What is the Security Operations Center Market Size?

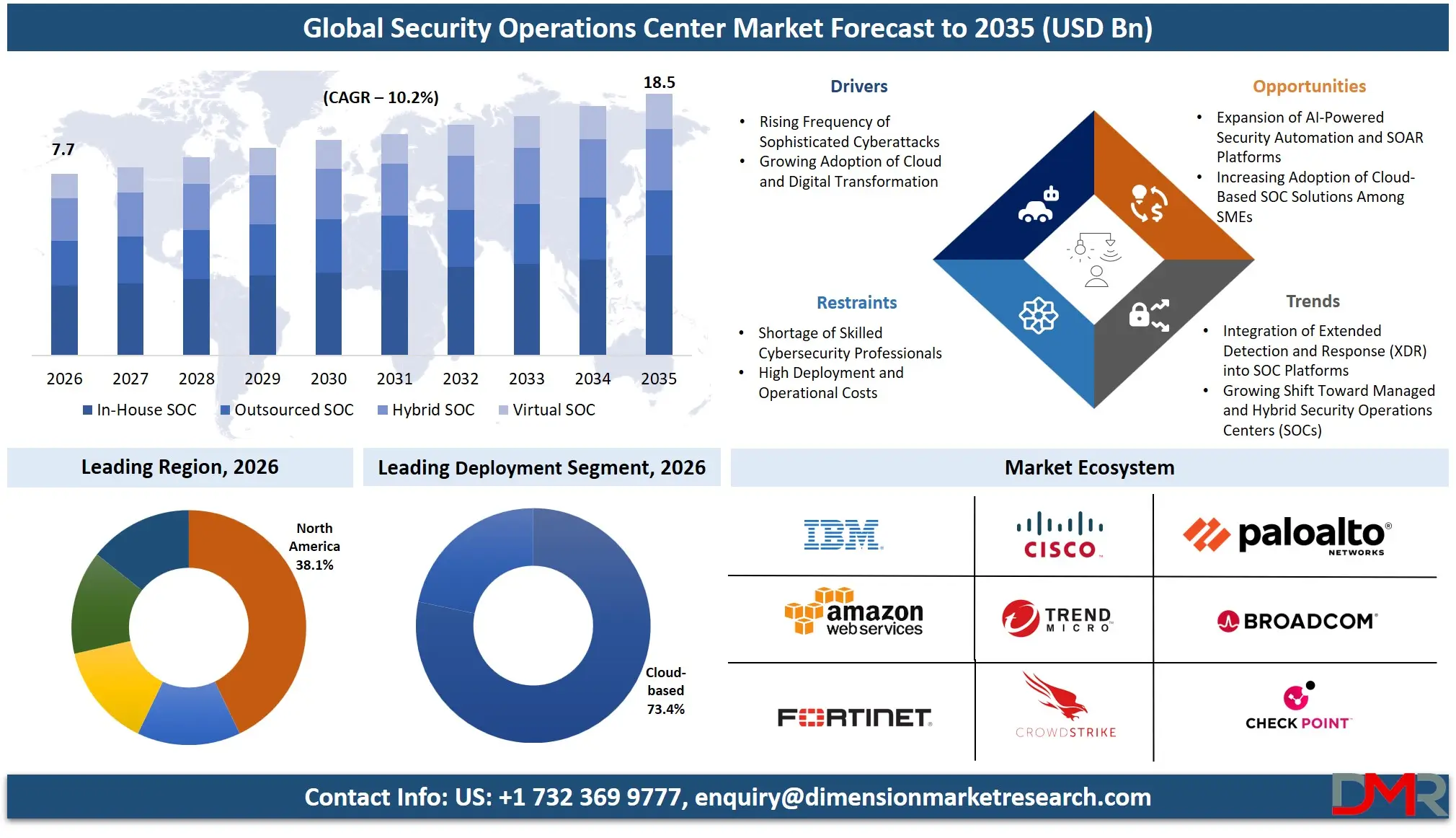

The Global Security Operations Center (SOC) Market is expected to reach a value of USD 7.7 billion in 2026, and it is further anticipated to reach USD 18.5 billion by 2035, growing at a CAGR of 10.2% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The SOC market has been growing at a high rate as enterprises face an escalating volume and sophistication of cyber threats, moving beyond perimeter-based defenses to intelligence-led, continuous security operations. The market consists of solutions and services that enable organizations to monitor, detect, investigate, and respond to security incidents across on-premises, cloud, and hybrid environments. The increasing complexity of multi-cloud architecture, the proliferation of ransomware, and the integration of AI-driven threat actors are driving the necessity of specialized SOC capabilities. Enterprises are the most frequent adopters, with cloud-based deployment remaining the most popular because of its scalability and lower upfront costs. The BFSI, government & defense, and healthcare industries are key players as they need continuous monitoring, rapid incident response, and strict compliance adherence within secure and highly available security ecosystems.

