Market Overview

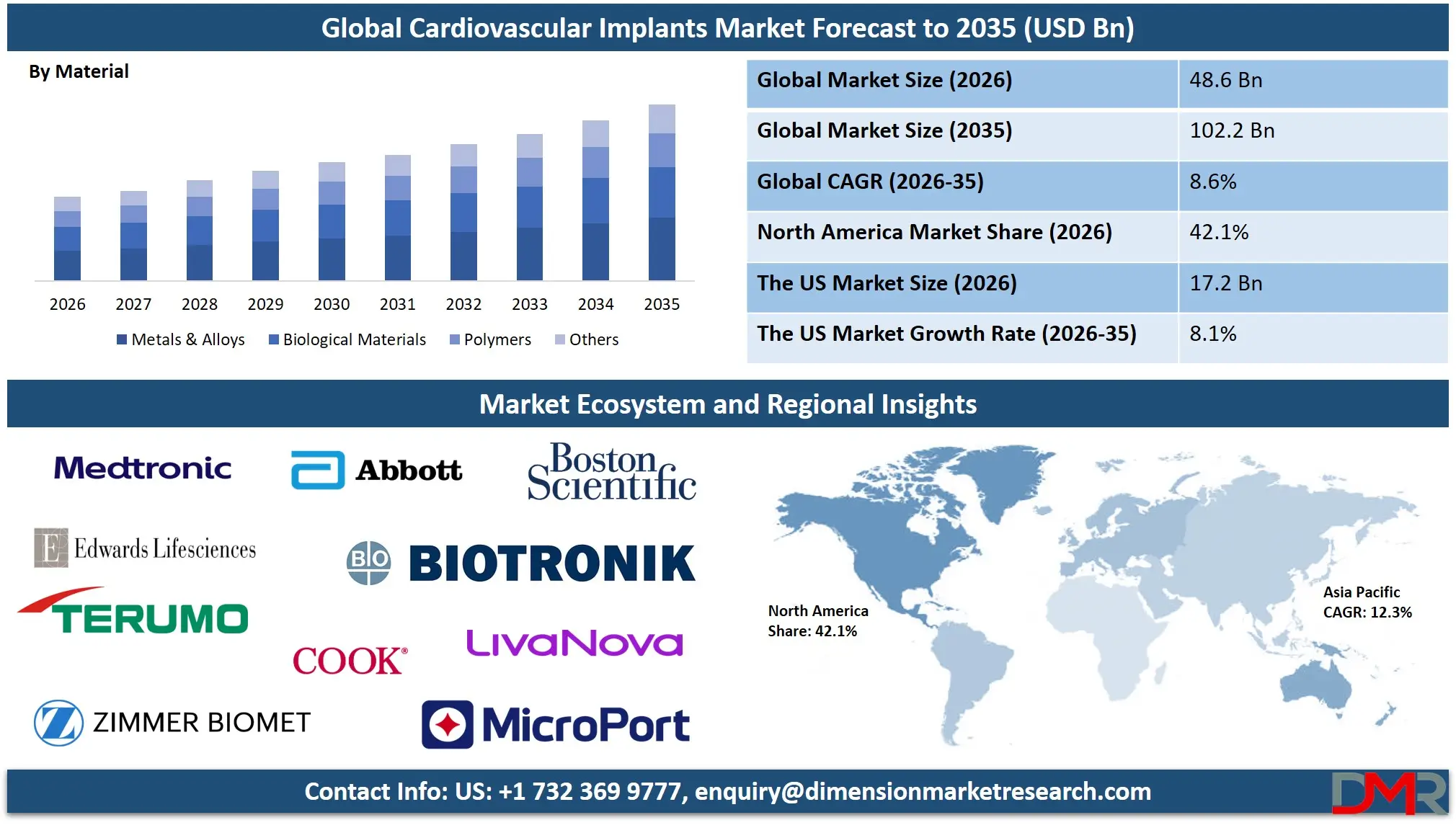

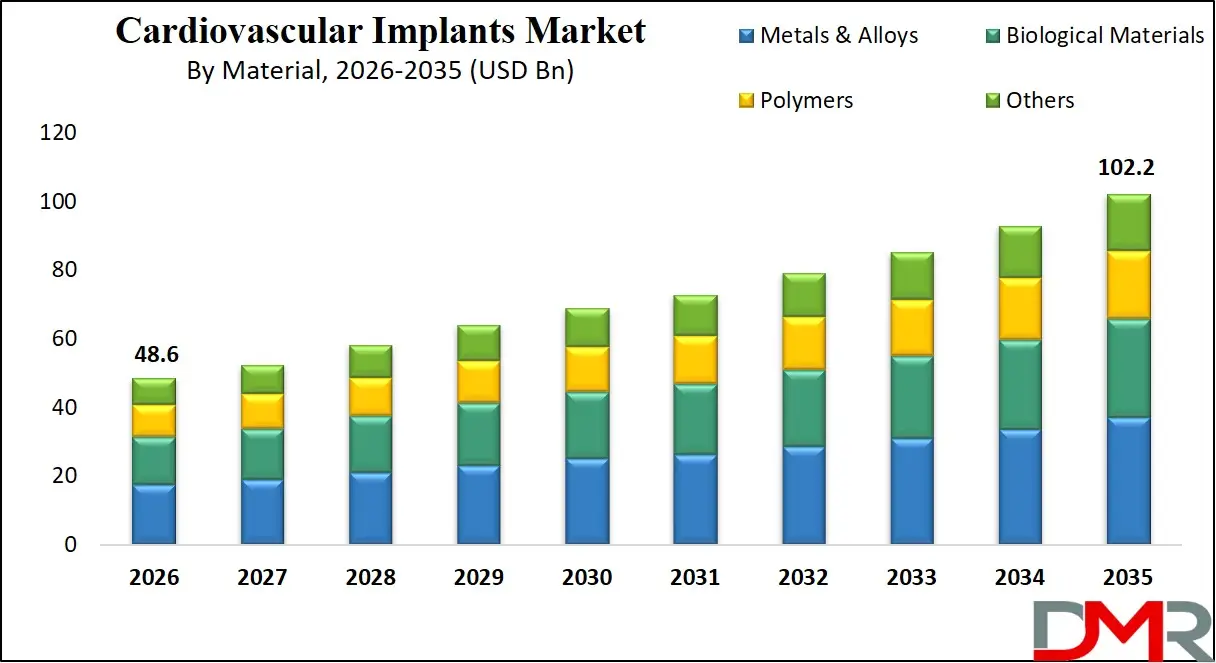

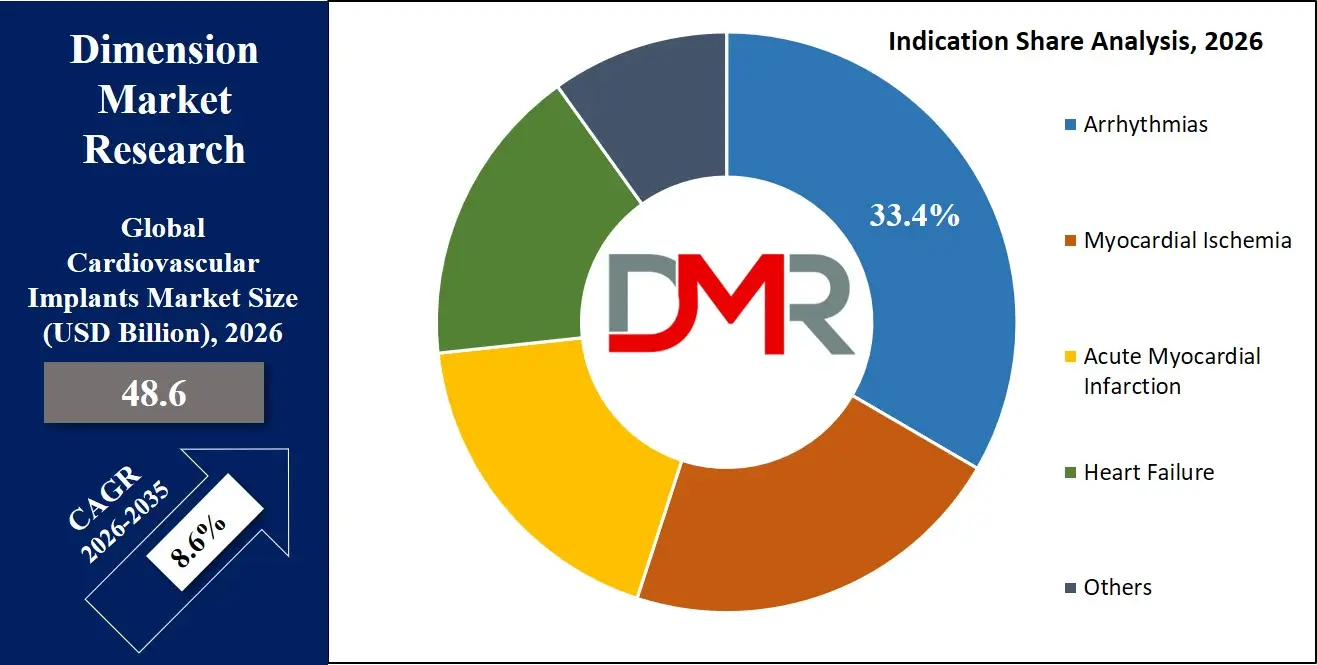

The Global Cardiovascular Implants Market is estimated to be valued at USD 48.6 billion in 2026 and is projected to witness strong expansion over the forecast period. Growing at a compound annual growth rate (CAGR) of 8.6% from 2026 to 2035, the market is anticipated to reach approximately USD 102.2 billion by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

This growth reflects increasing demand for minimally invasive cardiac interventions, rising prevalence of cardiovascular diseases globally, expanding adoption of advanced implantable technologies across healthcare systems, and greater deployment of next-generation cardiac devices in hospitals, specialty clinics, ambulatory surgical centers, and cardiac catheterization laboratories. The market expansion is further supported by advancements in bioresorbable materials, leadless pacemaker technology, transcatheter valve systems, and remote patient monitoring capabilities, along with strengthening clinical guidelines promoting early intervention and improved patient outcomes worldwide.

Cardiovascular implants enable restoration of cardiac function, rhythm management, and vascular patency through innovative device engineering, biocompatible materials, extended battery longevity, and miniaturized form factors optimized for percutaneous delivery. These solutions address critical gaps in cardiovascular care related to aging populations, rising sedentary lifestyles, and increasing prevalence of comorbidities, supporting healthcare systems in reducing mortality and disability from cardiac conditions.

Technological advancements, including smart implants with remote hemodynamic monitoring, MRI-compatible pacing systems, drug-eluting bioresorbable scaffolds, robotic-assisted delivery platforms, and app-integrated patient management interfaces, are transforming the market into a highly sophisticated and patient-centric ecosystem. Integration of advanced biomaterials including platinum-iridium alloys, expanded polytetrafluoroethylene, and bovine pericardial tissue, alongside nanocomposite polymer coatings for enhanced biocompatibility, is reshaping clinical outcomes across both structural and electrophysiological interventions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Growing government healthcare expenditures requiring expanded access to cardiac care under initiatives like global universal health coverage frameworks further accelerate adoption. However, barriers such as stringent regulatory approval pathways, reimbursement limitations in developing regions, product recall risks associated with device failures, and specialized training requirements for implant procedures remain. Despite these limitations, the convergence of precision medicine, minimally invasive surgical techniques, and value-based healthcare delivery positions cardiovascular implants as a cornerstone of global cardiac care through 2035.

