What is the Global Positron Emission Tomography Market Size?

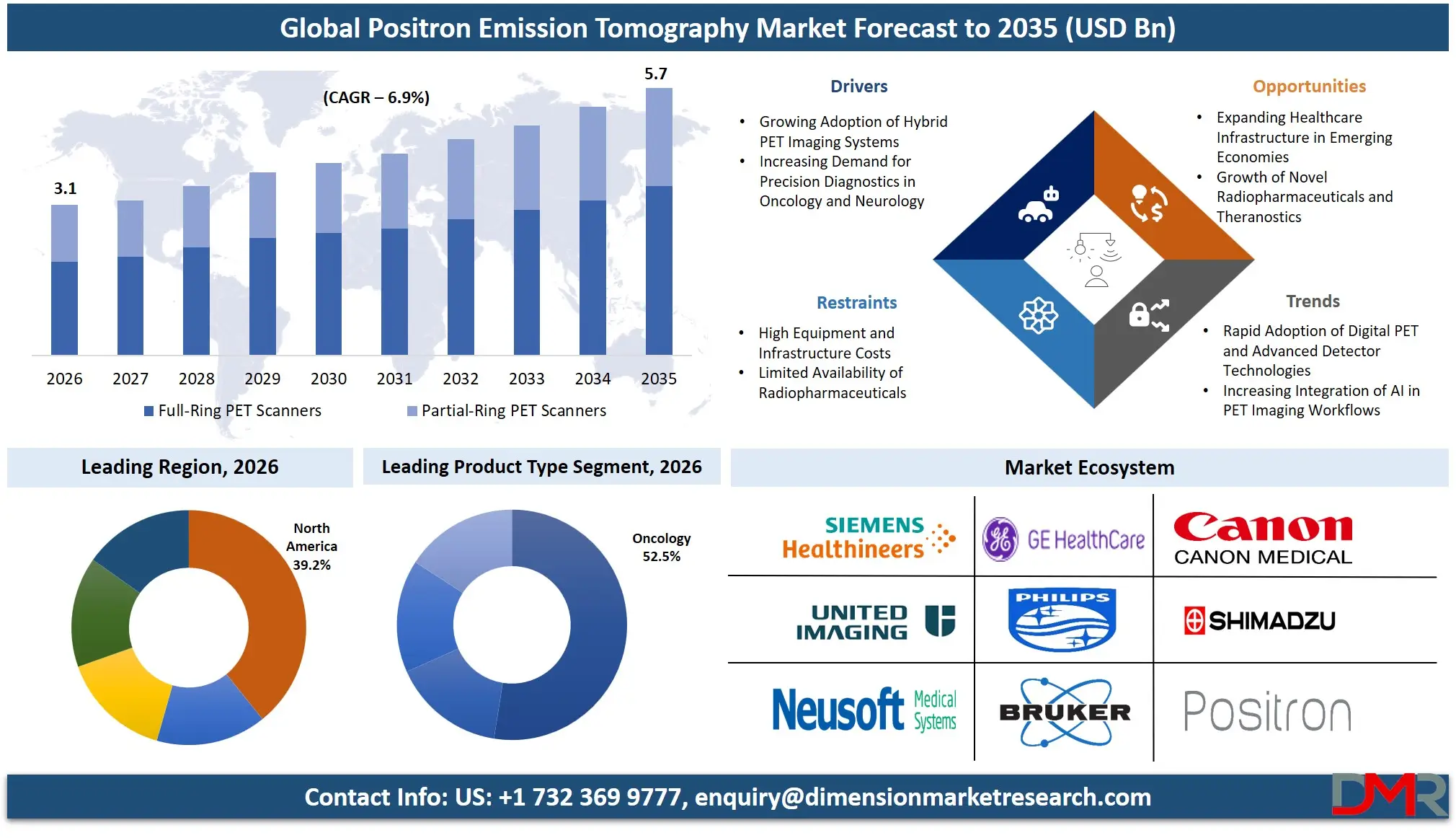

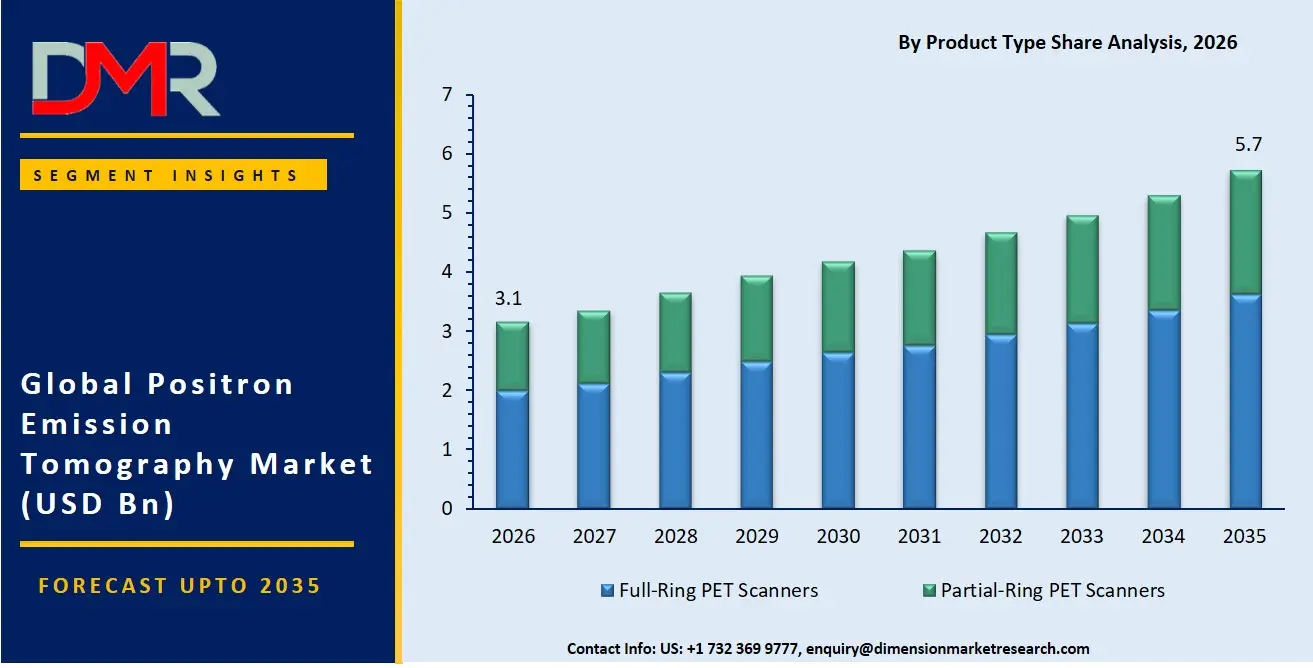

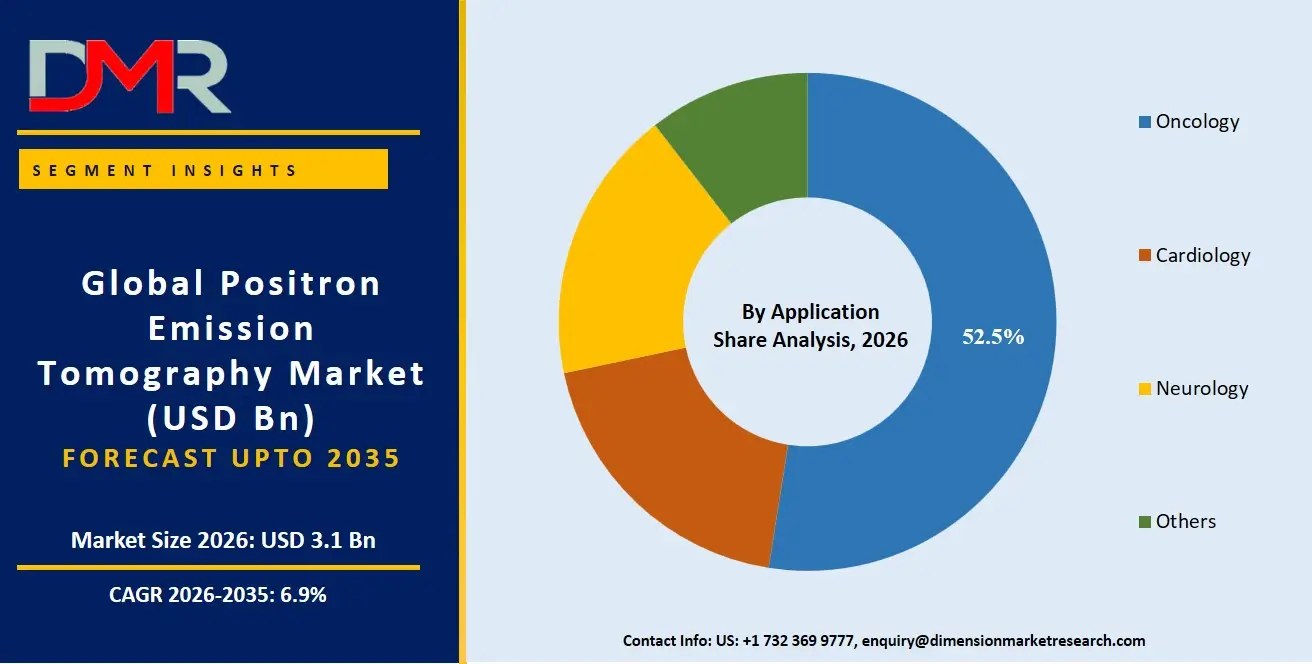

The Global Positron Emission Tomography Market size is estimated at USD 3.1 billion in 2026 and is projected to reach USD 5.7 billion by 2035, exhibiting a CAGR of 6.9% during the forecast period, driven by the rising use of hybrid imaging systems, accelerated regulatory approvals for novel radiopharmaceuticals, expanding cyclotron networks for tracer production, and increasing adoption of PET imaging across oncology, neurology, and cardiology applications.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

There has been growth in the positron emission tomography market due to increased use of sophisticated detectors in oncology and neurology applications, greater regulatory incentives that decrease development time for novel radiopharmaceuticals and help secure orphan drug designation for radiological targeting agents, and additional funding in the area of automatic reconstruction and correction of attenuation for PET images.

