Market Overview

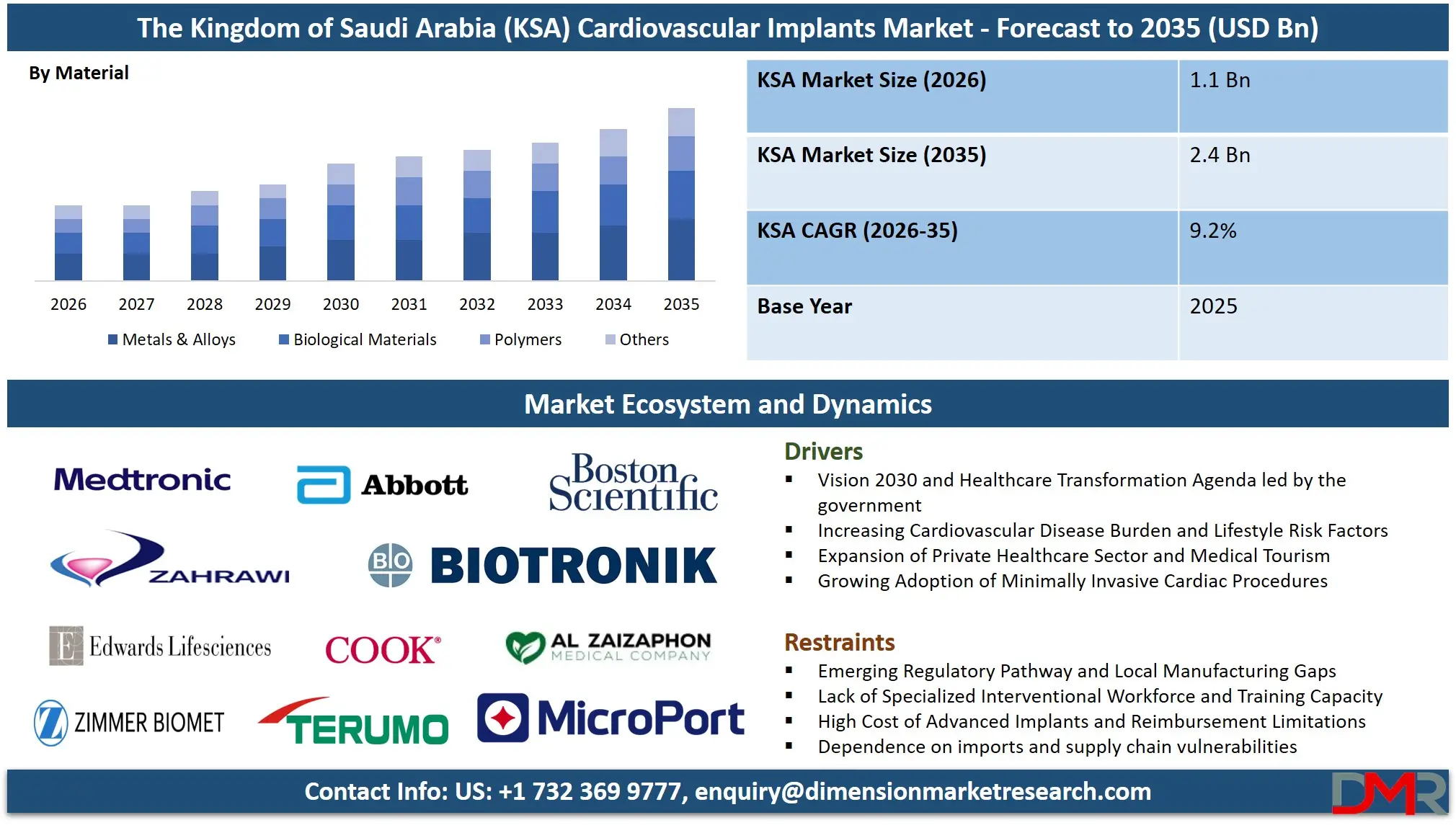

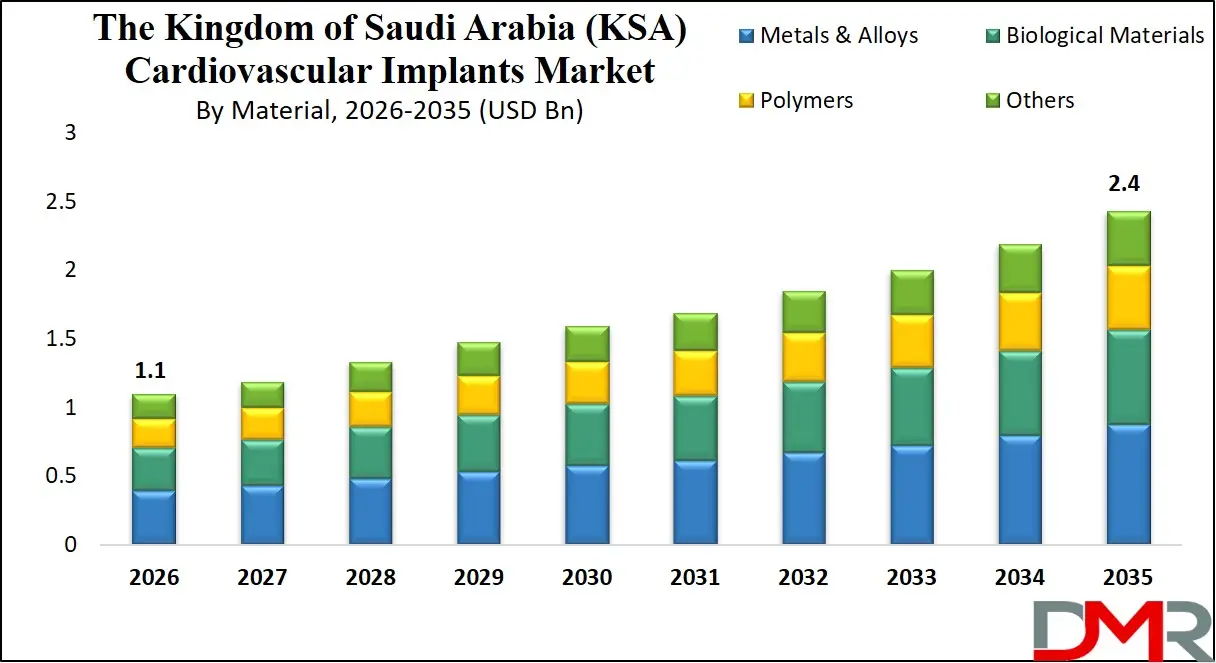

The Saudi Arabia Cardiovascular Implants Market size is expected to reach a value of USD 1.1 billion in 2026, and it is further anticipated to reach a market value of USD 2.4 billion by 2035 at a CAGR of 9.2%.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Saudi Arabia cardiovascular implants market is one of the rapidly growing markets in the Middle East because the region has set ambitious healthcare transformation objectives that should be reached by integrating the Vision 2030 and the Health Sector Transformation Program. With the increase in cardiovascular diseases (CVDs) cases attributed to lifestyle changes, diabetes, and obesity, the public sector is responding to the need of providing sophisticated cardiac care and implantable devices, and so, are the individual healthcare organizations.

The issue of the cardiovascular implant management in Saudi Arabia is evolving to a higher stage in the form of a national healthcare security scenario and economic diversification. The government initiative to localize the production of medical devices, and the creation of the mega health sectors such as the King Salman Medical City and NEOM Health and Wellbeing sector, is placing a huge demand on cardiovascular implants and related healthcare services.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Saudi Arabia Cardiovascular Implants Market: Key Takeaways & Other Influencing Factors

- Market Growth Insights: The market is anticipated to reach approximately USD 1.1 billion in 2026 and is projected to expand to around USD 2.4 billion by 2035, registering a CAGR of 9.2% during the forecast period.

