What is the Sustainable Agrochemical Formulation Market Size?

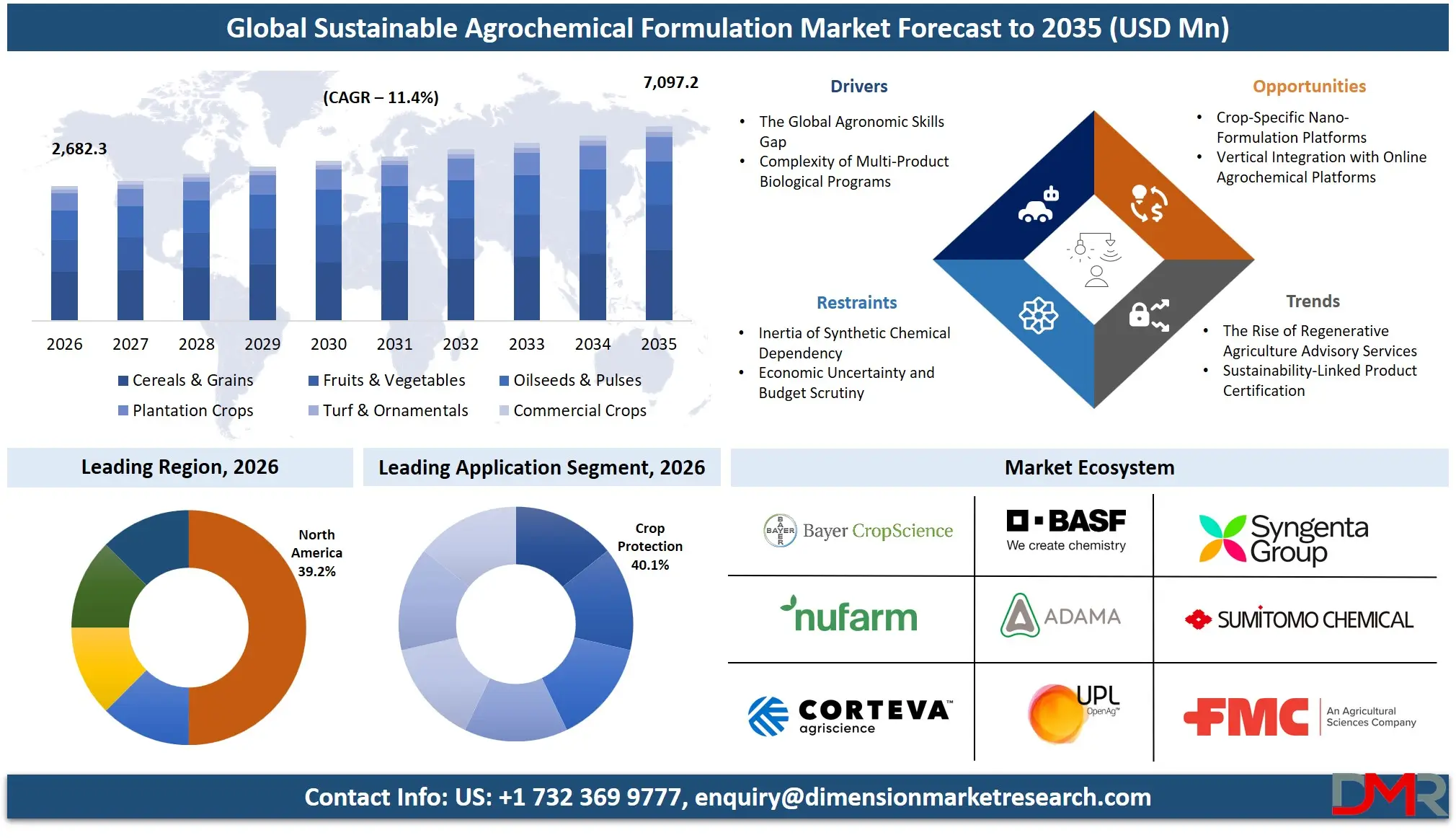

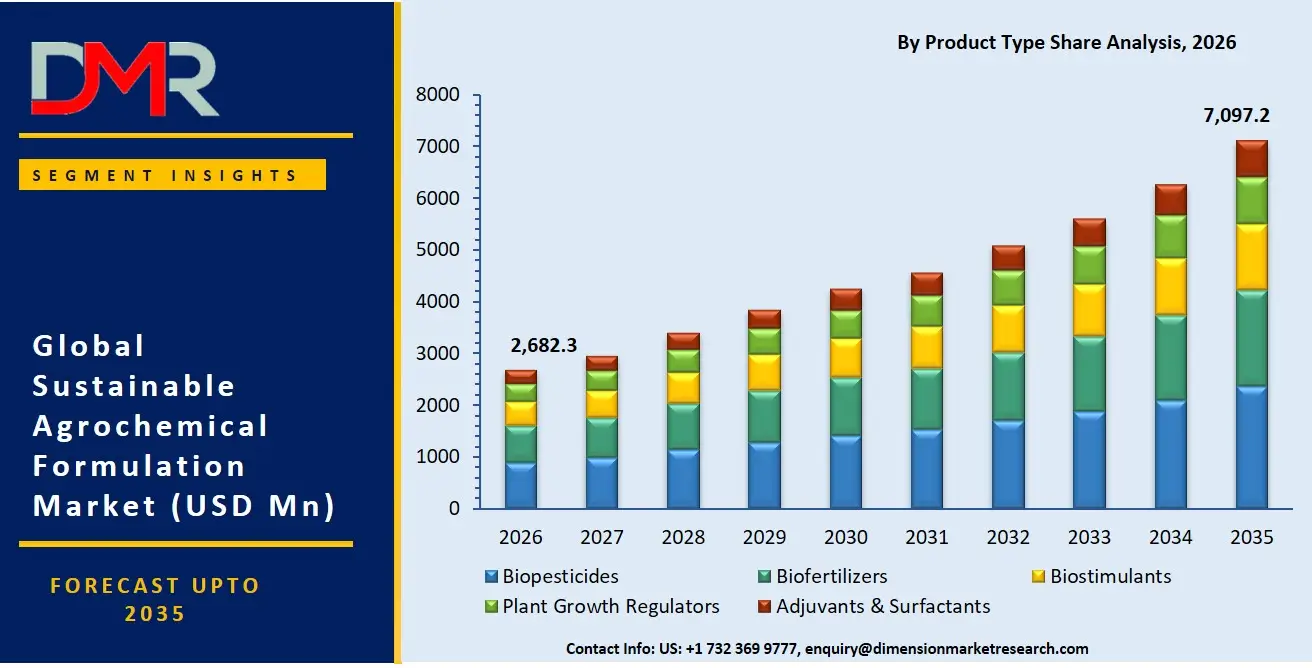

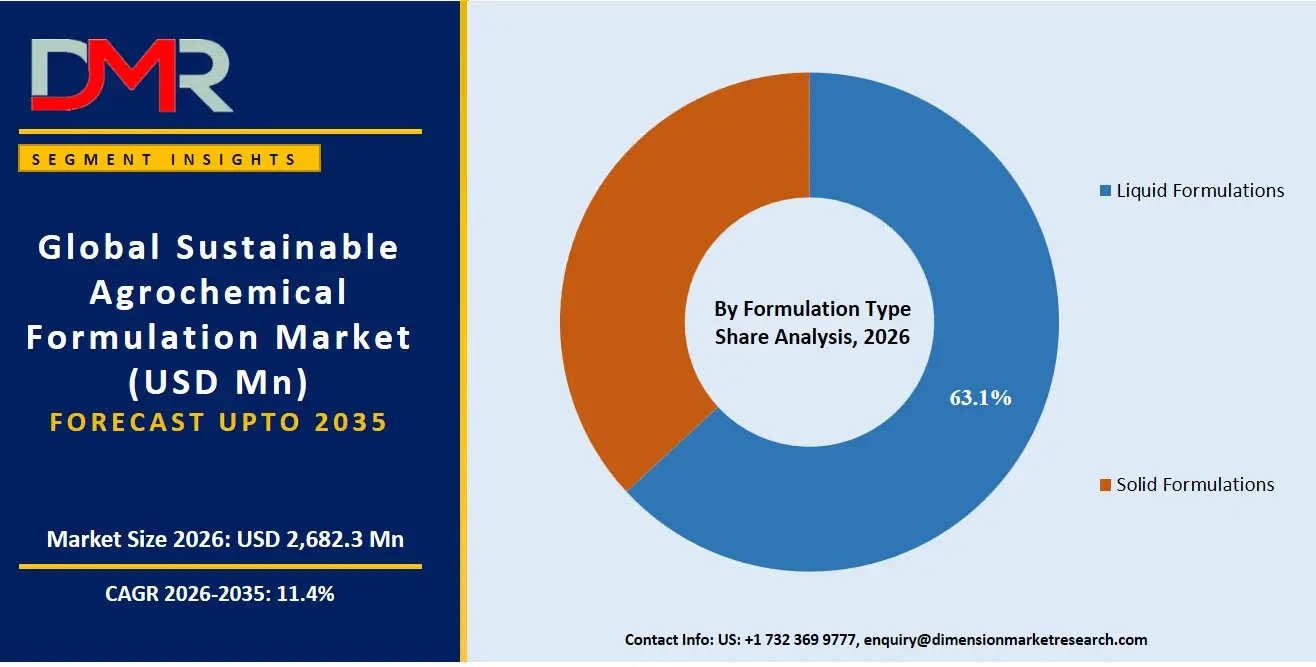

The Global Sustainable Agrochemical Formulation Market is expected to reach a value of USD 2,682.3 million in 2026, and it is further anticipated to reach USD 7,097.2 million by 2035, growing at a CAGR of 11.4% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The market for sustainable agrochemical formulation is growing due to the rise in regenerative processes being adopted in the agricultural industry, as well as the process of moving away from the usage of chemicals towards bio-based or biochemicals. This market consists of bio-pesticides, bio-fertilizers, bio-stimulants, among others.

