What is the Photo-Catalytic Chemistry Market Size?

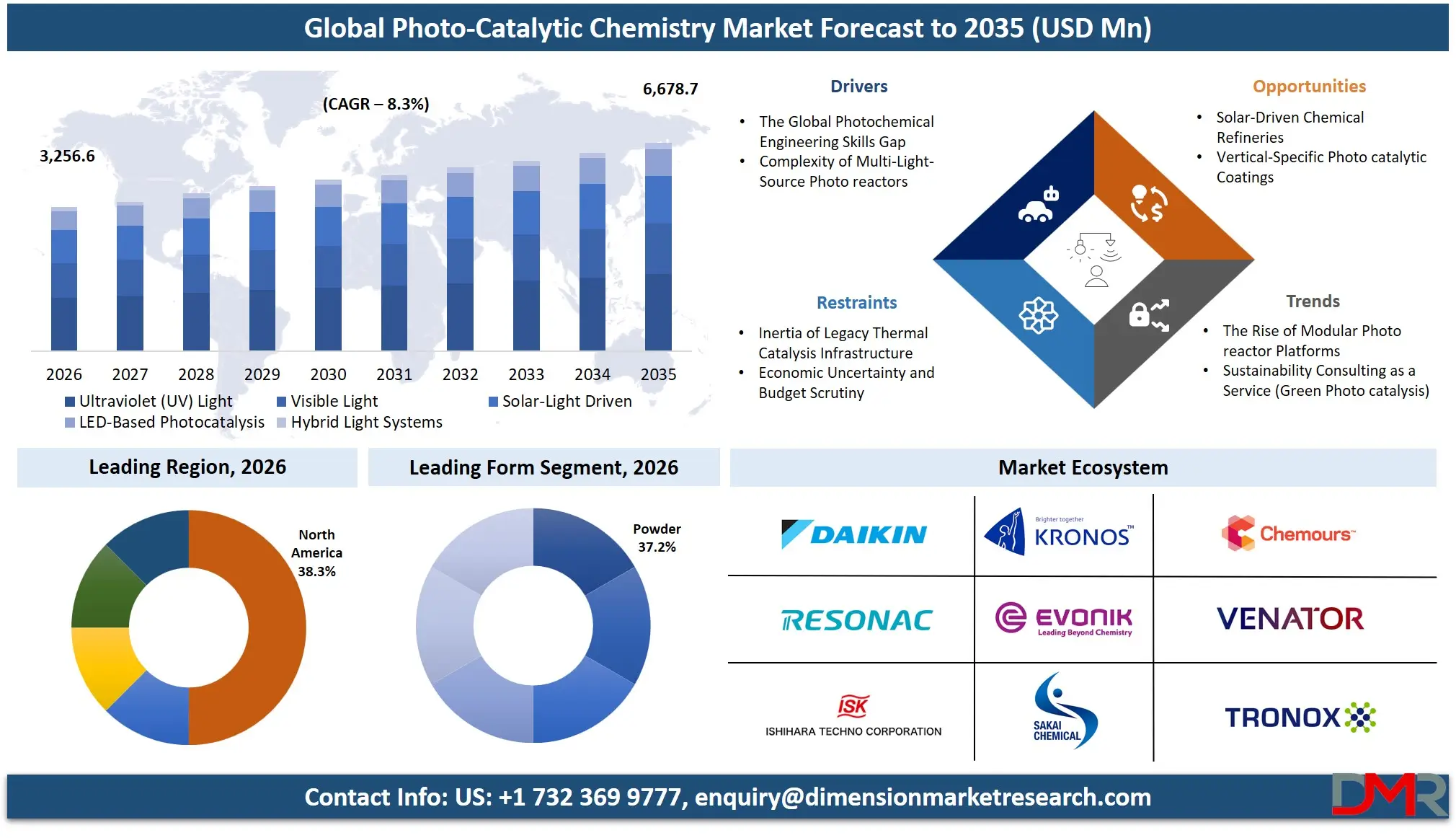

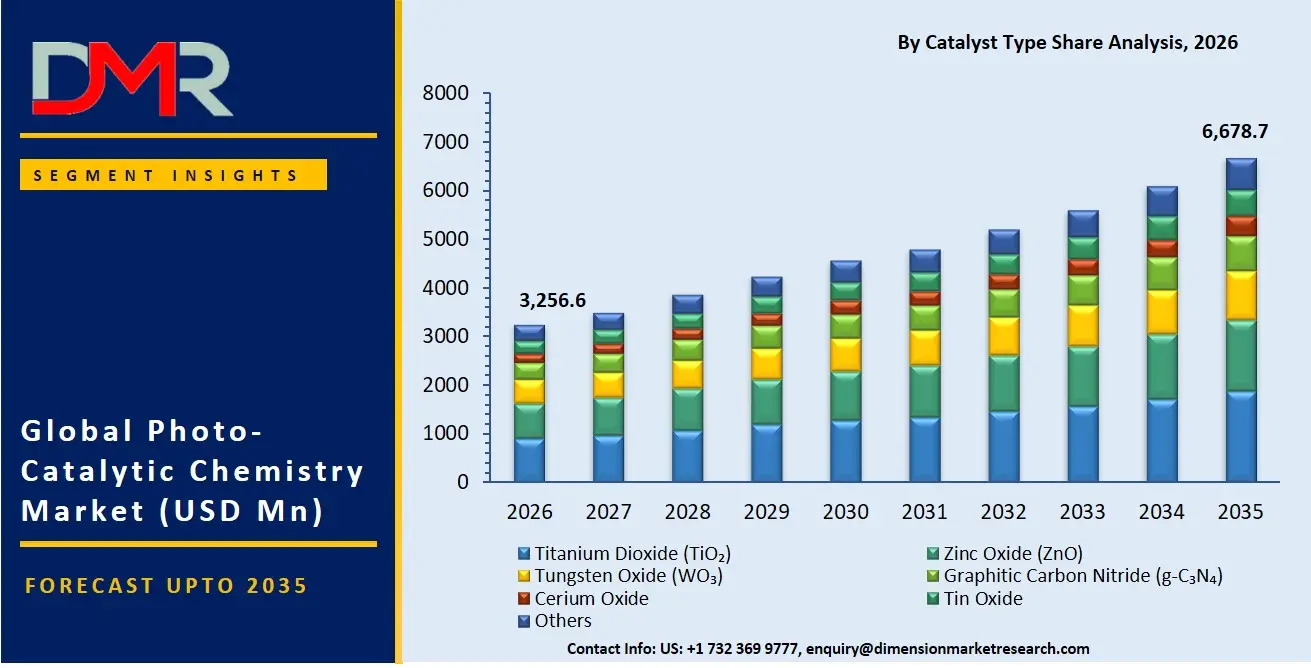

The Global Photo-Catalytic Chemistry Market is expected to reach a value of USD 3,256.6 million in 2026, and it is further anticipated to reach USD 6,678.7 million by 2035, growing at a CAGR of 8.3% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The market of photo-catalytic chemistry is consistently gaining momentum owing to a rapid transition by industries towards light-based chemical reactions rather than energy-demanding thermal catalysis. The market includes specific catalysts such as TiO₂, ZnO, g-C₃N₄, chemical reaction engineering, photoreactor design, and surface coating solutions to help businesses harness the power of UV, visible, or even sunlight to conduct chemical reactions.

There is an urgent requirement to develop specific photocatalytic solutions for decentralized water purification, green hydrogen fuel production, and self-cleaning construction materials. Municipalities and industries represent the largest customer base for photocatalysis applications, with TiO₂ catalysts and UV lights representing the preferred choice because of their efficiency and affordability. The environmental & water treatment industry, chemicals sector, and energy & utilities sector represent the major stakeholders as they require robust and efficient photocatalytic solutions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