Other factors contributing to growth in this market include new innovations in digital silicon photomultiplier detectors, TOF-PET using enhanced spatial resolution, automated high throughput synthesis of tracers, high throughput radiopharmaceutical manufacturing platforms, and better collaborations in rare disease imaging research. Digitalization of oncology and neurology departments has proven beneficial in helping speed up the diagnostic process while allowing for more efficient management of highly sensitive imaging data, which also entails AI enabled clinical imaging analytics research. Moreover, government initiatives to develop nuclear medicine and ensure isotope supply chains have led to consistent research in PET systems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US Positron Emission Tomography Market

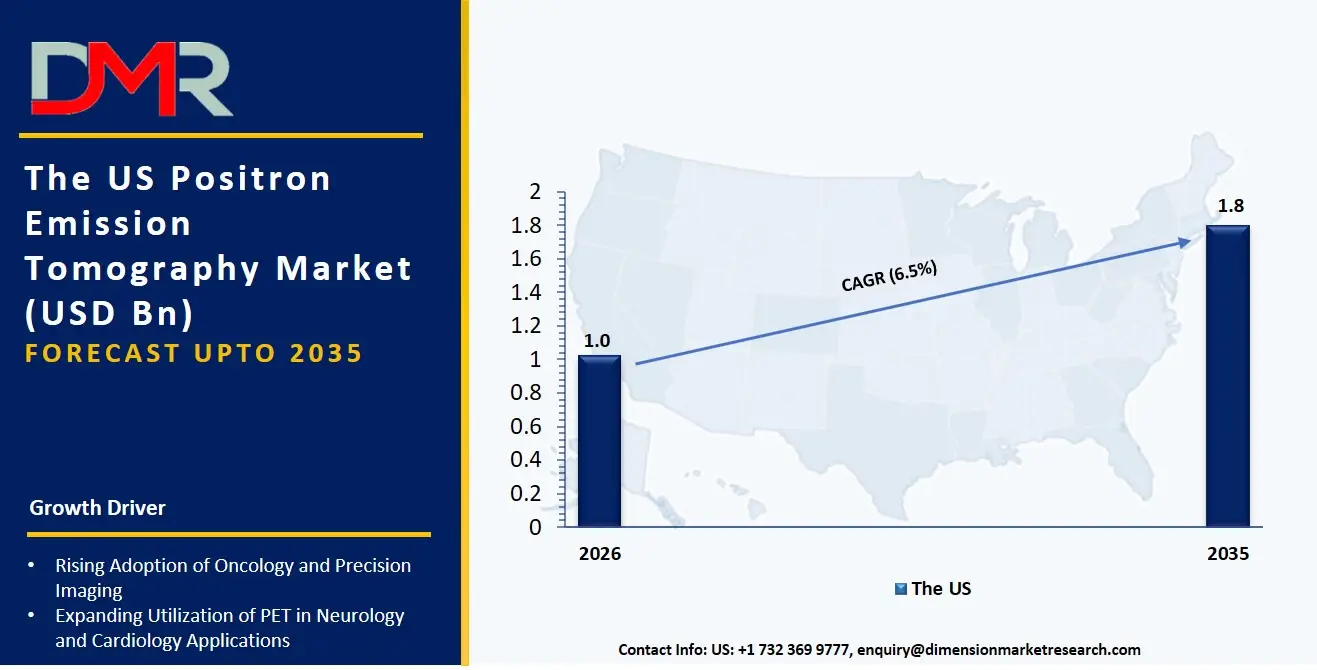

The US Positron Emission Tomography Market is estimated to grow to USD 1.0 billion in 2026 with a compound annual growth rate of 6.5% during the forecast period.

The US market is influenced by significant government-led programs in both the federal and state sectors in favor of personalized molecular imaging, wide PET use due to the FDA's fast-track approvals for radiopharmaceuticals and rare diseases, and efforts at nuclear medicine modernization led by the NIH. These programs encourage the use of advanced tracer development, real-time kinetic modeling, and predictive dosimetry assessment software for PET candidates. Automated PET platform technologies are being rapidly adopted, and the US continues to invest in better collaboration between research labs, advanced preclinical imaging systems, and reliable PET performance assessment tools for tracer platforms. Service providers are also influenced by laws like GLP, GCP, and national molecular imaging data management strategies to offer services that ensure PET data integrity, regulatory compliance, and smooth integration across academic and commercial manufacturing environments.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Europe Positron Emission Tomography Market

The European Positron Emission Tomography Market is estimated to be valued at USD 868.0 million in 2026, witnessing growth at a CAGR of 5.9%, during the forecast period.