The US Cardiovascular Implants Market

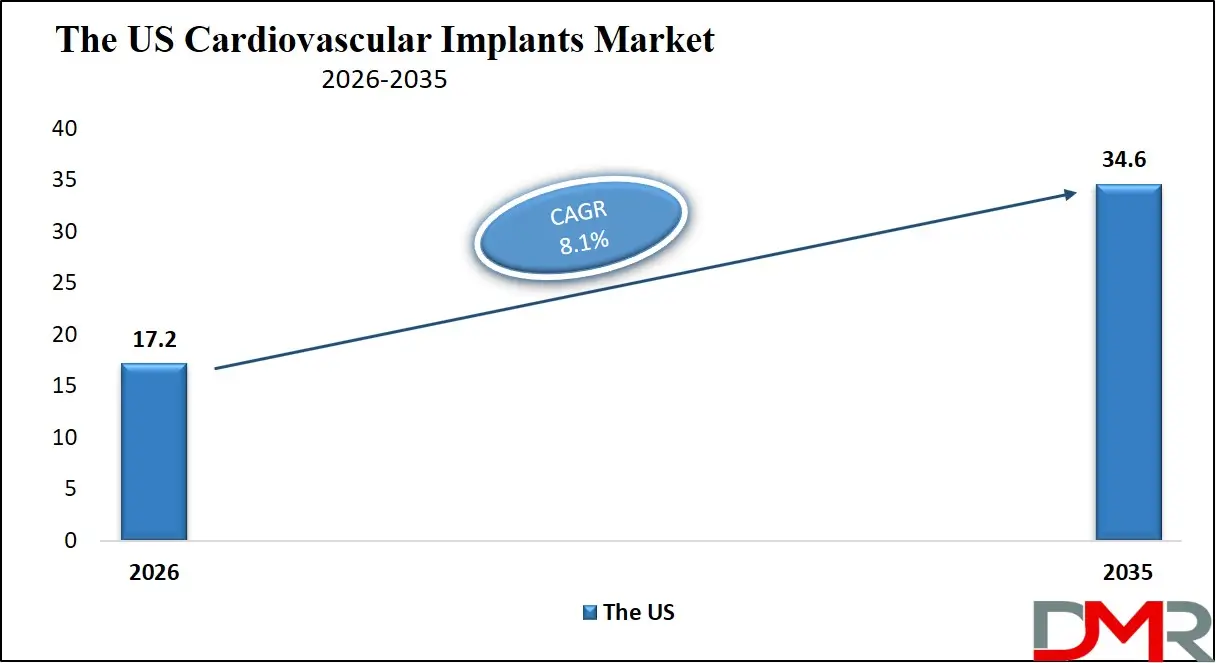

The US Cardiovascular Implants Market is projected to reach USD 17.2 billion in 2026 at a compound annual growth rate of 8.1%, reaching USD 34.6 billion by 2035. The U.S. leads global adoption due to its mature interventional cardiology infrastructure, robust Medicare coverage for implant procedures, high prevalence of cardiovascular risk factors, and strong emphasis on technological innovation adoption.

The national expansion of structural heart programs in community hospitals, coupled with growing institutional demand from large health systems and cardiac centers of excellence, fuels sustained market growth. Major manufacturers such as Abbott Laboratories, Medtronic, and Boston Scientific are scaling production and innovating next-generation transcatheter valve systems and leadless pacemaker platforms optimized for elderly and high-surgical-risk populations.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

U.S. federal support through NIH cardiovascular research funding, CMS coverage determinations for emerging technologies, and FDA breakthrough device designation programs encourages continued innovation. Partnerships between medical device manufacturers and professional societies like the American College of Cardiology continue to advance clinical guidelines and procedural training.

The rapid rise of transcatheter aortic valve replacement expansions into intermediate and low-risk populations, integration with digital health platforms for remote device monitoring, and development of fully bioresorbable stent technologies continues to redefine the U.S. cardiac care landscape, positioning the country as the global benchmark for cardiovascular implant innovation and clinical adoption.

The Europe Cardiovascular Implants Market

The Europe Cardiovascular Implants Market is projected to be valued at approximately USD 13.3 billion in 2026 and is projected to reach around USD 27.2 billion by 2035, growing at a CAGR of about 8.3% from 2026 to 2035. Europe's leadership is anchored by strengthening cardiac care networks, increasing structural heart program penetration, and harmonized medical device regulations under the Medical Device Regulation framework across member states.

Countries such as Germany, the U.K., France, Italy, and Spain are widely adopting advanced cardiovascular implant technologies, driven by aging populations, well-established social health insurance systems, and EU initiatives like cross-border healthcare directives facilitating patient access to specialized cardiac procedures. The U.K.'s National Health Service cardiovascular networks and Germany's centralized heart center model are particularly active in deploying next-generation implants in high-volume cardiac facilities.

Europe's emphasis on clinical outcomes research, demand for cost-effectiveness evidence, and focus on interoperable device data systems across borders further drive adoption. Funding through Horizon Europe health research programs and national innovation agency grants supports R&D in extended-durability heart valves, miniaturized pacemaker systems, and MRI-compatible device platforms.

Urban healthcare infrastructure upgrades in Paris university hospitals, Berlin heart centers, and London tertiary cardiac facilities increasingly deploy robotic-assisted implant delivery systems, integrated imaging platforms, and comprehensive device registries co-located with clinical outcomes tracking. With robust reimbursement frameworks, integration into ESC clinical practice guidelines, and emphasis on multidisciplinary heart team approaches, Europe remains one of the most advanced regions in cardiovascular implant penetration.

The Japan Cardiovascular Implants Market

The Japan Cardiovascular Implants Market is anticipated to be valued at approximately USD 3.4 billion in 2026 and is expected to attain nearly USD 6.1 billion by 2035, expanding at a CAGR of about 6.7% during the forecast period. Japan's rapidly aging population, among the highest global life expectancy rates, combined with high prevalence of valvular heart disease and age-related conduction disorders, drives strong demand for advanced implantable cardiac devices in the world's most elderly demographic.

The Ministry of Health, Labour and Welfare actively supports cardiovascular implant access through national health insurance coverage, centralized device reimbursement mechanisms, and integration into geriatric care pathways and longevity society health policy frameworks. Japan's leadership in miniaturized electronics manufacturing and precision engineering accelerates innovation in ultra-compact pacemaker designs and delivery systems optimized for smaller-stature Asian populations.

Japan's concept of "Community-Based Integrated Care Systems", supported by prefectural governments and regional medical associations, integrates cardiovascular implant follow-up care into neighborhood health promotion hubs. Advanced cardiac devices are being deployed in Tokyo metropolitan hospitals, Osaka cardiovascular centers, and regional core hospitals across all prefectures. Japan's cultural emphasis on technological precision and meticulous post-procedure management, combined with demographic urgency, positions the country as a high-growth innovator in cardiovascular implant technologies.

Global Cardiovascular Implants Market: Key Takeaways

- Strong Global Market Growth Outlook: The Global Cardiovascular Implants Market is expected to be valued at USD 48.6 billion in 2026 and is projected to reach USD 102.2 billion by 2035, showcasing rapid expansion supported by rising cardiovascular disease burden and technological innovation in device design.