There are also other categories of formulations such as nano-encapsulated and controlled release formulations, which are aimed at helping farmers and agricultural companies switch towards adopting IPM and organic farming approaches. There is an increasing need for formulation due to factors such as precision agriculture, restoring the soil, and building resilience to climatic challenges in nutrient intake for crops. Farming companies are the main adopters of these formulations, with the preference of formulations being Liquid formulations (Suspension Concentrates) and Microbial sources because of how easy and efficient they are to use and perform in the field. Some of the sectors that require formulations are cereals and grains, plantation crops, and fruits and vegetables.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

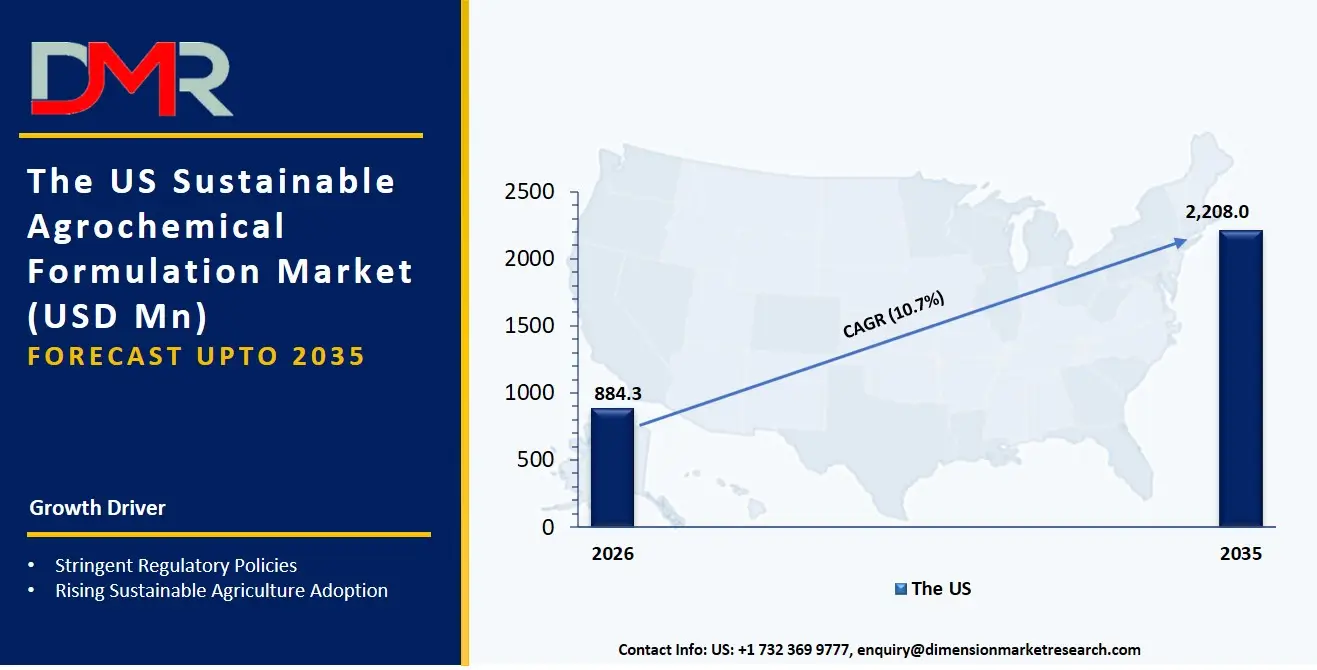

The US Sustainable Agrochemical Formulation Market

The US Sustainable Agrochemical Formulation Market is projected to reach USD 884.3 million in 2026 at a compound annual growth rate of 10.7% over its forecast period, culminating in a value of USD 2,208.0 million by 2035. With an increase in the number of biological R&D centers, and the agribusiness giants initiating regenerative agriculture initiatives in the United States, the country continues to be the biggest and most developed market for sustainable formulations for agrochemicals. There has been immense interest in using bio-fungicides and bio-insecticides, where there has been a need to ensure that LSC's (liquid suspension concentrates) have microbial stability. In addition, the introduction of Nano-formulation tools in the process flow of agrochemicals is leading to the same requirement for Adjuvants & Surfactants Consulting Service.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Europe Sustainable Agrochemical Formulation Market

The Europe Sustainable Agrochemical Formulation Market is estimated to be valued at USD 1,051.5 million in 2026 and is further anticipated to reach USD 2,782.1 million by 2035 at a CAGR of 11.4%. The regulatory activities of the likes of the EU Green Deal and the Farm to Fork Strategy have a significant effect on the European market. This is because there is an increasing need for biostimulant (seaweed extract & humic acid) and controlled release application. Microencapsulation technology is experiencing rapid growth within Europe due to the need to balance crop protection and MRLs for fruits, vegetables, and vines grown in countries like France, Italy, and Spain. Another factor influencing the development of new technologies within the formulation market is initiatives like the EU Soil Health Law, which calls for the creation of soil treatment products capable of carbon sequestration and microbial diversity.

The Japan Sustainable Agrochemical Formulation Market

The Japan Sustainable Agrochemical Formulation Market is projected to be valued at USD 155.6 million in 2026. It is further expected to witness robust growth, holding USD 395.8 million in 2035 at a CAGR of 10.9%. What sets Japan apart in the agricultural sector is that due to the aging population of farmers coupled with abandonment of arable lands, a common approach within corporations at the national level is regenerative agriculture. As far as the percentage of plant growth regulators and biofertilizers (phosphate solubilizing microbes) is concerned, it constitutes a major part of the costs as agricultural cooperatives switch from artificial fertilizer to biological fertilizer. Another factor where the need for integration is essential is in local distribution channels, in light of the gap that exists between traditional methods of agriculture and innovative approaches such as nano-fertilizer in the form of WDG and micro-encapsulated formulation.

