthought are capturing commercial-stage stickiness that purely manufacturing-focused competitors miss.

Molecule Type Analysis

With a 68.3% share in 2026, Small Molecules outpaced all other Molecule Type categories.

Decades of accumulated process knowledge, widely available synthesis infrastructure, and a generics pipeline generating high-volume outsourcing contracts anchor this position. Lonza's Advanced Synthesis platform reported +22.4% CER sales growth in FY 2025 with a CORE EBITDA margin of 41.8%, confirming that small molecule CDMO operations remain highly profitable when executed at scale. The margin performance at that growth rate signals that pricing power in this segment is intact despite its maturity.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Biologics are attracting the largest absolute capital investments of any molecule type. Samsung Biologics reported FY 2025 revenue of KRW 4,557 Billion (USD 3 Billion), up 30.3% year-over-year, with operating profit of KRW 2,069.2 Billion (USD 1.3 Billion) up 56.6%, driven by full utilization across Plants 1 through 4. Highly Potent APIs require specialized containment infrastructure that limits the number of capable CDMOs, creating pricing power for those that have made the required facility investments. That structural scarcity makes HPAPI manufacturing one of the more defensible sub-segments in the broader market.

Development Phase Analysis

Phase III led the Development Phase segment with a 35.6% share in 2026.

Phase III demands the largest batch sizes, the most rigorous regulatory documentation, and the closest alignment between CDMO and sponsor processes. CDMOs that win Phase III contracts frequently transition directly into commercial supply agreements, making this the most strategically valuable entry point in the development pipeline. Winning at Phase III is not just a revenue event. It is a relationship lock that compounds value over the entire commercial lifecycle of a drug.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Phase II sits at the critical decision point where clinical proof-of-concept converts into scaled development programs. CDMOs with strong Phase II relationships gain early pipeline visibility and position themselves for downstream Phase III and commercial contracts. Pre-Clinical services carry higher attrition risk because most molecules entering this stage do not reach commercialization, making revenue at this phase volume-dependent rather than value-driven. Commercial manufacturing delivers the highest revenue per program but demands the deepest compliance infrastructure to sustain across multiple simultaneous programs.

End User Analysis

Large Pharma captured a 48.6% share of the End User segment in 2026, ahead of all rivals.

Large pharma clients bring program scale, multi-year contract structures, and predictable volume commitments that anchor CDMO revenue forecasts. Samsung Biologics secured a KRW 1.1 trillion (USD 730 Million) manufacturing agreement with a European pharmaceutical company in Q4 2025. Deals at that scale are only achievable with large pharma counterparties and reflect the contract concentration that defines this end-user tier.

Emerging and venture-backed biotech companies bring novel molecule types and compressed timelines but require CDMOs to manage a larger number of simultaneous programs across diverse portfolios. Generics and specialty pharma clients focus on cost-efficient high-volume production. Arxada's 2025 small-molecule CDMO campaign delivered an 18% increase in volumetric productivity with a batch success rate above 99%, showing the operational discipline required to serve this cost-sensitive segment profitably. Virtual pharma companies operate without internal manufacturing infrastructure and rely entirely on CDMOs, creating longer-duration but more resource-intensive relationships that reduce attrition risk for operators who invest in deep account integration.

Business Model Analysis

The End-to-End Integrated model led the Business Model segment due to full-service continuity across development and commercial manufacturing.

Lonza's CDMO business generated CHF 6.5 Billion (USD 8.2 Billion) in sales in FY 2025 across biologics, small molecules, bioconjugates, and drug product platforms simultaneously. Full-service integration reduces client dependency on multiple vendors and creates a revenue base that spans multiple service categories, lowering concentration risk at the operator level. CDMOs with genuine end-to-end capability are not competing on price; they are competing on the operational simplicity they offer sponsors managing complex global programs.