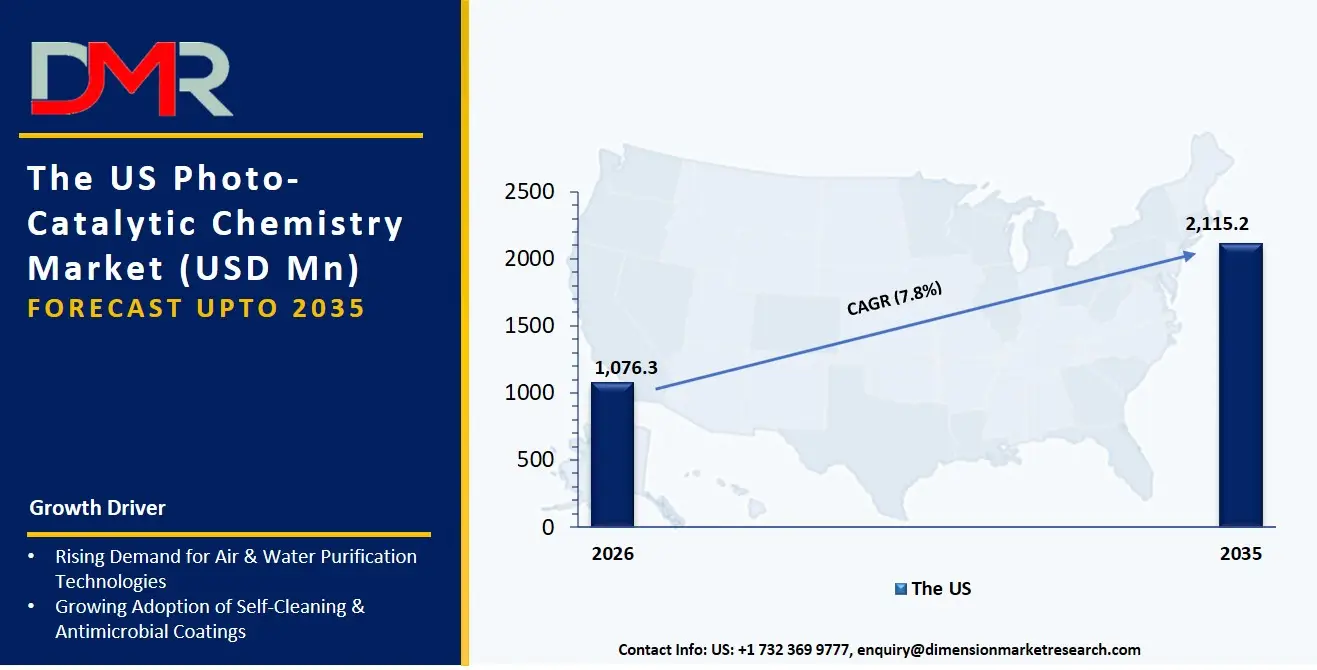

The US Photo-Catalytic Chemistry Market

The US Photo-Catalytic Chemistry Market is projected to reach USD 1,076.3 million in 2026 at a compound annual growth rate of 7.8% over its forecast period, culminating in a value of USD 2,115.2 million by 2035.

Despite all changes and developments that are being observed in the field, the United States remains the biggest and most advanced market in the industry because of the ongoing water treatment requirements set by the EPA, as well as an increasing number of deadlines for discharging industrial contaminants into wastewater streams. The market has always been characterized by the increased demand for environmental remediation reactions, as there is an attempt to decompose PFAS and pharmaceutical contaminants found in wastewater effluent. In addition, an increase in LED-Based Photocatalysis usage in air cleaning systems leads to another need for Thin Film & Coatings applications.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Europe Photo-Catalytic Chemistry Market

The Europe Photo-Catalytic Chemistry Market is estimated to be valued at USD 940.5 million in 2026 and is further anticipated to reach USD 1,892.1 million by 2035 at a CAGR of 8.1%. EU initiatives, such as the EU Green deal, the zero pollution action plan, and the new drinking water directive, play an influential role in the European market and create a need for Water Splitting & Hydrogen Generation and CO2 Reduction technologies to be installed. Another rapidly growing sector in Europe is Solar-Light Driven photocatalysis, as chemical and petrochemical industries from Germany and France are seeking ways of decarbonizing their businesses while continuing with chemical production. Moreover, consortia, like Solar-Driven Chemistry, have put forward the challenge for catalyst manufacturers to design and manufacture dedicated Hybrid Light Systems to guarantee maximum photon efficiency.

The Japan Photo-Catalytic Chemistry Market

The Japan Photo-Catalytic Chemistry Market is projected to be valued at USD 275.4 million in 2026. It is further expected to witness robust growth, holding USD 540.1 million in 2035 at a CAGR of 7.8%. In the Japanese market, the corporate push towards GX stems from the issues of energy import dependence and age-related depreciation of the existing infrastructure. Water splitting & hydrogen generation and self-cleaning surfaces represent a significant portion of the budget allocation as big builders and chemical companies move from high-temperature thermal systems to ambient photocatalysis. Additionally, there is a necessity for close integration into local supply chains to connect the traditional approach of using UV lamps with LED-Based Photocatalysis, thus creating an additional niche in photoreactor retrofitting and flow chemistry automation.

Key Takeaways

- Market Size & Forecast: The global photo-catalytic chemistry market size is estimated to grow to USD 3,256.6 million by 2026 and reach USD 6,678.7 million by 2035, driven by the increasing environmental regulatory requirements and the requirement for the complete substitution of high-energy catalysis reactions.

- Growth Rate & Outlook: In terms of growth rate, the global photo-catalytic chemistry market is expected to grow at a CAGR of 8.3% during the forecast period due to the lack of skilled photochemical engineers and the complex process of controlling photon efficiency and quantum yield in photoreactor operations.

- Primary Growth Drivers: Some important factors driving the global photo-catalytic chemistry market growth are the transition from using thermocatalysts to photo-catalysts to save money on energy bills, the requirement of consulting services in oxidation reactions and organic synthesis reactions, and avoiding toxic by-product production.

- Key Market Trends: Major trends are the introduction of photocatalyst formulation that is specific to industries (for example, anti-fouling agents for marine applications or air sterilizers in hospitals), AI-based tuning in LED-based photo-catalysis process, and CO₂ conversion consulting, among others.

- By Catalyst Type Analysis: Titanium Dioxide (TiO₂) models are expected to dominate industrial discussions because of their affordability and durability. However, there will be a growing need for g-C₃N₄ catalysts in visible light-based systems, where solar energy is directly linked to continuous chemical synthesis on-site.

- By Application Analysis: Water & Wastewater Treatment and Air Purification will become the two most profitable applications owing to strict discharge standards. Hydrogen Production will record the highest growth rate because of the availability of industrial Internet of Things data about electrolyzers, necessitating catalyst durability assessment and membrane-embedded photoreactor design.