Key Takeaways

- Market Size & Forecast: The Global Sustainable Agrochemical Formulation market is projected to reach USD 2,682.3 million in 2026, and further increase to USD 7,097.2 million in 2035 due to growing demand for regenerative farming and the necessity of removing artificial chemicals from the food production cycle.

- Growth Rate & Outlook: The overall market is expected to grow at a CAGR of 11.4% due to the scarcity of biologists skilled in formulating agrochemicals in-house and challenges faced in maintaining microbial life in liquid form formulations and nano-encapsulation technology.

- Primary Growth Drivers: The main factors driving market growth are the gradual movement from conventional fertilizers to biofertilizers, which include nitrogen-fixation and phosphate-solubilization, the need for adjuvants and surfactants to avoid tank mixing issues, and the implementation of IPM practices using novel biopesticide formulation processes.

- Key Market Trends: The most prominent trends include the formulation of product blends specific to crops, such as corn biostimulant formulation and rice bio-fertilizer, application of Artificial Intelligence in analyzing the stability of microencapsulation formulas to forecast the release rates, and the shift towards nano-formulations as board members aim to improve input use efficiency.

- By Product Type Analysis: The biopesticides is projected to hold a major share of the product type segment owing to the increasing awareness about chemical residue and pest resistance issues. The bio-insecticides have become more prevalent owing to increased insect attacks due to climate change and growing demand for organic products.

- By Crop Type Analysis: The liquid formulations segment is anticipated to hold the dominant share of the formulation type segment. This can be attributed to their ease of application and higher mixing efficiency. Their ability to retain microbes, better nutrient intake, and suitability for foliar application contributes to their widespread acceptance in commercial agriculture.

- Regional Leadership: North America is expected to lead as it accounts for 39.2% market share by 2026, largely due to the extensive use of biological transition among row crop growers, as well as the advanced biological research and development environment.

What is the Sustainable Agrochemical Formulation?

Sustainable agrochemical formulations are specialized biological and biochemical input development services provided by third-party agrochemical formulators, R&D labs and agrochemical contract manufacturers to help the agrochemical companies at every stage in the product lifecycle. Such services, which do not involve the production of raw active ingredients, pertain to the how of biological stability and field performance. This involves microbial fermentation optimization to ensure bacterial/fungal viability, biochemical extraction from plant sources, nano-encapsulation for controlled release, and adjuvant chemistry to ensure tank-mix compatibility. Biological investments have a tangible impact on yield and not product degradation when 85% of growers require reduced chemical residues, but professional formulation services are required to ensure shelf-life stability, thermal tolerance and field efficacy.

Use Cases

- Nano-Formulation for Soybean Nematode Control: Agricultural input companies seek and pay for microencapsulated formulation services that help them formulate bio-nematicides with controlled-release profiles that protect soybean root zones for 60 days against root-knot nematodes.

- Seaweed Extract Stabilization in Horticulture: Greenhouse growers utilize biostimulant formulation services to stabilize seaweed extracts and humic acids in liquid suspension concentrates (SC) that can be stored and effectively applied by drip irrigation without emitter blockages.

- Bio-Insecticide Viability in Tropical Climates: Plantation crop growers (oil palm, rubber) partner with microbial formulation companies to create desiccation-tolerant spores of bacteria (such as Bacillus thuringiensis) that can endure high-temperature storage and field use.

- Regenerative Soil Amendment Blending: Large organic farms offer a granular formulation service to mix phosphate-solubilizing bacteria with organic carriers and directly apply them to the soil, thereby increasing phosphorus availability and increasing soil organic matter.

How AI is Transforming the Sustainable Agrochemical Formulation Market?

AI is transforming the sustainable agrochemical formulation market by speeding up formulation stability testing and boosting the prediction of field efficacy. AI-driven predictive modeling tools can streamline the development process by automatically optimizing the polymer wall thickness and release kinetics in nano-formulations and microencapsulated formulations, significantly reducing the requirement for iterative wet-lab testing and development timeline. At the same time, AI capabilities within adjuvants & surfactants development enable formulators to more accurately predict tank-mix interactions by processing thousands of compatibility data points and help eliminate the potential for precipitation or viability loss prior to field application.

AI is also the subject of governance and product development projects. In terms of biopesticide development, intelligent viability monitoring algorithms continuously predict degradation trends and detect formulation weaknesses, allowing an organization to meet regulatory requirements such as the USDA Organic and EU EC 834/2007. Moreover, generative AI assistants are complementing contract formulation consulting by simulating field release profiles and modeling crop uptake dynamics to give stakeholders a visualization of product performance before committing manufacturing resources.

Market Dynamics

Key Drivers in the Global Sustainable Agrochemical Formulation Market

The Global Biological Formulation Skills Gap

Various global agricultural firms are struggling to recruit qualified formulation biologists with know-how on microbial stabilization, nano-encapsulation and biopolymer chemistry. There is a structural shortage in the labor market, as these skills are growing faster than the number of educated talents. This has resulted in a trend for enterprises to rely on the work of professional contract formulation companies instead of relying on their own R&D. These companies help in critical operations such as optimization of microbial fermentation process, microencapsulation, or design of controlled-release matrix. By outsourcing these functions, companies can speed up the process of getting biological products to market and reduce the risk of batch failures because of inadequate in-house capacity.

