What is the Sovereign Cloud Services Market Size?

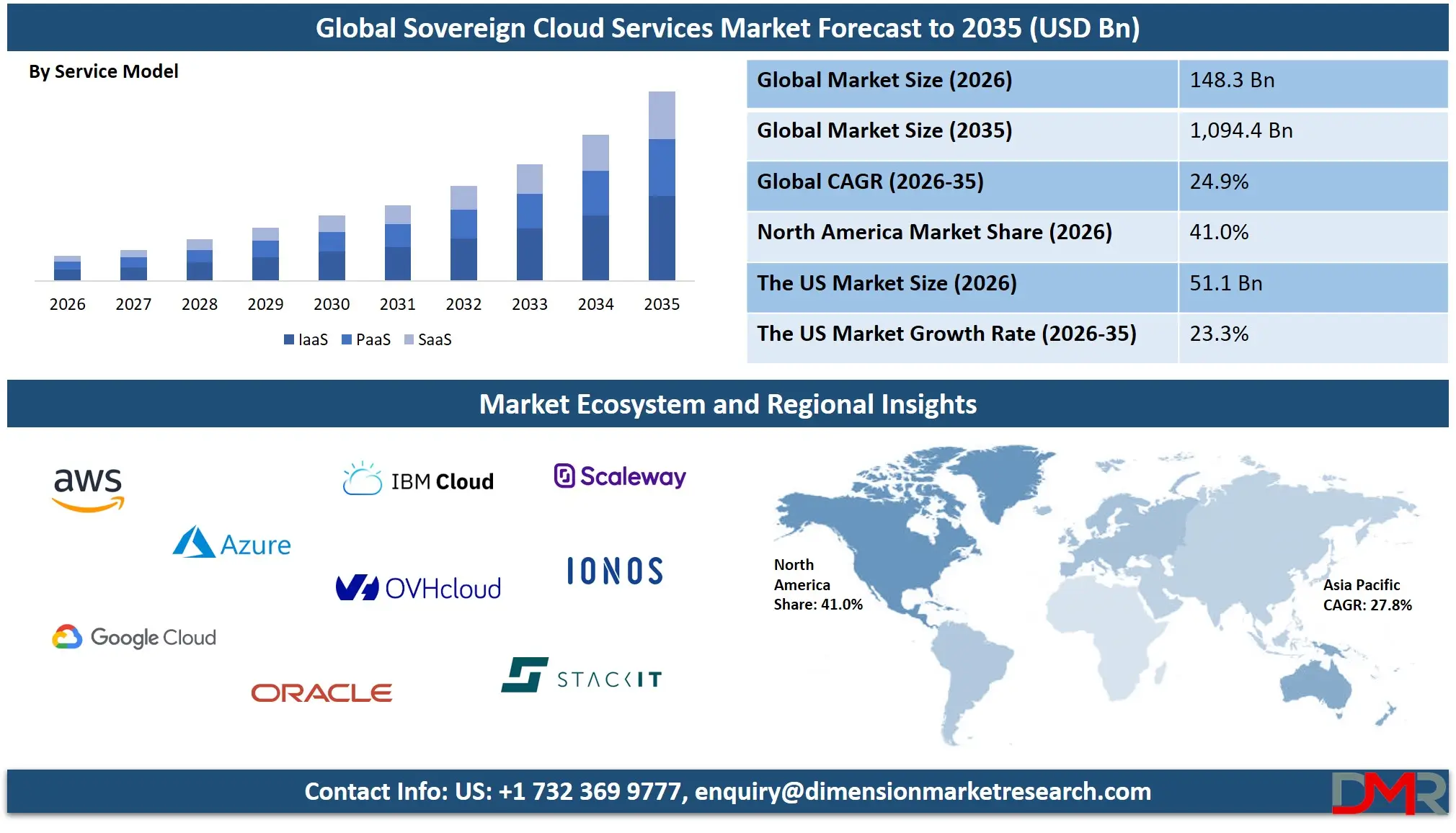

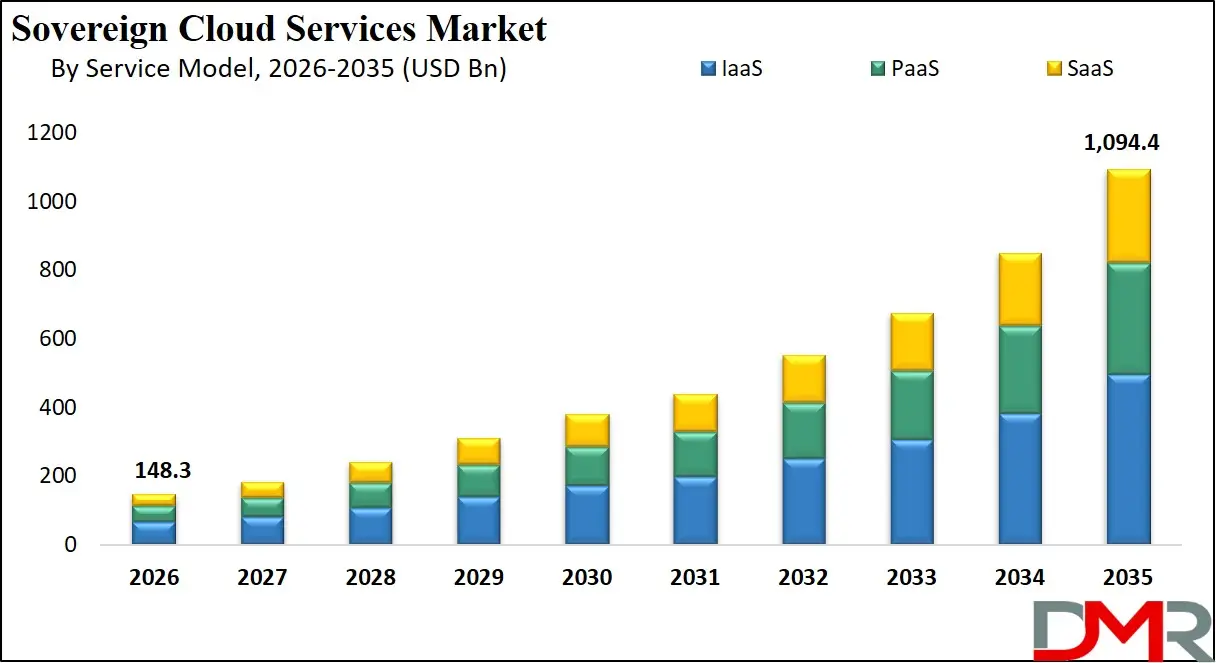

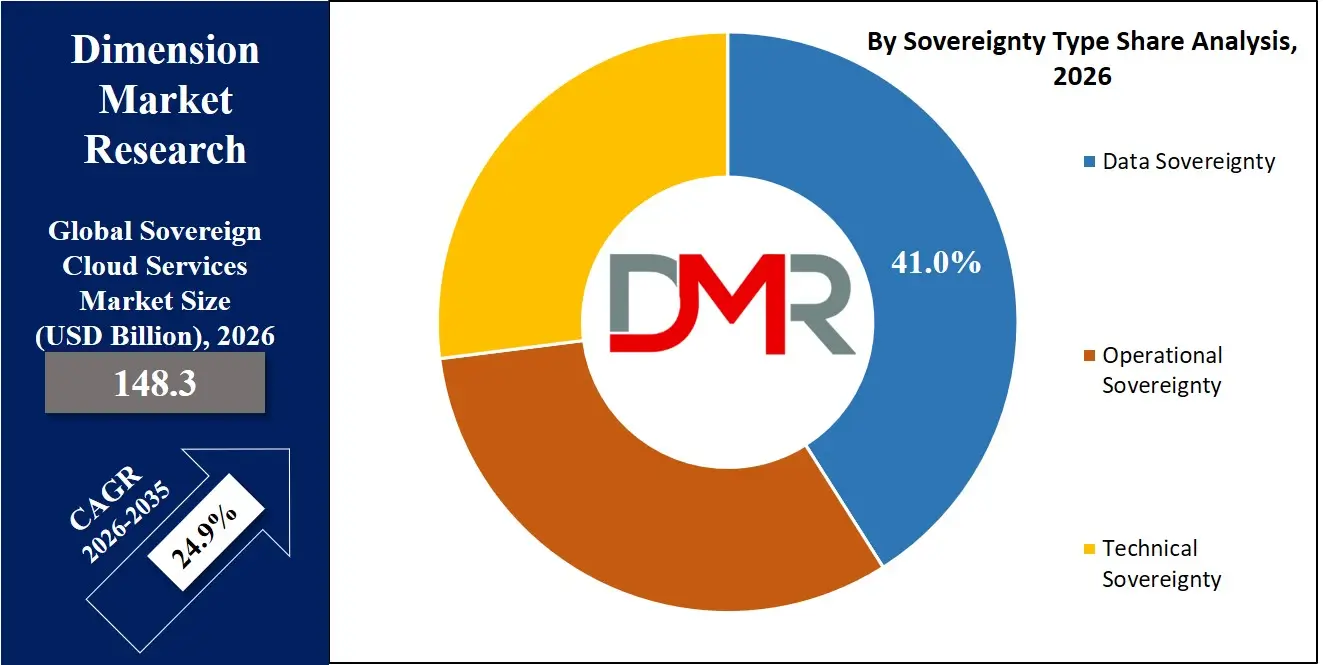

The global sovereign cloud services market size is expected to reach USD 148.3 billion in 2026, growing at a 24.9% CAGR to USD 1,094.4 billion by 2035, driven by data sovereignty, regulatory compliance, and secure cloud infrastructure demand.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Sovereign Cloud Services Market targets cloud systems where the data and operations are controlled by national laws. The increase in data localization legislation, cybersecurity requirements, and regulatory compliance in key industries is a growth driver. The European Commission is progressing sovereign data policies such as GAIA-X and the Government of India is supporting a secure digital infrastructure through Digital India.

The U.S. National Institute of Standards and Technology highlights secure cloud and zero-trust models, as well. Growing cyber threats and cross border data limitations are driving up adoption. In the future, it will be in demand due to AI governance, digital identity systems, and digitization of critical infrastructure.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

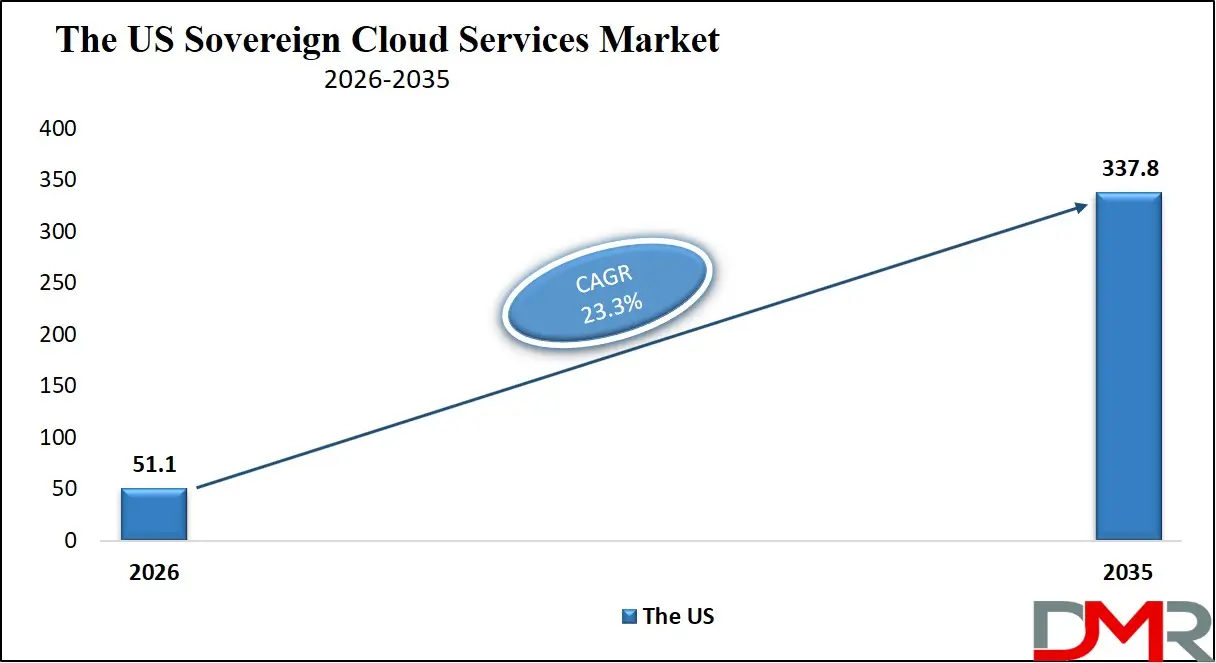

US Sovereign Cloud Services Market

The US Sovereign Cloud Services Market size is projected to reach USD 51.1 billion in 2026 and grow at a compound annual growth rate of 23.3%, reaching USD 337.8 billion by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US sovereign cloud services market is fueled by tough cybersecurity and data governance guidelines by the National Institute of Standards and Technology and compliance initiatives such as the FedRAMP. Growth is increasing at a rapid rate due to the increasing cyber risks, adoption of zero trust and the need to have secure infrastructure of a federal cloud, enhanced by the continuing digital transformation and modernization of defense. The growing interest in AI governance and securing critical infrastructure information is further boosting long-term demand.

Europe Sovereign Cloud Services Market

The Europe Sovereign Cloud Services Market is expected to hit USD 43.0 billion in the year 2026 and grow with a CAGR of 24.5%. The market is also fueled by effective data protection laws and the European Commission-driven initiatives of digital sovereignty. BFSI, government and telecom sectors are driving up demand, and are driving the use of compliant cloud infrastructure. Increasing investments in the local cloud ecosystems and decreased dependency on external providers are also contributing to market growth.

Japan Sovereign Cloud Services Market

Japan Sovereign Cloud Services Market is anticipated to reach USD 9.6 billion in 2026, expanding with a CAGR of 26.7%. The market is driven by strong government focus on data security and digital sovereignty initiatives supported by the Government of Japan. Increasing adoption across manufacturing, BFSI, and public sector is accelerating demand for compliant cloud infrastructure. Growing emphasis on AI integration and secure digital transformation is further boosting market growth.

Key Takeaways

- Market Size: The market is projected to reach USD 148.3 billion in 2026 to USD 1,094.4 billion by 2035, driven by rising demand for sovereign data infrastructure.

- Growth Rate and Outlook: Expected to grow at a CAGR of 24.9%, reflecting rapid adoption across regulated and security-sensitive sectors.

- Primary Growth Drivers: Rising data localization laws, increasing cybersecurity threats, regulatory compliance mandates, and demand for jurisdiction-controlled cloud environments.

- By Service Model Analysis: IaaS leads the segment with a 45.0% share, driven by demand for sovereign control over core cloud infrastructure and scalable deployment.

- By Deployment Model Analysis: Cloud-based dominates with an 83.0% share due to its flexibility, scalability, and ability to meet compliance through localized cloud regions.

- By Industry Vertical Analysis: BFSI holds the largest share at 27.0%, supported by strict regulatory requirements and high sensitivity of financial data.