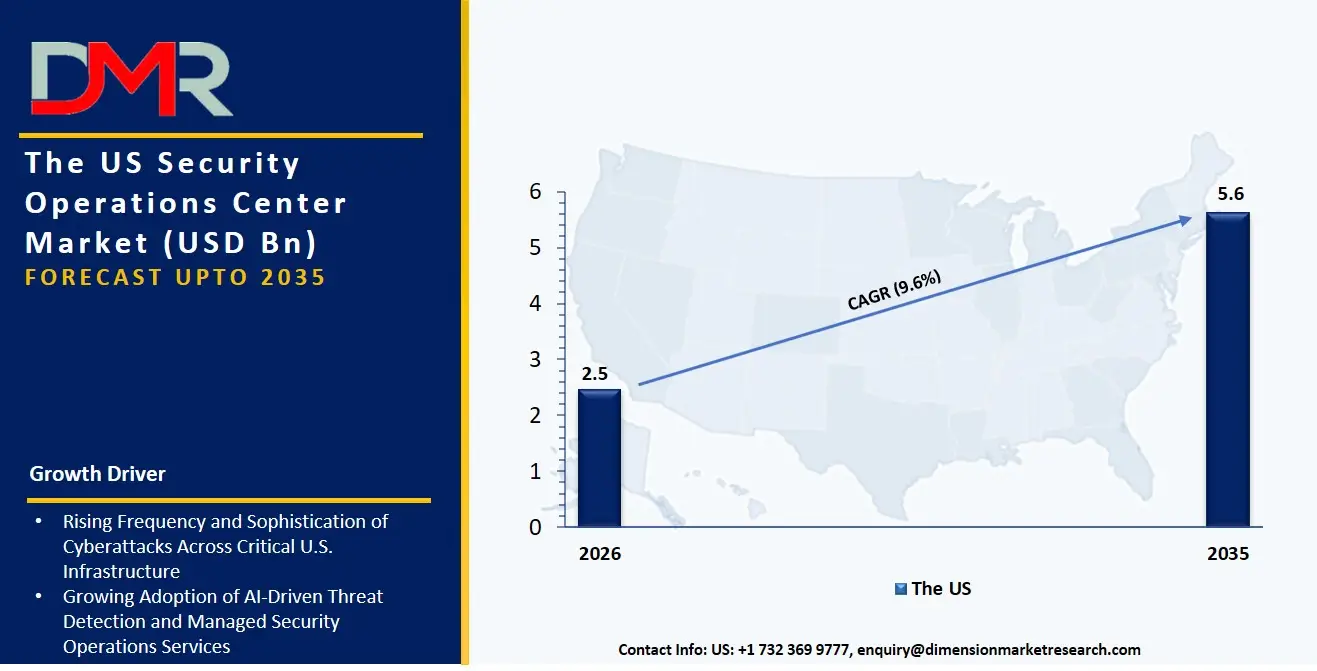

The US Security Operations Center Market

The US Security Operations Center (SOC) Market is projected to reach USD 2.5 billion in 2026 at a compound annual growth rate of 9.6% over its forecast period, culminating in a value of USD 5.6 billion by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US continues to be the largest and most mature market for SOC solutions, fueled by an aggressive threat landscape targeting Fortune 500 companies and critical national infrastructure. The market has been typified by high demand for Managed Security Services (MSS), whereby organizations are aimed at augmenting or fully outsourcing their security monitoring to address the acute cybersecurity skills shortage. Besides, the convergence of operational technology (OT) and IT networks is producing a similar need for specialized SOC services to monitor industrial control systems and ensure the resilience of manufacturing and energy sectors.

The Europe Security Operations Center Market

The Europe SOC Market is estimated to be valued at USD 2.3 billion in 2026 and is further anticipated to reach USD 5.3 billion by 2035 at a CAGR of 9.9%. The regulatory frameworks, including the NIS2 Directive and GDPR, have a significant impact on the European market and drive the need to employ robust Compliance Management and incident reporting services. Accelerated growth of Hybrid SOC deployments is also being experienced in the region as Germany's manufacturing and the UK's financial services industries are trying to strike a balance between data sovereignty requirements and cloud-based threat intelligence. In addition, initiatives such as sovereign clouds are challenging service providers to create dedicated security analytics solutions that provide data residency and interoperability across European cyber ecosystems.

The Japan Security Operations Center Market

The Japan SOC Market is projected to be valued at USD 893.2 million in 2026 at a CAGR of 9.1%. The Japanese market is unique, with a corporate drive to strengthen national cybersecurity posture ahead of global events and in response to a surge in supply chain attacks targeting its manufacturing base. Managed Security Services and Outsourced SOC models make up a large part of the spending as large conglomerates grapple with a severe shortage of cybersecurity professionals. There is also a strong need to deeply integrate security controls to bridge the gaps between legacy industrial systems and modern SaaS applications, which forms a niche in Identity & Access Management (IAM) and Network Detection & Response (NDR).

Key Takeaways

- Market Size & Forecast: The Global SOC market is projected to reach USD 7.7 billion in 2026, expanding steadily to USD 18.5 billion by 2035, fueled by the dual drivers of an unrelenting cyber threat landscape and the mandatory modernization of security architecture to support digital transformation.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 10.2%, driven by a critical shortage of skilled cybersecurity analysts and the escalating complexity of managing security across expanding attack surfaces, including cloud, edge, and IoT.

