The stem cell therapy market is experiencing significant growth, driven by increasing investments in research and development. Governments, private investors, and pharmaceutical companies are making substantial commitments to advance stem cell research, particularly as part of the rapidly expanding regenerative medicine industry.

For instance, India’s Department of Biotechnology (DBT) invested over USD 8.80 million between 2019 and 2022 in projects focused on fundamental biology, translational research, and genetic technologies for clinical applications. These investments reflect the potential of stem cell therapies to revolutionize healthcare by repairing damaged tissues and organs. The rising prevalence of chronic diseases, fueled by aging populations and sedentary lifestyles, further propels the market, especially as cell-based therapies gain clinical acceptance.

According to a February 2024 CDC report, approximately 128 million Americans live with at least one chronic illness, including cardiovascular, neurodegenerative, and autoimmune disorders. Stem cell therapies offer regenerative solutions that improve treatment outcomes for these conditions, providing hope for patients with severe ailments.

The market’s expansion is also attributed to advancements in stem cell technologies, including adult stem cells, induced pluripotent stem cells (iPSCs), and embryonic stem cells, alongside the growing emphasis on personalized medicine. Both allogeneic and autologous stem cell therapies have contributed significantly to this growth, supported by clinical trials and collaborations. Increased funding and innovation are expected to drive further market expansion during the forecast period.

The US Stem Cell Therapy Market

The US Stem Cell Therapy Market is projected to be valued at USD 7.1 billion in 2024. It is expected to witness subsequent growth in the upcoming period as it holds USD 19.5 billion in 2033 at a CAGR of 11.8%.

New findings in stem cell science and therapy advancement make the United States one of the world leaders in the stem cell therapy market. Since most of these chronic conditions treatments using stem cell therapy are autologous, notable advancements in the US stem cell market have been witnessed in diseases such as heart ailments, arthritis, and neurological disorders.

where personalized medicine is becoming an important area of interest the stem cells' ability to repair damaged tissue at a faster rate is used as therapeutic solutions through the MSC collected from adipose tissue or bone marrow and therefore therapeutic development occurs at a faster rate with increasing use. Another ongoing trend is an increase in funding from both public and private sources for research on stem cells.

The United States has led the world in creating innovative therapies using human embryonic-derived cell therapy iPSCs, moreover studies on applications of stem cell-based treatments for age-related diseases or injury also, and regulatory developments by FDA-approved cell therapy products have helped facilitate development, encouraging clinical trials, and research activities here in America factors likely to promote market expansion over the coming ten years and position itself as an innovator globally.