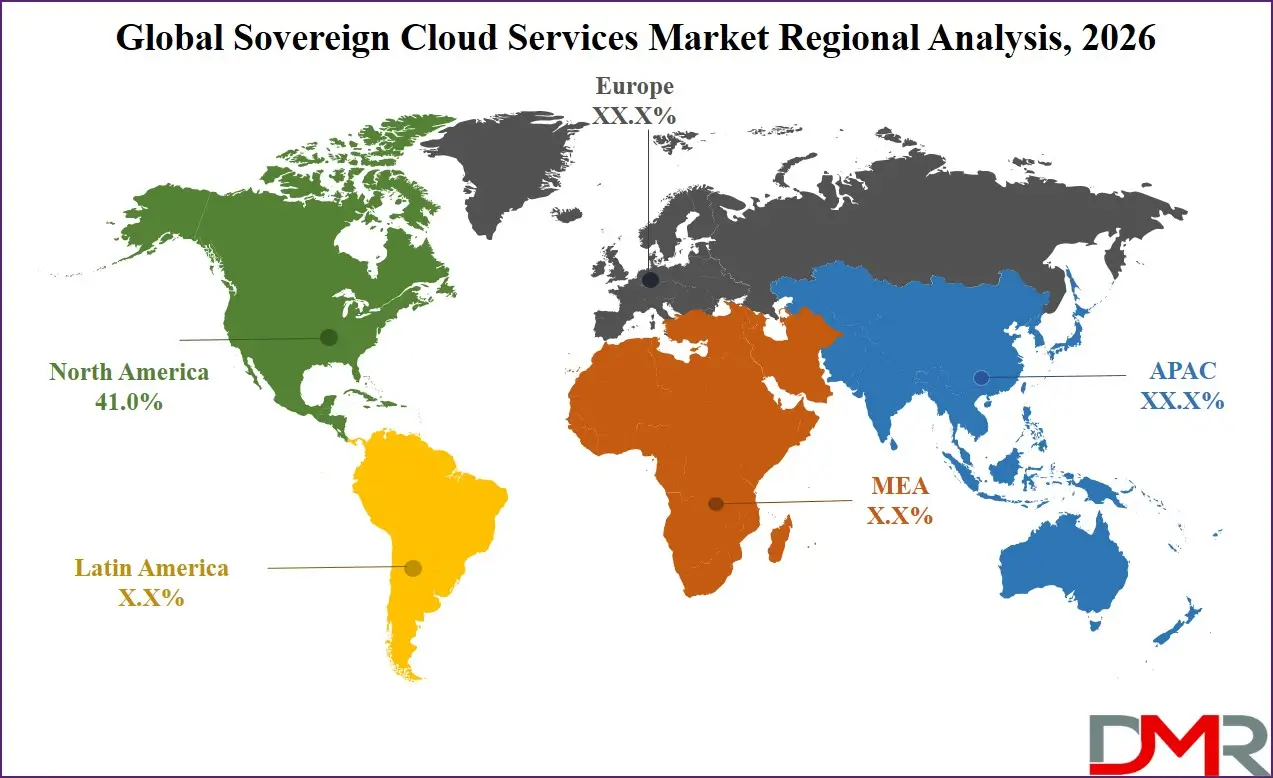

- Regional Leadership: North America leads the market with a 41.0% share, driven by advanced cloud infrastructure and strong regulatory frameworks.

What are the Sovereign Cloud Services?

Sovereign cloud services refer to cloud platforms where data and infrastructure are managed by national laws. They guarantee data residency, regulatory compliance, and limited cross-border data flows. The European Commission points out a change to local data processing within the framework of sovereignties. The Government of India implements data localization in principal areas as well. The solutions find common use in defense, BFSI and public services. They guarantee local control of encryption and access. All in all, they play a crucial role in secure and compliant digital infrastructure.

Use Cases

- Government Data Infrastructure: Sovereign cloud hosts citizen records and e-governance systems within national jurisdiction, ensuring compliance with local laws and preventing foreign access, while supporting secure digital identity and public service delivery.

- Financial Data Compliance (BFSI): Banks use sovereign cloud to meet data localization requirements, enabling secure domestic transaction processing and storage, while reducing risks of cross-border data exposure and regulatory breaches.

- Defense and National Security Systems: Defense agencies deploy sovereign cloud for classified data, ensuring full control over infrastructure and encryption, while supporting secure communication, intelligence, and surveillance operations.

- Healthcare Data Management: Healthcare providers use sovereign cloud to store patient data within national boundaries, ensuring compliance with privacy regulations, while enabling secure data sharing for research and public health systems.

How AI is Transforming the Sovereign Cloud Services Market?

The sovereign cloud services market is being transformed by AI to allow automated data governance, compliance checks, and real-time threat detection in controlled settings. It complements zero-trust designs with intelligent access management and anomaly detection, boosting the safety of sensitive national information.

The AI-powered analytics can also aid effective resource management and local decision making in sovereign infrastructures. With governments increasingly focusing on AI governance, sovereign clouds are emerging as major platforms to deploy secure and regulation compliant AI systems.