- By Type of Product: The most active segment is composed of coronary stents, both drug-eluting and bioresorbable. Implantable Cardioverter Defibrillators (ICDs) and Cardiac Resynchronization Therapy (CRT) devices are exponentially becoming significant as the Kingdom deals with the increasing number of heart failure and arrhythmia cases.

- By Material Insights: Metals and alloys (cobalt-chromium and nitinol) are expected to take over the market due to their durability and radiopacity. The most rapidly developing segments are the polymers and the biological materials with the development of bioresorbable scaffolds and heart-valve tissue-engineered valves.

- By End-User Insights: Hospitals and cardiac catheterization laboratories are popularized as complex implant procedures, whereas ambulatory surgical centers (ASCs) are rapidly increasing because of their lower cost and shorter recovery time of specific interventions.

- Saudi Health Sector Transformation Program (HSTP): The HSTP is a project to privatize 290 primary healthcare centers and increase the number of specialized cardiac centers across the Kingdom which is a colossal undertaking in terms of access to cardiovascular implants and management of risk linked to late interventions.

- Ministry of Health (MOH), Saudi Arabia: Saudi Arabia has one of the highest rates of diabetes and obesity in the world and over 18.0% of the adult population in the country already has diabetes and cardiovascular risks to the population should be assessed and reduced.

- General Authority for Statistics (GASTAT), Saudi Arabia: It is projected that over 25.0 percent of the population in Saudi Arabia would be aged 50 years or above by 2035. This population change worsens the risk factor of coronary artery disease and triggers the development of cardiovascular implant solutions to aging infrastructure, housing and population health services.

Impact of the Iran conflict on Saudi Arabia Cardiovascular Implants Market

Iran crisis is a risk that has augmented supply chain and regulatory risks in Cardiovascular Implants Market in Saudi Arabia. The mounting tensions risk disruption of import pathways of raw herbs and finished goods, and accelerate the necessity to have localized production capacities, which include quality assurance and supply chain resilience. The players (NEOM Wellness, Ajmal Perfumes (Ayurveda division), and local distributors) are making investments in local manufacturing partners, e-commerce solutions and quality certification solutions. The market is shifting towards vertically-integrated markets with a combination of local sourcing, GMP-certified production and digital distribution. It will give an opportunity to local producers, logistics companies, and certification organizations across the wellness programs in Saudi Arabia.

Saudi Arabia Cardiovascular Implants Market: Use Cases

- Giga-Project Healthcare Infrastructure and Resilience: NEOM Health and Wellbeing, King Abdullah Medical City, and King Salman Medical City must be planned in terms of the problem of cardiovascular implant logistics. These initiatives are employing high-tech modelling to understand and address the risk of supply chain interruptions, implant recalls and inventory expiry to guarantee operational sustainability in the long term and patient safety.

- Chronic Disease Management and Preventive Cardiology: The burden of ischemic heart disease is considered one of the national concerns. Cardiovascular implant risk management is being intensively invested in by the government and the private sector in the form of hospital procurement resilience, post-operative monitoring, and remote cardiac rehabilitation to control the risks of repeat interventions and device complications.

- Public-Private Partnership (PPP) to Cardiac Care Expansion: Since the Ministry of Health and the Private Sector Participation Center (PCP) are concerned with the expansion of specialized cardiac services, healthcare operators are reducing access risks. It includes investments in hybrid operating rooms, capacity building of cath labs, and purchasing of implants on the basis of outcomes in accordance with the international standards of clinical practices.

- Insurance Sector Risk Stratification and Reimbursement Alignment: The Council of Health Insurance (CHI) and the Saudi Central Bank (SAMA) are beginning to implement value-based healthcare and implant outcome guidelines on the health insurance sector. Major underwriters, as well as third-party administrators (TPAs), have started to conduct clinical and financial risk management of their cardiology books, particularly risks associated with high-priced implants (ICDs, CRT devices) and rehospitalization.