- High CAGR Driven by Minimally Invasive Procedures: The market is expected to grow at an impressive CAGR of 8.6% from 2026 to 2035, fueled by accelerating transcatheter valve replacement adoption, expanding indications for cardiac resynchronization therapy, increasing percutaneous coronary intervention volumes, and growing prevalence of heart failure worldwide.

- Strong Growth Trajectory in the United States: The U.S. Cardiovascular Implants Market stands at USD 17.2 billion in 2026 and is projected to reach USD 34.6 billion by 2035, expanding at a CAGR of 8.1% due to robust Medicare coverage policies, high procedural volumes in structural heart programs, and advanced medical device innovation ecosystem.

- North America Maintains Regional Dominance: North America is expected to capture approximately 42.1% of the global market share in 2026, supported by mature interventional cardiology infrastructure, significant private and public healthcare investment, and early adoption of next-generation implantable cardiac technologies.

- Rapid Advancement in Implant Technologies: Innovations including leadless pacemakers, transcatheter mitral valve systems, bioresorbable coronary scaffolds, and remote monitoring-enabled implantable defibrillators are significantly improving patient outcomes, reducing procedure times, and expanding treatable patient populations.

- Growing Cardiovascular Disease Burden Boosts Adoption: Rising global incidence of coronary artery disease, heart failure, valvular disorders, and arrhythmias, coupled with aging population demographics and increasing prevalence of diabetes and hypertension, is driving sustained demand for durable, high-performance cardiac implant solutions.

Global Cardiovascular Implants Market: Use Cases

- Coronary Artery Disease Management: Drug-eluting coronary stents implanted via percutaneous coronary intervention restore blood flow in stenosed arteries, preventing myocardial infarction and reducing need for repeat revascularization procedures in patients with stable angina and acute coronary syndromes.

- Heart Failure Treatment Optimization: Cardiac resynchronization therapy devices with biventricular pacing improve ventricular synchrony, reduce heart failure hospitalizations, and enhance quality of life in patients with reduced ejection fraction and wide QRS duration.

- Sudden Cardiac Arrest Prevention: Implantable cardioverter defibrillators continuously monitor cardiac rhythm and deliver life-saving shocks for ventricular tachyarrhythmias in primary and secondary prevention populations with compromised left ventricular function.

- Valvular Heart Disease Intervention: Transcatheter aortic and mitral valve replacements provide minimally invasive treatment options for high-surgical-risk patients with severe symptomatic valvular stenosis or regurgitation, reducing recovery times and procedural complications.

- Bradycardia Rhythm Management: Implanted cardiac pacemakers with rate-responsive algorithms maintain adequate heart rates in patients with symptomatic bradycardia, sick sinus syndrome, and atrioventricular conduction disorders, enabling normal daily activities and improved functional capacity.

Global Cardiovascular Implants Market: Stats & Facts

World Health Organization (WHO)

- Cardiovascular diseases are the leading cause of death globally, accounting for approximately 17.9 million deaths annually.

- Ischemic heart disease alone causes an estimated 8.9 million deaths each year worldwide.

- Over 75% of cardiovascular disease deaths occur in low- and middle-income countries.

- Hypertension affects an estimated 1.28 billion adults aged 30-79 years globally.

- Heart failure prevalence ranges from 1-3% of the general population in developed countries.

- Rheumatic heart disease affects over 40 million people, predominantly in developing regions.

- Atrial fibrillation affects approximately 33.5 million individuals worldwide.

- Tobacco use contributes to approximately 10% of all cardiovascular disease deaths.

- Physical inactivity is estimated to cause 6% of coronary heart disease burden globally.

American Heart Association (AHA)

- Nearly half of all U.S. adults have some form of cardiovascular disease.

- Coronary heart disease is the leading cause of death in the U.S. , with over 375,000 annual deaths.

- Approximately 805,000 heart attacks occur annually in the United States.

- Heart failure affects about 6.7 million Americans aged 20 and older.

- Stroke accounts for 1 in 19 U.S. deaths, with over 160,000 annual deaths.

- Atrial fibrillation prevalence in the U.S. is projected to reach 12.1 million by 2030.

- Over 350,000 out-of-hospital cardiac arrests occur annually in the U.S.

- Congenital heart defects affect approximately 1% of live births, or about 40,000 infants annually.

- Cardiovascular disease costs the U.S. healthcare system over $400 billion annually.

National Institutes of Health (NIH) / National Library of Medicine

- Approximately 30-50% of patients with heart failure die within 5 years of diagnosis.

- Sudden cardiac death accounts for up to 50% of all cardiovascular deaths.

- Restenosis rates following bare-metal stent implantation range from 20-35% within 6 months.

- Drug-eluting stents reduce restenosis rates to less than 10% in appropriate patient populations.

- Pacemaker implantation rates exceed 1 million procedures annually worldwide.

- Transcatheter aortic valve replacement procedures have grown to over 300,000 annually globally.

- Cardiac implantable electronic device infections occur in 1-4% of implant procedures.

- Average battery longevity for modern pacemakers ranges from 8-12 years.

- Leadless pacemakers reduce device-related complications by approximately 50% compared to conventional systems.

European Society of Cardiology (ESC)

- Cardiovascular disease causes over 4 million deaths annually in Europe.

- Coronary artery disease accounts for approximately 40% of all cardiovascular deaths in Europe.

- Heart failure prevalence in Europe ranges from 1-2% of the adult population.

- Atrial fibrillation affects over 11 million people in the European Union.

- Valve disease prevalence increases with age, affecting over 10% of individuals aged 75 and older.

- Transcatheter valve procedures have grown exponentially, exceeding 150,000 annually in Europe.

- Cardiac resynchronization therapy reduces heart failure mortality by approximately 30% in appropriate candidates.

- Implantable cardioverter defibrillator implantation rates vary 10-fold across European countries.

Global Cardiovascular Implants Market: Market Dynamic

Driving Factors in the Global Cardiovascular Implants Market

Aging Population and Cardiovascular Disease Prevalence

The accelerating global demographic shift toward older populations represents a primary driver for cardiovascular implant adoption. Age-related cardiac conditions including aortic stenosis, conduction system disease, and heart failure increase exponentially with advancing age, creating sustained demand for valve replacements, pacemakers, and ventricular assist devices. Healthcare systems worldwide are scaling interventional capacity to address this demographic imperative, with the over-65 population projected to double by 2050, ensuring multi-decade growth tailwinds for cardiac implant manufacturers. The convergence of increased life expectancy with rising cardiovascular risk factor prevalence creates an unprecedented procedural volume trajectory.