- Regional Leadership: North America will lead this market by accounting for 39.3% of market share in 2026. This is mainly because of the region's highly developed environmental laws and its broad industrial footprint leveraging photocatalytic technology to the maximum extent possible.

What is the Photo-Catalytic Chemistry?

Photo-Catalytic Chemistry is a subset of the specialised catalyst formulation, reaction engineering and photoreactor integration services provided by third party catalyst experts, materials suppliers and R&D consultancies to help organisations from the initial stages of photocatalysis through to the final integration of a photoreactor. These services are different from the supply of the catalyst itself, and are related to the how of the adoption of photocatalysis. This includes Reaction Type (Oxidation vs. Reduction vs. Water Splitting) consulting to develop a strategic approach, Form optimization (Powder vs. Thin Films vs. Nanoparticles) to make it possible to physically immobilization of the catalyst without loss of activity, and Light Source integration (UV, visible, solar photons) to ensure efficient interaction of light with the catalyst surface. Over 70% of industrial photocatalytic reactors operate at sub-optimal quantum efficiency, and professional engineering services are required to achieve photon utilization, mass transfer and longevity, rather than laboratory complexity, and to make photocatalysis investments count in terms of operational savings.

Use Cases

- PFAS Degradation in Municipal Water: Under UV-LED irradiation, water utilities can utilize Environmental Remediation Reactions services to break down perfluorinated compounds in drinking water and ensure compliance in real time with EPA limits, thereby eliminating the need to use expensive alternative methods.

- Solar Hydrogen Generation in Refineries: Energy companies are employing Water Splitting & Hydrogen Generation and Thin Films & Coatings services to coat large-area photoreactors with g-C₃N₄ for the generation of green hydrogen for desulfurization processes.

- Self-Cleaning Facade Deployment in Construction: Self-Cleaning Surfaces consulting is used in the construction industry to spray TiO₂ nanoparticles onto building facades, allowing them to react passively with the NOₓ present in the atmosphere and soot, which will not damage the surface.

- Pharmaceutical Continuous Manufacturing: Organic Synthesis Reactions and LED-Based Photocatalysis services help global pharma manufacturers to replace batch thermochemical steps with continuous-flow photoreactors which facilitates safe and rapid synthesis of APIs under ambient condition.

How AI is Transforming the Photo-Catalytic Chemistry Market

AI is revolutionizing photo-catalytic chemistry by enabling the discovery of catalysts at a faster speed and improving the efficiency of operating photoreactors. For Catalyst type selection, AI-based high-throughput screening technologies can automatically predict the properties of novel doped TiO₂ or g-C₃N₄ formulations, significantly reducing the amount of manual experimentation needed. Meanwhile, the AI-powered features in Reaction Type optimization enable operators to more effectively manage reaction pathways and identify undesired reaction pathways, calculate the optimum light intensity, and recommend pH adjustments to enhance the quantum yield.

Projects on governance and process transformation are also focused on AI. Light Source integration includes intelligent photon flux monitoring agents which constantly monitor UV-LED degradation and fouling on Thin Films, and which will detect hotspots and recommend cleaning cycles to maintain systems within ISO 10678 (Photocatalytic activity standards). Additionally, the AI assistant capabilities can complement Chemical Synthesis consulting by modelling the chemical reactions and simulating the performance of a scaled photoreactor, providing a visual of the improvement in yield before investing in capital equipment.

Market Dynamics

Key Drivers in the Global Photo-Catalytic Chemistry Market

The Global Photochemical Engineering Skills Gap

A global challenge is the recruitment of qualified chemists and chemical engineers with expertise in photocatalytic reactor design, light distribution modeling, catalyst immobilization and measurement of photon flux. These skills are needed more quickly than the number of trained talents, and so there is a structural labor market deficit. This is leading to a shift in the way companies are using photocatalytic process design services; they are no longer relying on their own R&D efforts. They can help with catalyst selection, sizing of the photoreactor, integration of light sources and troubleshooting of continuous operations. Delegating these tasks enables companies to advance green chemistry efforts and reduce the likelihood of facing late project delays because of a lack of their own photochemical engineering capabilities.

Complexity of Multi-Light-Source Photoreactors

The simultaneous use of multiple arrays of UV, visible and LED light is emerging as a growing trend for industrial-scale photoreactors to drive multiple catalyst bands for multi-step reactions. But, controlling these systems is very complicated. There is a need for integrating photon flux distribution, cooling, wavelength switching and reaction kinetics over several zones in the same organization. This complexity may cause inefficiencies, thermal runaway, and unnecessary energy expenditure without the guidance of experts. Therefore, there is an increasing need in Integration & Optimization services (in photocatalysis context) which are able to help enterprises to work in such environment.