Saudi Arabia Cardiovascular Implants Market: Market Dynamics

Driving Factors in Saudi Arabia Cardiovascular Implants Market

Vision 2030 and Healthcare Transformation Agenda led by the government

The most important driving forces of cardiovascular implants market are the Vision 2030 Health Sector Transformation Program and the National Transformation Program. These initiatives of the government impose the quality of healthcare and patient safety and localization of medical technologies that give a top-down demand on the purchase of cardiovascular implants and the provision of clinical reporting and post-market surveillance services throughout the healthcare economy.

Increasing Cardiovascular Disease Burden and Lifestyle Risk Factor

The rising incidence of coronary artery disease, heart failure and arrhythmias which are caused by obesity, diabetes, hypertension and sedentary lifestyles are major drivers of the market. These are the conditions that require deep cardiovascular implant interventions and long-term patient management plans, which will equip them with the capability to decrease mortality and sustainability in the long-term.

Restraints in Saudi Arabia Cardiovascular Implants Market

Emerging Regulatory Pathway and Local Manufacturing Gaps

The system of regulatory accelerated approval of new cardiovascular implants, which is built in Saudi Arabia through the Saudi Food and Drug Authority (SFDA) is not as developed as in Europe and the US. Lack of rapid ways of bioresorbable devices and lack of localized production of implants can lead to dependence on supply chain and will not allow the mass adoption and cost-cutting of the market.

Lack of Specialized Interventional Workforce and Training Capacity

The local interventional cardiologists and cardiac electrophysiologists are not sufficient in the special field of complicated implantations, particularly in such fields as CRT implantation, and lead extraction. This reliance on international clinical experts can increase costs and slow down the experience of instilling new cardiovascular implant skills into homeland hospitals.

Opportunities in Saudi Arabia Cardiovascular Implants Market

Development of Local MedTech Manufacturing and Supply Chain Capabilities

The possibility of developing and developing local expertise in the fields of cardiovascular implants assembly, coating, and sterilization has a strong chance of growth and development. Localized manufacturing plants, AI-based inventory systems, and cold chain logistics, specific to the demands of the Gulf area, can address some of the most important market demands and help the Kingdom become self-sufficient in this important sphere of healthcare.

Value-Based Reimbursement and Outcomes-Based Contracting

With the Saudi Arabia coming up with a value-based healthcare framework, the cardiovascular implant outcomes management services have a huge prospect. Demand in both the public hospitals and the private cardiac centers will be high as a result of the necessity to independently clinically verify, risk assess patients in the patient registry and to be compliant with international clinical guidelines.

Trends in Saudi Arabia Cardiovascular Implants Market

Cardiovascular Implant Data and Digital Health Platforms Integration

The fact that cardiovascular implant intelligence is being integrated into the basic design and operational model of digital health platforms at Saudi Arabia is one of the significant trends in this market. Implant data are being fed into electronic medical records (EMRs) and remote monitoring applications and into hospital command centers to allow real-time adverse event detection and automatic follow-up scheduling.

Growing Focus on Bioresorbable and Leadless Implant Technologies

Taking into account the saliency of long-term device complications, the focus on managing the risks associated with the use of devices is one of the trends that should be considered, which also presupposes the introduction of the next-generation implants. Such technologies as bioresorbable vascular scaffolds (BVS) and leadless pacemakers are highly important in terms of investments and their application is becoming the norm in large cardiac centers as post-market surveillance of such new devices.

Saudi Arabia Cardiovascular Implants Market: Research Scope and Analysis

By Product Type Analysis

The Saudi Arabia market is currently dominated by Coronary stents, and it means that the acute coronary syndromes burden the kingdom on the spot. They are drug-eluting stents (DES), bare-metal stents (BMS) and bioresorbable scaffolds. Evaluation and usage of these devices are vital to the decrease in myocardial infarction, the survival of revascularization, and health economics. The rate of Implantable Cardioverter Defibrillators (ICDs) is growing at an alarming pace due to the commitment of the country to curb the sudden cardiac deaths as well as control heart failure. This will involve sudden death risk, risks of infection of the device and improper management of shocks. Heart Valves and Cardiac Resynchronization Therapy (CRT) devices are in the most primitive stages and still under development as the population grows old and structural heart disease is growing more common.