Technological Innovation and Expanding Indications

Cardiovascular implant innovation has shifted decisively toward less invasive delivery, enhanced biocompatibility, and expanded patient eligibility. Advancements in transcatheter delivery systems, ultra-thin stent struts with optimized drug elution profiles, extended battery longevity in cardiac rhythm devices, and fully MRI-compatible systems lower the barrier to adoption and expand treatable populations. Smart implants with remote monitoring capabilities and automated physiologic response algorithms enable proactive disease management and reduce healthcare utilization. The convergence of materials science, microelectronics, and interventional cardiology techniques makes definitive cardiac care accessible to increasingly complex and high-risk patient populations than ever before.

Restraints in the Global Cardiovascular Implants Market

Regulatory Hurdles and Reimbursement Constraints

Stringent regulatory approval pathways requiring extensive clinical evidence of safety and effectiveness significantly delay market entry and increase development costs for novel implant technologies. The evolving regulatory landscape, including MDR implementation in Europe and increasingly demanding FDA pre-market approval requirements, creates uncertainty and extends time-to-market by 12-24 months for innovative devices. Simultaneously, reimbursement pressures in mature healthcare systems, including procedure bundling, value-based payment models, and strict coverage criteria, limit adoption velocity, particularly for premium-priced novel technologies without clear cost-effectiveness demonstrations.

Device Longevity and Reintervention Requirements

Cardiovascular implants, despite technological advances, carry finite functional lifespans requiring eventual replacement or revision procedures. Pacemaker battery depletion, stent restenosis, bioprosthetic valve degeneration, and lead fracture represent ongoing clinical challenges that necessitate repeat interventions, exposing patients to cumulative procedural risks and healthcare systems to recurring costs. The psychological burden of device dependency and the clinical complexity of managing device end-of-life scenarios create patient reluctance and physician practice pattern variations that can delay appropriate implantation, particularly in younger patient populations facing multiple expected replacement procedures over their lifetime.

Opportunities in the Global Cardiovascular Implants Market

Expansion into Emerging Economy Cardiac Care Infrastructure

Rapidly urbanizing regions across Southeast Asia, Latin America, Eastern Europe, and the Middle East represent major growth frontiers as governments establish comprehensive cardiac care capabilities and expand health insurance coverage. Partnerships with local healthcare providers, development of tiered product portfolios addressing varying ability-to-pay segments, and establishment of training academies for interventional cardiologists and cardiac surgeons can accelerate market penetration. Localized manufacturing through joint ventures and technology transfer arrangements can address cost sensitivity while meeting local content requirements, unlocking massive volume-driven expansion in populous markets with rising cardiovascular disease burden.

Digital Integration and Remote Patient Management

Integration of implantable devices with smartphone applications, cloud-based remote monitoring platforms, and artificial intelligence-powered arrhythmia detection algorithms creates recurring revenue opportunities through software-as-a-service models and predictive maintenance alerts. Data generated from continuous hemodynamic monitoring, even in otherwise stable patients, can inform clinical decision-making and enable early intervention before acute decompensation events. This transforms cardiovascular implants from passive therapeutic devices into intelligent nodes within integrated digital health ecosystems, improving outcomes while reducing healthcare utilization through proactive disease management.

Trends in the Global Cardiovascular Implants Market

Transcatheter Structural Heart Expansion

Building on the success of transcatheter aortic valve replacement, next-generation delivery systems are enabling percutaneous approaches to mitral, tricuspid, and pulmonic valve disease, expanding the addressable patient population by orders of magnitude. Transcatheter mitral valve repair and replacement technologies, annular reduction devices, and leaflet approximation systems are rapidly maturing, offering alternatives to high-risk open surgical procedures. This structural heart revolution, enabled by collaborative innovation between interventional cardiologists and device engineers, positions catheter-based approaches as the default treatment pathway for valvular heart disease across expanding risk strata.

Personalized and Patient-Specific Implant Design

Advanced imaging, 3D printing, and computational modeling are enabling patient-specific implant selection and customization previously impossible with standard sizing paradigms. Pre-procedural simulation of hemodynamic performance, virtual implantation to predict device-host interactions, and custom-fabricated implants for complex anatomies improve outcomes in challenging patient subsets. This trend toward precision implantation, combined with growing genetic understanding of differential treatment responses, reflects maturation beyond one-size-fits-all approaches toward personalized cardiovascular care delivery.

Global Cardiovascular Implants Market: Research Scope and Analysis

By Product Type Analysis

Coronary Stents are projected to dominate the Product Type segment of the Global Cardiovascular Implants Market. This dominance is driven by the enormous global burden of coronary artery disease and the established clinical efficacy of percutaneous coronary intervention as the primary revascularization strategy for both stable angina and acute coronary syndromes. Drug-eluting stent technology, now in its fourth generation, combines ultra-thin strut designs with biocompatible or bioresorbable polymers and optimized antiproliferative agents to achieve single-digit restenosis rates while minimizing thrombotic risk. The sheer procedural volume, exceeding 4 million PCIs annually worldwide, ensures sustained revenue generation despite declining per-unit pricing through competitive dynamics. While premium pricing pressures exist in mature markets, volume growth in emerging economies and expanding indications for complex lesion subsets including left main and bifurcation disease maintain the coronary stent category's leadership position throughout the forecast period.

While Implantable Cardioverter Defibrillators and Cardiac Resynchronization Therapy Devices represent the highest per-unit value segment and remain critical for sudden death prevention in heart failure populations, their relative unit volume is constrained by stringent implantation criteria and specialized referral pathways. Heart Valves represent the fastest-growing major product category, driven by the transcatheter revolution expanding treatment access to previously inoperable patients and now moving into lower-risk populations. Implanted Cardiac Pacemakers maintain steady volume growth driven by aging demographics and conduction disease prevalence, though technological disruption from leadless systems is reshaping the competitive landscape. Peripheral Stents address the growing burden of peripheral artery disease, particularly in diabetic and elderly populations, with drug-coated balloon and atherectomy device competition influencing adoption patterns.