Restraints in the Global Photo-Catalytic Chemistry Market

Inertia of Legacy Thermal Catalysis Infrastructure

In most chemical plants the heat reactors are still operated in a fixed-bed, which was developed over decades and is quite optimized for the high-temperature processes. Although photocatalysis offers potential energy savings, these legacy systems are a major barrier to change in the most mild conditions. Replacing the large scale steam-heated reformers with LED-based photoreactors can be expensive and risky. Extensive validation is needed for catalyst migrations that include immobilization of nanoparticles on new supports. The fear of business interruption, deactivation of the catalyst and unexpected scale up costs are the concerns of organizations. As a result, technical debt slows down the implementation of photocatalysis and has a tendency to stall or even hinder green chemistry transformation initiatives.

Economic Uncertainty and Budget Scrutiny

Unstable economies and unpredictable energy prices have caused organizations to be more hesitant to spend on photocatalytic retrofitting and R&D consulting. Despite green chemistry transformation being a strategic goal, executives are now under pressure to justify each investment, and they have to demonstrate tangible energy savings and/or CO₂ reduction. The pricing and long-term contract terms for photoreactor integrators are being put to the test. Businesses have changed to projects that are short, equipment-oriented, and provide immediate operational benefits (e.g., reduced chemical oxidant demand). Novel CO₂ Conversion projects and long-term catalyst development efforts are more likely to be postponed until it can be shown that there is a near-term payoff. The transition is driving engineering companies to become more performance-guarantee oriented.

Growth Opportunities in the Global Photo-Catalytic Chemistry Market

Solar-Driven Chemical Refineries

An important development opportunity lies in the support of organizations to develop large-scale chemical refinery plants driven by Solar energy (Solar Fuel Generation and CO₂ Conversion). Numerous companies have tested the CO₂ photoreduction process on a laboratory scale, but are now seeking integrated systems to work in real intermittent sunlight. The development of these advanced facilities needs special expertise in photoreactor design, in the resistance of the catalyst to thermal cycling, and in the separation of the product. Energy companies can create scalable, passive solar energy ecosystems with the aid of service providers to deliver flue gas CO₂ as a source to generate syngas or formic acid. Specialised consulting and reactor engineering services have high potential demand in this area.

Vertical-Specific Photocatalytic Coatings

The need to integrate both materials science and understanding of particular industries is driving growth for professional services as catalyst suppliers create formulations specific to an industry (e.g., antimicrobial coatings for healthcare HVAC, antifouling coatings for marine vessels, NOₓ-degrading coatings for tunnels). In the health, construction and automotive industries, there are strict requirements for durability and toxicity. Therefore, they must have implementation partners who possess an understanding of photocatalyst technology and industry compliance requirements.

Trends in the Global Photo-Catalytic Chemistry Market

The Rise of Modular Photoreactor Platforms

Modular photoreactor engineering is becoming increasingly adopted in organizations as an alternative to custom-built, one-off systems. Tackling the challenges of independent teams working on photochemistry, thermal control, and analytics, enterprises are building standardized photoreactor skids that allow plug-and-flow photocatalysis in R&D and pilot plants. These platforms allow for a fast switch between Oxidation Reactions and Reduction Reactions with a change of LED modules and catalyst cartridges. In response to this, the photocatalytic engineering service vendors are offering their expert services in the field of modular design, continuous-flow automation, and optimizing the quantum yield.

Sustainability Consulting as a Service

As businesses increasingly strive to meet their ESG targets and reduce energy consumption and chemical waste, environmental sustainability is becoming a crucial factor in photocatalysis decisions. Photocatalytic approaches that improve performance and reduce operational carbon footprints are of interest to businesses now. This has brought about the need for Photon Efficiency Consulting. Professional service providers help organizations choose the best light source (LED rather than UV), to design a catalyst recovery loop, and to eliminate the need for the sacrificial oxidants.

Research Scope and Analysis

The Global Photo-Catalytic Chemistry Market is segmented by catalyst type, reaction type, light source, form, application, and end-use industry. Titanium Dioxide, Oxidation Reactions, UV Light, Powder formulations, Water & Wastewater Treatment, and Environmental & Water Treatment dominate due to efficiency, commercial maturity, environmental regulations, and sustainability-driven industrial adoption.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Catalyst Type Analysis

Titanium Dioxide (TiO₂) is the poised to be the most prevalent type of catalyst, because it is chemically stable, cost effective, highly efficient in photocatalytic reaction, and has a high oxidation capability when it comes to UV exposure. It is used in various applications such as water treatment, air treatment, antimicrobial coatings and self-cleaning surfaces. Large cosmetic companies persist in developing new formulations of TiO₂ with enhanced activity and durability in the visible light range. The high commercial maturity, wide industrial acceptance and large-scale production of TiO₂ make it the leader in visible-light applications, while Zinc Oxide and Graphitic Carbon Nitride are catching up. It has a wide range of applications in construction materials, coatings, and environmental remediation systems, reinforcing its leading global footprint in various industries.