Europe is a matured market for positron emission tomography due to various EU policies including European Reference Network for rare diseases, the PRIME program of the EMA, and national policies for promoting radiopharmaceuticals innovation hubs such as those in Germany and France. Countries are also making PET post-authorization monitoring more flexible to align payer and provider demands and enable the sharing of real-world imaging outcomes across borders. The market grows due to new tools like software for tracer development assessment and image analysis systems for PET operations. Use is made easier by teamwork between public and private consortia and shared imaging protocols. Manufacturers have access to technologies such as SiPM-based high-resolution detection, TOF-mediated image quality improvement, and advanced PET workflow management systems, and Europe is at the forefront of the digitisation of safe and efficient PET operations.

Japan Positron Emission Tomography Market

The Japan Positron Emission Tomography Market is projected to be valued at USD 186.2 million in 2026, progressing at a CAGR of 6.7%, during the period spanning from 2026 to 2035.

Japan's PET market is well developed, with advanced radiopharmaceutical production platforms, connected tracer manufacturing management systems, and a wide array of PET analytics software tools. National focus on automation, efficiency, and process integrity is delivered via integrated PET workflow models and smart imaging management systems. Growth opportunities are helped by government measures under the Japan Agency for Medical Research and Development (AMED)'s radioisotope strategy, METI's biomanufacturing initiatives, and continued investment in PET research and development. AI-driven PET imaging research, collaborative analytics for disease-specific imaging studies, and modernized PET production environments all need effective PET software to keep pace with novel tracer synthesis. Higher costs for validating new PET platform technologies and connecting them with existing infrastructure are significant, but there are opportunities for the export of Japanese PET technologies to the Asia-Pacific market.

Key Takeaways

- Market Size & Forecast: The Global Positron Emission Tomography (PET) Market is estimated to be valued at USD 3.1 billion in 2026 and is expected to grow to USD 5.7 billion by 2035.

- Growth Rate & Outlook: The market is expected to witness growth at a compound annual growth rate of 6.9% in the forecast period.

- Primary Growth Drivers: The availability of new digital detector technologies that use SiPM and TOF, the need to speed up regulatory outcomes for novel tracers and improve success rates of targeted molecular imaging, and more government investment in national nuclear medicine infrastructure are key growth drivers.

- Key Market Trends: The real-time profiling of PET tracer stability risks, novel radiopharmaceutical payload handling, and the shift to AI-driven PET reconstruction platforms and automated tracer manufacturing management are key market trends.

- By Application: The oncology segment is expected to take the largest revenue share in 2026.

- By Isotope Type: Fluorine-18 (18F) tracers are expected to take the largest revenue share in 2026 in the PET market.

- By End-User: Hospitals & surgical centers are estimated to take the lead in 2026 with the largest share in the PET market.

- Regional Leadership: North America is estimated to take the lead in 2026 with 39.2% share in the PET market.

What is Positron Emission Tomography?

Positron Emission Tomography (PET) is a term used to refer to a collection of molecular imaging approaches that employ intravenous administration of radio tracers to detect biochemical changes within tissues in a way that enhances the capacity to quantify receptor density, blood flow, and tumor hypoxia before treatment, among other capabilities not seen in conventional anatomical imaging. Examples of PET radiotracers used today include 18F-FDG tracers, 68Ga-somatostatin analogs, 82Rb perfusion agents, and 64Cu-labeled antibodies. The platforms employ technologies ranging from image reconstruction methodologies, automated synthesizers, and workflow management to effectively control for and document patient molecular response and outcomes. In order to optimize PET diagnostics, variability in imaging and protocol for certain conditions, and expand coverage to personalized molecular medicine, the following recommendations will be made.

Use Cases

- Cancer Detection and Treatment Monitoring: PET platforms can provide significant clinical benefits through advanced imaging analytics, quantitative assessment tools, and workflow optimization systems to reduce diagnostic uncertainty and support treatment response evaluation in a timely and efficient manner.

- Long-Term Imaging Asset Management: Long-term data on ongoing PET operational issues, including radioisotope intermittency, supply chain price spikes, or tracer degradation, are studied to better understand imaging performance and to help plan long-term patient care strategies.

- Radiopharmaceutical Production Optimization: Tracer production and quality control are handled through PET platform software in CDMO and corporate settings to support operational efficiency and capacity management for novel radiopharmaceutical workloads.

- Government & Regulated Programs: Faster PET tracer development helps molecular imaging innovation and targeted rare disease programs; government programs, through smart monitoring of national real-world PET outcomes, advance national molecular imaging initiatives and help the adoption of operational standards.

How AI Is Transforming the Global Positron Emission Tomography Market?

Artificial intelligence (AI) is being used progressively more often in PET platforms to improve image reconstruction accuracy, identify diagnostic patterns in imaging datasets, and automatically detect unusual findings in patient scans. It also allows faster imaging analysis because it can handle large-scale image processing and quantitative assessments efficiently. Clinical imaging records are easier to study and help healthcare providers find workflow issues, reduce mistakes, and improve the overall accuracy of PET-based diagnoses. This has resulted in imaging workflows being more cost-effective, quicker, and more efficient than traditional manual interpretation methods.