Market Dynamics

Key Drivers in the Global Sovereign Cloud Services Market

Increasing Data Localization Rules.

Data localization policies are becoming more stringent in governments around the world so that sensitive data may not leave national borders. The national frameworks and policies championed by the European Commission are hastening sovereign cloud adoption. Businesses must transition off the international models of clouds to jurisdiction-regulated settings. This regulatory drive is especially intense in the BFSI, healthcare, and the government sectors. With the shift to mandatory compliance, instead of optional compliance, the demand of sovereign cloud infrastructure keeps growing.

Increasing Cybersecurity Threat Landscape

Critical infrastructure is being targeted by the proliferation of cyberattacks, which are fueling the necessity to use secure and isolated cloud environments. Sovereign cloud provides better governance over access to data, encryption, and governance of operations. Several agencies with standards set by the National Institute of Standards and Technology focus on zero-trust and secure architectures. Companies are focusing on platforms that reduce foreign surveillance or intrusions. This increasing risk landscape is greatly increasing investment in sovereign cloud solutions.

Restraints in the Global Sovereign Cloud Services Market

Expensive infrastructure and operations

The sovereign cloud infrastructure is a capital-intensive endeavor, involving localized data centers and safe systems. Companies also have to have committed compliance and governance structures, which raise the cost of operation. Smaller businesses usually cannot afford these expenses as compared to the public cloud options. Financial burden is further enhanced by the requirement of redundancy, resilience and certification. Such barriers are expensive and may slow down the pace of adoption especially in developing economies.

Poor Scalability and Maturity of Ecosystems

Global hyperscalers can be more flexible and offer larger scale than sovereign cloud environments. Poor access to sophisticated tools, AI services, and developer ecosystems limits the potential of innovation. Business organizations can have difficulties adopting sovereign cloud in combination with their current multi-cloud plans. The ecosystem is in the process of development and has less standardized solutions and interoperability frameworks. This drawback may impede mass enterprise adoption even with vigorous regulatory motivators.

Growth Opportunities in the Global Sovereign Cloud Services Market

Growth of Digital Sovereignty Projects

The national digital infrastructure is being invested in by countries to minimize reliance on foreign cloud-based services. Initiatives led by governments such as the Government of India are promoting indigenous cloud ecosystems. This opens up great prospects to the local and regional cloud providers. The use of sovereign cloud platforms is being deployed faster through public-private partnerships. The increasing focus on self-sustaining digital economies will lead to the expansion of markets in the long-term.

Connection with AI and Advanced Technologies

The emergence of AI, edge computing, and IoT is driving a need to have reliable and compliant data processing platforms. Sovereign cloud offers a regulated solution to deploy AI models under the scope of regulation. The demand is increasing as governments are starting to pay more attention to AI governance. Combining with advanced analytics improves operational efficiency and decision-making. Such integration of technologies gives the market a big opportunity to grow.

Trends in the Global Sovereign Cloud Services Market

Hybrid Sovereign Cloud Models

The integrations in organizations of hybrid models of sovereign control and public cloud scalability are on the increase. This strategy can enable businesses to achieve a balance between compliance and performance and cost-efficiency. Hyperscaler partnerships with local providers are on the rise. These models allow flexibility in deployment and still have jurisdictional control over sensitive data. Hybrid sovereign cloud is the architecture of choice in regulated industries.

Emergence of Sovereign Cloud Platforms by Telecom

The telecom operators are emerging as leaders in developing sovereign cloud infrastructure because they are locally located and are aligned with government regulations. They are using the available network resources as a way of providing secure cloud computing services on the national borders. Services are being augmented by collaborations with international cloud vendors. Telecom-based models are becoming common in areas such as Europe and Asia. This is transforming the competitive environment in the sovereign cloud market.

Research Scope and Analysis

By Sovereignty Type Analysis

Data sovereignty is estimated to dominate the segment with 41.0% in 2026 due to the increased data localization regulations and the necessity to retain sensitive data within states. This demand is being further reinforced by regulatory push by regulatory bodies such as the European Commission.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Meanwhile, operational sovereignty is on the rise whereby organizations desire local control of cloud operations, access, and management. It minimizes the use of foreign providers and at the same time meets the national policies. Both of these trends are supporting secure and controlled cloud adoption.