Stem Cell Therapy Market Key Takeaways

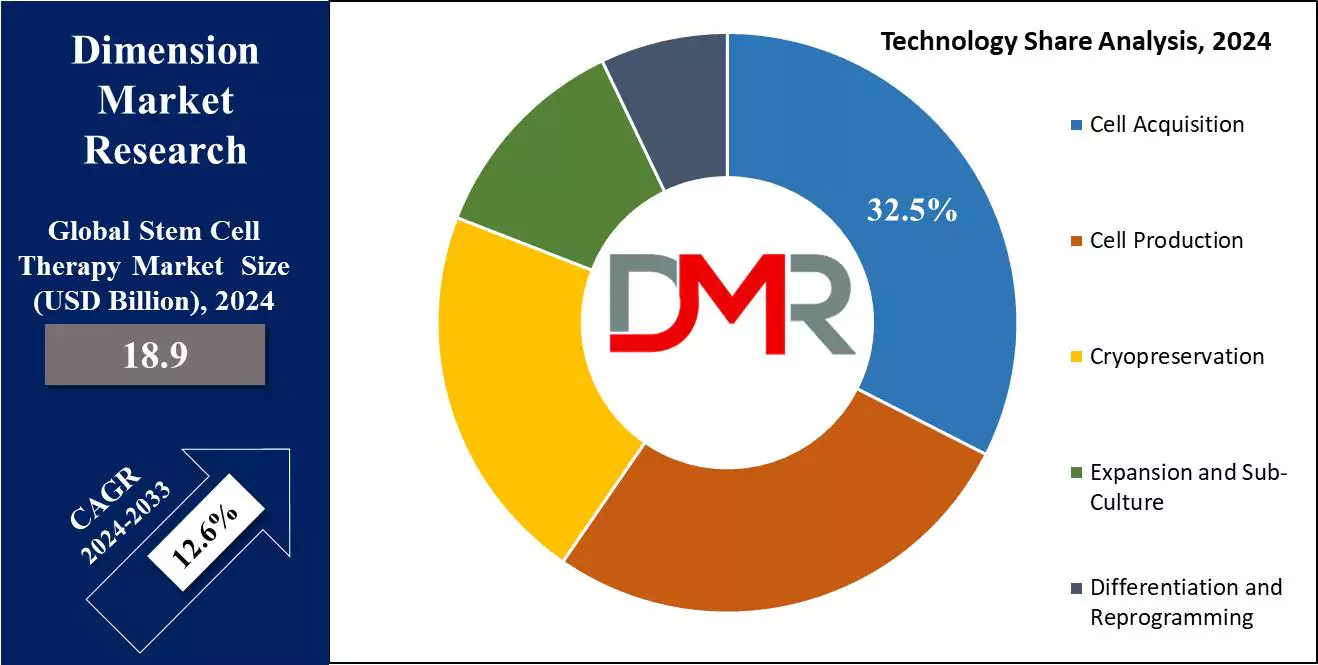

- Global Market Value: The Global Stem Cell therapy Market size is estimated to have a value of USD 18.9 billion in 2024 and is expected to reach USD 54.7 billion by the end of 2033.

- The US Market Value: The US Stem Cell therapy Market is projected to be valued at USD 19.5 billion in 2033 from a base value of USD 7.1 billion in 2024 at a CAGR of 11.8%.

- By Therapy Segment Analysis: Allogeneic stem cell therapy dominates the therapy segment as it holds the highest market share in 2024.

- By Technology Segment Analysis: Cell acquisition technology leads the technology segment of this market as it holds 32.5% of the market share in 2024.

- Regional Analysis: North America is expected to have the largest market share in this market with a share of about 44.89% in 2024.

- Regional Analysis: Some of the major key players in the global stem cell therapy market are Thermo Fisher Scientific Inc., STEMCELL Technologies Inc., Merck KGaA, Sartorius AG, and many others.

- Global Growth Rate: The market is growing at a CAGR of 12.6 percent over the forecasted period.

Stem Cell Therapy Market Use Cases

- Musculoskeletal Disorders: Treatments for degenerative diseases of articular tissues, osteoarthritis, and injuries of cartilage and bone injuries are being replaced with stem cell therapies. The treatments make use of MSCs for regenerations in the cartilage and repair of bones.

- Cardiovascular Diseases: Stem cells are used for myocardial infarction and heart failure, regenerating heart tissue and improving heart function in clinical trials.

- Wound Healing: With the use of stem cell therapies, the skin and tissues develop a greater capacity for regeneration, which aids in the curing of chronic wounds such as diabetic ulcers and burns, hence reducing complications.

- Neurodegenerative Diseases: These are targeted by stem cells in Parkinson's and Alzheimer's diseases, utilizing neural stem cells to regenerate neurons, hence restoring the lost function.

Stem Cell Therapy Market Dynamic

Trends

Rising Focus on Regenerative Medicine

The global market of stem cell therapy is gradually observing a shift in therapeutic trends toward the emerging area of regenerative medicine. It is driven by an increasing demand for the treatment of degenerative conditions related to cardiovascular diseases, neurodegenerative disorders, and orthopedic injuries. In tissue repair or the regeneration of impaired tissues or organs, regenerative medicine exploits the self-renewal and differentiation properties of stem cells mainly MSCs and iPSCs.