AI is also strengthening research and development by improving image quality assessment and enabling more accurate capacity planning for PET facilities. It helps providers predict imaging demand, identify possible workflow delays, and monitor the performance of PET networks more effectively. In addition, automation of routine image analysis and performance tracking is reducing operational workload, lowering administrative costs, and improving overall efficiency. This is leading to better financial results and more stable operations across the PET imaging ecosystem.

Market Dynamics

Key Drivers of the Global Positron Emission Tomography Market

Growing Adoption of Hybrid PET Imaging Systems

The industry is experiencing tremendous growth owing to the rising use of hybrid imaging technologies such as PET/CT and PET/MRI in hospitals, imaging centers, and laboratories. Hybrid imaging involves the integration of two imaging techniques to provide healthcare specialists with better diagnostic insights from a single imaging process. Hybrid imaging allows for the detection of various diseases, enables the staging of cancer accurately, and facilitates the planning and monitoring of treatments. Hospitals are purchasing more hybrid PET devices as they are time-saving and efficient, and thus, enable medical practitioners to make quick and well-informed decisions. Technological innovations are constantly improving the performance of hybrid PET imaging systems, and hence, contributing to their increased adoption in the industry.

Increasing Demand for Precision Diagnostics in Oncology and Neurology

The growing prevalence of cancer, neurological disorders, and other illnesses has made it necessary to have advanced diagnostic imaging techniques. This has led to greater popularity of the PET scan. The importance of PET scan lies in oncology, where its application has proved essential in early detection, staging of the illness, assessing response to therapy, and recurrence of the disease. The use of the PET scan in the domain of neurology makes it possible to diagnose different neurodegenerative disorders, such as Alzheimer's disease, epilepsy, Parkinson's disease, among others. In the era of personalized medicine becoming increasingly popular, there has been increased need for highly advanced molecular imaging technology.

Restraints in the Global Positron Emission Tomography Market

High Equipment and Infrastructure Costs

One of the most important aspects that influence the uptake of PET imaging technology is its significant costs. Health organizations have to purchase sophisticated PET machines along with other costly equipment, including radiopharmaceutical facilities, radiation shielding systems, and qualified staff members. In addition, such elements as routine maintenance, software upgrade, and quality control make the use of PET devices rather costly as well. Moreover, radiopharmaceutical manufacturing and delivery increase the expenses related to PET imaging considerably. All these financial factors may become especially hard for small health care facilities and organizations working in developing countries. Therefore, there is little doubt that costs remain one of the main factors restricting the growth of the market.

Limited Availability of Radiopharmaceuticals

The success of PET scanning is contingent upon the availability of radiopharmaceuticals, many of which have very short half-lives and need to be produced, distributed, and administered quickly. This causes logistical problems for medical professionals because of the fact that, in some areas where there is no facility for producing radiopharmaceuticals using a cyclotron, the radiopharmaceuticals cannot be procured readily. Problems in transportation and production might lead to reduced efficiency and availability of PET scanning processes. Many emerging economies suffer from insufficient production and distribution networks due to which they do not enjoy easy access to PET imaging. Moreover, legal regulations pertaining to the manufacture and transportation of radiopharmaceuticals make things more complicated for medical professionals.

Growth Opportunities in the Global Positron Emission Tomography Market

Expanding Healthcare Infrastructure in Emerging Economies

Developing countries have created numerous growth opportunities for the PET industry due to continued investment in healthcare infrastructure development. Emerging nations all over Asia-Pacific, Latin America, the Middle East, and Africa are focusing on enhancing access to cutting-edge diagnosis methods to cope with high incidences of cancer, neurological diseases, and heart diseases. Rising health care expenditure, increasing disease detection awareness, and improved access to specialized healthcare services will aid in adopting PET imaging devices. Healthcare institutions in these countries are focusing on improving their diagnostics capabilities by adding nuclear medicine units due to the increasing number of patients. With continued healthcare infrastructure improvement and enhanced payment models, developing countries are likely to emerge as growth drivers for the PET industry.

Growth of Novel Radiopharmaceuticals and Theranostics

Innovations within the area of novel radiopharmaceuticals and theranostics have opened up exciting possibilities for the use of PET technology in various medical applications. New types of tracers are helping achieve better results by visualizing certain biological markers, and hence improving the diagnosis of various diseases. Theranostics has emerged as an important technique that uses both diagnostic imaging and targeted therapy in providing better healthcare for the patients. The increasing use of novel techniques such as PSMA imaging in prostate cancers, amyloid imaging in neurodegenerative conditions, and many others has helped expand the applications of PET beyond conventional imaging. Continued advances in research and development activities would result in more innovative radiopharmaceuticals and would drive the adoption of advanced PET imaging devices.

Global Positron Emission Tomography Market Trends

Rapid Adoption of Digital PET and Advanced Detector Technologies

There is an emerging trend in the market involving the introduction of digital PET scanners with innovative detectors, which offer superior image quality, higher sensitivity, and shorter scan time. Improvements such as silicon photomultipliers (SiPMs), time-of-flight (TOF) imaging, and new reconstruction algorithms have greatly improved the diagnostic capability of these technologies as compared to their older counterparts. Such improvements enable medical practitioners to detect lesions more efficiently, as well as make imaging processes easier and more accurate. The use of such systems by healthcare facilities is gaining popularity as they provide greater diagnostic confidence and enable precision medicine. With the continued development of high-performance PET systems, the move towards advanced detector technology seems to be the major trend for the future.