Complexity of Multi-Strain Microbial Compatibility

Larger businesses are more likely to be producing products with multiple microbial strains (bacteria, fungi and algae) that offer a diverse range of soil health benefits. However, it is extremely difficult to keep multiple organisms viable in single liquid formulations. It is important to consider the needs for different genera in terms of pH, osmotic pressure, preservative systems and anaerobic vs aerobic requirements. Without the expertise of skilled formulators this complexity can result in antagonism, shorter shelf life, and failures in the field. Therefore, the need for suspension concentrate (SC) and water-dispersible granule (WDG) formulation services to support businesses in co-formulating compatible microbial consortia has been increasing.

Restraints in the Global Sustainable Agrochemical Formulation Market

Inertia of Synthetic Chemical Distribution Channels

The majority of the agricultural distributors still have decades-old infrastructure for synthetic chemical herbicides and pesticides that are thermally stable with an infinite shelf life. Although biological products provide better soil health results, these distribution networks are a big hurdle towards change. Expensive and risky to change refrigerated supply chain for viable microbes or to educate dealer network to store it correctly. Rather a lot of cold chain planning and stability testing is required when there are shelf life failures of millions of dollars of inventory. The organisations are worried of product returns, loss of farmers' trust and unexpected storage costs in the process. Therefore, legacy distribution slows down the biological adoption process and is likely to stall more impactful scales of regenerative agriculture transition.

Economic Uncertainty and Farm Budget Scrutiny

The uncertainty of commodity prices and weather conditions has made growers more reluctant to invest in higher-cost biological inputs. Despite soil health still being a long-term goal, farm managers are under increasing pressure to account for every dollar spent on inputs and deliver an output response. Formulation fees and long-term R&D engagement models of contract manufacturing providers are more likely to be under greater scrutiny. Growers turned to short-term, one-season biological tests that offer immediate operational advantage or cost savings. Until the formulators can show a short-term return on investment, long-term soil regeneration and multi-year application plans for biostimulants are more likely to be postponed. All this is making formulation companies more performance-driven and results-oriented.

Growth Opportunities in the Global Sustainable Agrochemical Formulation Market

Nano-Formulation for Targeted Delivery

Environmental soil health is also emerging as a key aspect in formulation decisions as agribusinesses are under pressure to achieve carbon sequestration goals and minimize synthetic input dependence. Now, agricultural companies are on the lookout for formulation strategies that can boost crop performance, minimize soil disturbance, and reduce environmental impact. This has brought about the need for regenerative agriculture formulation consulting services. A professional formulation service provider can help organizations choose the right carbon-based carriers, optimize microbial consortia for soil carbon building and formulate seed treatments to help lower synthetic fertilizer needs.

Vertical-Specific Biostimulant Blends

Environmental soil health is also emerging as a key aspect in formulation decisions as agribusinesses are under pressure to achieve carbon sequestration goals and minimize synthetic input dependence. Now, agricultural companies are on the lookout for formulation strategies to boost crop performance, minimize soil disturbance, and reduce environmental impact. This has brought about the need for regenerative agriculture formulation consulting services. A professional formulation service provider can help organizations choose the right carbon-based carriers, optimize microbial consortia for soil carbon building and formulate seed treatments to help lower synthetic fertilizer needs.

Trends in the Global Sustainable Agrochemical Formulation Market

The Rise of Microencapsulated Biopesticides

Microencapsulation is one of the latest techniques gaining interest in the biopesticide industry as an alternative to the traditional emulsifiable concentrates (EC). Agricultural companies are constructing microencapsulated formulations that deliver extended pest control over weeks rather than days, rather than having rapid UV degradation and wash-off. The microcapsules allow slow release of bio-insecticide or bio-fungicide in the phyllosphere or rhizosphere. Contract formulation service providers are responding with expertise in polymer shell chemistry, release kinetics modeling and spray drying scale-up.

Regenerative Agriculture Formulation Services

Environmental soil health is also emerging as a key aspect in formulation decisions as agribusinesses are under pressure to achieve carbon sequestration goals and minimize synthetic input dependence. Now, agricultural companies are on the lookout for formulation strategies which can be used for boosting the performance of the crop and reducing the disturbance of the soil, as well as reduce the environmental impact. This has brought about the need for regenerative agriculture formulation consulting services. A professional formulation service provider can help organizations choose the right carbon-based carriers, optimize microbial consortia for soil carbon building and formulate seed treatments to help lower synthetic fertilizer needs.

Research Scope and Analysis

The enzymatic chemical synthesis market is driven by rising adoption across pharmaceuticals, biotechnology, diagnostics, and green manufacturing industries. Growth is supported by advancements in enzyme engineering, increasing demand for sustainable synthesis methods, and expanding applications in biologics, nucleic acids, and fine chemical production.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Source Analysis

The microbial segment is projected to be the leading segment in the Global Sustainable Agrochemical Formulation Market due to its compatibility with environment-friendly agricultural practices and effectiveness in enhancing the productivity of the crops. Bacterial formulations are the most widely used microbial formulations, as they have many applications, such as nitrogen fixation, phosphate solubilization and biological pest suppression. Fungi based products are also in great demand in disease management and soil health restoration. The growing adoption of residue-free farming, the limitation of synthetic chemicals, and governmental support of bio-based farming inputs are driving the penetration of microbial products. Microbial formulations are the most important source category in the world because they are easy to scale up, have less environmental impact and are compatible with IPM systems.

By Product Type Analysis

The product type segment is projected to be led by biopesticides as people become more concerned with chemical pesticide residues, pest resistance, and environmental sustainability. Among biopesticides, bio-insecticides are the most represented ones due to the growing number of insect infestation due to climate change and to regulations on conventional insecticides. Biological methods of crop protection are being adopted quickly by farmers as they provide pest control without killing beneficial organisms and soil biodiversity. Increased growth is especially evident in export oriented and residue compliance crops, such as fruits and vegetables. The market is witnessing continued leadership of biopesticides globally as the acreage for organic farming continues to expand and microbial technologies are being developed and the preference of consumers for clean label food products continues to rise.

By Formulation Type Analysis

Liquid formulations are poised to hold on to the major share of the formulation type segment, owing to its ease of application, good mixing characteristics, and high compatibility with the latest precision agriculture devices. Suspension concentrate and emulsifiable concentrate are especially desirable for field use due to the greater stability and uniform dispersion, and the greater biological activity. Liquid products are preferred by farmers for foliar spraying and fertigation particularly in high value horticulture and commercial farms. Moreover, liquid formulations allow nutrients to be better absorbed and for the microbes to be more viable than some of the traditional solid formulations. The widespread use of automated spraying technologies and precision farming practices also helps to propel liquid sustainable agrochemicals as the global market leader.

By Crop Type Analysis

The leading crop type segment is cereals and grains, as they are the largest agricultural land under cultivation and are in constant need of crop protection and soil enhancement solutions. Wheat, rice and maize are the major crops that use significant amounts of sustainable agrochemical formulations to sustain productivity against the growing climate stress and pest pressure. Many governments in various countries are encouraging the use of sustainable farming inputs in the production of staple crops to enhance food security and dependability while decreasing reliance on chemicals. Biofertilizers and biostimulants, are more and more incorporated in cereal cropping systems to maximize the nutrient efficiency and soil fertility. Cereals and grains are the key crop area, mainly owing to the volume of production and the regularity of application requirements.

By Distribution Channel Analysis

The distribution channel segment is dominated by distributors and dealers, offering farmers a wide reach in rural areas, technical support, and product availability in various farming regions. Farmers depend on local agrochemical pedlars for advice on products, dosage levels and the like, and on their experiences to decide on which agrochemicals to buy when. These channels are better in touch with farmers and provide instant availability of products, and are more influential than direct sales in various markets in developing countries. Dealers play an important role in emerging economies by enabling credit-based sales and regional after-sales service. While online agrochemical platforms increase in number at an impressive rate, traditional distributor systems are still dominant because of the existing level of trust, the logistics system, and the robust field-level engagement.

By Application Analysis

The crop protection application segment is the most prominent one as the sustainable agrochemical formulations are primarily being adopted to control weeds, pest, and diseases while maintaining low environmental impact. The use of biological crop protection products is gaining ground as a result of growing resistance to synthetic pesticides and increasingly strict global residue regulations. Sustainable formulations assist in preserving the quality of crop yields and promote the conservation of biodiversity and improvement of soil health. There is a high demand in high value horticulture, export crops and integrated farming system for residue free production. Crop protection remains the largest application area in the global market, as more growers are adopting IPM practices and there is greater awareness of ecological methods.

By End User Analysis

Commercial farming is the major end user segment, owing to the huge scale of farming operations, greater purchasing power and the increasing focus on sustainable productivity improvement. As commercial farmers face pressure to adhere to environmental regulations, enhance soil health and cater to the consumer demand for sustainable food production, there is a growing trend towards using bio-based formulations of agrochemicals. These farms proactively incorporate biostimulants, biofertilizers, and biopesticides into precision agriculture systems to maximize potential yields and minimize reliance on synthetic chemicals. In addition, the increasing requirements for export quality and for sustainability certification are driving commercial agricultural producers to move towards greener agricultural production methods.

The Global Sustainable Agrochemical Formulation Market Report is segmented on the basis of the following:

By Source

- Microbial

- Biochemical

- Plant Extracts

- Organic Acids

- Botanical

- Plant-Derived Essential Oils

- Resins

By Product Type

- Biopesticides

- Bio-Insecticides

- Bio-Fungicides

- Bio-Nematicides

- Biofertilizers

- Nitrogen-Fixing

- Phosphate-Solubilizing

- Potash-Mobilizing Microbes

- Biostimulants

- Seaweed Extracts

- Humic Acids

- Amino Acids

- Plant Growth Regulators

- Adjuvants & Surfactants

By Formulation Type

- Liquid Formulations

- Suspension Concentrates (SC)

- Emulsifiable Concentrates (EC)

- Water-Dispersible Granules (WDG)

- Solid Formulations

- Water-Dispersible Granules (WDG)

- Granular Formulations

- Microencapsulated Formulations

- Controlled-Release Formulations

- Nano-Formulations

By Crop Type

- Cereals & Grains

- Fruits & Vegetables

- Oilseeds & Pulses

- Plantation Crops

- Turf & Ornamentals

- Commercial Crops

By Distribution Channel

- Direct Sales

- Distributors & Dealers

- Agricultural Cooperatives

- Online Agrochemical Platforms

By Application

- Crop Protection

- Soil Treatment

- Seed Treatment

- Foliar Spray

- Fertilizer Application

- Integrated Pest Management (IPM)

- Regenerative Agriculture

By End User

- Commercial Farming

- Organic Farming

- Greenhouse Cultivation

- Agrochemical Manufacturers

- Contract Formulation Companies

- Agricultural Cooperatives

Regional Analysis

Leading Region by Market Share

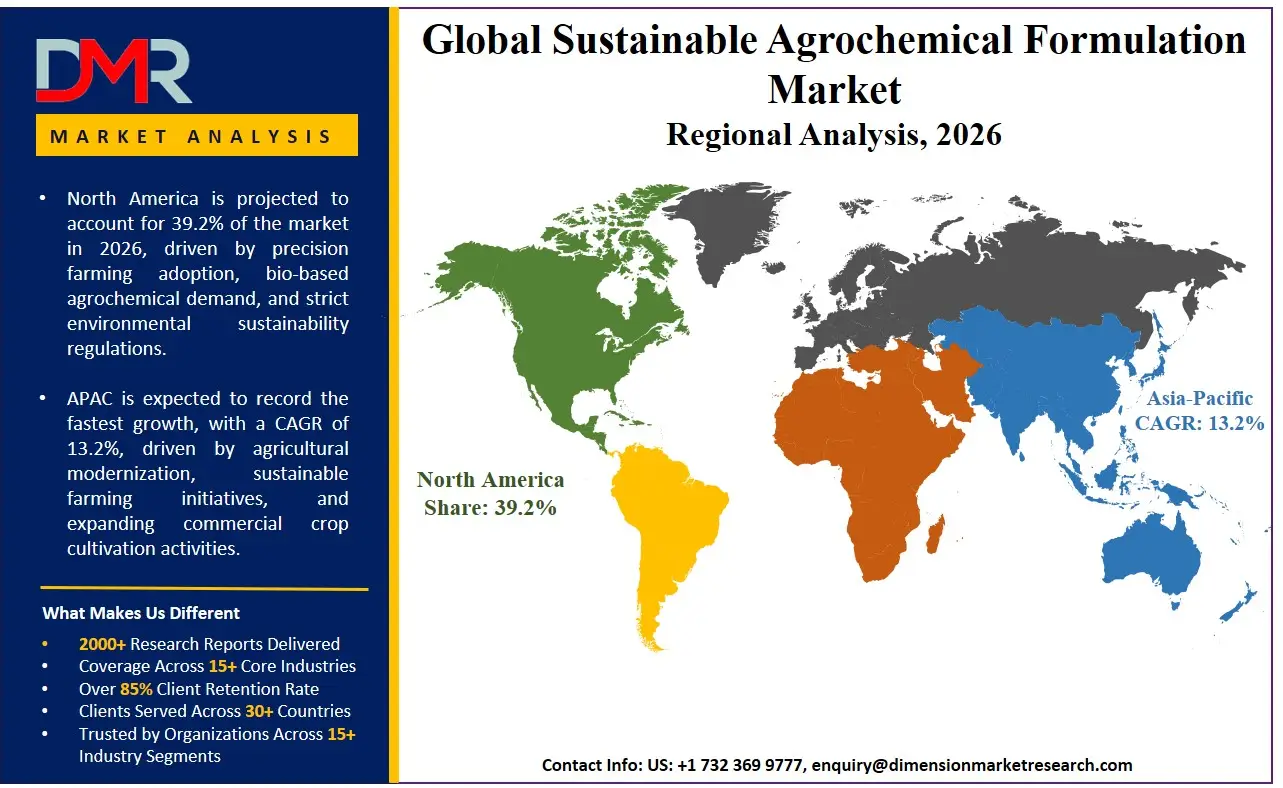

North America is set to lead the global sustainable agrochemical formulation market accounting for 39.2% of the market share by the end of 2026. The United States leads North America in this market due to its unparalleled biological R&D hub and the ambitious programs of regenerative farming of key agribusinesses. Contracted formulators and microbial fermentation facilities exist in the region, and there is a large pool of talent in the fields of formulation chemistry and fermentation science. The rising demand for bio-insecticide and bio-fungicide formulation and stability optimization is driven by enterprises' investment in biological alternatives and in nano-formulation technologies, as well as in overall transition from synthetic soil fumigants. Further, a positive view on VC activity is always investing in new biological startups that require specialized formulation solutions to scale up quickly and comply with regulations.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Regional Market

The Asia Pacific region is anticipated to witness the fastest growth in the sustainable agrochemical formulation market in the coming years, owing to the government initiatives for complete elimination of the use of chemical fertilizers in India, China, Japan, and Southeast Asia. The rapid population growth, growing awareness of food safety among the middle class and the evolving and vibrant organic export market are forcing the existing agribusinesses and agricultural cooperatives to abandon the traditional use of synthetic inputs. The production of biofertilizer formulations and biostimulants (seaweed extract & humic acid) is much sought after to guide these big institutions towards a biological operating model. Additionally, there is a serious shortage of qualified formulation biologists and fermentation engineers in the region, and most importantly contract formulation services need to be outsourced to implement, scale and stabilize biological products to bridge the skills gap and accelerate investments in sustainable agriculture projects.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competition dynamics in the formulation of sustainable agrochemicals globally have been characterized by intense competition in the presence of a diverse collection of multinational contract manufacturing organizations (CMOs), biological research and development branches of established agrochemical firms, and boutique microbial formulations firms. The strategy behind all of this is that only the most powerful strategic partnerships with agricultural biological firms (such as Corteva Biologicals, UPL Natural Plant Protection, Syngenta Biologicals) will provide the needed collaborations and access to microbial strains and actives. Market consolidation trends have been on the rise, with legacy chemical formulation firms purchasing boutiques with capabilities for microencapsulation and nano-formulation. Proprietary intellectual property, such as stabilized microbial platforms for viability and crop-specific models for release kinetics, is now more valuable to competitive advantage than mere fermentation and mixing capabilities.

Some of the prominent players in the Global Sustainable Agrochemical Formulation Market are:

- Bayer CropScience

- Syngenta Group

- BASF SE

- Corteva Agriscience

- FMC Corporation

- UPL Limited

- Sumitomo Chemical

- Nufarm Limited

- ADAMA Ltd.

- Bioceres Crop Solutions (formerly Marrone Bio Innovations)

- Novonesis Group (formerly Novozymes)

- Koppert Biological Systems

- Certis Biologicals

- Yara International

- Valent BioSciences

- Verdesian Life Sciences

- Andermatt Group

- PI Industries

- Seipasa S.A.

- Other Key Players

Recent Developments

- January 2026: BASF made an announcement about expanding its biological formulation innovation center that is a professional formulation strategy to help its clients who work in fruits & vegetables and plantation crops to develop their own microbial consortium using its microencapsulation technology and suspension concentrate formulation capability.

- November 2025: Corteva Agriscience reinforced its partnership with Novozymes and also established a special practice of phosphate solubilizing biofertilizers along with a controlled-release formulation strategy that will help cereal and grain farmers to switch from high phosphorus input to low phosphorus in corn and wheat production.

- October 2025: The NPP segment (Natural Plant Protection) of UPL purchased a European microencapsulation technology company in order to continue with its development in formulation strategies related to bio-insecticides and seed treatments for plantation crops because of complex demands from rubber and oil palm farmers in Southeast Asia.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 2,682.3 Mn |

| Forecast Value (2035) |

USD 7,097.2 Mn |

| CAGR (2026–2035) |

11.4% |

| The US Market Size (2026) |

USD 884.3 Mn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Source, By Product Type, By Formulation Type, By Crop Type, By Distribution Channel, By Application, and By End User |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Sustainable Agrochemical Formulation Market?

▾ The Global Sustainable Agrochemical Formulation market is poised to be valued at USD 2,682.3 million in 2026 and is projected to reach USD 7,097.2 million by 2035, driven by the universal need for specialized skills in microbial stabilization, nano-formulation, and biological product scale-up.

What is the CAGR of the Global Sustainable Agrochemical Formulation Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 11.4% from 2026 to 2035, reflecting the accelerating complexity of multi-strain microbial formulation and the persistent shortage of internal biological formulation engineering talent.

What factors are driving the growth of the Global Sustainable Agrochemical Formulation Market?

▾ Key drivers include the global biological formulation skills gap, the imperative to replace synthetic inputs with biofertilizers and biopesticides, the management complexity of microbial viability in liquid formulations, and the surge in demand for nano-formulations and controlled-release systems amid evolving fertilizer reduction regulations.

Which region held the largest share of the Sustainable Agrochemical Formulation Market in 2026?

▾ North America (specifically the United States) is projected to hold 39.2% of the market share in 2026, driven by a mature biological R&D ecosystem and aggressive enterprise investment in suspension concentrate (SC) formulation and microbial fermentation capabilities.

Which region is expected to grow the fastest in the Sustainable Agrochemical Formulation Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid regenerative agriculture adoption in India, China, and Japan, where biofertilizer formulation and biostimulant production are critical for transitioning large agricultural economies to reduced-chemical operating models.

What are the major trends in the Global Sustainable Agrochemical Formulation Market?

▾ Major trends include the integration of microencapsulated biopesticides, the rise of nano-formulations for targeted delivery, the demand for crop-specific biostimulant blends (e.g., for fruits & vegetables), and the focus on controlled-release formulations within regenerative agriculture systems.

Who are the key players in the Global Sustainable Agrochemical Formulation Market?

▾ Key players include large agrochemical biological divisions like BASF, Bayer, Corteva, UPL, and Syngenta, alongside specialized biological manufacturers such as Novozymes, Koppert, Valent BioSciences, Marrone Bio Innovations, and contract formulation companies.

How is the Global Sustainable Agrochemical Formulation Market segmented?

▾ The market is segmented by Source, Product Type, Formulation Type, Crop Type, Distribution Channel, Application, and End User.