By Material Analysis

The most prominent segment is Metals and Alloys (cobalt-chromium, platinum-iridium, nitinol), since it provides the basic mechanical properties on the basis of which all the other functions of implants work. This is radial strength, MRI compatibility and long-term durability fatigue resistance. The most rapidly developing category is Polymers (including bioresorbable polymers) and Biological Materials (tissue heart valves) because of the need to have fewer long-term complications and be better biocompatible. Biological Materials will still be an important part of heart valve replacement and the Metals and Alloys will still be needed in stent platforms and electrodes in devices.

By Procedure Type Analysis

This segment is poised to be dominated by angioplasty (percutaneous coronary intervention) because it is recommended that least invasive solutions should serve the acute myocardial infarction patient requirements as well as be compatible with the 24/7 cath lab networks currently being established. Also important is Open Heart Surgery (coronary artery bypass grafting, valve replacement), here complex multivessel disease, advanced heart failure and surgery of critical valve cases are of paramount importance due to the complete revascularization and durability required.

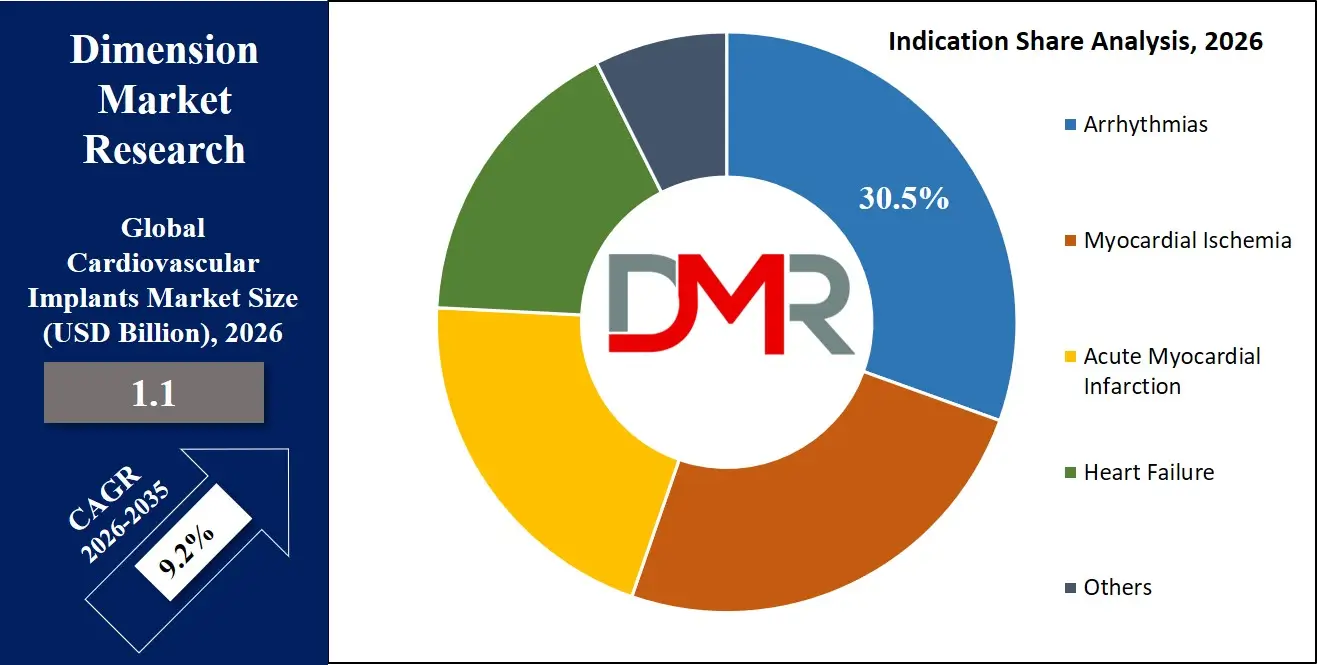

By Indication Analysis

Myocardial Ischemia and Acute Myocardial Infarction are the segments that will prevail in the market since they command the greatest market share in 2026. The majority of emergent implant procedures are represented by the large number of patients who have stable angina, NSTEMI, and STEMI.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Such conditions have the clinical urgency and procedural requirement to spend a lot of money on coronary stents and devices. Arrhythmias (such as atrial fibrillation, ventricular tachycardia) and Heart Failure are developing but maturing areas, largely due to population ageing and general improvement in diagnostic measures, and are becoming more and more treated with ICDs, pacemakers, and CRT devices.

By End-User Analysis

Hospitals account for the largest share as these are the most optimal location site and funder of cardiovascular implant procedures via the MOH and other governmental bodies. The Cardiac Catheterization Laboratories (cath labs) are also right behind since not only do they have to cope with the angioplasty acute procedural volume, but also the follow-up of implanted devices. The growth vectors include Specialty Clinics and Ambulatory Surgical Centers (ASCs) as the operators of the new outpatient cardiac centers must consider the role of efficiency and cost-effectiveness in their approach. Others (including academic medical centers and military hospitals), working with complex research and trauma cases, is also another end-user, although a less important one.