Advancements in Autologous and Allogeneic Therapies

Key trends that are gaining wider acceptance include autologous and allogeneic stem cell therapies. Autologous therapies are showing greater appeal due to the lower possibility of immune rejection and personalized treatment outcomes.

Meanwhile, allogeneic stem cell therapy is taken into consideration, by taking donor hematopoietic stem cells, especially for the treatment of blood cancers and genetic disorders. Advancements in cell isolation, gene editing, and cell expansion technologies are improving efficacy and availability for both autologous and allogeneic treatments.

Growth Drivers

Increasing Prevalence of Chronic Diseases

One of the key factors driving the growth of the global market in stem cell therapy includes the rising incidence of chronic diseases. Cardiovascular diseases, diabetes, neurological disorders, and cancers are on the increase due to changes in lifestyle and an aging population. These are, indeed, pathologies that have promising treatments; the regenerative answer lies with the stem cell therapies that help repair or replace destroyed tissues and organs.

Hematopoietic stem cells, for example, are being increasingly applied in the treatment of blood cancers, while mesenchymal stem cells have shown potential in cardiovascular and neurodegenerative disorders.

Technological Advancements in Stem Cell Therapies

CRISPR gene editing, 3D bioprinting, and advanced cell expansion techniques that involve the use of stem cells more efficient, scalable, and safe. Furthermore, these advances are complemented by cryopreservation and improvements in cell production to guarantee the viability and longevity of stem cells for large quantities that can be widely distributed.

These technological innovations of stem cells make therapies more accessible, thus accelerating market growth as more therapies become viable options for treatment by a greater percentage of healthcare providers.

Growth Opportunities

Emerging Markets and Government Support

This can also be expected to provide enormous growth opportunities for the global stem cell therapy market, considering the large growth potentials of the emerging economies in Asia-Pacific and Latin America. This includes increased investments that emerge in health infrastructure, like China, Japan, and South Korea, coupled with stem cell research.

Governmental support across the regions, through regulatory frameworks that promise to boost this development and funding for clinical trials, also fosters stem cell treatment growth. For example, Japan has already introduced progressive policies related to regenerative medicine, and it is considered one of the pioneers in stem cell-related innovations.

Expansion in Clinical Applications

Another key growth opportunity will be represented by the extension of the clinical application of stem cell therapies. They foresee the use of stem cell therapies in the treatment of not only hematological conditions but also orthopedic, neurological, cardiovascular, and autoimmune conditions, among others.

Increasing clinical trials for new therapeutic areas, such as the treatment of wounds and injuries, and genetic disorders, are extending the market potential of these therapies. So, as the success rate for these trials continues increasing, the range of applications of this stem cell will widen, thereby leading more healthcare providers to this innovative therapy, hence driving market growth in the forecast period.

Restraints

High Cost of Stem Cell Therapies

Even with the promising potential of stem cell therapies, the treatment expense supporting the procedures remains among the key restraints. This is largely because acquisition and isolation, expansion, and cryopreservation of cells are intricate processes that require sophisticated technologies and infrastructures, hence running at very high costs for treatment. This personalized nature of the treatment-for instance, therapies involving autologous stem cells can make such treatments very expensive.

Additionally, there are costs associated with clinical trials, regulatory approvals, and commercialization. These high costs limit accessibility to stem cell therapies, especially within developing regions, which is a factor that frankly speeds up the market growth.

Ethical and Regulatory Challenges

The ethical concern in using embryonic stem cells has been identified as another major drawback to the development of the global stem cell therapy market. The research and therapeutic application of human embryonic stem cells has thus been surrounded by ethical debates due to the generalized destruction of embryos, hence very strict regulations in most countries.

These restrictions will act as barriers to progress in this field of research and hamper the development of therapies derived from embryonic cells. Added to this is the need to navigate multifarious regulatory frameworks for different countries, which are also variable, raising challenging conditions faced by market players and constraining the ability of the market to expand in such regions.