- Primary Growth Drivers: Key forces include the widespread shift from siloed security tools to integrated platforms like Extended Detection & Response (XDR), the need for continuous Monitoring & Detection to identify advanced persistent threats (APTs), and the adoption of Security Automation to bridge the human-machine gap in alert triage.

- Key Market Trends: Major trends include the rise of industry-specific SOC solutions (e.g., for healthcare IoT security), the use of AI-powered tools within SOAR platforms to auto-remediate low-level incidents, and the shift toward Threat Hunting as a proactive service to identify latent intrusions that evade automated defenses.

- By Deployment Analysis: Cloud-based SOC models are expected to dominate enterprise discussions due to scalability and cost-effectiveness. Professional services are increasingly required to build seamless integration layers that connect on-premise security appliances with cloud-native security analytics engines.

- By Enterprise Vertical Analysis: BFSI and Government & Defense are the most lucrative verticals due to stringent compliance and national security needs. Healthcare & Life Sciences is the fastest-growing sector as patient data protection and medical device security require robust vulnerability assessment and monitoring.

- Regional Leadership: North America is poised to dominate this market with 38.1% of the market share in 2026 due to its well-developed technological ecosystem that is the prime target for cybercrime and state-sponsored espionage, making it a leader in this market.

What is the Security Operations Center (SOC)?

A Security Operations Center is a centralized function that employs people, processes, and technology to continuously monitor and improve an organization's security posture while preventing, detecting, analyzing, and responding to cybersecurity incidents. Unlike a simple software purchase, a SOC represents an operational capability to manage the how of cybersecurity in real-time. This involves Monitoring & Detection to establish a 24/7 watch over all digital assets, Incident Response to contain and eradicate threats before they cause business disruption, and Threat Hunting to proactively search for unknown threats that bypass existing controls. With most organizations running hybrid IT environments, professional and managed services are needed to achieve continuous security monitoring, cost governance of security tooling, and performance tuning of detection rules, making SOC investments translate into a tangible business resilience, as opposed to a technical checkbox.

Use Cases

- Comprehensive Threat Detection in Banking: Banking institutions hire Managed Security Services (MSS) to operate a Hybrid SOC, combining on-premise SIEM for core banking system logs with cloud-based Threat Intelligence Platforms to correlate real-time transaction fraud with cyber intrusion attempts.

- Medical IoT Security in Healthcare: Hospital networks use Vulnerability Assessment & Management and Incident Response services to continuously monitor connected medical devices and life-support systems, ensuring patient safety by rapidly isolating compromised equipment from the IT network.

- Sovereign Data Protection in Government: Government agencies use Consulting and Integration & Deployment services to architect On-Premises SOC solutions that comply with stringent data residency legislation, ensuring citizen data never leaves a sovereign boundary, yet is protected by advanced Security Analytics.

- OT/IT Convergence in Manufacturing: Global manufacturers use NDR and IAM solutions, managed via a Virtual SOC, to integrate factory floor PLCs with enterprise networks, enabling the detection of anomalous lateral movement from IT malware to operational technology (OT) environments.

How AI is Transforming the Security Operations Center Market?

Comprehensive Threat Detection in Banking: Banking institutions hire Managed Security Services (MSS) to operate a Hybrid SOC, combining on-premise SIEM for core banking system logs with cloud-based Threat Intelligence Platforms to correlate real-time transaction fraud with cyber intrusion attempts.

Medical IoT Security in Healthcare: Hospital networks use Vulnerability Assessment & Management and Incident Response services to continuously monitor connected medical devices and life-support systems, ensuring patient safety by rapidly isolating compromised equipment from the IT network.

Sovereign Data Protection in Government: Government agencies use Consulting and Integration & Deployment services to architect On-Premises SOC solutions that comply with stringent data residency legislation, ensuring citizen data never leaves a sovereign boundary, yet is protected by advanced Security Analytics.

OT/IT Convergence in Manufacturing: Global manufacturers use NDR and IAM solutions, managed via a Virtual SOC, to integrate factory floor PLCs with enterprise networks, enabling the detection of anomalous lateral movement from IT malware to operational technology (OT) environments.

Market Dynamics

Key Drivers in the Global Security Operations Center Market

Rising Frequency of Sophisticated Cyberattacks

The growing volume and complexity of cyberattacks are significantly driving demand for Security Operations Centers (SOCs). Organizations across industries face persistent threats from ransomware, phishing, advanced persistent threats (APTs), insider attacks, and supply chain compromises. As digital assets become increasingly valuable, enterprises require continuous monitoring, rapid threat detection, and coordinated incident response to minimize operational disruptions and financial losses. SOCs provide centralized visibility across networks, cloud environments, endpoints, and applications, enabling organizations to identify malicious activity in real time. Increasing regulatory scrutiny and business continuity requirements further encourage investments in advanced SOC capabilities, strengthening market growth worldwide.