Saudi Arabia Cardiovascular Implants Market Report is segmented on the basis of the following:

By Product Type

- Coronary Stents

- Implantable Cardioverter Defibrillators (ICDs)

- Heart Valves

- Implanted Cardiac Pacemakers

- Cardiac Resynchronization Therapy (CRT) Devices

- Peripheral Stents

- Others

By Material

- Metals & Alloys

- Polymers

- Biological Materials

- Others

By Procedure Type

- Angioplasty

- Open Heart Surgery

By Indication

- Arrhythmias

- Myocardial Ischemia

- Acute Myocardial Infarction

- Heart Failure

- Others

By End-User

- Hospitals

- Specialty Clinics

- Ambulatory Surgical Centers

- Cardiac Catheterization Laboratories

- Others

Impact of Artificial Intelligence in Saudi Arabia Cardiovascular Implants Market

The integration of machine learning algorithms also makes AI-powered analytics platforms more intelligent and useful to the Saudi Arabia Cardiovascular Implants Market. Having patient health trend predictive models, demand forecasting and inventory optimization, healthcare providers and distributors are able to predict market changes and integrate their supply chains accordingly. This can enable manufacturers to lower inventory levels of hot selling implantable products like coronary stents and ICDs or a hospital to streamline seasonal cath lab inventory selections out of the box.

The incorporation of AI assists in the sourcing of transparency and quality assurance of cardiovascular implants as well. AI-based spectroscopy devices and supply chain analytics can verify raw materials (cobalt-chromium alloys, polymers, and biological tissues), identify production flaws or material contamination, and forecast sourcing upheavals depending on environmental and geopolitical conditions. This is particularly crucial to the healthcare plans of Saudi Arabia including the health-related projects of NEOM, where the purity, sterility, and regulatory quality of the implants becomes more guaranteed with time without the need to conduct a lot of hand-held tests before it is clear.

Saudi Arabia Cardiovascular Implants Market: Competitive Landscape

The Saudi Arabia market of cardiovascular implants is a dynamic place, with large government-funded hospital systems, top international medical equipment manufacturers, and an additional ecosystem of local distributors. The focus of competition lies in the realization of the Vision 2030 healthcare goals.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Anchors, key consumers, and innovators are state-owned hospital networks and project developers, including the Ministry of Health, King Faisal Specialist Hospital, NEOM Health, and Dr. Sulaiman Al Habib Medical Group. They are associated with the largest companies worldwide such as Medtronic, Abbott, Boston Scientific and Johnson and Johnson on device technologies and clinical training. The developing healthcare is served by local and regional distributors such as Tamer Group and Nahdi Medical.