Increasing Integration of AI in PET Imaging Workflows

The importance of artificial intelligence as part of the PET imaging process becomes evident as healthcare providers attempt to boost their efficiency, uniformity, and diagnosis accuracy. Various AI-enabled solutions have been implemented to optimize image reconstruction and processing, aid in detecting lesions and analyzing images quantitatively. Such technologies are effective in cutting down the time for interpretation and help providers deal with the rising imaging workload efficiently. AI is also capable of boosting the image quality obtained by performing low-dose scans, thus ensuring that less radiation is involved in diagnosing patients' conditions. Furthermore, there are AI-based workflow optimization solutions available to streamline various processes involved in PET imaging such as scheduling, reporting, and data management. With continuous improvements in AI, its implementation in PET imaging will become even more popular.

Research Scope and Analysis

The Global Positron Emission Tomography (PET) Market is witnessing strong growth driven by rising approvals of novel tracers, expansion into new clinical applications, and increasing demand for targeted molecular imaging. The market is segmented based on product type, detector type, isotope type, application, and end-user.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Product Type Analysis

The Full-Ring PET Scanners segment is likely to continue dominating the market in 2026, accounting for approximately 39.2% of the global PET market share. This is due to its key role in enabling superior sensitivity, volumetric coverage, and quantitative accuracy for oncology and neurology indications, and its usefulness in high-throughput clinical settings where high image quality is required. Within this segment, Time-of-Flight (TOF) full-ring scanners hold the largest share, driven by established clinical presence, long-term real-world evidence, and continued international access programs. The Partial-Ring PET Scanners segment is driven by novel compact designs for organ-specific imaging and lower-cost installations. These systems support ongoing clinical activity and standardized safety management across community hospital settings.

By Detector Type Analysis

The Lutetium Oxyorthosilicate (LSO) detector segment is likely to continue holding the lead in 2026, accounting for approximately 41.5% of the global PET market share, driven by excellent coincidence timing resolution for TOF, high light output, and rapid decay time. This segment reflects the continued need for high-sensitivity, low-noise detectors despite higher material costs. The Lutetium Yttrium Orthosilicate (LYSO) segment is the second-largest, supported by mechanical robustness and lower manufacturing complexity, while the Bismuth Germanate (BGO) segment is also growing, driven by high stopping power for higher-energy isotopes.

By Isotope Type Analysis

The Fluorine-18 (18F) tracers segment is expected to dominate with around 38.5% market share in 2026, driven by broad global reimbursement for 18F-FDG oncology imaging, established nuclear medicine familiarity, and continued expansion into neurology and cardiology programs. 18F-FDG supports long-term patient management plans because of its well-characterized half-life and real-world durability data. The Gallium-68 (68Ga) tracers segment is the fastest-growing, driven by pipeline candidates for neuroendocrine tumors (68Ga-DOTATATE) and prostate cancer (68Ga-PSMA). This segment is seeing strong growth with increasing venture capital investment and orphan drug designations.

By Application Analysis

The Oncology segment is the largest application in 2026, accounting for 52.5% share, driven by widespread use for tumor staging, restaging, treatment response monitoring, and radiotherapy planning. These applications provide molecular characterization of tumors and support systemic and localized cancer management. The Neurology segment is the second-largest, supported by enhanced ability to quantify amyloid, tau, and dopamine transporter density in Alzheimer's and Parkinson's diseases, while Cardiology is the fastest-growing, driven by ultra-high sensitivity for myocardial perfusion and viability assessment.

By End-User Analysis

The Hospitals & Surgical Centers segment is the largest end-user in 2026, accounting for 48.5% share, driven by the need for specialized tracer administration, patient monitoring for adverse events, and multidisciplinary oncology and neurology care. Comprehensive cancer centers and specialized neurology hospitals are adopting PET for direct patient management. Diagnostic Imaging Centers is the second-largest and fastest-growing segment, supported by outpatient demand for cost-effective PET/CT studies, streamlined workflows, and increasing partnerships with radio-pharmacy networks.

The Global Positron Emission Tomography Market Report is segmented based on the following:

By Product Type

- Full-Ring PET Scanners

- Partial-Ring PET Scanners

By Detector Type

- Bismuth Germanate (BGO)

- Lutetium Oxyorthosilicate (LSO)

- Gadolinium Oxyorthosilicate (GSO)

- Lutetium Yttrium Orthosilicate (LYSO)