By Reaction Type Analysis

Oxidation Reactions are expected to be dominant in the reaction type segment due to their wide application in environmental remediation, wastewater treatment, air purification and pollutant degradation. In the photocatalytic oxidation processes, the VOCs, industrial contaminants, dyes, bacteria and harmful gases are destroyed by the formation of ROS under the action of light. Due to the stringent environmental regulations and sustainability goals, industries and municipalities are increasingly turning to oxidation based photocatalysis. Water Splitting & Hydrogen Generation and CO₂ Reduction are growing rapidly, especially in renewable energy applications, but where there is successful commercial application, proven efficiency and broad application in industrial cleaning and purification applications worldwide, oxidation reactions continue to lead the way.

By Light Source Analysis

UV Light is expected to be the largest light source market due to the activation of most commercially available photocatalysts, particularly Titanium Dioxide, under this wavelength. With their proven efficiency and operational reliability, UV systems are widely used in industrial wastewater treatment, air disinfection, air sterilization and self cleaning. Large-scale implementation due to established UV lamp infrastructure and reduced technological complexity. But, the technology of Visible Light and Solar-Light Driven is becoming popular as industries look for energy efficient and sustainable solutions. Despite this change, UV technology remains the leader in the market for the reasons of strong commercial maturity, research and validation, and as it is widely used in all environmental and industrial photocatalytic operations worldwide.

By Form Analysis

The powder form is more predominant in the market since it has a higher surface area, greater catalytic activity, ease of synthesis and flexibility in its industrial processing applications. The photocatalysts are widely used in wastewater treatment plants, chemical synthesis processes, air purification processes and research labs in virtue of their good dispersion and reaction efficiency properties when in the form of powder. Powder formulations are preferred by manufacturers because they are scalable, cost effective and customizable for catalyst engineering. Although the increase in demand is higher for Nanoparticles and Thin Films & Coatings in advanced applications like self-cleaning surfaces and antimicrobial materials, powders are still on the rise, as they have an extensive industrial compatibility, they are easy to use and are widely applied in large-scale environmental remediation processes globally.

By Application Analysis

The Water & Wastewater Treatment segment is anticipated to hold the largest share in the application segment as the global concerns about industrial pollution, scarcity of water and strict environmental regulations are increasing. Wastewater treatment using photocatalytic technologies is effective in the sustainable oxidation of organic compounds, pathogens, heavy metals and toxic compounds. Photocatalytic treatment systems are being used by municipal authorities and industries to improve water quality and to decrease the amount of chemicals used. The areas of Hydrogen Production and CO₂ Conversion are also on the rise, with levels of clean energy investment increasing, while Water Treatment is the largest application due to the need for water in real time, the use of this product in the commercial market, and the investments of infrastructures in sustainable technologies for water purification in developed and developing countries worldwide.

By End-Use Industry Analysis

The end-use industry segment is projected to be dominated by Environmental & Water Treatment because of increasing pollution concerns across industries and the increasing regulatory pressure in wastewater discharge. Increased re-use of water, the removal of hazardous substances and a decrease in environmental harm are the goals for which photocatalytic systems are being introduced into the water industry and government. Photocatalytic oxidation is used in a wide range of applications in the sector such as treatment of municipal wastewater, management of industrial effluents and air purification. In addition, there are increasing cases of adoption of green chemistry initiatives and hydrogen generation in the Chemicals & Petrochemicals, and Energy & Utilities sectors. But environmental treatment is leading the way due to the pressing need for sustainable solutions around the world, robust policy backing and the ever increasing need for advanced remediation techniques.

The Global Photo-Catalytic Chemistry Market Report is segmented on the basis of the following:

By Catalyst Type

- Titanium Dioxide (TiO₂)

- Zinc Oxide (ZnO)

- Tungsten Oxide (WO₃)

- Graphitic Carbon Nitride (g-C₃N₄)

- Cerium Oxide

- Tin Oxide

- Others

By Reaction Type

- Oxidation Reactions

- Reduction Reactions

- Water Splitting & Hydrogen Generation

- CO₂ Reduction

- Organic Synthesis Reactions

- Polymerization Reactions

- Environmental Remediation Reactions

By Light Source

- Ultraviolet (UV) Light

- Visible Light

- Solar-Light Driven

- LED-Based Photocatalysis

- Hybrid Light Systems

By Form

- Powder

- Suspension/Dispersion

- Thin Films & Coatings

- Nanoparticles

- Pellets & Granules

- Spray Formulations

By Application

- Water & Wastewater Treatment

- Air Purification

- Self-Cleaning Surfaces

- Chemical Synthesis

- Hydrogen Production

- Solar Fuel Generation

- Antimicrobial & Sterilization Solutions

- CO₂ Conversion

- Energy Storage & Conversion

- Industrial Process Catalysis

By End-Use Industry

- Chemicals & Petrochemicals

- Environmental & Water Treatment

- Pharmaceuticals

- Energy & Utilities

- Construction & Infrastructure

- Automotive

- Electronics & Semiconductors

- Healthcare

- Food & Beverage

- Research & Academia

Regional Analysis

Leading Region by Market Share

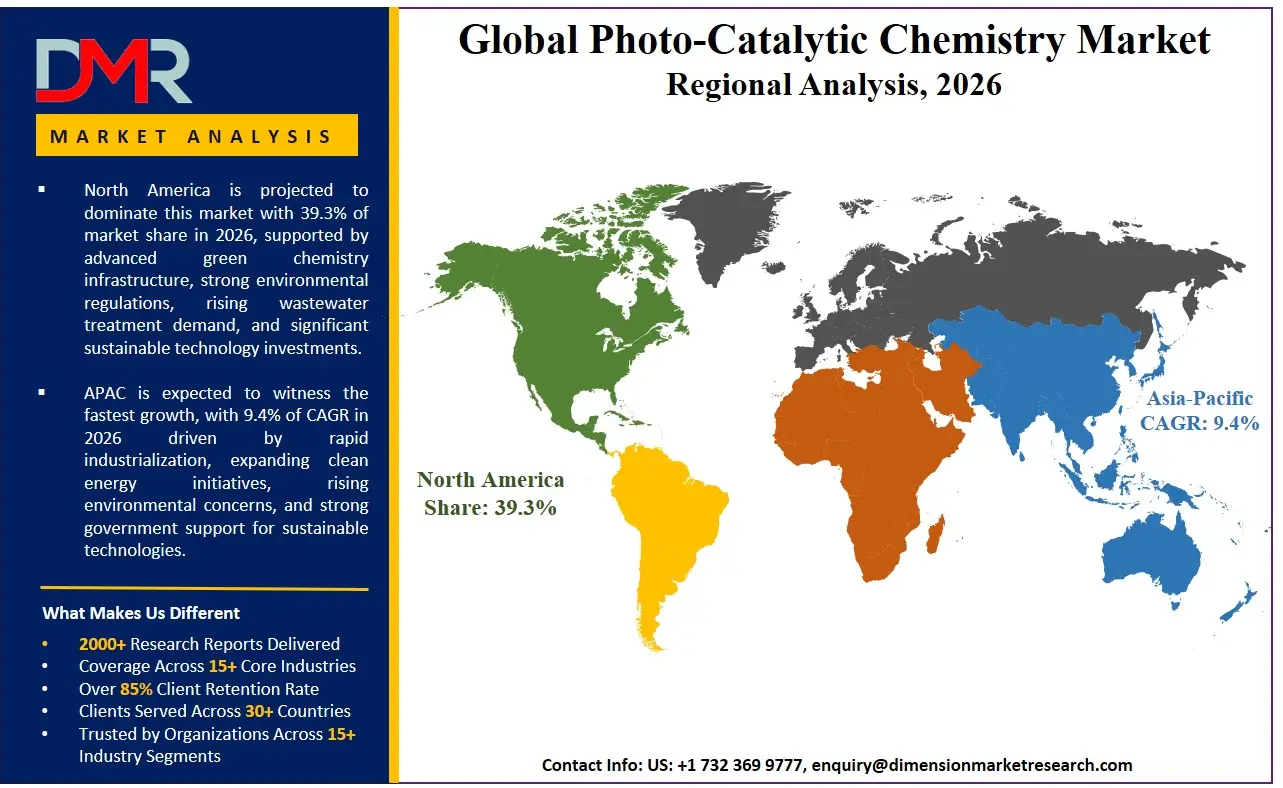

North America is poised to dominate the global photo-catalytic chemistry market, holding 39.3% of the market share by the end of 2026. The United States has the largest percentage because of the unique EPA enforcement timelines for PFAS and microplastics, and driven decarbonization policies of Fortune 500 chemical companies. There is a proven track record of photoreactor integrators, specialty catalyst vendors, and a large pool of photochemical engineers in the region. Demand for Energy Intensive Thermal Process Optimization, Energy Intensive Thermal Process Retirement, Environmental Remediation and Hydrogen Production services continues as enterprise invests in solar fuels and advanced oxidation. Not only that, but a culture of innovation keeps investing in new photo-catalysis ventures that require technical assistance to scale up and bring to regulation.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Regional Market

The Asia-Pacific region is projected to grow at the highest rate in the market of photo-catalytic chemistry, as a result of the aggressive water quality and air pollution programs headed by the government in countries such as India, China, Japan, and Southeast Asian nations. The fast-paced industrial growth, urbanization, and the dynamic expansion of manufacturing are compelling municipal utilities and state agencies to discard inefficient biological treatment. Water Splitting & Hydrogen Generation consulting is highly sought after to assist these large scale energy companies in the transition to green hydrogen. The region also lacks qualified photochemical engineering skills, which necessitates the outsourcing of professional services for implementing the photoreactors, catalysing the processes and optimising the processes, to cover the skills gap, so as to enable faster payback of the photocatalytic investments.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The global photo-catalytic chemistry market is competitive and has diversified to include a range of multinationals including catalyst manufacturers (Evonik, Cristal Global), engineering arms from the large environmental companies (Veolia, Suez) and other specialist photochemical consultancies. Close partnerships with manufacturers of LEDs and photoreactor fabricators will be critical to success, as they will enable key co-selling opportunities and first access to new light source features. Traditional water treatment equipment companies are also consolidating quickly as they seek to revive by buying in the photochemical engineering boutique. Immobilized catalyst coating processes and industry-specific photon distribution models are examples of proprietary intellectual property that are increasingly a key factor in competitive differentiation besides the supply of catalysts.

Some of the prominent players in the Global Photo-Catalytic Chemistry Market are:

- Evonik Industries AG

- Tronox Holdings plc

- KRONOS Worldwide Inc.

- The Chemours Company

- TOTO Ltd.

- TAYCA Corporation

- Ishihara Sangyo Kaisha Ltd.

- SHOWA DENKO K.K. (Resonac Holdings)

- LB Group (Lomon Billions)

- Venator Materials PLC

- Sakai Chemical Industry Co., Ltd.

- Shin-Etsu Chemical Co., Ltd.

- Daicel Miraizu Ltd.

- Nippon Soda Co., Ltd.

- Osaka Titanium Technologies Co., Ltd.

- Kilburn Chemicals Limited

- Daikin Industries Ltd.

- Beijing DK Nano Technology Co., Ltd.

- Nanoptek Corporation

- Catalysts & Chemicals Industries Co., Ltd.

- Other Key Players

Recent Developments

- January 2026: Evonik announced a significant expansion of the Photocatalysis Innovation Center, a professional engineering project to support clients in Water & Wastewater Treatment, and clients in Hydrogen Production, in deploying its proprietary TiO₂-g-C₃N₄ composites using advanced Thin Films & Coatings expertise.

- November 2025: BASF expanded its partnership with LED-based photoreactor manufacturers and added a dedicated practice called CO₂ Reduction and Hybrid Light Systems to help energy clients with the decarbonization of their flue gas to syngas in accordance with international frameworks for carbon use.

- October 2025: Dürr Group acquired a photocatalytic coating startup to strengthen its self-cleaning surfaces and air purification solutions for sovereign infrastructure projects, supporting public-sector requirements for particulate matter reduction.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 3,256.6 Mn |

| Forecast Value (2035) |

USD 6,678.7 Mn |

| CAGR (2026–2035) |

8.3% |

| The US Market Size (2026) |

USD 1,076.3 Mn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Catalyst Type, By Reaction Type, By Light Source, By Form, By Application, and By End-Use Industry |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Photo-Catalytic Chemistry Market?

▾ The Global Photo-Catalytic Chemistry market is poised to be valued at USD 3,256.6 million in 2026 and is projected to reach USD 6,678.7 million by 2035, driven by the universal need for specialized skills in catalyst deployment, photoreactor engineering, and solar fuel integration.

What is the CAGR of the Global Photo-Catalytic Chemistry Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 8.3% from 2026 to 2035, reflecting the accelerating complexity of industrial photocatalytic processes and the persistent shortage of internal photochemical engineering talent.

What factors are driving the growth of the Global Photo-Catalytic Chemistry Market?

▾ Key drivers include the global photochemical engineering skills gap, the imperative to replace energy-intensive thermal catalysis, the management complexity of multi-light-source photoreactors, and the surge in demand for CO2 Reduction consulting amid evolving carbon capture and utilization mandates.

Which region held the largest share of the Photo-Catalytic Chemistry Market in 2026?

▾ North America (specifically the United States) is poised to hold 39.3% of the market share in 2026, driven by a mature EPA regulatory enforcement ecosystem and aggressive industrial investment in Environmental Remediation Reactions and solar-driven chemical capabilities.

Which region is expected to grow the fastest in the Photo-Catalytic Chemistry Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid water quality and air pollution mandates in India, China, and Japan, where Water Splitting & Hydrogen Generation consulting is critical for transitioning large energy conglomerates to green hydrogen operations.

What are the major trends in the Global Photo-Catalytic Chemistry Market?

▾ Major trends include the integration of LED-Based Photocatalysis into industrial flow chemistry, the rise of photon efficiency (Photon-Efficiency) consulting, the demand for industry-specific photocatalytic coatings, and the focus on Hybrid Light Systems for complex multi-step reactions.

Who are the key players in the Global Photo-Catalytic Chemistry Market?

▾ Key players include global catalyst manufacturers like Evonik, BASF, and Cristal Global, as well as specialized coating providers like TOTO Ltd. and niche photochemical engineering consultancies focused on continuous-flow photoreactors.

How is the Global Photo-Catalytic Chemistry Market segmented?

▾ The market is segmented by Catalyst Type, Light Source, Form, Application, and End-Use Industry.