Stem Cell Therapy Market Research Scope and Analysis

By Therapy

In the global stem cell therapy market, allogeneic stem cell therapy dominates the therapy segment because of its high therapeutic potential and wider applicability. Allogeneic stem cell therapy is thereby considered a more promising therapy compared to autologous stem cell therapy, in which treatment depends upon the patient's cells. On the other hand, allogeneic stem cell therapy uses stem cells from a donor.

There are a couple of advantages to this: the most important ones being that it can make available off-the-shelf stem cell products for administration to multiple patients. This is important scalability in the treatment of conditions requiring immediate intervention, such as acute graft versus host disease, leukemia, and certain cancers.

Moreover, allogeneic stem cells-especially from bone marrow, umbilical cord blood, and peripheral blood can be readily supplied through established cell banking. This is done to allow a much larger volume of cell administration-oftentimes required for the needed curative effect, especially in the cases of life-threatening diseases.

Allogenic stem cell therapy is also increasingly preferred for conditions where the cells of the patient themselves may not be viable for treatment, including disorders of the immune system and genetic diseases. The improvement of techniques of immunosuppression has reduced further the chances of rejection in allogeneic stem cell therapy, hence making it safer and more dependable.

The rising demand for regenerative medicine is going to keep allogeneic stem cell therapy dominant in the therapy market during the forecast period and provide the undergoing market with substantial market growth.

By Cell Source

Among the cell sources, the segment of the adult stem cell leads the global stem cell therapy market, due to their easy availability and established therapeutic benefits. The ethical issues concerning ESCs are also lower for adult stem cells.

Adult tissues like bone marrow, adipose tissue, and peripheral blood serve as sources for stem cells such as hematopoietic stem cells and mesenchymal stem cells. These cells have been in clinical use for several decades and are widely applied in the treatment of blood disorders such as leukemia and lymphoma.

Most clinical applications of stem cells to date have involved adult stem cells, mainly because potential tumorigenesis is lower compared to that of embryonic stem cells. The differentiation capacity of an ASC is more limited; this renders the ASCs much safer for therapeutic application, preserving the lower capability of forming teratomas or any other unwanted tissues. Also, in autologous stem cell therapy in which a patient's cells are used to prevent possible immune rejection use of adult stem cells is preferred.

Besides, the approval processes taken by adult stem-based therapies have been smoother compared to human embryonic stem cells and induced pluripotent stem cells, hence their increased usage in the stem cell therapy market. Because of their potency to differentiate into a wide range of cell types, ranging from bone and cartilage to muscle and fat cells, they are one of the versatile approaches to regenerative medicine, considering diseases of musculoskeletal disorders, cardiovascular diseases, and even skin wound healing.

Therefore, with the increasing demand for adult stem cells, market growth will be expected to be driven during the forecast period.

By Technology

Cell acquisition technology leads the technology segment of the global stem cell therapy market. This may be ascribed to the fact that high-quality stem cells are necessary for various therapeutic purposes and this is only possible through this technique. This technique involves collection from several sources such as bone marrow, peripheral blood, and umbilical cord blood.

These sources, especially bone marrow-derived stem cells and umbilical cord blood, form a significant basis for the treatment since they are the raw materials needed for the various forms of therapies. The dominance of this technology is mainly because it forms a pre-requisite for successful autologous and allogeneic stem cell therapies.

Given that steps of processing, expansion, and application can be effective only when there are efficient and safe methods of harvesting, bone marrow aspiration, apheresis, and the collection of cord blood have become established in clinical practice as reliable methods to harvest stem cells with minimal risk to the donor or patient.

Also, besides the development of methods of cell acquisition, such as better apheresis machines and the enhancement of bone marrow harvesting, the processes are getting faster, more efficient, and less invasive. This, in turn, has increased the availability of stem cells for therapeutic use and helped minimize the general cost of treatments with stem cells. While demands for stem cell therapies increase, technologies of cell acquisition will continue to play a key role in the market, boosting growth in the forecasted period.