- Others

By Isotope Type

- Fluorine-18 (18F) Tracers

- Rubidium-82 (82Rb) & Nitrogen-13 (13N) Tracers

- Gallium-68 (68Ga) Tracers

- Copper-64 (64Cu) & Zirconium-89 (89Zr) Tracers

- Other Isotopes

By Application

- Oncology

- Neurology

- Cardiology

- Others

By End-User

- Hospitals & Surgical Centers

- Diagnostic Imaging Centers

- Research & Academic Institutes

- Others

Regional Analysis

Leading Region in the Positron Emission Tomography (PET) Market

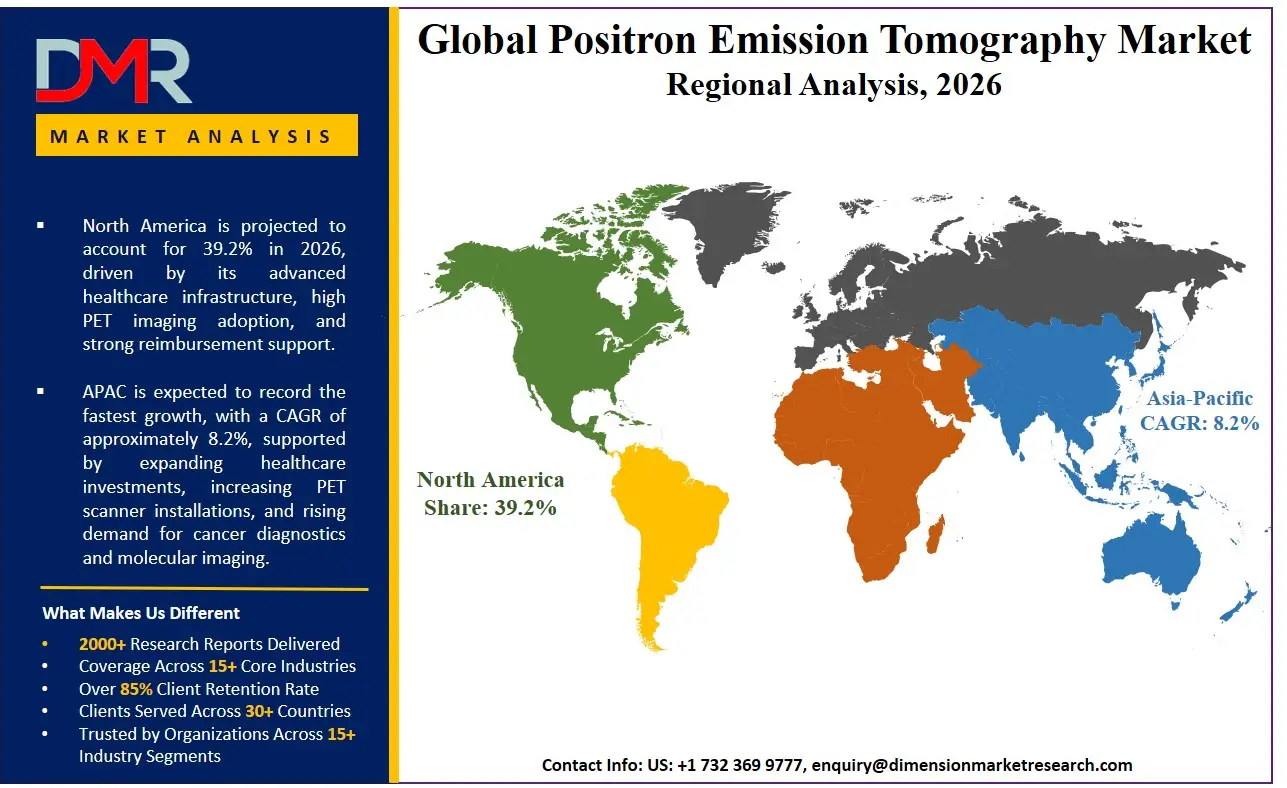

It is projected that North America will take the lead in the global PET market, covering a market share of about 39.2% in the year 2026. The region's dominance is driven by the presence of the world's largest radiopharmaceutical R&D clusters (Boston, San Francisco), rapid clinical adoption of full-ring TOF PET/CT and digital PET/MR systems, strong nuclear medicine modernization spending funded by private and public sources, higher average imaging volumes compared to other regions, a mature supply chain for advanced cyclotron and tracer manufacturing, and the presence of major PET system developers. The widespread adoption of advanced PET reconstruction and automation for oncology, neurology, and cardiology further strengthens North America's leading position. Additionally, ongoing investments in newborn screening programs and cross-system interoperability under the FDA's real-world evidence frameworks further reinforce the region's technology leadership.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Region in the Positron Emission Tomography (PET) Market

Asia-Pacific is the fastest-growing region, supported by strong nuclear medicine infrastructure goals in China, Japan, and India, increasing cancer and neurological disease diagnosis awareness efforts, rising investments in local cyclotron and tracer manufacturing capabilities, and growing adoption of cost-effective generic tracer alternatives. The region benefits from well-established hospital systems for oncology and neurology management, increasing business activity in CROs/CDMOs, and alignment with national molecular imaging protection roadmaps. Countries across the region are actively setting up specialized cancer centers and PET access programs to improve diagnostic efficiency and strengthen imaging data privacy infrastructure. Growing focus on PET research and structured rare disease registries further speed up market expansion. Moreover, increasing government support and corporate oncology commitments are expected to keep growth momentum high.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The global positron emission tomography market is highly competitive, with technological innovation and strategic collaborations shaping the competitive environment. To gain an advantage, companies are focused on developing advanced detector technologies such as digital SiPM PET, time-of-flight (TOF) PET, and total-body PET systems, along with AI-enabled image reconstruction and workflow optimization solutions. There are high barriers to entry due to the substantial investment required for research and development, regulatory clearances, specialized manufacturing capabilities, and the establishment of reliable radiopharmaceutical supply networks.

Strategic approaches to increase market presence include partnerships with radio-pharmacy networks, academic medical centers, and healthcare providers, as well as long-term service agreements with hospitals and government institutions. Companies are also expanding their radiopharmaceutical portfolios and investing in next-generation isotope production technologies, including 64Cu- and 89Zr-based tracers, to strengthen their competitive positions. In addition, continued research into automated tracer synthesis, digital imaging platforms, and advanced molecular imaging applications remains important for meeting evolving clinical and operational requirements.

Some of the prominent players in the Global Positron Emission Tomography Market are:

- Siemens Healthineers AG

- GE HealthCare Technologies Inc.

- Koninklijke Philips N.V.

- Canon Medical Systems Corporation

- Shanghai United Imaging Healthcare Co., Ltd.

- Shimadzu Corporation

- Neusoft Medical Systems Co., Ltd.

- Mediso Medical Imaging Systems Ltd.

- MinFound Medical Systems Co., Ltd.

- Positron Corporation

- Bruker Corporation

- Spectrum Dynamics Medical Ltd.

- CMR Naviscan Corporation

- Cubresa Inc.

- SOFIE Biosciences, Inc.

- Cardinal Health, Inc.

- Lantheus Holdings, Inc.

- Curium Netherlands Holding B.V.

- Eckert & Ziegler SE

- IBA Radiopharma Solutions

- Other Key Players

Recent Developments

- March 2026: Lantheus Holdings, Inc. received U.S. FDA approval for Pylarify TruVu, a new formulation of its PSMA PET imaging agent for prostate cancer. The enhanced formulation increases production capacity by approximately 50%, improves distribution efficiency, and expands access to PET imaging services, particularly in underserved regions.

- January 2026: Siemens Healthineers AG received U.S. FDA clearance for its second-generation Biograph One PET/MR scanner, featuring AI-powered image reconstruction and simultaneous PET/MR imaging capabilities to support oncology, neurology, and theranostics applications, strengthening its molecular imaging portfolio.

- November 2025: GE HealthCare Technologies Inc. expanded the rollout of its FDA-approved Flyrcado (flurpiridaz F 18) cardiac PET radiotracer through a broader adoption agreement with Cardiovascular Associates of America (CVAUSA), supporting increased utilization of PET myocardial perfusion imaging across cardiovascular care networks.

- April 2025: Curium Netherlands Holding B.V. completed the acquisition of Nucleis, a Belgian PET radiopharmaceutical manufacturer, expanding its PET tracer production capacity, strengthening its distribution network across Western Europe, and enhancing its capabilities in oncology, neurology, and cardiology PET imaging.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 15.9 Bn |

| Forecast Value (2035) |

USD 27.6 Bn |

| CAGR (2026–2035) |

6.3% |

| The US Market Size (2026) |

USD 4.6 Bn |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimated Year |

2026 |

| Segments Covered |

By Product Type, By Reinforcement Type, By Resin System, By Application, By End-Use Industry |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Positron Emission Tomography Market?

▾ The Global Positron Emission Tomography Market is estimated to be valued at USD 3.1 billion in 2026 and is expected to reach USD 5.7 billion by the end of 2035.

What is the CAGR of the Global Positron Emission Tomography Market from 2026 to 2035?

▾ The market is growing at a CAGR of 6.9% over the forecasted period.

What factors are driving the growth of the Global Positron Emission Tomography Market?

▾ The market is driven by advances in digital SiPM and TOF PET detector technologies, regulatory pressure to speed up novel tracer designation and reduce image reconstruction mistakes, and increased government investment in national nuclear medicine infrastructure.

What are the major trends in the Global Positron Emission Tomography Market?

▾ The key market trends include the adoption of real-time tracer stability tracking and AI-driven reconstruction, along with a growing shift toward personalized tracer manufacturing and real-world evidence management systems.

Which region held the largest share of the Global Positron Emission Tomography Market in 2026?

▾ North America is expected to account for the largest market share in 2026, with a share of about 39.2%.

Which region is expected to grow the fastest in the Global Positron Emission Tomography Market?

▾ Asia Pacific is the fastest-growing region in the market during the forecast period.

Who are the key players in the Global Positron Emission Tomography Market?

▾ Some of the major key players in the Global PET Market are GE Healthcare Technologies Inc., Siemens Healthineers AG, Philips Healthcare, Canon Medical Systems Corporation, Neusoft Medical Systems Co., Ltd., and many others.

How is the Global Positron Emission Tomography Market segmented?

▾ The market is segmented by product type, detector type, isotope type, application, and end-user.