Growing Adoption of Cloud and Digital Transformation

Rapid cloud adoption and enterprise digital transformation initiatives are accelerating the need for advanced Security Operations Centers. Organizations increasingly operate hybrid and multi-cloud environments, expanding the cybersecurity attack surface and requiring continuous monitoring across distributed infrastructures. SOC platforms integrate cloud-native security tools, AI-driven analytics, and automated response capabilities to provide centralized visibility and improve operational efficiency. The widespread adoption of remote work, SaaS applications, IoT devices, and digital business platforms further increases cybersecurity complexity. Enterprises are investing in scalable SOC solutions to protect critical workloads, maintain regulatory compliance, and ensure resilient security operations across evolving digital ecosystems.

Restraints in the Global Security Operations Center Market

Shortage of Skilled Cybersecurity Professionals

A significant restraint affecting the Security Operations Center market is the global shortage of experienced cybersecurity professionals. Effective SOC operations require analysts, incident responders, digital forensics specialists, threat hunters, and security architects capable of managing increasingly sophisticated attacks. However, organizations struggle to recruit and retain qualified personnel due to rising demand and limited talent availability. This workforce gap leads to alert fatigue, slower incident response, and operational inefficiencies. Smaller organizations are particularly affected because they often lack the financial resources to build dedicated SOC teams, limiting widespread adoption despite growing cybersecurity risks.

High Deployment and Operational Costs

Establishing and maintaining a modern Security Operations Center requires substantial financial investment, limiting adoption among many organizations. Costs include advanced SIEM and SOAR platforms, endpoint security solutions, threat intelligence subscriptions, cloud infrastructure, skilled personnel, ongoing software licensing, compliance management, and continuous technology upgrades. Around-the-clock monitoring further increases operational expenses through staffing and infrastructure requirements. Small and medium-sized enterprises often find these investments difficult to justify despite increasing cyber threats. Budget constraints can delay SOC implementation or encourage reliance on limited security capabilities, restricting overall market growth in cost-sensitive industries and developing economies.

Growth Opportunities in the Global Security Operations Center Market

Expansion of AI and Security Automation

Artificial intelligence and security automation present significant growth opportunities for the Security Operations Center market. AI-powered analytics enhance threat detection accuracy by identifying abnormal behavior, prioritizing high-risk alerts, and reducing false positives. Automation through SOAR platforms accelerates incident investigation, response, and remediation while improving operational efficiency. These technologies enable SOC teams to manage increasing alert volumes without proportionally expanding staff. As organizations seek faster response times and stronger cyber resilience, investments in intelligent automation continue to grow. Vendors integrating machine learning, behavioral analytics, and automated workflows are well positioned to capture future market demand.

Increasing Demand from Small and Medium Enterprises

Small and medium enterprises represent a major growth opportunity as cyber threats increasingly target organizations with limited security resources. Cloud-based SOC platforms, managed detection and response services, and subscription-based security offerings enable SMEs to access enterprise-grade cybersecurity capabilities without building expensive in-house infrastructure. Governments and industry regulators are also encouraging stronger cybersecurity practices among smaller businesses through compliance initiatives and awareness programs. As SMEs accelerate digital transformation, cloud adoption, and e-commerce expansion, demand for affordable, scalable, and managed Security Operations Center solutions is expected to increase substantially across both developed and emerging markets.

Trends in the Global Security Operations Center Market

Integration of XDR and Unified Security Platforms

A major trend in the Security Operations Center market is the growing integration of Extended Detection and Response (XDR) with unified security platforms. Organizations increasingly seek centralized visibility across endpoints, networks, cloud environments, email systems, and identities through integrated cybersecurity ecosystems. XDR consolidates security telemetry from multiple sources, enabling faster threat detection, improved correlation, and automated response. This unified approach reduces tool complexity, minimizes alert fatigue, and improves analyst productivity. Vendors continue expanding platform capabilities by integrating AI, threat intelligence, and orchestration technologies to deliver more comprehensive and efficient security operations.

Shift Toward Managed and Hybrid Security Operations Centers

Organizations are increasingly adopting managed and hybrid Security Operations Center models to address cybersecurity talent shortages and rising operational complexity. Managed Security Service Providers deliver continuous monitoring, incident response, threat intelligence, and compliance support while reducing infrastructure and staffing costs. Hybrid SOCs combine internal security teams with external expertise, offering greater flexibility and access to advanced cybersecurity technologies. This approach enables organizations to maintain strategic control while benefiting from specialized knowledge and 24/7 monitoring capabilities. Growing demand for cost-effective, scalable, and resilient cybersecurity services continues to accelerate the adoption of managed and hybrid SOC solutions globally.

Research Scope and Analysis

The Global Security Operations Center Market is segmented by Component, SOC Type, Deployment, Organization Size, Service Model, Security Type, and Enterprise Vertical, covering solutions and services, multiple SOC operating models, deployment environments, enterprise sizes, security functions, protection categories, and major end-use industries including BFSI, government, healthcare, IT, manufacturing, retail, energy, transportation, media, and education.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