By Administration

Due to its efficacy in treating joint-related conditions, the intra-articular route of administration constitutes the dominant segment of the route of administration section in the global stem cell therapy market. Intra-articular injections deliver the stem cells into the joint space directly, which enables the imparting of local treatment to the damaged joint cartilage and tissues. This form of administration enables the target tissue to have a more concentrated dose of stem cells, which may accelerate the process of tissue regeneration and alleviate pain.

The major advantage of intra-articular administration is that the delivery method is less invasive compared to surgical methods. Most patients with degenerative joint diseases would avoid surgery at all costs since other alternative treatments ensure quicker recovery and fewer risks.

Thus, intra-articular injections are a solution of convenience and efficiency, especially in elderly patients or those with comorbid conditions that make surgery hazardous. Additionally, the burgeoning prevalence of osteoarthritis and other joint disorders is increasing the demands placed on intra-articular stem cell therapies.

Moreover, advances in imaging technologies, such as ultrasound and MRI, have improved the accuracy of intra-articular injections by ensuring the deposition of stem cells precisely at damaged areas. All these have significantly enhanced the efficacy of the stem cell therapies administered for joint disorders and, therefore, increased the demand for this route of administration. With ongoing research into musculoskeletal disorders, this route of administration is poised to retain its lead within the global stem cell therapy market.

By Application

Musculoskeletal disorders currently lead the global stem cell therapy market due to rising incidence rates for diseases like osteoarthritis, tendonitis, and cartilage injuries for which stem cell therapy therapy offers significant promise. Muscle cells possess great potential for regenerative processes via MSCs in conditions affecting damaged cartilage and bone. Musculoskeletal applications remain highly popular due to the growing occurrence of degenerative joint and bone diseases in an aging population.

Osteoarthritis, one of the main causes of disability worldwide, can only currently be addressed with pain relief or surgical replacement of joints. Although noninvasive, intraarticular injection therapy helps repair and regenerate tissues which reduces pain while improving joint function. Patients often prefer its minimally invasive or nonsurgical nature for intra-articular injection treatments.

Stem cell therapy's ability to differentiate into both cartilage and bone cells combined with its anti-inflammatory functions make them very effective treatments for osteoarthritis and rheumatoid arthritis, among other musculoskeletal conditions. Current research and clinical trials related to stem cell therapy further support its utilization for these purposes.

By End User

Pharmaceutical and

biotechnology companies have always led in the research, development, and commercialization of treatments utilizing stem cells. They provide both financial support and technical expertise to advance therapeutic uses for stem cells. Companies invest heavily in stem cell therapies through

clinical trials for treating chronic illnesses like cancer, neurodegenerative conditions, and cardiovascular conditions - while their emphasis on regenerative medicine remains an attractive point.

Pharmaceutical and biotech companies are spearheading efforts to translate stem cell research into effective treatments, including cell-based therapies. Other companies increasingly specialize in personalized medicine, where stem cell therapies can be tailored specifically to individual patient's individual needs, providing benefits associated with traditional modes of therapy.

Strategic partnerships and collaborations with academic institutions and research centers further augment pharmaceutical and biotechnology companies' capability of exploring stem cell-related applications, providing more opportunities for finding treatments through academic, and industrial collaboration making these firms crucial stakeholders within stem cell therapy industries.