By Service Model Analysis

In 2026, IaaS will take up a dominant position in the segment with a 45.0% market share, as organizations demand sovereign control over compute, storage and networking within the borders of each country. It is highly flexible and aligns with compliance requirements, which are why it is suitable to governments and regulated industries. PaaS, in the meantime, is expanding by allowing applications to be developed and deployed on sovereign infrastructure in a secure manner. It helps in accelerated innovation and regulatory compliance and data control. Combined, the two models are boosting scalable sovereign cloud use.

By Architecture Type Analysis

Private dedicated cloud is expected to lead the segment with a 36.0% share in 2026, driven by demand for isolated, highly secure, and compliant environments within national boundaries. It is widely adopted by governments and regulated sectors for maximum control and customization. Meanwhile, national cloud is gaining traction as countries build centralized sovereign infrastructures to reduce reliance on foreign providers. It supports large-scale public sector digitalization with full jurisdictional control. Together, these models are driving secure sovereign cloud adoption.

By Deployment Model Analysis

The cloud-based deployment will lead the pack with 83.0% share in 2026, owing to its scalability, flexibility and its capacity to address the data residency needs through localized territories. Enterprises and governments are using it extensively to obtain agile but compliant cloud solutions. On-premise, in the meantime, is essential when there is a high sensitivity in the workload and the need to maintain complete physical control over information and equipment. It is mainly used in defense and high-security.

By Compliance Driver Analysis

In 2026, regulatory compliance is projected to be in the lead with a share of 46.0% as a result of stringent data protection regulations and localization requirements in industries such as BFSI and government. Compliance-based adoption is being expedited by European Commission policies. Meanwhile, data security is paramount because organizations are concerned with sensitive data security against cyber-attacks. Sovereign cloud enhances encryption and access control on national borders. Together, compliance and security are key growth drivers.

By Enterprise Size Analysis

In 2026, large enterprises will dominate the segment, with a share of 69.0% as they can afford investment in sovereign cloud infrastructure and address complex regulatory and security needs. Their activities in the regulated sectors create the need to have high-control and compliant cloud environments. The other key focus areas of these organizations are data governance and scale-based risk management. In the meantime, the small and medium enterprises are slowly implementing sovereign cloud solutions under managed and cloud-based solutions. This allows them to attain compliance and security without having to invest in heavy infrastructure. The two segments are collectively making inroads into the wider market.

By Industry Vertical Analysis

BFSI is expected to lead with a 27.0% share in 2026, driven by strict regulations and the need for secure, compliant financial data processing. It relies on sovereign cloud for data protection and risk management within national boundaries. Meanwhile, government and defense adopt it to secure classified and sensitive national data. It ensures full control over infrastructure, access, and jurisdiction. Together, both sectors drive strong demand for sovereign cloud solutions.

The Global Sovereign Cloud Services Market Report is segmented on the basis of the following:

By Sovereignty Type

- Data Sovereignty

- Operational Sovereignty

- Technical Sovereignty

By Service Model

By Architecture Type

- Private Dedicated Cloud

- National Cloud

- Sovereign Public Region

By Deployment Model

By Compliance Driver

- Regulatory Compliance

- Data Security

- Digital Sovereignty Strategy

By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

By Industry Vertical

- BFSI

- Government and Defense

- Telecom

- Healthcare

- Energy and Utilities

- Manufacturing

- Others

Regional Analysis

Leading Region by Market Share

In 2026, North America is expected to dominate the sovereign cloud services market with a 41.0% market share due to its robust regulatory frameworks, cloud infrastructure, and government, BFSI, and defense adoption. The area also enjoys developed standards in cybersecurity and extensive adoption of compliance-based solutions in the cloud. Its market dominance is also enhanced through continuous investment in digital transformation and safe cloud technology.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Regional Market

The Asia Pacific region is expected to experience the most significant growth rate, with an increasing speed of digitalization, the growth of data localization regulations, and the rising use of clouds in the growing economies. Governments are spending a lot on their own digital infrastructures to minimize the dependence on external providers. Growth is further accelerated by increasing demand by BFSI, telecom, and public sector.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive landscape is characterized by a mix of global cloud providers, regional players, and telecom-led operators competing on compliance, security, and localized infrastructure capabilities. Companies are focusing on partnerships, joint ventures, and sovereign cloud alliances to meet jurisdictional requirements. Innovation is centered on zero-trust architecture, AI integration, and hybrid sovereign models to enhance differentiation. Regulatory alignment and the ability to offer fully controlled, compliant environments remain key competitive factors.

Some of the prominent players in the Global Sovereign Cloud Services Market are:

- Amazon Web Services

- Microsoft Azure

- Google Cloud

- Oracle Cloud

- IBM Cloud

- OVHcloud

- Scaleway

- IONOS Cloud

- STACKIT

- T-Systems

- Atos

- Orange Business

- Capgemini

- Thales Group

- Proximus

- Naver Cloud

- Kakao Cloud

- NTT Data

- Tata Communications

- Yotta Data Services

- Other Key Players

Recent Developments

- April 2026: The European Commission awarded a €180 million sovereign cloud contract to a consortium of European providers, strengthening regional cloud sovereignty through multi-company collaboration.

- April 2026: GalaxEye secured support through partnerships and government-backed channels to expand sovereign data capabilities via satellite infrastructure for defense and commercial use.

- January 2026: Amazon Web Services introduced the AWS European Sovereign Cloud, offering a fully isolated cloud environment within the EU to meet strict data residency and sovereignty requirements.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 148.3 Bn |

| Forecast Value (2035) |

USD 1,094.4 Bn |

| CAGR (2026–2035) |

24.9% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Sovereignty Type (Data Sovereignty, Operational Sovereignty, Technical Sovereignty),

By Service Model (IaaS, PaaS, SaaS),

By Architecture Type (Private Dedicated Cloud, National Cloud, Sovereign Public Region),

By Deployment Model (Cloud-based, On-premises),

By Compliance Driver (Regulatory Compliance, Data Security, Digital Sovereignty Strategy),

By Enterprise Size (Large Enterprises, Small and Medium Enterprises),

By Industry Vertical (BFSI, Government and Defense, Telecom, Healthcare, Energy and Utilities, Manufacturing, Others) |

| Regional Coverage |

North America – The US and Canada;

Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe;

Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC;

Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America;

Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Sovereign Cloud Services Market?

▾ The market is expected to be valued at USD 148.3 billion in 2026 and is projected to reach USD 1,094.4 billion by 2035.

What is the CAGR of the Sovereign Cloud Services Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 24.9% during the forecast period.

What factors are driving the growth of the Sovereign Cloud Services Market?

▾ Growth is driven by rising data localization laws, increasing cybersecurity threats, strict regulatory compliance, and demand for secure, jurisdiction-controlled cloud infrastructure.

What are the major trends in the Sovereign Cloud Services Market?

▾ Key trends include adoption of hybrid sovereign cloud models, AI integration, zero-trust security frameworks, and telecom-led sovereign cloud platforms.

Which region held the largest share of the Sovereign Cloud Services Market in 2026?

▾ North America held the largest share, accounting for approximately 41.0% in 2026.

Which region is expected to grow the fastest in the Sovereign Cloud Services Market?

▾ Asia Pacific is expected to be the fastest-growing region during the forecast period.

Who are the key players in the Sovereign Cloud Services Market?

▾ Amazon Web Services, Microsoft Azure, Google Cloud, Oracle Cloud, IBM Cloud, OVHcloud, Scaleway, IONOS Cloud, STACKIT, T-Systems, Atos, Orange Business, Capgemini, Thales Group, Proximus, Naver Cloud, Kakao Cloud, NTT Data, Tata Communications, Yotta Data Services, and other key players.

How is the Sovereign Cloud Services Market segmented?

▾ The market is segmented by Sovereignty Type, Service Model, Architecture Type, Deployment Model, Compliance Driver, Enterprise Size, and Industry Vertical.