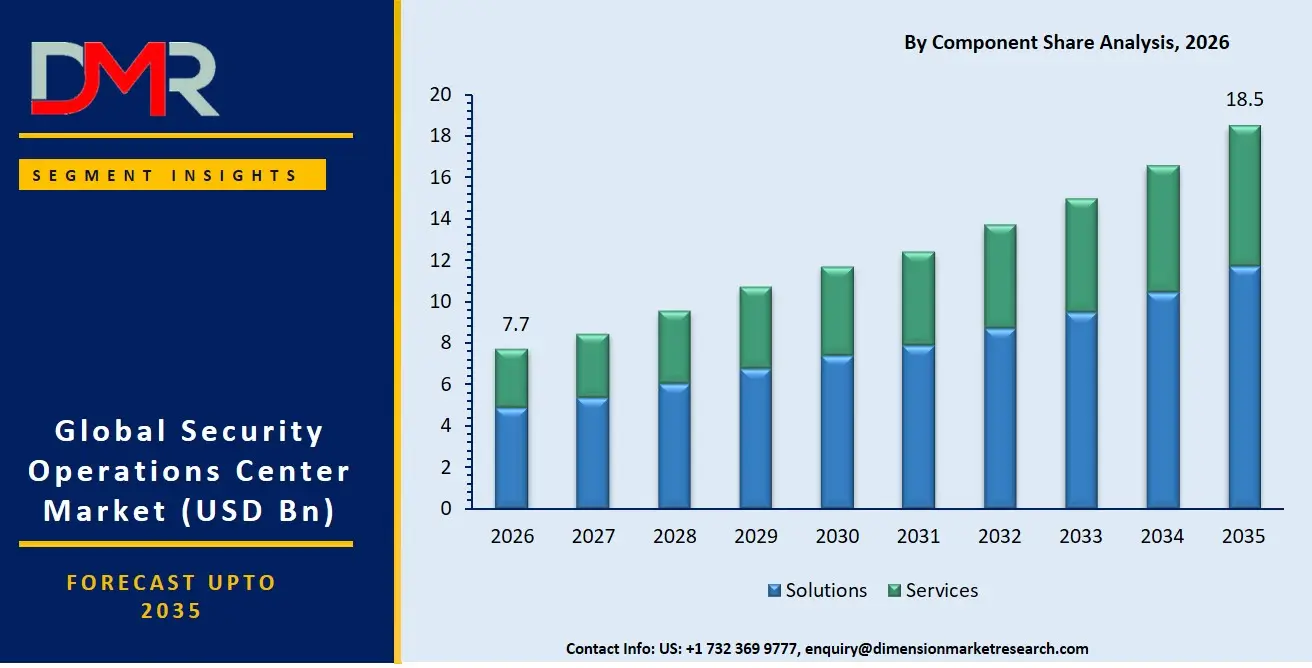

By Component Analysis

The Solutions segment is poised to dominates the global Security Operations Center (SOC) market because organizations prioritize advanced cybersecurity platforms that enable continuous monitoring, real-time threat detection, automated response, and centralized security management.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Solutions such as SIEM, SOAR, EDR, XDR, and threat intelligence platforms form the technological foundation of modern SOCs, allowing enterprises to manage increasingly sophisticated cyber threats efficiently. Rising ransomware attacks, cloud migration, regulatory compliance requirements, and the adoption of AI-driven security analytics have accelerated investments in integrated SOC solutions. Compared with services, software platforms provide scalable, long-term security capabilities, making solutions the largest revenue-generating component across enterprises, government agencies, financial institutions, healthcare organizations, and critical infrastructure operators.

By SOC Type Analysis

The Hybrid SOC segment is expected to dominate the market because it combines the strengths of in-house security expertise with outsourced managed security services. This model enables organizations to maintain control over sensitive security operations while leveraging external specialists for continuous monitoring, threat intelligence, and incident response. Hybrid SOCs provide greater scalability, cost efficiency, and access to advanced cybersecurity technologies without requiring organizations to build extensive internal teams. As cyber threats become more sophisticated and security talent shortages persist globally, enterprises increasingly adopt hybrid SOC models to improve operational resilience, accelerate incident response, and ensure 24/7 protection while meeting regulatory and industry-specific compliance requirements.

By Deployment Analysis

The Cloud-Based deployment is projected to segment dominates the Security Operations Center market due to increasing enterprise migration to cloud infrastructure and hybrid IT environments. Cloud-based SOC platforms provide faster deployment, centralized visibility, remote accessibility, automated updates, AI-powered analytics, and lower infrastructure costs than traditional on-premises systems. Organizations benefit from elastic scalability that supports growing security workloads while enabling rapid response to evolving cyber threats. The widespread adoption of SaaS applications, multi-cloud environments, and remote work has further increased demand for cloud-native SOC capabilities. Continuous innovation by leading cloud providers also strengthens the dominance of cloud-based security operations across industries worldwide.

By Organization Size Analysis

Large Enterprises is expected to dominate the global Security Operations Center market because they manage extensive IT infrastructures, valuable digital assets, and complex cybersecurity risks across multiple locations. These organizations face higher exposure to ransomware, advanced persistent threats, insider attacks, and regulatory compliance requirements, driving significant investments in dedicated SOC capabilities. Large enterprises possess greater financial resources to deploy advanced SIEM, SOAR, XDR, threat intelligence, and managed security solutions while maintaining skilled cybersecurity teams. Their ongoing investments in digital transformation, cloud computing, artificial intelligence, and critical infrastructure protection continue to generate the highest spending on comprehensive security operations compared with small and medium enterprises.