Tech-Enabled CDMOs are building digital process tools and automated quality systems into their competitive positioning. ESTEVE CDMO committed USD 15.5 Million to its Morton Grove small-molecule API facility in March 2026, reflecting a niche-focused capital strategy where depth in a defined technical area creates competitive barriers that generalist operators cannot easily replicate. Sustainability-Driven CDMOs are responding to pharma procurement criteria that now include environmental performance metrics. On-Demand and POD Manufacturing models offer sponsors flexible capacity without long-term volume commitments, commanding a flexibility premium that compensates for lower utilization rates.

Drug Type Analysis

Small Molecules led the Drug Type segment due to established process infrastructure and high-volume generics outsourcing.

Lonza's Advanced Synthesis platform, covering small molecules and bioconjugates, delivered +22.4% CER sales growth in FY 2025. The CORE EBITDA margin of 41.8% at that growth rate confirms that small molecule manufacturing generates returns that continue to justify capital allocation to this drug type despite the sector's maturity. Operators with efficient synthesis platforms are not under margin pressure; they hold pricing power in a segment where process expertise is the barrier.

Biologics attract the largest absolute capital commitments across the sector. FUJIFILM Biotechnologies' total Holly Springs investment exceeded USD 3.2 Billion, with 8 x 20,000L bioreactors planned by 2028. Advanced Therapies, including cell and gene therapies, represent the highest-complexity category. CDMOs entering this space face stringent FDA oversight and long validation timelines, but those that establish validated capacity operate in a segment where client alternatives are extremely limited, which translates directly into pricing power and long-term contract security.

Therapeutic Area Analysis

Oncology led the Therapeutic Area segment due to high pipeline volume and complex molecule manufacturing requirements.

Oncology pipelines generate a disproportionate share of biologics and ADC manufacturing contracts, which are among the highest-value programs in the CDMO sector. Lonza's bioconjugates platform was a key contributor to its +21.7% CER sales growth in FY 2025, confirming oncology-linked manufacturing as a core revenue driver for top-tier operators. CDMOs that build ADC and bioconjugate capability are not just serving oncology; they are accessing the highest per-program revenue tier in the entire CDMO portfolio.

Rare and Orphan Diseases attract CDMO investment because small patient populations require highly specialized, low-volume manufacturing with premium pricing structures. Infectious Diseases provide revenue stability through both commercial contracts and government procurement programs, a dual-channel dynamic that purely commercial pipelines cannot replicate. Autoimmune and CNS Disorders increasingly involve biologic treatments that require mammalian cell culture manufacturing, meaning CDMOs expanding biologics capacity for oncology simultaneously gain the infrastructure to compete for autoimmune and CNS contracts without incremental capital.

Key Market Segments

By Service

- API Development and Manufacturing

- Finished-Dosage Development and Manufacturing

- Analytical and Testing Services

- Packaging and Logistics

By Molecule Type

- Small Molecules

- Biologics

- Highly Potent APIs

By Development Phase

- Phase III

- Phase II

- Pre-Clinical

- Commercial

By End User

- Large Pharma

- Emerging / Venture-Backed Biotech

- Generics / Specialty Pharma

- Virtual Pharma and Tech-Bio

By Business Model

- End-to-End Integrated

- Tech-Enabled CDMOs

- On-Demand / POD Manufacturing

- Niche-Focused

- Sustainability-Driven

- Hybrid Partnerships

By Drug Type

- Small Molecules

- Biologics

- Advanced Therapies

By Therapeutic Area

- Oncology

- Rare / Orphan Diseases

- Infectious Diseases

- Autoimmune and CNS Disorders

Regional Analysis

North America held a 42.0% share in 2026, anchored by a U.S. market valued at USD 69.9 Billion.

The region's dominance reflects its concentration of FDA-regulated manufacturing infrastructure, a deep pool of biopharmaceutical sponsors, and active onshoring investment. U.S.-based CDMO capacity is attracting multi-hundred-million dollar commitments from operators seeking to serve the world's largest regulated pharmaceutical market from within its borders. Operators without a U.S. manufacturing footprint face a growing competitive disadvantage as pharma sponsors prioritize supply chain proximity and regulatory alignment.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Asia Pacific is the fastest-growing region, driven by expanding biomanufacturing infrastructure, lower operational costs, and a rising base of local biotech companies generating outsourcing demand. The BIOSECURE Act enacted in late 2025 is prompting pharma companies to reassess supply relationships with certain Asian operators, creating both disruption for incumbents and entry opportunities for compliant regional CDMOs that can absorb transferred programs. Europe maintains a strong position through established regulatory expertise and deep small-molecule manufacturing history. Latin America and the Middle East and Africa remain early-stage CDMO geographies where regulatory alignment with FDA and EMA standards constrains international investment in the near term.

Key Regions and Countries

North America

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Market Dynamics

Outsourcing Acceleration and U.S. Onshoring Drive Biologics Capacity Investment

Pharmaceutical companies are transferring manufacturing responsibility to specialized CDMOs at a measurable and accelerating pace. As reported in Lonza's January 2026 results, its CDMO business delivered CHF 6.5 Billion (USD 8.2 Billion) in sales with +21.7% CER growth in FY 2025. That level of growth at the market's largest operator confirms outsourcing is a strategic manufacturing model, not a cost-cutting response. FUJIFILM Biotechnologies' total investment in its Holly Springs, NC facility exceeded USD 3.2 Billion, with 8 x 20,000L mammalian cell culture bioreactors planned by 2028, creating one of the largest cell culture CDMO facilities in North America. Capital at this scale is irreversible and locks competitive positioning for a decade.

GLP-1 therapies are reshaping CDMO investment priorities toward injectable and peptide manufacturing capacity. CDMOs that establish sterile fill-finish capacity now will control a bottleneck that competitors will struggle to replicate quickly. Operators without this capability face structural exclusion from one of the fastest-growing drug categories in the current commercial cycle.

BIOSECURE Act Timelines and FDA Scrutiny Raise Compliance Thresholds

The BIOSECURE Act, enacted in late 2025, forces CDMOs and pharma clients to rebuild supplier relationships on multi-year transition timelines while maintaining uninterrupted manufacturing. CDMOs with diversified, geographically distributed supply bases absorb this pressure better than those with concentrated overseas dependencies. The FDA has increased 483 observations and Warning Letters alongside heightened oversight of advanced therapies and quality agreements. For CDMOs manufacturing cell and gene therapies, tighter documentation and longer inspection cycles raise the cost of compliance in ways that do not scale linearly with revenue, placing disproportionate burden on smaller operators.

Advanced Therapy Capacity and Biosimilar Production Open New Revenue Tiers

Advanced therapy and high-potency manufacturing represent the segment where CDMO investment is most concentrated and most defensible. Technical barriers alone deter most new entrants, so operators that establish validated advanced therapy capacity face very limited competition for the highest-value contracts. As reported by BioPlan Associates, 35.8% of biomanufacturing facilities named bioprocess automation as their top new budget area in 2025, and 44.3% were deploying automated continuous processing systems. CDMOs leading on automation shorten client timelines and improve batch consistency, converting technology investment into tangible contract-winning advantage.

Biosimilar and complex molecule production is generating consistent demand from CDMOs with mammalian bioreactor capacity. Strategic facility transfers from pharma to CDMO are creating revenue streams that did not exist under the traditional outsourcing model. These deals transfer existing infrastructure and trained workforces, shortening time to commercial production while expanding CDMO service footprints without greenfield construction timelines.

Market Trends

AI Process Optimization and M&A Consolidation Are Redefining Competitive Hierarchy

Fujifilm Bio CDMO's Bio AI tools achieved 1.4 times higher antibody production than conventional methods, as confirmed in its February 2026 briefing. Oxford Biomedica's machine learning optimization for plasmid ratio studies saved around 100 hours per study, an 80% reduction in time, while increasing product yields, as confirmed by its 2025 Annual Report. These gains directly improve client timelines and CDMO margins, making digital process investment a competitive necessity rather than a differentiator. CDMOs that treat AI as optional are ceding measurable performance advantages to operators that have already embedded it into production workflows. Consolidation through M&A is simultaneously restructuring competitive hierarchy, with facility acquisitions and platform integrations accelerating in 2025 and 2026 as operators build geographic and technical breadth faster than organic growth allows.