Some of the prominent players in Saudi Arabia Cardiovascular Implants Market are:

- Medtronic plc

- Abbott Laboratories

- Boston Scientific Corporation

- Edwards Lifesciences Corporation

- Johnson & Johnson MedTech

- BIOTRONIK SE & Co. KG

- Terumo Corporation

- B. Braun Melsungen AG

- Jamjoom Medical Industries Co. Ltd.

- NABD Medical Industries Company

- Atlas Medical LLC

- Al Zaizaphon Medical Distribution Company

- Al Rowais Medical Equipment Co. Ltd.

- Al Zahrawi Medical Supplies LLC

- MicroPort Scientific Corporation

- LivaNova PLC

- Getinge AB

- Cook Medical LLC

- W. L. Gore & Associates, Inc.

- Meril Life Sciences Pvt Ltd.

- Other Key Players

Recent Developments in Saudi Arabia Cardiovascular Implants Market

- February 2026: Boston Scientific Corporation issued a global recall of certain AXIOS stent and delivery systems due to deployment and expansion issues, reinforcing the importance of safety monitoring and quality control in cardiovascular implant devices.

- October 2025: Medtronic plc signed a five-year agreement with King Faisal Specialist Hospital & Research Centre (KFSHRC) to ensure continuous supply of cardiac catheterization devices and expand cardiac care capacity, including new cardiac unit setup and staff training programs.

- January 2025: Abbott Laboratories collaborated in the above procedure, with its HeartMate 3 left ventricular assist device (LVAD) used in the robotic implant, highlighting the growing adoption of advanced implantable heart failure technologies in Saudi Arabia.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 1.1 Bn |

| Forecast Value (2035) |

USD 2.4 Bn |

| CAGR (2026–2035) |

20.3% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Product Type (Coronary Stents, Implantable Cardioverter Defibrillators (ICDs), Heart Valves, Implanted Cardiac Pacemakers, Cardiac Resynchronization Therapy (CRT) Devices, Peripheral Stents, and Others), By Material (Metals & Alloys, Polymers, Biological Materials, and Others), By Procedure Type (Angioplasty and Open Heart Surgery), By Indication (Arrhythmias, Myocardial Ischemia, Acute Myocardial Infarction, Heart Failure, and Others), By End-User (Hospitals, Specialty Clinics, Ambulatory Surgical Centers, Cardiac Catheterization Laboratories, and Others) |

| Country Coverage |

The Kingdom of Saudi Arabia (KSA) |

| Prominent Players |

Medtronic plc, Abbott Laboratories, Boston Scientific Corporation, Edwards Lifesciences Corporation, Johnson & Johnson MedTech, BIOTRONIK SE & Co. KG, Terumo Corporation, B. Braun Melsungen AG, Jamjoom Medical Industries Co. Ltd., NABD Medical Industries Company, Atlas Medical LLC, Al Zaizaphon Medical Distribution Company, Al Rowais Medical Equipment Co. Ltd., Al Zahrawi Medical Supplies LLC, MicroPort Scientific Corporation, LivaNova PLC, Getinge AB, Cook Medical LLC, W. L. Gore & Associates, Inc., Meril Life Sciences Pvt Ltd., and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users), and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Saudi Arabia Cardiovascular Implants Market?

▾ The Saudi Arabia Cardiovascular Implants Market size is estimated to have a value of USD 1.1 billion in 2026 and is expected to reach USD 2.4 billion by the end of 2035.

Who are the key players in the Saudi Arabia Cardiovascular Implants Market?

▾ Some of the major key players in the Saudi Arabia Cardiovascular Implants Market are Medtronic plc, Abbott Laboratories, Boston Scientific Corporation, Edwards Lifesciences Corporation, Johnson & Johnson MedTech, and Biotronik SE & Co. KG, and many others.

What is the growth rate in the Saudi Arabia Cardiovascular Implants Market?

▾ The market is growing at a CAGR of 9.2% over the forecasted period.