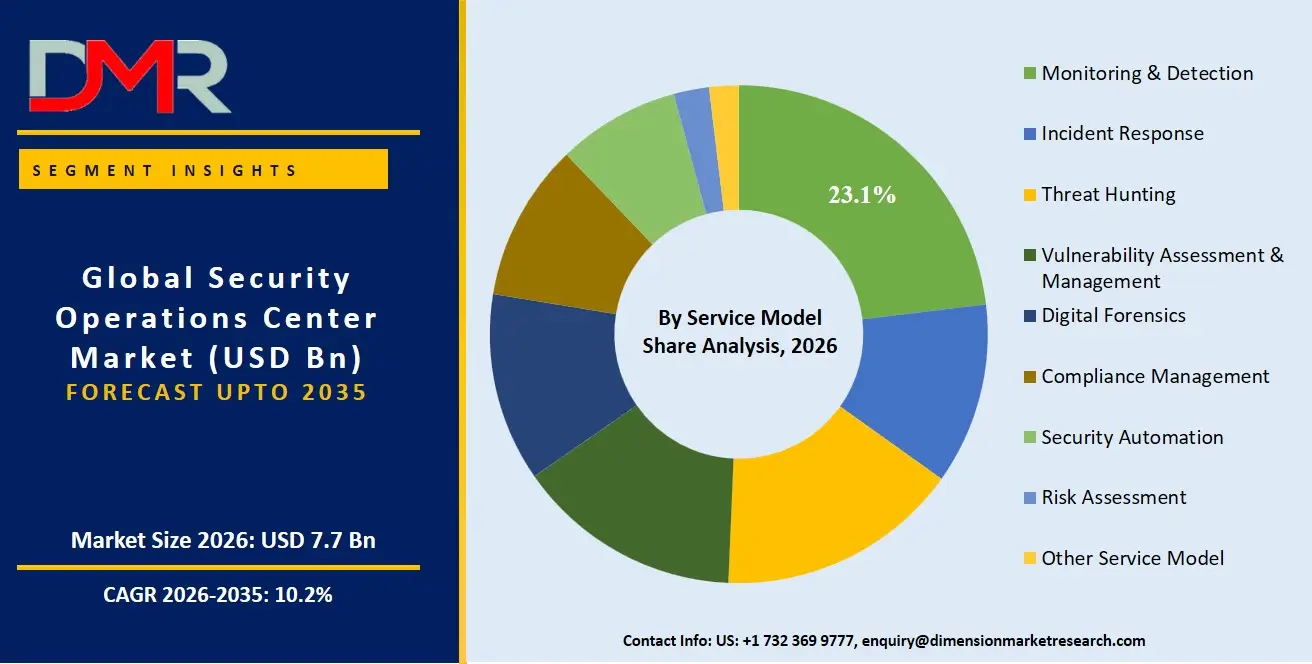

By Service Model Analysis

The Monitoring & Detection segment is projected to dominate the SOC market because continuous surveillance is the primary function of every security operations center. Organizations require real-time monitoring of networks, endpoints, cloud environments, applications, and user activities to identify suspicious behavior before attacks escalate into major incidents. Advanced analytics, AI, threat intelligence, and automated alert management significantly improve detection accuracy while reducing response times. Continuous monitoring is essential for maintaining regulatory compliance, minimizing operational disruptions, and protecting critical digital assets. Since proactive threat identification forms the foundation for all subsequent security operations, monitoring and detection account for the largest share of SOC service demand.

By Security Type Analysis

Network Security is expected to dominate the global Security Operations Center market because enterprise networks remain the primary target for cyberattacks, including ransomware, malware, phishing, distributed denial-of-service attacks, and unauthorized access attempts. SOC teams continuously monitor network traffic, firewalls, intrusion detection systems, and network behavior analytics to identify and contain threats before they spread across organizational environments. As enterprises expand hybrid work, cloud connectivity, and interconnected digital ecosystems, securing network infrastructure becomes increasingly critical. Continuous investments in network visibility, segmentation, zero-trust architectures, and advanced threat detection technologies reinforce network security's leadership within modern SOC operations.

By Enterprise Vertical Analysis

The Banking, Financial Services & Insurance (BFSI) segment is projected to dominate the Security Operations Center market due to its high exposure to financial fraud, ransomware, identity theft, data breaches, and sophisticated cyberattacks. Financial institutions process enormous volumes of sensitive customer and transaction data, making continuous threat monitoring and rapid incident response essential. Strict regulatory frameworks and compliance standards further drive investments in advanced SOC capabilities, including SIEM, SOAR, AI-powered threat detection, and digital forensics. Increasing digital banking adoption, mobile payment platforms, fintech integration, and cloud-based financial services continue to strengthen BFSI's position as the largest end-user of Security Operations Center solutions.

The Global Security Operations Center Market Report is segmented on the basis of the following:

By Component

- Solutions

- Security Information and Event Management (SIEM)

- Security Orchestration, Automation & Response (SOAR)

- Threat Intelligence Platforms

- Endpoint Detection & Response (EDR)

- Extended Detection & Response (XDR)

- Network Detection & Response (NDR)

- Identity & Access Management (IAM)

- Log Management & Analytics

- Security Analytics

- Other Solutions

- Services

- Professional Services

- Consulting

- Integration & Deployment

- Training & Support

- Managed Security Services (MSS)

By SOC Type

- In-House SOC

- Outsourced SOC

- Hybrid SOC

- Virtual SOC

By Deployment

By Organization Size

- Large Enterprises

- Small & Medium Enterprises (SMEs)

By Service Model

- Monitoring & Detection

- Incident Response

- Threat Hunting

- Vulnerability Assessment & Management

- Digital Forensics

- Compliance Management

- Security Automation

- Risk Assessment

- Other Service Model

By Security Type

- Network Security

- Endpoint Security

- Cloud Security

- Application Security

- Identity Security

- Data Security

- IoT Security

By Enterprise Vertical

- Banking, Financial Services & Insurance (BFSI)

- Government & Defense

- Healthcare & Life Sciences

- IT & Telecommunications

- Manufacturing

- Retail & E-commerce

- Energy & Utilities

- Transportation & Logistics

- Media & Entertainment

- Education

- Other Verticals

Regional Analysis

Leading Region by Market Share

ℹ

To learn more about this report –

Download Your Free Sample Report Here

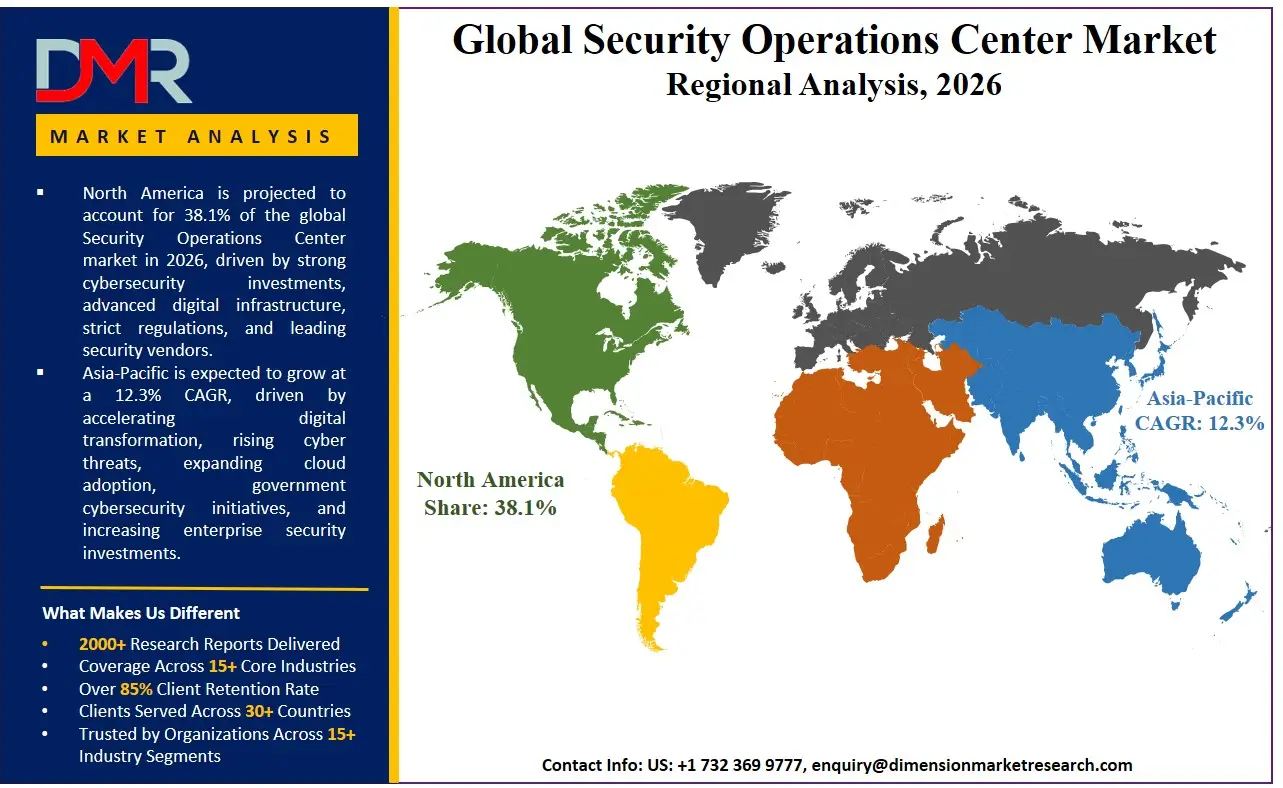

North America is poised to dominate the global SOC market as it is projected to hold 38.1% of the market share by the end of 2026. The United States, which dominates North America, has the highest share in the SOC market because of the unmatched concentration of hyperscale cloud platforms, the world's most targeted digital infrastructure, and the aggressive modernization agendas of Fortune 500 companies. The area has an established ecosystem of global system integrators, specialized MSS providers, and a deep pool of talent in threat intelligence and incident response. Enterprise investment in artificial intelligence-driven defense, advanced threat hunting, and the overall consolidation of legacy SIEM tools contribute to the continued demand for XDR platforms and managed services along with continuous security optimization. Moreover, a mature venture capital climate persistently finances upcoming cloud-native security vendors that need expert professional services to achieve rapid deployment and help their clients become compliant.