Market Competition Overview

The market is moderately consolidated at the top tier and fragments significantly below it. The leading operator generated USD 8.1 Billion in CDMO revenue in 2024. The second-largest generated USD 7 Billion, and the third USD 4.43 Billion, as reported by GEN. That revenue step-down beyond the top two players reflects a scale advantage in biologics infrastructure and client relationships that took years of capital investment to build. The fourth-ranked operator generated USD 3.277 Billion in 2024, growing at 30.3% year-over-year in FY 2025, confirming that disciplined capacity expansion is the primary growth mechanism for operators with strong client pipelines.

Lonza deployed CHF 1.3 Billion (USD 1.6 Billion) in CapEx at 19.6% of sales in 2025, a reinvestment rate that mid-size competitors cannot match without sacrificing margins or taking on debt. Technology differentiation is becoming the second axis of competition alongside scale. The Novo Holdings acquisition of Catalent raised client neutrality questions that independent CDMOs are actively exploiting. Pharma companies competing with Novo products may redirect manufacturing programs to operators outside that ownership structure, creating a client acquisition dynamic that will play out over the next several years.

Company Profiles

Lonza is the global revenue leader in pharmaceutical CDMO services, generating USD 8.14 Billion in CDMO revenue in 2024. Its strategic advantage rests on a fully integrated biologics and small molecule platform spanning mammalian cell culture, bioconjugates, and drug product. CHF 1.3 Billion (USD 1.6 Billion) in CapEx deployed in 2025 reinforces a competitive position that rivals would require a decade to replicate.

Samsung Biologics operates as a pure-play biologics CDMO. As reported in its January 2026 financial results, FY 2025 revenue reached KRW 4,557 Billion, up 30.3% year-over-year, with operating profit of KRW 2,069.2 Billion, up 56.6%. Cumulative contract value exceeded USD 21 Billion with 420 regulatory approvals by end of 2025. Its acquisition of the GSK Rockville facility in March 2026, adding approximately 60,000L capacity, established its first U.S. manufacturing presence and positions it to capture biosimilar and biologics contracts from sponsors prioritizing North American supply chains.

Key Players

- Lonza Group

- Catalent

- Thermo Fisher Scientific

- Samsung Biologics

- WuXi AppTec

- WuXi Biologics

- Recipharm

- Boehringer Ingelheim BioXcellence

- Siegfried Holding

- Almac Group

- PCI Pharma Services

- Fareva

- Patheon

- Cambrex

- CordenPharma

- Piramal Pharma Solutions

- Jubilant Biosys

- Jubilant HollisterStier

- Curia

- AGC Biologics

Supply Chain and Value Chain Analysis

The Pharmaceutical CDMO 2.0 value chain flows from raw material and starting material suppliers through API development, into finished-dosage production, analytical testing, packaging, and finally to the pharmaceutical sponsor for commercial distribution. API manufacturing and biologics drug substance steps represent the highest technical complexity and the greatest revenue concentration, confirmed by the 63.8% service revenue share held by API Development and Manufacturing. Lonza's Integrated Biologics platform delivered +32.2% CER sales growth in FY 2025, with the Vacaville site contributing approximately CHF 0.6 Billion (USD 0.8 Billion), confirming where operating leverage concentrates in the chain.

The supply chain faces structural pressure at the raw material layer. BIOSECURE Act compliance timelines are forcing qualification of alternative suppliers without interrupting active manufacturing programs. CDMOs with pre-established, geographically diversified supply relationships hold a meaningful operational advantage over those rebuilding from a single-source position. Packaging and logistics, while lower in per-unit margin, generates client stickiness across the full commercial lifecycle. CDMOs that control multiple chain stages reduce vendor management complexity for sponsors and capture more revenue per program, which explains why the End-to-End Integrated business model commands the strongest commercial position across the sector.