The Stem Cell therapy Market Report is segmented on the basis of the following

By Therapy

- Allogeneic Stem Cell Therapy

- Autologous Cellular Immunotherapies

- Autologous Stem Cell Therapy

- Syngeneic Stem Cell Therapy

By Cell Source

- Adult Stem Cells (ASCs)

- Hematopoietic Stem Cells (HSCs)

- Mesenchymal Stem Cells (MSCs)

- Neural Stem Cells

- Epithelial/Skin Stem Cells

- Others

- Human Embryonic Stem Cells (HESCs)

- Induced Pluripotent Stem Cells (iPSCs)

- Very Small Embryonic Stem Cells

By Technology

- Cell Acquisition

- Bone Marrow Harvest

- Umbilical Blood Cord

- Apheresis

- Cell Production

- Therapeutic Cloning

- In-vitro Fertilization

- Cell Culture and Isolation

- Gene Editing

- Cryopreservation

- Expansion and Sub-Culture

- Differentiation and Reprogramming

By Route of Administration

- Intraarticular

- Intracoronary

- Intramuscular

- Intramyocardial

- Intrathecal

- Intravenous

- Surgical Implantation

By Application

- Musculoskeletal Disorders

- Acute Graft Versus Host Disease (GVHD)

- Wounds and Injuries

- Cardiovascular Diseases

- Surgeries

- Gastrointestinal Diseases

- Other Applications

By End User

- Pharmaceutical and Biotechnology Companies

- Hospitals & Cell Banks

- Academic & Research Institutes

How Does Artificial Intelligence Contribute To Improve Stem Cell Therapy Market?

- Accelerated Research and Discovery: AI expedites the identification of stem cell differentiation pathways and potential therapeutic targets by analyzing large datasets from genomics, proteomics, and other studies. It helps predict cell behavior and optimize stem cell modifications for specific applications.

- Personalized Therapies: AI enhances personalized medicine by analyzing patient-specific data to develop tailored stem cell treatments. It predicts treatment efficacy and minimizes risks, ensuring optimal outcomes for individual patients.

- Clinical Trial Optimization: AI streamlines clinical trials by identifying suitable candidates, predicting trial outcomes, and improving study designs. It reduces time and costs associated with developing stem cell therapies.

- Quality Control: AI-powered systems monitor stem cell manufacturing processes, ensuring consistency, precision, and compliance with regulatory standards. Machine learning algorithms detect anomalies during production to maintain high-quality therapies.

- Predictive Analytics: AI provides insights into disease progression and treatment responses, enabling clinicians to refine therapeutic strategies and improve patient outcomes.