Fastest-Growing Regional Market

Asia-Pacific is expected to be the most rapidly expanding SOC market, driven by government-led sweeping national cybersecurity initiatives and digital transformation in India, China, Japan, and Southeast Asia. The fast-paced economic growth, the rise of a digital-first middle-income population, and the dynamic expansion of the e-commerce economy is compelling established conglomerates and state agencies to discard unproductive legacy antivirus and firewall-only defenses. Consulting and Managed Security Services are in high demand to help these large organizations pivot in the direction of 24/7 SOC operating models. There is also a severe lack of qualified cybersecurity analysts in the region, making it necessary to outsource security operations to MSS and Hybrid SOC models to cover the skills gap and enable the faster protection of new cloud investments.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive environment of the global SOC market has become highly dynamic with a heterogeneous array of multinational managed security service providers (MSSPs), the security divisions of large hyperscalers, and niche cloud-native SOC consultancies. The key to success will be deep strategic alliances with SIEM and XDR platform vendors like Splunk, Microsoft, or CrowdStrike because they will open the necessary co-marketing opportunities and early access to new detection capabilities. The movement towards market consolidation is rapidly progressing, with traditional IT outsourcing companies acquiring boutique incident response and threat intelligence firms to stay afloat. Proprietary intellectual property, including automated threat hunting frameworks and industry-specific detection content libraries, is becoming a more important basis of competitive differentiation than just labor arbitrage or generic security monitoring.

Some of the prominent players in the Global Security Operations Center Market are:

- IBM

- Microsoft

- Cisco Systems

- Palo Alto Networks

- Fortinet

- CrowdStrike

- Check Point Software Technologies

- Trend Micro

- Broadcom

- Google Cloud

- Amazon Web Services

- AT&T Cybersecurity

- BAE Systems

- Secureworks

- Rapid7

- SentinelOne

- Arctic Wolf Networks

- Sophos

- Trellix

- Splunk

- Other Key Players

Recent Developments

- December 2025: Amazon Web Services announced new Security, Identity & Compliance enhancements at AWS re:Invent 2025, including updates to Amazon Security Lake and related security services to improve centralized threat detection, analytics, and cloud security operations.

- January 2025: IBM and Palo Alto Networks released a global cybersecurity study highlighting the growing importance of security platform consolidation to reduce operational complexity across hybrid cloud and AI environments, reinforcing demand for integrated SOC platforms.

- May 2024: IBM and Palo Alto Networks announced a strategic cybersecurity partnership under which Palo Alto Networks agreed to acquire IBM's QRadar SaaS assets. The collaboration includes AI-powered security offerings, migration of QRadar customers to Cortex XSIAM, and the establishment of a joint Security Operations Center (SOC).

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 7.7 Bn |

| Forecast Value (2035) |

USD 18.5 Bn |

| CAGR (2026–2035) |

10.2% |

| The US Market Size (2026) |

USD 2.5 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Component, By SOC Type, By Deployment, By Organization Size, By Service Model, By Security Type, By Enterprise Vertical |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Security Operations Center Market?

▾ The Global Security Operations Center market is poised to be valued at USD 7.7 billion in 2026 and is projected to reach USD 18.5 billion by 2035, driven by the universal need for specialized skills in continuous threat monitoring, incident response, and the management of complex security tools.

What is the CAGR of the Global Security Operations Center Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 10.2% from 2026 to 2035, reflecting the accelerating complexity of the enterprise threat landscape and the persistent shortage of internal cybersecurity talent.

What factors are driving the growth of the Global Security Operations Center Market?

▾ Key drivers include the global cybersecurity skills gap, the imperative to modernize detection from legacy SIEM to AI-driven XDR platforms, the management complexity of multi-cloud security, and the surge in demand for Compliance Management amid evolving data sovereignty and breach notification laws.

Which region held the largest share of the Security Operations Center Market in 2026?

▾ North America is projected to hold 38.1% of market share in 2026, driven by a mature hyperscaler ecosystem, a highly targeted digital economy, and aggressive enterprise investment in Managed Security Services and AI-driven threat detection capabilities.

Which region is expected to grow the fastest in the Security Operations Center Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid digital transformation and national cybersecurity initiatives in India, China, and Japan, where Managed Security Services are critical for protecting expanding digital infrastructure against a surge in ransomware.

What are the major trends in the Global Security Operations Center Market?

▾ Major trends include the integration of Generative AI into security analysts' workflows, the rise of Threat Exposure Management, the demand for industry-specific SOC solutions (e.g., for OT/IoT security), and the focus on consolidating security tooling onto XDR platforms.

Who are the key players in the Global Security Operations Center Market?

▾ Key players include Global System Integrators and MSSPs like IBM, NTT Security, and Secureworks, as well as the security divisions of hyperscalers like Microsoft, AWS, and Google Cloud, alongside specialized pure-play security consultancies like CrowdStrike and Palo Alto Networks.

How is the Global Security Operations Center Market segmented?

▾ The market is segmented by Component, SOC Type, Deployment, Organization Size, Service Model, Security Type, and Enterprise Vertical.