Regulatory Landscape

The Pharmaceutical CDMO 2.0 market operates under the U.S. FDA, European Medicines Agency, and regional health authorities, each imposing distinct requirements for facility qualification, process validation, and batch release. CDMOs operating across multiple geographies must maintain compliance with all applicable frameworks simultaneously. The BIOSECURE Act, enacted in late 2025, is the most consequential regulatory development for CDMO supply chains in this forecast period. Rebuilding qualified supplier networks while maintaining uninterrupted manufacturing creates a dual operational challenge that carries real program delay risk if not managed proactively from 2026 onward.

The FDA has intensified its oversight of advanced therapies, increasing 483 observations and Warning Letters alongside heightened scrutiny of quality agreements. SK pharmteco committed USD 100 Million in March 2026 to its viral vector business partly to meet regulatory expectations attached to gene therapy manufacturing at commercial scale. Operators that do not match this level of compliance investment will find themselves excluded from the highest-value program categories where regulatory validation is a non-negotiable entry requirement. Regulation in this market functions as a commercial filter. Samsung Biologics' 420 cumulative regulatory approvals by end 2025 represent an asset that clients use as a primary vendor selection criterion, making compliance investment a direct revenue enabler.

Investment and White Space Analysis

Investment is currently concentrated in biologics manufacturing capacity, U.S. onshoring, and advanced therapy infrastructure. Halo Pharma is executing an over USD 30 Million investment at its Whippany, NJ facility to establish sterile injectable manufacturing, with commercial production expected in H2 2026. LGM Pharma committed a total of USD 15 Million across its Rosenberg, Texas and Colorado Springs facilities for suppositories, semi-solids, liquids, and oral solid doses. This oral solid dose and specialized delivery segment is underserved relative to the attention biologics receives, and its lower capital threshold offers viable entry points for mid-size investors that cannot compete at the multi-billion biologics infrastructure level.

SK pharmteco's USD 100 Million commitment in March 2026 to viral vector manufacturing in Pennsylvania and France highlights the gap between pipeline demand and available commercial-scale capacity for gene therapies. CDMOs and investors that establish compliant viral vector capacity in the 2026 to 2028 window position themselves ahead of the commercialization wave that advanced therapy pipelines will generate in the early 2030s. Asia Pacific represents a regional white space for regulatory-compliant operators: the region is the fastest-growing market globally, yet BIOSECURE Act disruption has created supply chain vacancies that compliant regional CDMOs are positioned to fill.

Recent Developments

- March 2026: ESTEVE CDMO commenced a USD 15.5 Million expansion of its Morton Grove, Illinois small-molecule API facility, including reactor upgrades and supporting systems, scheduled for completion in 2026, following its acquisition of Regis Technologies in July 2025.

- March 2026: LGM Pharma committed an additional USD 9 Million in a second phase to its U.S. facilities in Rosenberg, Texas and Colorado Springs, Colorado, bringing total recent investment to USD 15 Million for expanded capacity in suppositories, semi-solids, liquids, and oral solid doses.

- May 2026: Halo Pharma is executing an over USD 30 Million investment plan at its Whippany, NJ facility to establish sterile injectable manufacturing covering syringes, cartridges, and vials, with commercial production expected in H2 2026, alongside a strategic partnership with Apotex Corp. for U.S. sterile injectable filling capacity.

- October 2025: Adare Pharma Solutions completed a packaging and warehousing expansion at its Pessano facility in Milan, Italy, adding a purpose-built packaging hall, an expanded warehouse, and a high-speed blistering line to strengthen its commercial-stage service offering.

- April 2024: FUJIFILM Biotechnologies announced an additional USD 1.2 Billion investment in its Holly Springs, NC facility, bringing total investment to over USD 3.2 Billion, adding 8 x 20,000L mammalian cell culture bioreactors by 2028 and creating an estimated 1,400 new jobs by 2031.