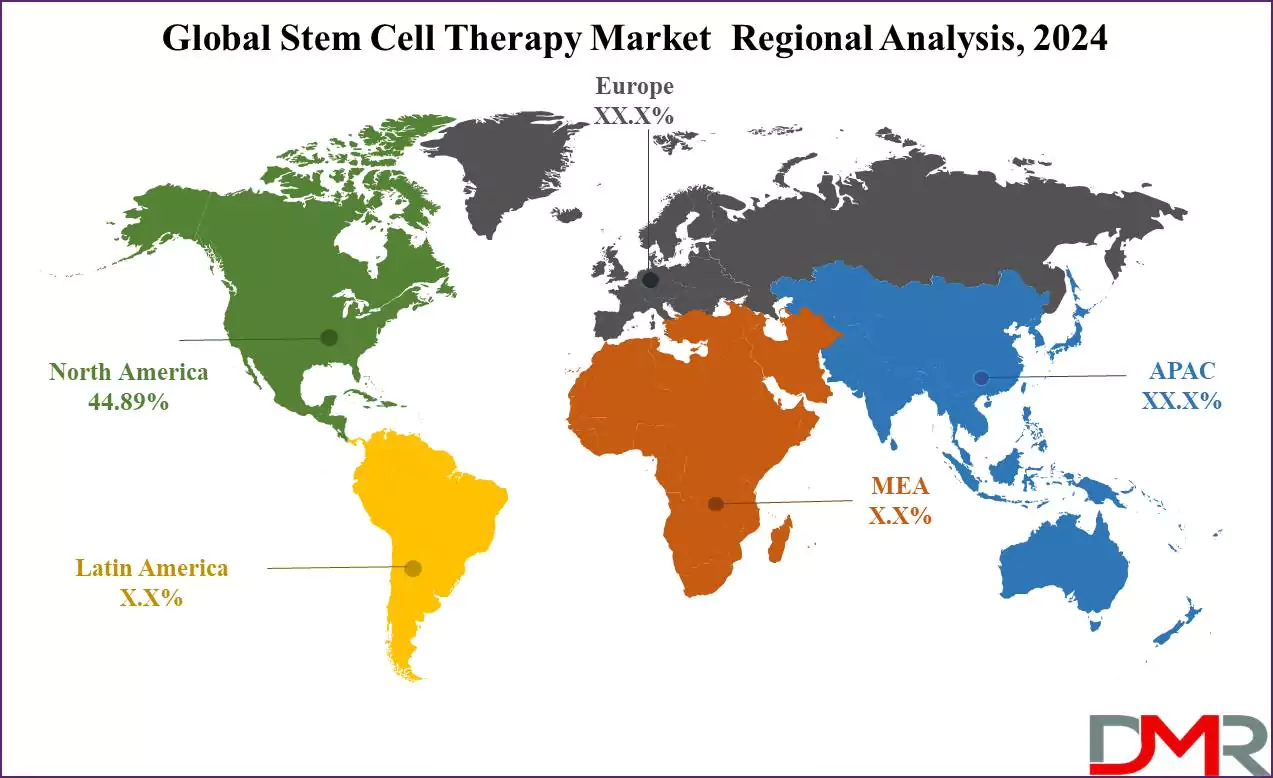

Stem Cell Therapy Market Regional Analysis

North America is projected to lead the global stem cell therapy market as it will

hold 44.89% of the market share by the end of 2024. The region is defined by various factors, including an established healthcare infrastructure, significant R&D investments, and supportive regulatory environments that foster commercialization.

Attributes that account for this market's high market share include its prevalence of chronic illnesses, an aging population, and increasing demands for personalized medicine in the U.S. The United States government has made tremendous strides toward stem cell research and development by allocating funding via agencies such as the National Institutes of Health. Private investments in biotechnology companies offering stem cell therapy products have also played a pivotal role in driving this market forward.

Furthermore, the FDA's rapid approval rate for

cell therapy products has fostered greater innovation and new therapies across the Asia Pacific region. Canada also plays an essential part in regional leadership through increasing clinical trials and research studies on stem cell therapy, while many Canadian research institutions pioneer innovative ways to harness stem cells to treat neurodegenerative disorders and cancer.

This dominance is Influencing several other key elements. One factor that plays an influential role is the presence of key market participants and biotech companies like Novartis, Pfizer, and Vertex Pharmaceuticals who specialize in stem cell therapies for further development and commercialization purposes. Furthermore, North America will likely maintain its dominant standing during this forecast period thanks to a robust ecosystem for research on advanced therapies as well as an expanding patient base.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Stem Cell Therapy Market Competitive Landscape

The global stem cell therapy market is relatively competitive, with major manufacturers involved in various strategies such as increasing their product portfolios, developing clinical trials, and strategic partnerships to further sustain the competitiveness in the market. Some of the key players operating in the market are Novartis AG, JCR Pharmaceuticals Co., Ltd., Fujifilm Holdings Corporation, Vertex Pharmaceuticals, Lonza Group, and Pluristem Therapeutics.

Novartis AG has announced its market-leading position in stem cell therapy, especially in

oncology, due to its CAR-T cell therapy known as Kymriah. Similarly, JCR Pharmaceuticals is developing regenerative medicines based on

stem cells, proposed for use in the treatment of various rare genetic disorders. Its experience in cell culture and manufacturing-related activities is being utilized by Fujifilm Holdings while developing stem cell therapy for indications related to age-related macular degeneration.

The market currently records strategic partnerships between biotechnology companies and research institutions or healthcare providers. For instance, the companies enter into licensing agreements or joint ventures to accelerate stem cell therapy developments. Mergers and acquisitions are also common, as bigger players seek capability expansion and market reach. This includes numerous key technological advances, especially in areas of cell expansion and cryopreservation.