By Material Analysis

Metals & Alloys are projected to dominate the Material segment of the Global Cardiovascular Implants Market. This dominance reflects the fundamental role of metallic platforms in providing the structural integrity, radiopacity, and mechanical performance required for nearly all cardiovascular implant categories. Cobalt-chromium and platinum-chromium alloys enable ultra-thin stent struts maintaining radial strength while improving deliverability. Titanium alloys provide the hermetic sealing and biocompatibility essential for pacemaker and ICD canisters. Nitinol's unique shape memory and super elastic properties enable self-expanding valve frames and peripheral stents deliverable through tortuous anatomy. The reliability, manufacturability, and extensive clinical history of metallic materials secure their continued dominance, though evolving hybrid designs increasingly incorporate advanced polymers and biological components.

Polymers represent the second-largest and most dynamic material category, with applications expanding rapidly in bioresorbable scaffolds, drug-eluting coatings, and delivery system components. Biological Materials including bovine pericardium, porcine valves, and human cadaveric tissue maintain an essential role in heart valve construction, offering superior hemodynamics and freedom from anticoagulation compared to mechanical alternatives, though with tradeoffs in long-term durability. The Others category encompasses emerging material platforms including nanocomposite coatings, magnesium-based bioabsorbable alloys, and tissue-engineered constructs, representing the innovation frontier where next-generation implant paradigms are being established.

By Procedure Type Analysis

Angioplasty-based procedures are projected to dominate the global market, fundamentally transforming cardiovascular intervention from open surgical approaches to minimally invasive percutaneous techniques. Their dominance stems from compelling advantages in patient recovery, procedural safety, and healthcare resource utilization across coronary, peripheral, and structural interventions. Percutaneous coronary intervention now accounts for over 90% of all coronary revascularization procedures in developed healthcare systems. Transcatheter valve replacement has revolutionized structural heart care, enabling treatment in patients historically deemed inoperable and now competing with surgical approaches in standard-risk populations. The driving forces behind angioplasty dominance are tri-fold: accelerating patient preference for minimally invasive approaches, expanding device capabilities enabling treatment of increasingly complex anatomy, and healthcare system pressures to reduce length of stay and procedural costs. As transcatheter technologies continue advancing into mitral, tricuspid, and combined structural interventions, the procedural volume gap between percutaneous and surgical approaches will widen further, solidifying angioplasty as the dominant cardiovascular implant delivery modality.

Open Heart Surgery forms the crucial and enduring second-largest procedure segment, maintaining essential roles in complex multi-valve disease, coronary artery bypass grafting for extensive multi-vessel disease, and congenital heart defect corrections where percutaneous approaches remain inadequate. The strength of open surgery lies in direct visualization, ability to address multiple pathologies in a single procedure, and proven long-term durability particularly for mechanical valve implants and arterial grafts in younger patients. By providing definitive correction for the most complex cardiac pathologies, this segment addresses the reality that not all patients are candidates for percutaneous approaches. This balance of invasiveness and completeness makes open surgery procedures the primary option for complex multi-system disease and younger patients prioritizing long-term durability over recovery speed. As such, open surgical procedures will remain indispensable, meeting the nuanced needs of patients and anatomies beyond current percutaneous capabilities.

By Indication Analysis

Arrhythmias are poised to be the largest indication segment for cardiovascular implants, driven by the high global prevalence of both bradyarrhythmias requiring pacemaker support and tachyarrhythmias warranting ICD protection. The relentless expansion of cardiac rhythm management indications creates a perfect use case: predictable progression of conduction system disease with age and the proven mortality benefit of device therapy in at-risk populations. This institutionalization of rhythm management in cardiology practice is where implant adoption scales most reliably, ensuring standardized treatment pathways across thousands of healthcare facilities globally. The segment is acutely reinforced by expanding primary prevention ICD indications in heart failure populations and the emerging role of implantable loop recorders for cryptogenic stroke evaluation. Beyond mortality benefits, rhythm management devices demonstrably improve quality of life, reduce hospitalization, and enable active aging in the expanding elderly demographic, directly impacting patient function and healthcare utilization.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Myocardial Ischemia ranks as the second-largest indication segment, fueled by the enormous global burden of coronary artery disease and the established role of coronary stents in restoring myocardial blood flow. The precision and reliability requirements of drug-eluting stents in preventing restenosis and thrombosis directly address clinical imperatives in acute coronary syndrome management and chronic angina control. Furthermore, the scale of coronary interventions justifies continuous product iteration based on clinical outcomes data and comparative effectiveness research. While more constrained in per-unit value compared to rhythm management devices, the sheer procedural volume of coronary interventions secures myocardial ischemia's role as an enduring market pillar.

By End User Analysis

Hospitals are anticipated to dominate the market as the primary drivers and beneficiaries of cardiovascular implant integration. These institutions possess the surgical infrastructure, catheterization laboratory capabilities, multidisciplinary heart team expertise, and perioperative support services essential for comprehensive cardiovascular implant programs. For them, investment in advanced implant technologies is a strategic imperative to attract patients, satisfy referral network expectations, and maintain competitive positioning in increasingly consolidated healthcare markets. Hospitals serve as essential anchor customers for manufacturers, providing predictable, high-volume demand signals that justify product development investment. Their focus on clinical outcomes, procedural efficiency, and comprehensive care pathways aligns perfectly with the maturation of integrated heart valve programs and complex arrhythmia management services. This control over cardiovascular service line development enhances their overall market position and clinical reputation.

Cardiac Catheterization Laboratories represent the vital second-largest end-user segment, for whom cardiovascular implant adoption is the core clinical mission. Confronted with rapidly evolving technology platforms, expanding indications for percutaneous intervention, and competitive pressures to offer the latest techniques, these specialized facilities are turning to comprehensive device portfolios to differentiate their procedural capabilities and fulfill patient expectations for minimally invasive options. For them, integrated solutions encompassing device selection, imaging guidance, and post-procedure management represent a clinically sophisticated path to optimal outcomes. Adoption in this segment is often accelerated following clinical evidence releases or updated professional guidelines demonstrating superiority of novel approaches. By mastering advanced implant techniques, catheterization laboratories transition from procedure-focused facilities to comprehensive cardiovascular care centers.

The Global Cardiovascular Implants Market Report is segmented on the basis of the following:

By Product Type

- Coronary Stents

- Implantable Cardioverter Defibrillators (ICDs)

- Heart Valves

- Implanted Cardiac Pacemakers

- Cardiac Resynchronization Therapy (CRT) Devices

- Peripheral Stents

- Others

By Material

- Metals & Alloys

- Polymers

- Biological Materials

- Others

By Procedure Type

- Angioplasty

- Open Heart Surgery

By Indication

- Arrhythmias

- Myocardial Ischemia

- Acute Myocardial Infarction

- Heart Failure

- Others

By End-User

- Hospitals

- Specialty Clinics

- Ambulatory Surgical Centers

- Cardiac Catheterization Laboratories

- Others

Impact of Artificial Intelligence in the Global Cardiovascular Implants Market

- AI for Patient Selection and Implant Sizing: AI models analyze echocardiographic, CT, and hemodynamic data to recommend optimal device selection and sizing for transcatheter valve procedures, reducing paravalvular leak rates and improving procedural success across structural heart interventions.

- AI-Driven Arrhythmia Detection and Management: Machine learning algorithms continuously analyze implantable device telemetry to detect emerging arrhythmia patterns, predict appropriate therapy delivery, and reduce inappropriate shocks through sophisticated rhythm discrimination.

- Predictive Analytics for Device Longevity: AI algorithms predict battery depletion timelines, lead performance degradation, and potential device failure modes across large patient cohorts, enabling proactive replacement scheduling and reducing emergency interventions.

- Procedural Planning and Simulation: AI-powered platforms simulate device deployment, predict device-host interactions, and optimize access route selection for complex structural heart procedures, reducing procedural time and complication rates.

- Remote Monitoring and Clinical Alerts: AI-enabled analysis of transmitted device data identifies clinically significant trends in hemodynamics, arrhythmia burden, and patient activity, triggering early clinical interventions before acute decompensation events.

Global Cardiovascular Implants Market: Regional Analysis

Region with the Largest Revenue Share

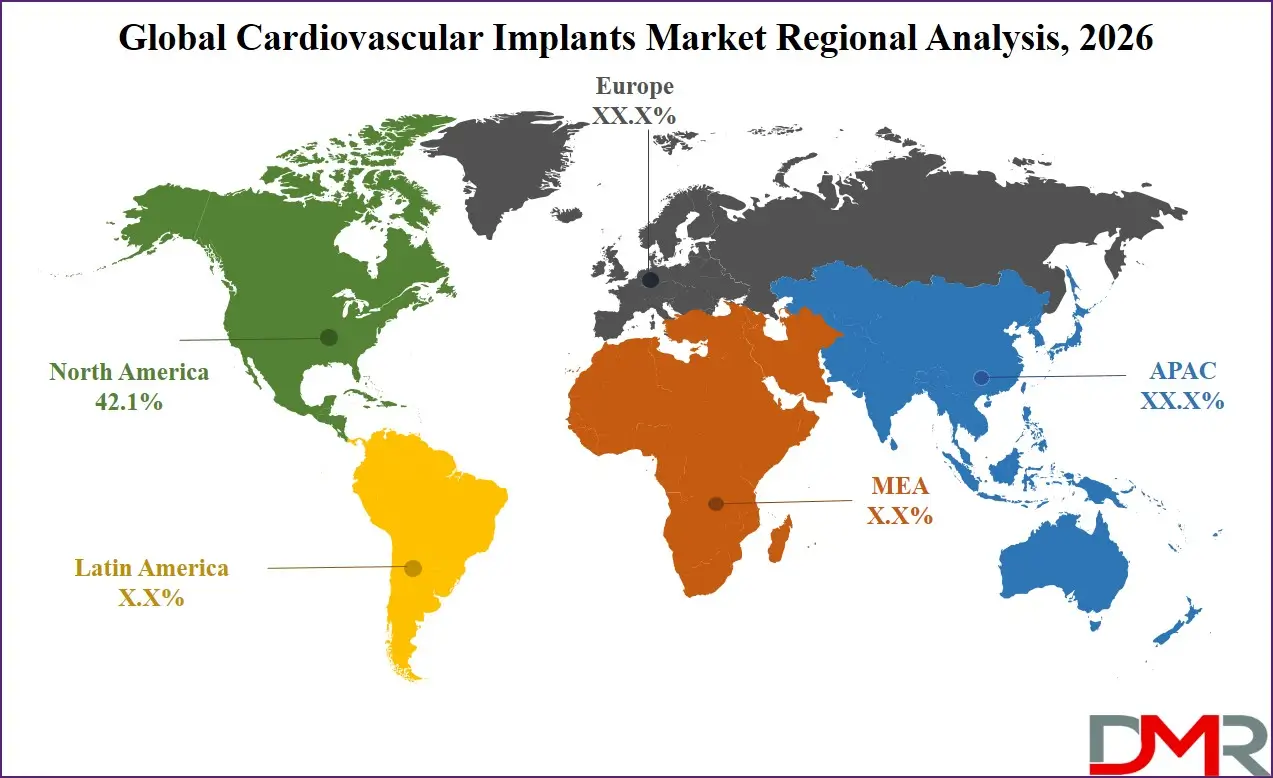

North America is projected to dominate the Global Cardiovascular Implants Market with 42.1% of market share by the end of 2026, owing to a powerful combination of high cardiovascular disease prevalence, mature interventional cardiology infrastructure, robust public and private insurance coverage, and the presence of dominant medical device innovators. The United States and Canada have rapidly integrated advanced implant technologies into comprehensive cardiac care pathways, tertiary hospital heart programs, and ambulatory surgery center expansion. Major manufacturers are scaling production capacity and distribution networks to meet sustained institutional and patient demand.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The region's aging population demographics, coupled with high obesity and diabetes prevalence and well-established screening programs, creates a durable multi-channel demand environment. Supportive Medicare coverage policies and gradual value-based payment model evolution further solidify North America's leadership position.

Region with the Highest CAGR

Asia-Pacific holds the highest CAGR of 12.3% and is poised to achieve rapid market share growth due to its massive population, rapidly expanding middle class, accelerating healthcare infrastructure investment, and emerging national cardiovascular disease control programs. Countries like China, India, Japan, and South Korea are investing heavily in comprehensive heart centers and interventional cardiology training programs. China's Healthy China 2030 initiative and India's National Program for Prevention and Control of Cancer, Diabetes, Cardiovascular Diseases and Stroke are creating fertile ground for government and institutional adoption. The region's cost sensitivity is being addressed through domestic manufacturing partnerships, tiered product portfolios, and scaled basic device configurations optimized for mass distribution. This, combined with immense urbanization-driven lifestyle changes and cardiovascular risk factor accumulation, positions APAC as the fastest-growing market for cardiovascular implant systems.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Global Cardiovascular Implants Market: Competitive Landscape

The Global Cardiovascular Implants Market is moderately consolidated, featuring a mix of established multinational medical device conglomerates, specialized cardiac rhythm management firms, and innovative structural heart technology developers. Leading medical device players Medtronic, Abbott Laboratories, and Boston Scientific are leveraging their comprehensive product portfolios, extensive clinical trial networks, and long-standing hospital relationships to capture institutional market share across all major implant categories. Pure-play structural heart innovators such as Edwards Lifesciences are driving market dynamics with mission-focused product development centered on transcatheter valve technologies.

Cardiac rhythm management specialists including Biotronik and MicroPort play increasingly influential roles in advancing pacemaker and ICD technologies through differentiated features and regional market strength. Emerging players in bioresorbable scaffolds, leadless pacing, and neuromodulation are also entering the space through strategic acquisitions and breakthrough technology designations, aiming to capture next-generation implant procedure adoption.

Some of the prominent players in the Global Cardiovascular Implants Market are:

- Medtronic plc

- Abbott Laboratories

- Boston Scientific Corporation

- Edwards Lifesciences Corporation

- Johnson & Johnson

- Biotronik SE & Co. KG

- Terumo Corporation

- LivaNova PLC

- MicroPort Scientific Corporation

- Zimmer Biomet Holdings, Inc.

- W. L. Gore & Associates, Inc.

- Cook Medical

- Lepu Medical Technology

- Meril Life Sciences

- B. Braun Melsungen AG

- Artivion, Inc.

- Abiomed, Inc.

- SynCardia Systems, LLC

- Berlin Heart GmbH

- OrbusNeich

- Other Key Players

Recent Developments in the Global Cardiovascular Implants Market

- August 2025: Medtronic plc received U.S. FDA approval for an expanded Redo-TAVR indication for its Evolut transcatheter aortic valve replacement system, enabling physicians to implant a new valve inside a previously implanted transcatheter valve, improving treatment options for patients experiencing valve degeneration.

- April 2025: Abbott Laboratories reported continued clinical adoption of its AVEIR dual-chamber leadless pacemaker system, designed to provide synchronized atrial and ventricular pacing while reducing complications associated with traditional pacemaker leads and surgical pockets.

- February 2025: Boston Scientific Corporation announced progress in the development of its pulsed field ablation technology for atrial fibrillation treatment, strengthening its electrophysiology portfolio and supporting the transition toward next-generation energy sources for cardiac rhythm management.

- October 2024: Edwards Lifesciences Corporation received CE Mark approval for its EVOQUE transcatheter tricuspid valve replacement system, expanding minimally invasive treatment options for patients suffering from severe tricuspid regurgitation and advancing structural heart therapy adoption in Europe.

- July 2024: Terumo Corporation expanded its interventional cardiology portfolio with advanced catheter-based technologies aimed at improving coronary intervention procedures, supporting the growing demand for minimally invasive treatments in complex cardiovascular cases.

- March 2024: Abiomed, Inc., a subsidiary of Johnson & Johnson, reported increased global adoption of its Impella heart pump systems used for temporary ventricular support during high-risk percutaneous coronary interventions and cardiogenic shock treatment.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 48.6 Bn |

| Forecast Value (2035) |

USD 102.2 Bn |

| CAGR (2026–2035) |

8.6% |

| The US Market Size (2026) |

USD 17.2 Bn |

| Historical Data |

2020 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Product Type (Coronary Stents, Implantable Cardioverter Defibrillators (ICDs), Heart Valves, Implanted Cardiac Pacemakers, Cardiac Resynchronization Therapy (CRT) Devices, Peripheral Stents, and Others), By Material (Metals & Alloys, Polymers, Biological Materials, and Others), By Procedure Type (Angioplasty and Open Heart Surgery), By Indication (Arrhythmias, Myocardial Ischemia, Acute Myocardial Infarction, Heart Failure, and Others), By End-User (Hospitals, Specialty Clinics, Ambulatory Surgical Centers, Cardiac Catheterization Laboratories, and Others) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia- Pacific– China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

Medtronic, Abbott Laboratories, Boston Scientific Corporation, Edwards Lifesciences Corporation, Johnson & Johnson, Biotronik SE & Co. KG, Terumo Corporation, LivaNova PLC, MicroPort Scientific Corporation, Zimmer Biomet Holdings, Inc., W. L. Gore & Associates, Inc., Cook Medical, Lepu Medical Technology, Meril Life Sciences, B. Braun Melsungen AG, Artivion, Inc., Abiomed, Inc., SynCardia Systems, LLC, Berlin Heart GmbH, OrbusNeich, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Cardiovascular Implants Market?

▾ The Global Cardiovascular Implants Market size is estimated to have a value of USD 48.6 billion in 2026 and is expected to reach USD 102.2 billion by the end of 2035.

What is the growth rate in the Global Cardiovascular Implants Market in 2026?

▾ The market is growing at a CAGR of 8.6% over the forecasted period of 2026.

What is the size of the US Cardiovascular Implants Market?

▾ The US Cardiovascular Implants Market is projected to be valued at USD 17.2 billion in 2026. It is expected to witness subsequent growth in the upcoming period as it holds USD 34.6 billion in 2035 at a CAGR of 8.1%.

Which region accounted for the largest Global Cardiovascular Implants Market?

▾ North America is expected to have the largest market share in the Global Cardiovascular Implants Market with a share of about 42.1% in 2026.

Who are the key players in the Global Cardiovascular Implants Market?

▾ Some of the major key players in the Global Cardiovascular Implants Market are Medtronic plc, Abbott Laboratories, Boston Scientific Corporation, Edwards Lifesciences Corporation, LivaNova PLC, and many others.