Report Details

| Report Characteristics |

| Market Value (2025) |

USD 179.6 Billion |

| Market Value (2026) |

USD 203.0 Billion |

| Forecast Revenue (2035) |

USD 593.6 Billion |

| CAGR (2026–2035) |

12.7% |

| Base Year for Estimation |

2025 |

| Historic Period |

2020 to 2024 |

| Forecast Period |

2026 to 2035 |

| Report Coverage |

Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered |

By Service (API Development and Manufacturing, Finished-Dosage Development and Manufacturing, Analytical and Testing Services, Packaging and Logistics), By Molecule Type (Small Molecules, Biologics, Highly Potent APIs), By Development Phase (Phase III, Phase II, Pre-Clinical, Commercial), By End User (Large Pharma, Emerging / Venture-Backed Biotech, Generics / Specialty Pharma, Virtual Pharma and Tech-Bio), By Business Model (End-to-End Integrated, Tech-Enabled CDMOs, On-Demand / POD Manufacturing, Niche-Focused, Sustainability-Driven, Hybrid Partnerships), By Drug Type (Small Molecules, Biologics, Advanced Therapies), By Therapeutic Area (Oncology, Rare / Orphan Diseases, Infectious Diseases, Autoimmune and CNS Disorders) |

| Regional Analysis |

North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape |

Lonza, Samsung Biologics, Thermo Fisher Scientific (Patheon), Catalent (Novo Holdings), WuXi AppTec / WuXi Biologics, Fujifilm Diosynth, Recipharm, AGC Biologics, Piramal Pharma Solutions, Siegfried |

| Customization Scope |

Customization for segments and region or country level will be provided. Additional customization can be done based on requirements. |

| Purchase Options |

Three license options: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |

Frequently Asked Questions

What is the biggest investment opportunity in Pharmaceutical CDMO 2.0 Market ?

▾ The strongest near-term opportunities lie in U.S.-based sterile injectable manufacturing, viral vector gene therapy capacity, and regulatory-compliant Asia Pacific facilities. SK pharmteco committed USD 100 Million to viral vector manufacturing in March 2026, and Halo Pharma is investing over USD 30 Million in sterile injectables, reflecting where commercial returns are expected to concentrate through 2030.

Who are the top companies in Pharmaceutical CDMO 2.0 Market ?

▾ Lonza leads with USD 8.1 Billion in CDMO revenue in 2024, followed by Thermo Fisher Scientific (Patheon) at USD 7 Billion, Catalent (Novo Holdings) at USD 4.4 Billion, and Samsung Biologics at USD 3.277 Billion, as reported by GEN. Other major operators include WuXi AppTec, Fujifilm Diosynth, Recipharm, AGC Biologics, Piramal Pharma Solutions, and Siegfried.

Which segment is growing fastest in Pharmaceutical CDMO 2.0 Market and why?

▾ Biologics is the fastest-growing molecule type, with Samsung Biologics delivering FY 2025 revenue growth of 30.3% year-over-year and Lonza's Integrated Biologics platform achieving +32.2% CER growth. The shift of drug pipelines toward monoclonal antibodies, biosimilars, and advanced therapies is driving pharma sponsors to outsource biologics manufacturing to operators with validated large-scale bioreactor capacity.

Which region is growing fastest in Pharmaceutical CDMO 2.0 Market and why?

▾ Asia Pacific is the fastest-growing region, supported by expanding biomanufacturing infrastructure, lower operational costs, and a growing base of local biotech companies. North America holds the largest share at 42.0%, but the U.S. market grows at a slower CAGR of 11.5%, confirming that incremental volume growth is increasingly Asia Pacific-driven.

What is the biggest challenge holding Pharmaceutical CDMO 2.0 Market back?

▾ BIOSECURE Act compliance timelines, enacted in late 2025, and heightened FDA scrutiny including increased 483 observations and Warning Letters are the two primary near-term challenges. Both raise operating costs and create program delay risks, with disproportionate impact on CDMOs dependent on overseas suppliers or manufacturing advanced therapies without robust quality management infrastructure.