Being able to construct efficient and scalable manufacturing processes will be an advantage for companies. Considering that more cell therapies are gaining regulatory approval and the arrival of new entrants into the market, the competitive intensity is high.

Some of the prominent players in the Global Stem Cell therapy Market are

- Thermo Fisher Scientific Inc

- STEMCELL Technologies Inc.

- Merck KGaA

- Sartorius AG (CellGenix GmbH)

- PromoCell GmbH

- Takara Holdings Inc.

- Lonza

- ATCC

- AcceGen

- Cell Applications Inc.

- Bio-Techne

- Cellular Engineering Technologies

- Other Key Players

Stem Cell Therapy Market Recent Developments

- October 2024: Fujifilm Holdings Corporation announced the expansion of its manufacturing facility for cell therapies in Texas, aimed at increasing production capacity for stem cell-based treatments targeting age-related macular degeneration.

- September 2024: JCR Pharmaceuticals Co., Ltd. received approval from the Japanese Ministry of Health for its stem cell therapy aimed at treating a rare form of genetic mucopolysaccharidosis, further strengthening its position in the regenerative medicine market.

- August 2024: Vertex Pharmaceuticals completed the acquisition of ViaCyte, a biotechnology firm focused on developing stem cell-derived therapies for type 1 diabetes. This acquisition enhances Vertex’s portfolio of regenerative treatments.

- July 2024: Pluristem Therapeutics announced the successful completion of Phase II clinical trials for its placental-derived stem cell therapy for the treatment of critical limb ischemia. The therapy is expected to move into Phase III trials by early 2025.

- June 2024: Novartis AG entered into a strategic partnership with a leading research institute in the U.S. to advance its pipeline of stem cell therapies for neurodegenerative diseases, focusing on Parkinson’s and Alzheimer’s diseases.

- May 2024: Lonza Group expanded its strategic collaboration with a U.S.-based biotech company to enhance its stem cell manufacturing capabilities, aiming to scale up production of autologous stem cell therapies for cancer and autoimmune diseases.

Stem Cell Therapy Market Report Details

|

Report Characteristics

|

| Market Size (2024) |

USD 18.9 Bn |

| Forecast Value (2033) |

USD 8.7 Bn |

| CAGR (2024-2033) |

12.6% |

| Historical Data |

2018 – 2023 |

| The US Market Size (2024) |

USD 7.1 Bn |

| Forecast Data |

2025 – 2033 |

| Base Year |

2023 |

| Estimate Year |

2024 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Therapy (Allogeneic Stem Cell Therapy, Autologous Cellular Immunotherapies, Autologous Stem Cell Therapy, Syngeneic Stem Cell Therapy), By Cell Source (Adult Stem Cells (ASCs), Human Embryonic Stem Cells (HESCs), Induced Pluripotent Stem Cells (iPSCs), and Very Small Embryonic Stem Cells), By Technology (Cell Acquisition, Cell Production, Cryopreservation, Expansion and Sub-Culture, and Differentiation and Reprogramming), By Route of Administration (Intraarticular, Intracoronary, Intramuscular, Intramyocardial, Intrathecal, Intravenous, and Surgical Implantation), By Application (Musculoskeletal Disorders, Acute Graft Versus Host Disease (AGVHD), Wounds and Injuries¸ Cardiovascular Diseases, Surgeries, Gastrointestinal Diseases, and Other Applications), By End Users (Pharmaceutical and Biotechnology Companies, Hospitals & Cell Banks, and Academic & Research Institutes) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia- Pacific– China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

Thermo Fisher Scientific Inc, STEMCELL Technologies Inc., Merck KGaA, Sartorius AG (CellGenix GmbH), PromoCell GmbH, Takara Holdings Inc., Lonza, ATCC, AcceGen, Cell Applications Inc., Bio-Techne, Cellular Engineering Technologies, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |