What is the Network Security Market Size?

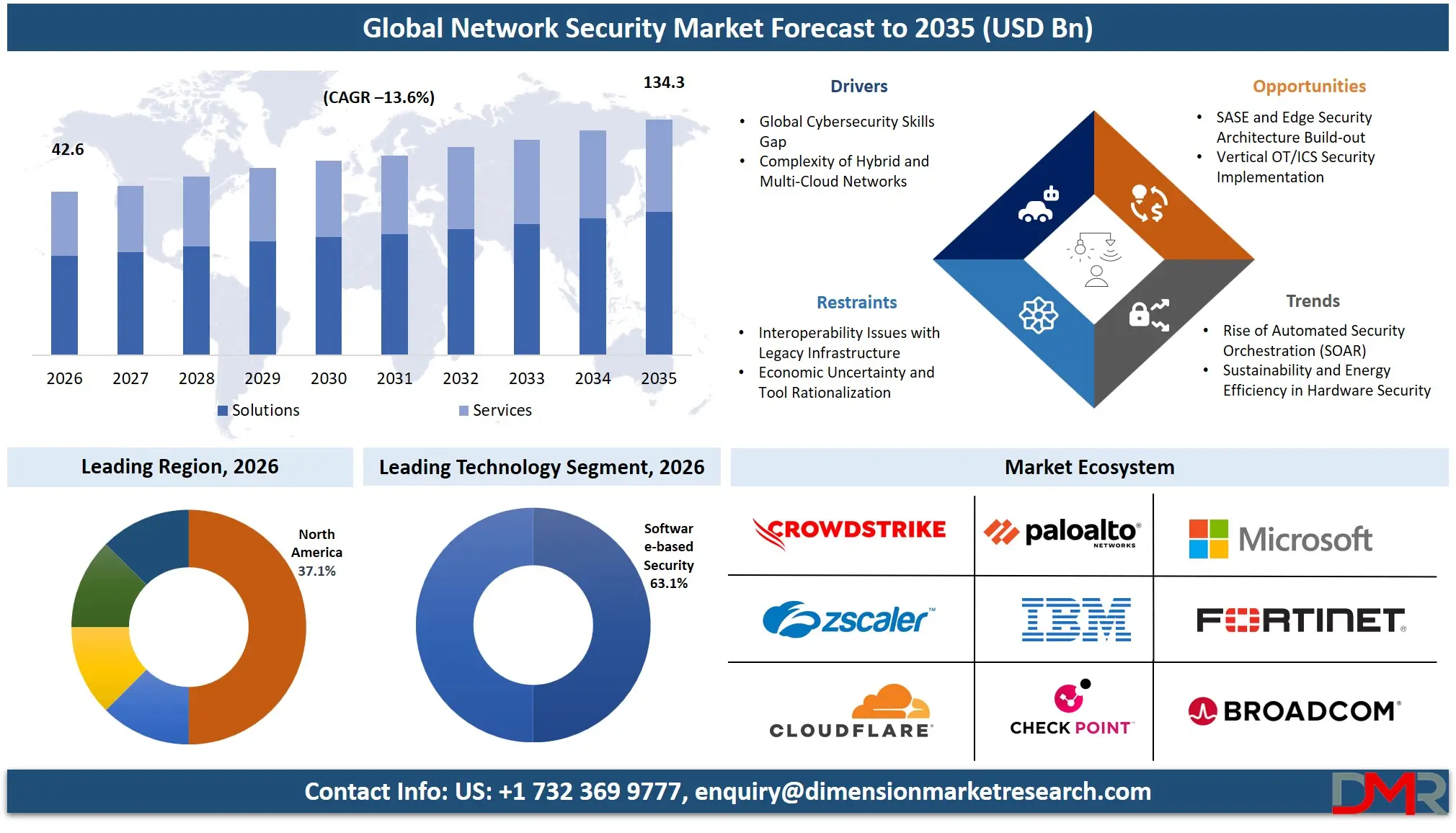

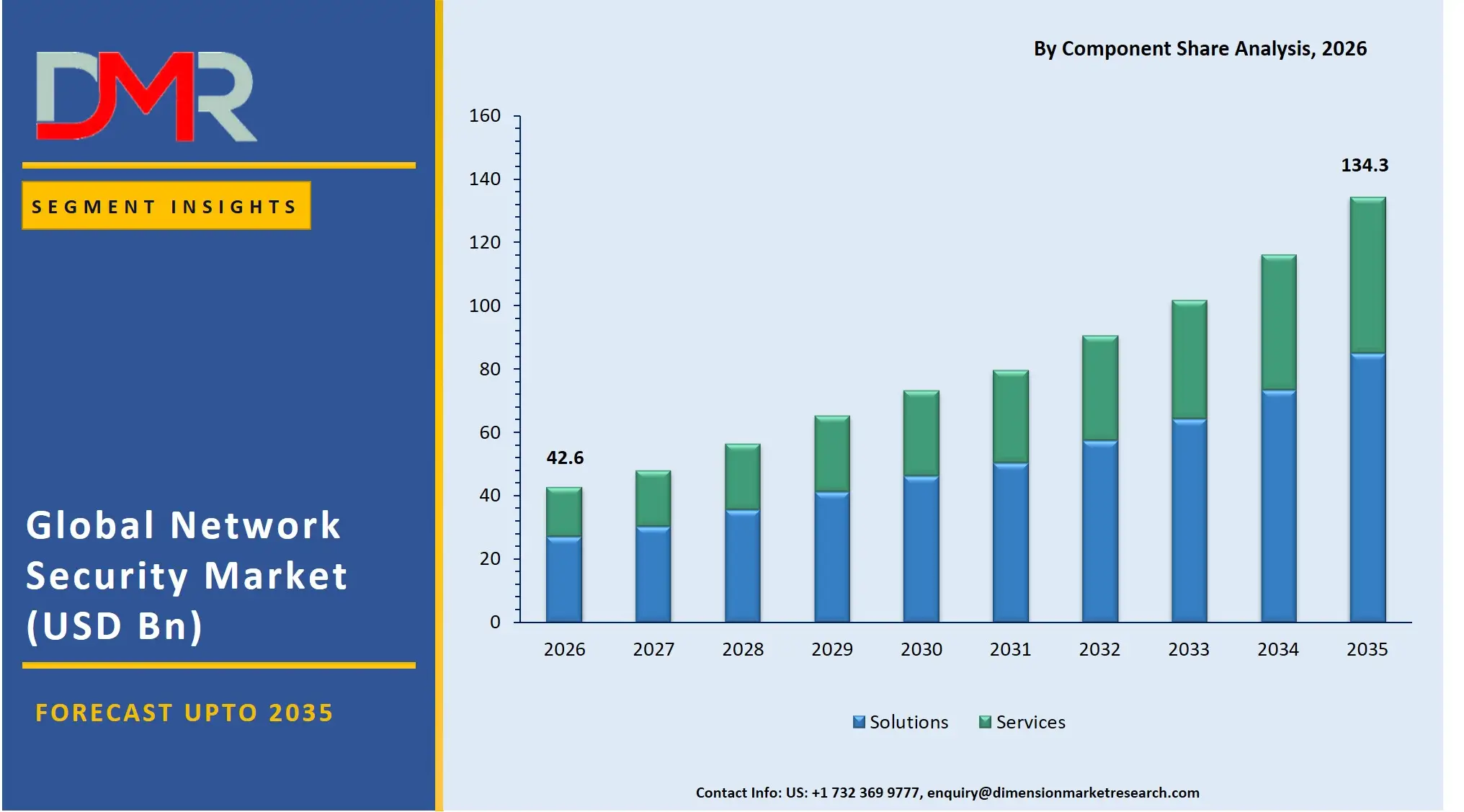

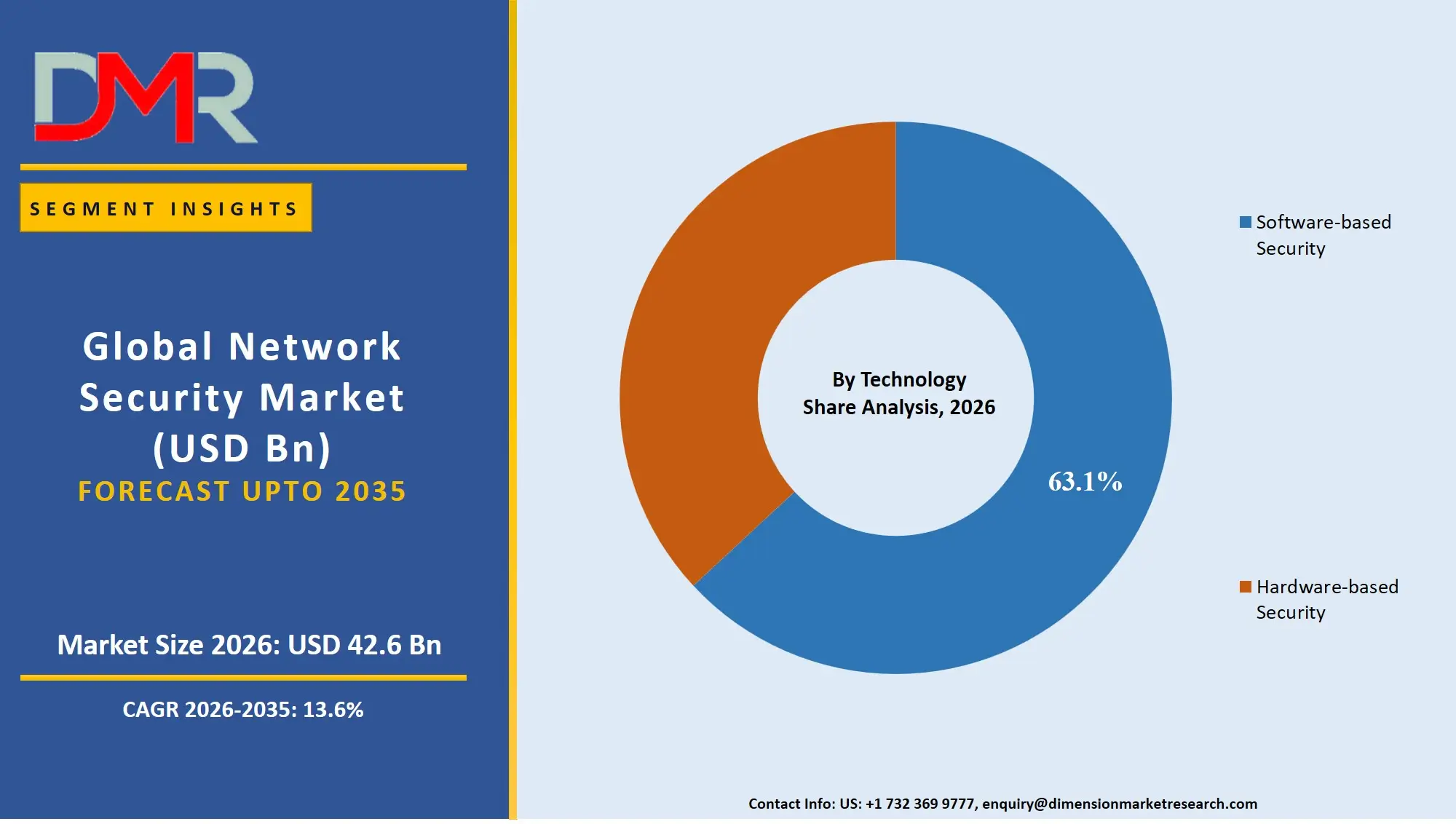

The Global Network Security Market size is expected to reach a value of USD 42.6 billion in 2026, and it is further anticipated to reach USD 134.3 billion by 2035, growing at a CAGR of 13.6% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The network security market has been growing at a high rate with enterprises accelerating their digital transformation and transitioning from traditional perimeter-based defenses to zero-trust architectures. The market consists of firewall, intrusion detection and prevention systems (IDS/IPS), secure web gateway (SWG), and managed security services which assist organizations in securing public, private, and hybrid cloud environments.

The increasing sophistication of ransomware, state-sponsored cyberattacks, and AI-powered threats is driving the necessity of specialized network security solutions. Large enterprises are the most frequent adopters, with hardware-based and cloud-based security models remaining popular because of their layered defense capabilities and scalability. The BFSI, government & defense, healthcare, and energy & utilities industries are key players as they need secure, compliant, and resilient network ecosystems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

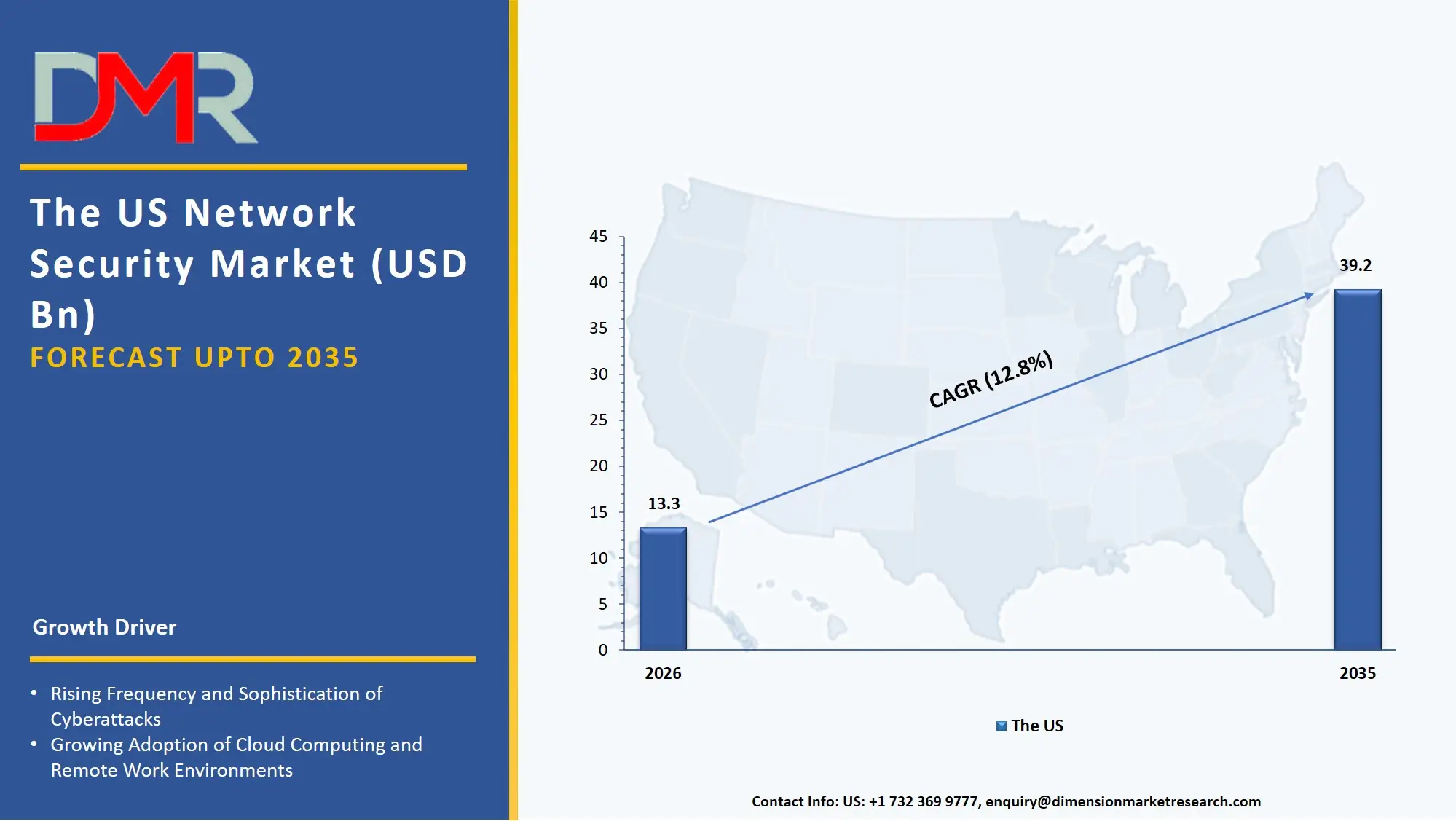

The US Network Security Market

The US Network Security Market is projected to reach USD 13.3 billion in 2026 at a compound annual growth rate of 12.8% over its forecast period, which is further projected to be valued at USD 39.2 billion by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US continues to be the largest and most developed market in network security due to the aggressive modernization efforts of critical national infrastructure and the growing distribution of hyperscale data centers. The market has been typified by high demand for Intrusion Detection & Prevention Systems (IDS/IPS) and DDoS Mitigation solutions, whereby organizations are aimed at defending against volumetric attacks and sophisticated application-layer exploits. Besides, the implementation of Generative AI tools in cyberattack workflows is producing a similar need in Managed Security Services to regulate real-time threat hunting and AI-driven incident response on the network.

The Europe Network Security Market

The Europe Network Security Market is estimated to be valued at USD 12.3 billion in 2026 and is further anticipated to reach USD 38.1 billion by 2035 at a CAGR of 13.4%. The regulatory frameworks including GDPR, NIS2 Directive, and the upcoming EU Cyber Resilience Act have a significant impact on the European market and drive the need to employ Data Loss Prevention (DLP) and Secure Web Gateway (SWG) solutions. Accelerated growth of Cloud-based security deployment is also being experienced in the region as manufacturing and automotive industries in Germany and France are trying to strike a balance in operational technology (OT) network security with IT-based analytics. In addition, efforts such as GAIA-X are challenging security service providers to create dedicated Professional Services to ensure data sovereignty and interoperability across European cloud and network ecosystems.

The Japan Network Security Market

The Japan Network Security Market is projected to be valued at USD 4.3 billion in 2026. It is further expected to witness robust growth, holding USD 13.1 billion in 2035 at a CAGR of 13.2%. The Japanese market is unique, with a corporate drive to strengthen national cybersecurity posture in response to rising geopolitical tensions and outdated legacy IT infrastructure. Unified Threat Management (UTM) and Managed Security Services make up a large part of the spending as large conglomerates seek to consolidate security tools and outsource monitoring of mission-critical networks. There is also a strong need to integrate deeply in the local market to bridge the gaps between old Electronic Medical Record (EMR) systems and industrial control systems to new cloud-based security platforms, which forms a niche in Network Access Control (NAC) and security workflow automation.

Key Takeaways

- Market Size & Forecast: The Global Network Security market is projected to reach USD 42.6 billion in 2026, expanding dramatically to USD 134.3 billion by 2035, fueled by the dual drivers of escalating ransomware attacks and the mandatory security overhaul of hybrid work infrastructure.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 13.6%, driven by a critical shortage of in-house cybersecurity analysts and the escalating complexity of managing security across distributed cloud edges and IoT devices.

- Primary Growth Drivers: Key forces include the widespread migration from on-premises data centers to zero-trust cloud models, the need for Firewall and IDS/IPS solutions to prevent costly data breaches, and the integration of DevSecOps pipelines requiring specialized Managed Security Services skills.

- Key Market Trends: Major trends include the rise of Secure Access Service Edge (SASE) frameworks converging network and security, the use of AI-powered tools within DDoS Mitigation services to auto-remediate traffic anomalies, and the shift toward Managed Detection and Response (MDR) as boards prioritize 24/7 network vigilance.

- By Deployment Mode Analysis: Cloud-based security models are expected to dominate enterprise discussions due to remote workforces and edge computing constraints.

- By Industry Vertical Analysis: BFSI (Banking, Financial Services and Insurance) are expected to dominate this segment due to stringent national security and compliance needs.

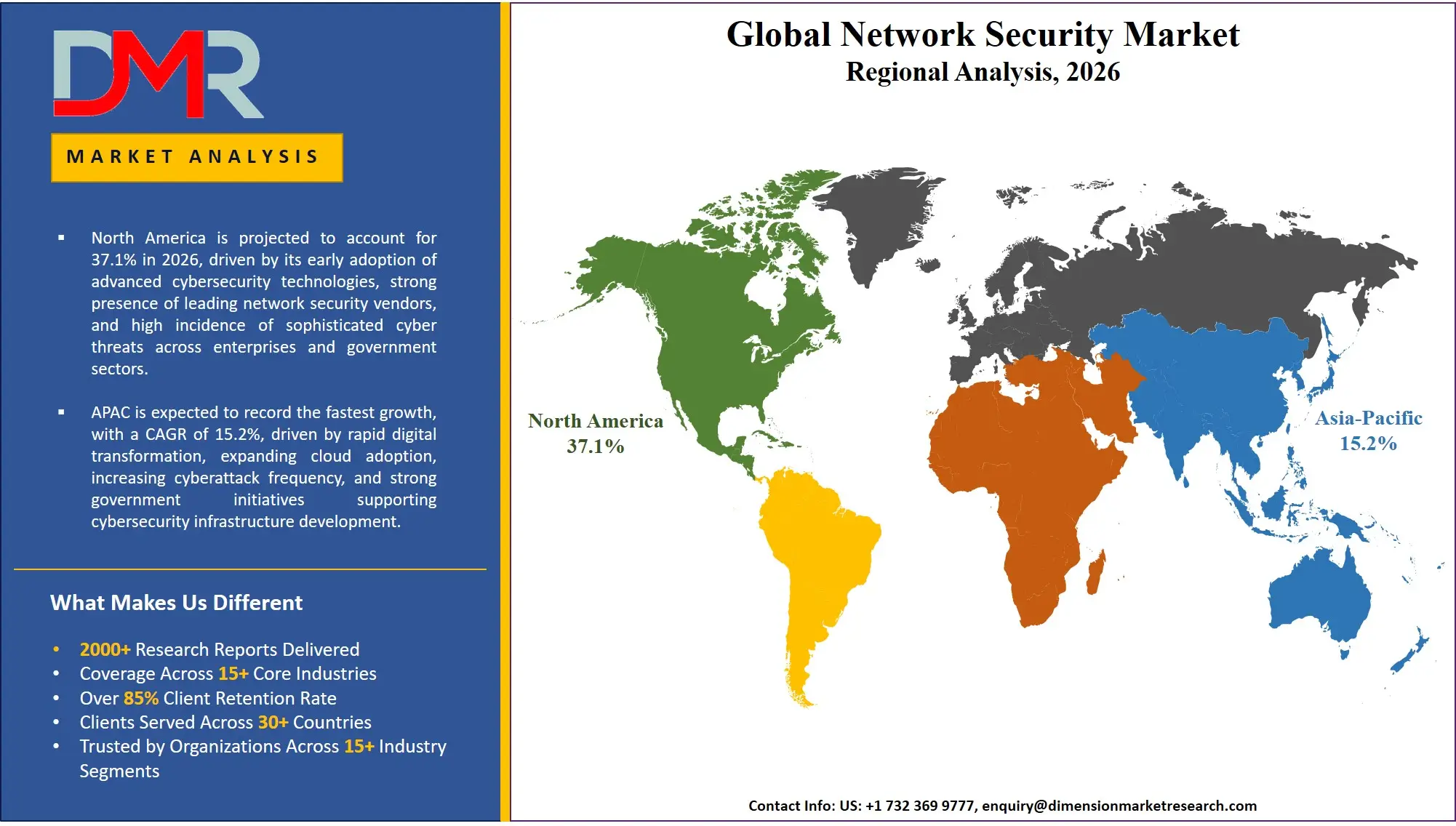

- Regional Leadership: North America is poised to dominate this market with 37.1% of the market share in 2026 due to its well-developed technological ecosystem and the high concentration of Fortune 500 companies that are prime targets for advanced persistent threats (APTs).

What is Network Security?

Network Security consists of the specialized hardware, software, and managed services that are deployed by enterprises, government agencies, and third-party experts to protect the integrity, confidentiality, and availability of data traversing computer networks. These solutions, unlike endpoint or application security, are specifically focused on the pipes and gateways of digital communication. This involves Solutions such as Firewalls to enforce strict access control perimeters, Intrusion Detection & Prevention Systems (IDS/IPS) to actively block malicious traffic signatures, and DDoS Mitigation appliances to absorb volumetric attacks. With over 90% of organizations operating hybrid network architectures, professional and managed security services are needed to achieve end-to-end encryption, zero-trust micro-segmentation, and continuous compliance monitoring, making security investments translate into tangible business resilience, as opposed to a simple box-ticking exercise.

Use Cases

- Zero-Trust Segmentation in Banking: Banking institutions deploy internal Firewalls and Network Access Control (NAC) solutions to move from flat, vulnerable networks to a micro-segmented architecture, ensuring that a compromise in one loan application server cannot laterally move to core mainframe systems.

- Ransomware Defense in Healthcare: Hospital networks use IDS/IPS and DLP technologies, coupled with Managed Security Services, to detect and block the exfiltration of patient imaging data, ensuring that AI-driven diagnostic tools remain operational and HIPAA-compliant without paying ransoms.

- Sovereign Data Gateways in Government: Defense agencies use Secure Web Gateway (SWG) and Cloud-based Firewalls to deploy architectures that inspect encrypted traffic (TLS/SSL inspection) without violating data residency legislation, ensuring citizen data remains within national borders.

- OT-IT Convergence in Energy Utilities: Power grid operators use DDoS Mitigation appliances and Antivirus/Antimalware solutions to integrate factory floor SCADA systems with corporate IT networks, providing surge protection against cyberattacks that could cause physical kinetic damage to turbines.

How AI is Transforming the Network Security Market?

AI is changing the network security market by accelerating the identification of novel malware, as well as enhancing operational efficiency in Security Operations Centers (SOCs). In Solutions like NGFW (Next-Generation Firewall) and UTM, AI-based deep learning algorithms have the potential to automatically classify zero-day network traffic patterns, greatly minimizing the amount of time from infection to containment, and reducing breach impact. Meanwhile, AI-powered features in DDoS Mitigation allow businesses to precisely filter application-layer attacks from legitimate traffic spikes by predicting baseline behavior, suggesting adaptive rate-limiting rules to reinforce network availability without manual intervention.

Security governance and incident response are also revolving around AI. In the area of Managed Security Services, intelligent co-pilots and AI agents are used to continuously monitor multi-vendor network logs and autonomously triage alerts, identifying false positives, and escalating genuine threats with forensic context to keep organizations aligned with frameworks like NIST and SOC 2. Moreover, Generative AI assistants are complementing Professional Services by converting natural language security policies directly into low-level firewall rules and IDS signatures, giving IT stakeholders the ability to close security gaps without deep manual coding.

Market Dynamics

Key Drivers in the Network Security Market

The Global Cybersecurity Skills Gap

Global organizations are grappling to acquire skilled professionals who have the knowledge of advanced threat hunting, firewall configuration, security information and event management (SIEM) querying, and cloud networking. The demand for these skills is growing faster than the training pipeline, leading to a structural shortage in the labor market. This is leading to a trend of enterprises outsourcing Managed Security Services providers (MSSPs) rather than depending on in-house employment. These providers oversee essential processes like 24/7 security monitoring, intrusion detection tuning, and unified threat management. Outsourcing such functions allows organizations to maintain a strong defense posture and minimize the risks of alert fatigue and missed indicators of compromise due to insufficient in-house capacities.

Complexity of Hybrid and Multi-Cloud Networks

Enterprises of considerable size now run applications across on-premises data centers, AWS, Microsoft Azure, and private clouds. Controlling a secure fabric across these diverse environments is very complicated. Organizations need to align identity-aware firewalls, virtualized IDS/IPS sensors, and DLP policies on multiple platforms using various tools and standards. This complexity may cause security blind spots, misconfigurations, and compliance violations without the guidance of experts. Thus, there is a growing need for integration and professional services that can assist enterprises to unify security policies across such environments.

Restraints in the Network Security Market

Interoperability Issues with Legacy Infrastructure

Most businesses still run on old operational technology (OT) and general IT systems that were developed over decades and are incompatible with modern API-driven security. These outdated systems are a significant obstacle to upgrading security controls, despite the rising threat landscape. It can be technically impossible or operationally risky to install endpoint agents or software-based security on legacy manufacturing controllers or critical medical devices. Replacing these long-lifecycle assets requires massive capital outlay. Organizations fear business disruption, system instability, and performance latency introduced by security overhead. Consequently, technical debt forces security teams to rely on weak compensatory controls, delaying the implementation of robust zero-trust frameworks.

Economic Uncertainty and Tool Rationalization

Unstable economies have caused organizations to be more hesitant to spend on overlapping security subscriptions. Even though network security is a non-discretionary cost, executives are being pressurized to consolidate point solutions. The licensing fees and long-term engagement models of best-of-breed hardware-based security appliances are coming under increased scrutiny. Businesses have shifted to integrated platforms like Unified Threat Management (UTM) and cloud-based Secure Web Gateways that promise multiple features in a single SKU. Long-term hardware refresh cycles are more likely to be delayed in favor of subscription-based software and virtual appliances. This shift is compelling hardware-centric vendors to pivot toward service-centric and software-based security models.

Growth Opportunities in the Network Security Market

SASE and Edge Security Architecture Build-out

One of the significant growth opportunities in the network security market is assisting organizations to build out Secure Access Service Edge (SASE) frameworks. A lot of companies have tried connecting remote users via basic VPNs, but now they desire their own converged networking and security platforms that provide Zero Trust Network Access (ZTNA) and SWG from the cloud edge. The development of these unified environments involves specialized skills in SD-WAN routing, cloud-native firewall policies, and identity-aware data loss prevention. Security service providers can assist enterprises in replacing rigid castle-and-moat designs with scalable, personal network perimeters that support hybrid work. This area has the potential to create high demand for highly specialized integration and consulting services.

Vertical OT/ICS Security Implementation

The need to integrate both technical cybersecurity skills and understanding of specific industrial processes is driving the growth of professional services as critical infrastructure faces targeted attacks. These are energy-specific SCADA protections, healthcare-centric network segmentation, and manufacturing-specific DDoS mitigation. Companies within the energy, utilities, and defense sectors are required to adhere to stringent operational uptime requirements and physical safety rules. Thus, they require implementation partners that comprehend both the Purdue Model for OT networks and the digital IT protocols. Professional service providers can add significant value by deploying Network Access Control (NAC) to identify unmanaged industrial devices and aligning firewall rules with complex industrial automation workflows.

Trends in the Network Security Market

The Rise of Automated Security Orchestration (SOAR)

Automated threat response is becoming increasingly adopted in organizations as an alternative to slow, manual incident triage. Enterprises are constructing automated playbooks in which the firewall, IDS/IPS, and NAC platforms communicate without human intervention, rather than having analysts manually switch between disjointed dashboards. These platforms enable the automatic isolation of infected devices, dynamic updating of access control lists, and blocking of command-and-control servers. To counter this, network security vendors are providing expertise in API-based automation, playbook design, and machine learning-assisted perimeter tuning.

Sustainability and Energy Efficiency in Hardware Security

Environmental sustainability is also emerging as a key factor in hardware decisions as companies are under pressure to meet ESG objectives. Businesses are now interested in high-throughput firewalls and DDoS mitigation appliances that offer greener, lower-wattage power consumption without sacrificing packet processing speed. This has brought about the need for energy-optimized refresh cycles. Professional service providers assist organizations in selecting power-efficient hardware-based security, transitioning to virtualized platforms where possible, and decommissioning power-hungry legacy security boxes. This trend merges network resilience with corporate climate targets.

Research Scope and Analysis

The research scope and analysis highlights that network security market growth is driven by solutions dominance, cloud-based deployment adoption, software-based technologies, large enterprise demand, and BFSI sector leadership due to rising cyber threats, compliance needs, and digital transformation.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Component Analysis

The solutions segment is expected to dominate the global network security market, driven by widespread adoption of advanced tools such as firewalls, IDS/IPS, and secure web gateways to combat evolving cyber threats. Organizations prioritize these solutions to safeguard networks, endpoints, and sensitive data against ransomware, phishing, and DDoS attacks. Among solutions, firewalls and IDS/IPS hold the largest share due to their foundational role in threat detection and prevention. However, managed security services are rapidly gaining traction, especially among SMEs lacking in-house expertise. Professional services also support integration and compliance needs. Overall, solutions remain dominant due to their direct role in threat mitigation, while services complement them by enabling efficient deployment, monitoring, and management of increasingly complex security infrastructures.

By Deployment Mode Analysis

Cloud-based deployment is poised to dominate the network security market due to the rapid shift toward digital transformation, remote work, and cloud-native infrastructures. Organizations increasingly prefer cloud security solutions for their scalability, flexibility, and cost-effectiveness compared to traditional on-premises systems. Cloud deployment enables real-time threat monitoring, faster updates, and centralized management across distributed networks, making it ideal for modern enterprises. The rise of SaaS, IaaS, and hybrid cloud environments further accelerates demand for cloud-based security. While on-premises solutions remain relevant in highly regulated industries requiring strict data control, cloud deployment leads overall due to its ability to support dynamic workloads, remote accessibility, and evolving cybersecurity requirements in a digitally connected business landscape.

By Technology Analysis

Software-based security is anticipated to dominate this segment as organizations increasingly adopt virtualized and cloud-driven environments. Software solutions offer greater flexibility, scalability, and ease of integration with existing IT infrastructure compared to hardware-based alternatives. They enable rapid updates to address emerging threats and support advanced capabilities such as AI-driven threat detection and automation. The growing reliance on cloud platforms and software-defined networking further strengthens demand for software-based security. While hardware solutions remain important for perimeter defense and high-performance environments, their growth is comparatively slower due to higher costs and limited adaptability. Overall, software-based security leads the segment as enterprises prioritize agile, cost-efficient, and easily deployable cybersecurity solutions.

By Organization Size Analysis

Large enterprises are projected to dominate the network security market due to their extensive IT infrastructure, higher cybersecurity budgets, and increased exposure to sophisticated cyber threats. These organizations require comprehensive, multi-layered security solutions to protect vast amounts of sensitive data and ensure regulatory compliance. They are also early adopters of advanced technologies such as AI-based threat detection and zero-trust architectures. However, SMEs are witnessing faster growth due to rising awareness of cybersecurity risks and increasing adoption of managed security services. Despite this growth, large enterprises maintain dominance as they continue to invest heavily in robust security frameworks to safeguard complex network environments and mitigate financial and reputational risks associated with cyberattacks.

By Industry Vertical Analysis

The BFSI (Banking, Financial Services & Insurance) sector is expected to lead the network security market due to its critical need to protect highly sensitive financial data and comply with stringent regulatory requirements. Financial institutions are prime targets for cyberattacks, including fraud, data breaches, and ransomware, driving continuous investment in advanced security solutions. The sector heavily relies on encryption, intrusion detection systems, and secure access controls to maintain trust and operational integrity. While IT & telecommunications and government sectors also contribute significantly due to large-scale network infrastructure and national security concerns, BFSI remains the leading segment due to the high value of assets, strict compliance mandates, and constant threat landscape it faces.

The Global Network Security Market Report is segmented on the basis of the following:

By Component

- Solutions

- Firewall

- Intrusion Detection & Prevention Systems (IDS/IPS)

- Data Loss Prevention (DLP)

- Network Access Control (NAC)

- Secure Web Gateway (SWG)

- Antivirus/Antimalware

- DDoS Mitigation

- Unified Threat Management (UTM)

- Services

- Professional Services

- Managed Security Services

By Deployment Mode

By Technology

- Software-based Security

- Hardware-based Security

By Organization Size

- Small & Medium Enterprises (SMEs)

- Large Enterprises

By Industry Vertical

- BFSI (Banking, Financial Services & Insurance)

- IT & Telecommunications

- Healthcare

- Government & Defense

- Retail & E-commerce

- Manufacturing

- Energy & Utilities

- Other Industry Vertical

Regional Analysis

Leading Region by Market Share

North America is poised to dominate the global network security market as it is projected to hold 37.1% of the market share by the end of 2026. The United States, which dominates North America, has the highest share in the network security market because of the unmatched concentration of critical IT infrastructure, large federal cybersecurity budgets, and the aggressive digital postures of Fortune 500 companies. The area has an established ecosystem of leading global security software firms, boutique penetration testing consultancies, and a rich pool of cleared cyber defense engineers. Enterprise investment in artificial intelligence-driven threat hunting, advanced persistent threat (APT) neutralization, and the overall retirement of end-of-life firewalls contribute to the continued demand for hardware refresh cycles and managed security service providers. Moreover, a strict regulatory climate and SEC cyber disclosure rules compel publicly traded enterprises to require expert professional services to achieve rapid containment and legal compliance following network incursions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Regional Market

Asia-Pacific is expected to be the most rapidly expanding network security market, driven by government-led sweeping smart city initiatives and sweeping digital identity programs in India, China, Japan, and Southeast Asia. The fast-paced economic growth, the rise of a mobile-first population, and the dynamic expansion of the e-commerce economy are compelling established conglomerates and state agencies to discard outdated, unsupported networking gear. Managed Security Services are in high demand to help these massive organizations handle volumetric DDoS attacks that frequently target gaming and telecom sectors. There is also a severe lack of qualified cybersecurity forensic analysts in the region, and it is necessary to outsource incident response and continuous firewall management to cover the skills gap and enable faster containment of widespread supply chain attacks.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive environment of the global network security market has become highly dynamic with a heterogeneous array of large platform titans, pure-play security hardware vendors, and niche Managed Detection and Response (MDR) startups. The key to success will be the profound strategic alignment with the shift to SASE and zero-trust architectures because they will open the necessary co-selling opportunities and early integration into the new edge compute paradigms. The movement towards market consolidation is rapidly progressing with traditional chipset and networking giants acquiring cloud-native firewall and API-based security specialists to stay relevant. Proprietary threat intelligence, including automated sandboxing feeds and industry-specific vulnerability signatures, is becoming a more important basis of competitive differentiation than just port blocking or generic antivirus signature updates.

Some of the prominent players in the Global Network Security Market are:

- Cisco

- Palo Alto Networks

- Fortinet

- Check Point Software Technologies

- Zscaler

- CrowdStrike

- Cloudflare

- Broadcom

- Microsoft

- IBM

- Trend Micro

- Sophos

- Juniper Networks

- Forcepoint

- Akamai Technologies

- F5 Networks

- Rapid7

- SonicWall

- WatchGuard Technologies

- Barracuda Networks

- Other Key Players

Recent Developments

- January 2026: Palo Alto Networks declared a major expansion of its SASE-focused Professional Services initiative to assist Healthcare and Manufacturing clients in migrating legacy remote access VPNs to AI-powered Zero Trust Network Access (ZTNA) and cloud-native SWG.

- November 2025: Fortinet strengthened its collaboration with global MSSPs and introduced a dedicated operational technology (OT) practice focused on IDS/IPS Signature development and Network Access Control (NAC) aimed at supporting Energy & Utilities clients in securing industrial SCADA networks against state-sponsored ICS malware.

- October 2025: Cisco completed the acquisition of a cloud-native DLP and encryption startup to bolster its Security Cloud strategy and Workflow Automation solutions for sovereign and air-gapped defense networks, addressing the complex requirements of Government & Defense agencies handling classified secret data.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 42.6 Bn |

| Forecast Value (2035) |

USD 134.3 Bn |

| CAGR (2026–2035) |

13.6% |

| The US Market Size (2026) |

USD 13.3 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Component, By Deployment Mode, By Technology, By Organization Size, and By Industry Vertical |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Network Security Market?

▾ The Global Network Security market is poised to be valued at USD 42.6 billion in 2026 and is projected to reach USD 134.3 billion by 2035, driven by the universal need for specialized hardware and services in firewall protection, intrusion prevention, and zero-trust network access.

Which region held the largest share of the Network Security Market in 2026?

▾ North America is poised to lead this market with 37.1% market share in 2026, driven by a mature security vendor ecosystem and aggressive enterprise investment in AI-driven threat detection and Critical National Infrastructure (CNI) protection.

Who are the key players in the Global Network Security Market?

▾ Key players include firewall pure-plays like Palo Alto Networks and Fortinet, networking giants like Cisco, and cloud-native security platforms like Zscaler and CrowdStrike, alongside the managed security divisions of global system integrators.

What is the CAGR of the Global Network Security Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 13.6% from 2026 to 2035, reflecting the accelerating sophistication of ransomware campaigns and the persistent shortage of internal cybersecurity operations talent.

What factors are driving the growth of the Global Network Security Market?

▾ Key drivers include the global cybersecurity skills gap, the imperative to replace outdated data center firewalls, the management complexity of hybrid cloud and edge networks, and the surge in demand for DDoS Mitigation amid escalating geopolitical hacktivist attacks.

Which region is expected to grow the fastest in the Network Security Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid digitalization in India, China, and Japan, where Managed Security Services are critical for transitioning large conglomerates to cloud-based security operations to combat rising state-sponsored cyber espionage.

What are the major trends in the Global Network Security Market?

▾ Major trends include the convergence of networking and security into SASE frameworks, the use of Generative AI for automated policy creation, the demand for hardware-based energy-efficient appliances, and the focus on OT/ICS security within critical manufacturing and energy verticals.

How is the Global Network Security Market segmented?

▾ The market is segmented By Component, Deployment Mode, Technology, Organization Size, and By Industry Vertical.