What is the AdTech Market Size?

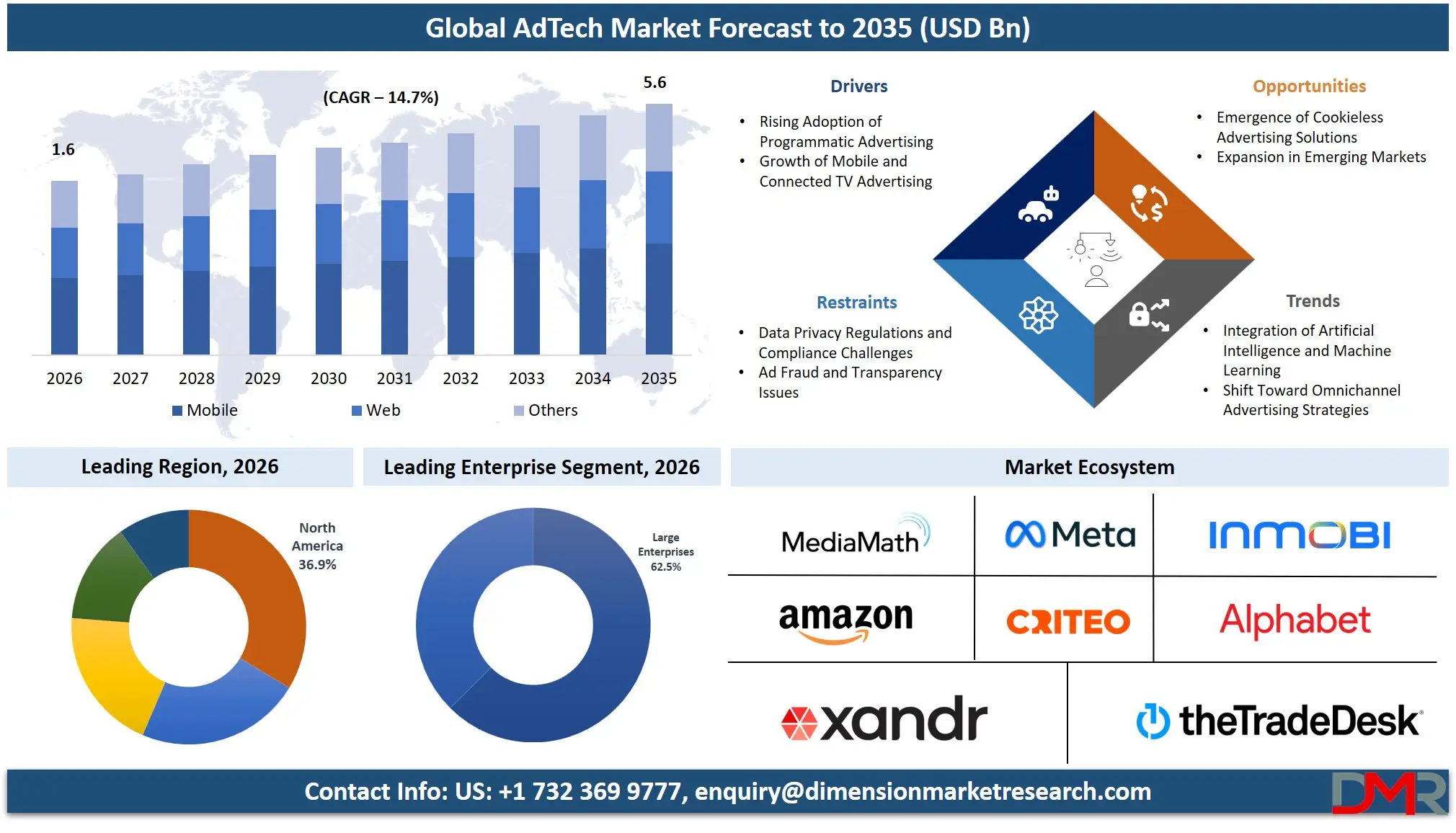

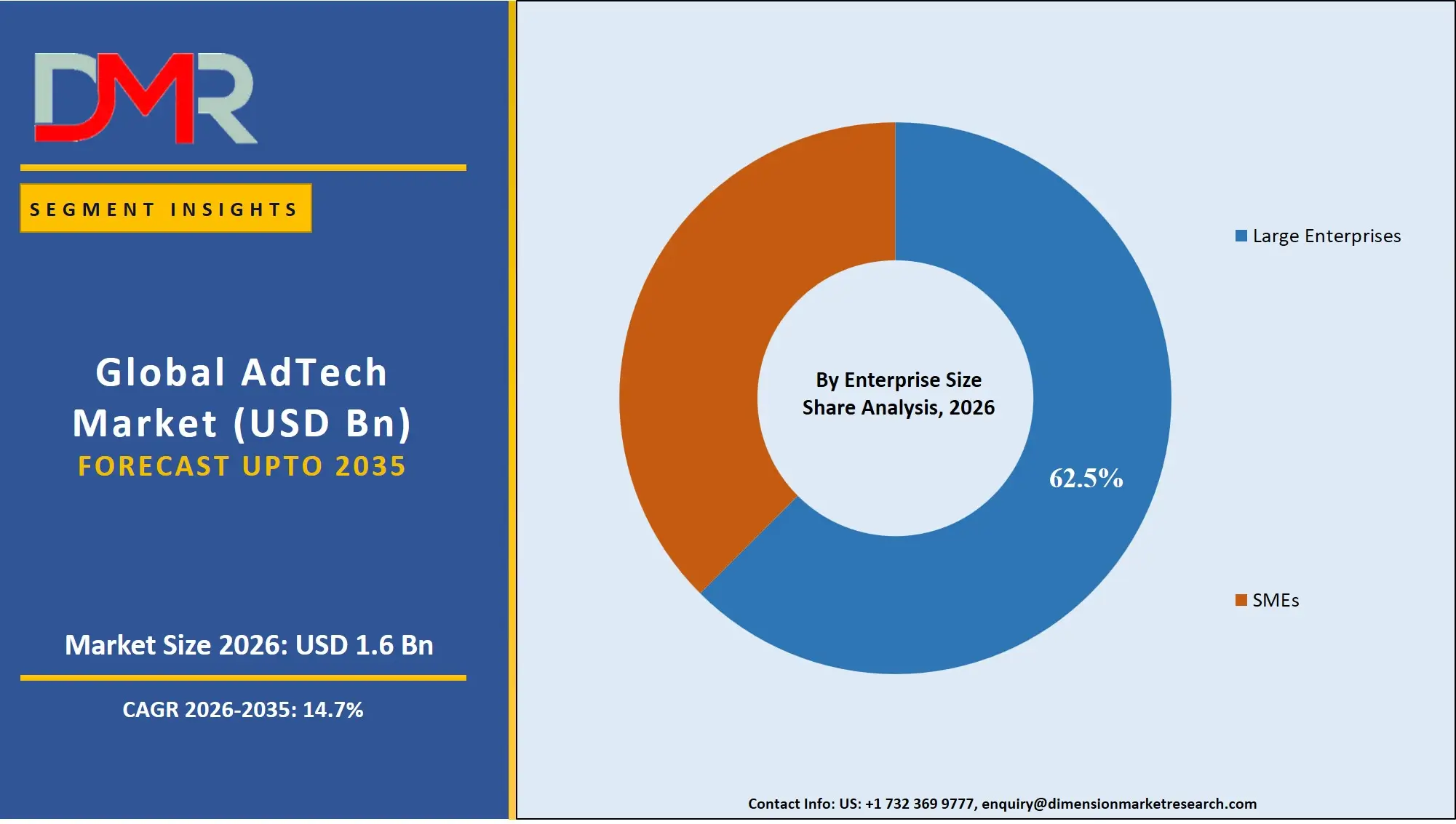

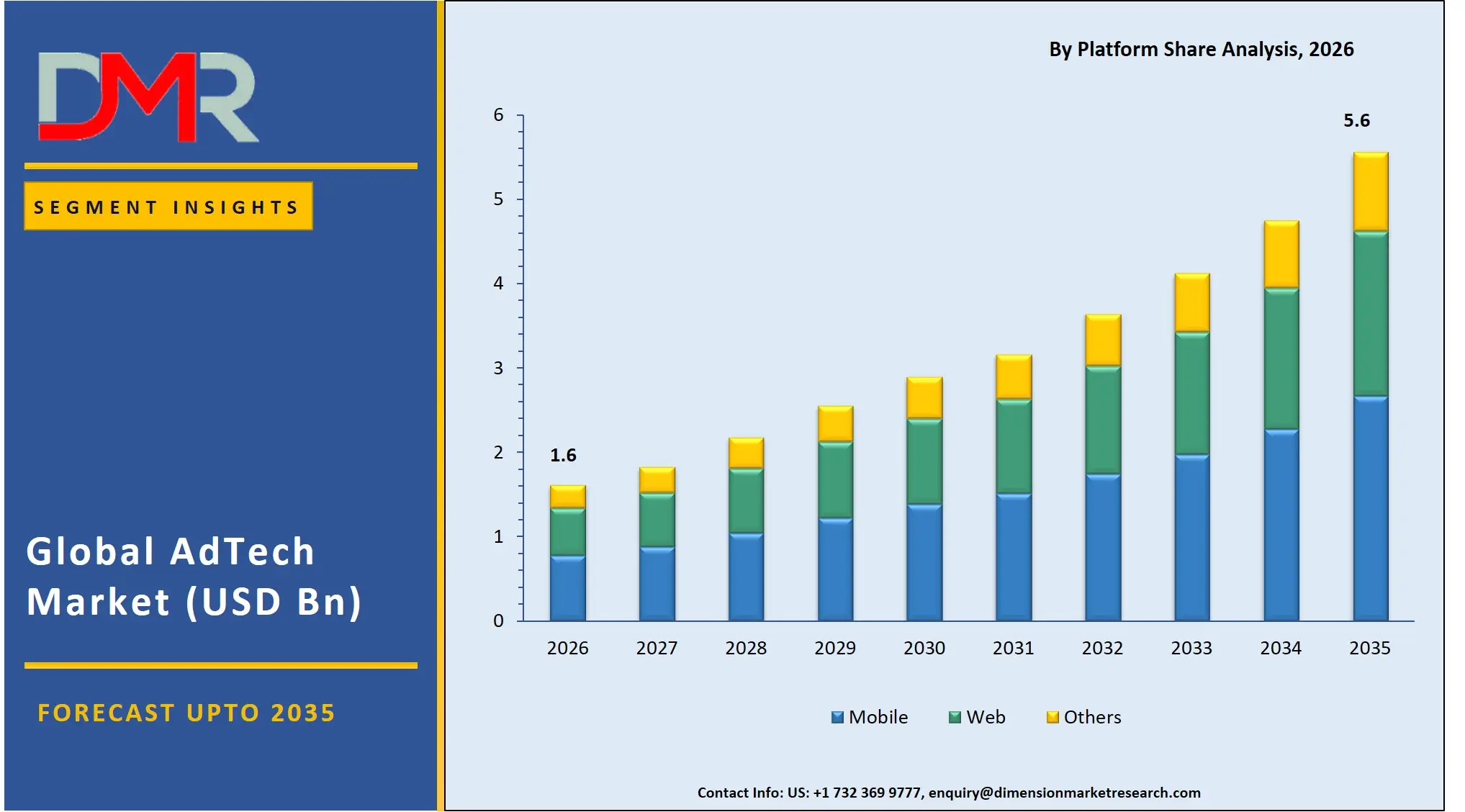

The AdTech Market size is expected to be USD 1.6 billion in 2026 and increase at a compound annual growth rate of 14.7% to USD 5.6 billion in 2035 due to the growing use of renewable energy sources like solar and wind.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The AdTech market includes a broad array of technologies and solutions that are used to deliver optimized digital ads through various channels. Some of the components of this segment include programmatic advertising, data management platforms, ad exchanges, and analytics that enable personal marketing. These technologies play a crucial role in the digital economy, making it easier for companies to become more effective as well as interact with their customers. There have been emerging trends involving the application of artificial intelligence in personalization, privacy-based advertising, and technologies that do not involve cookies.

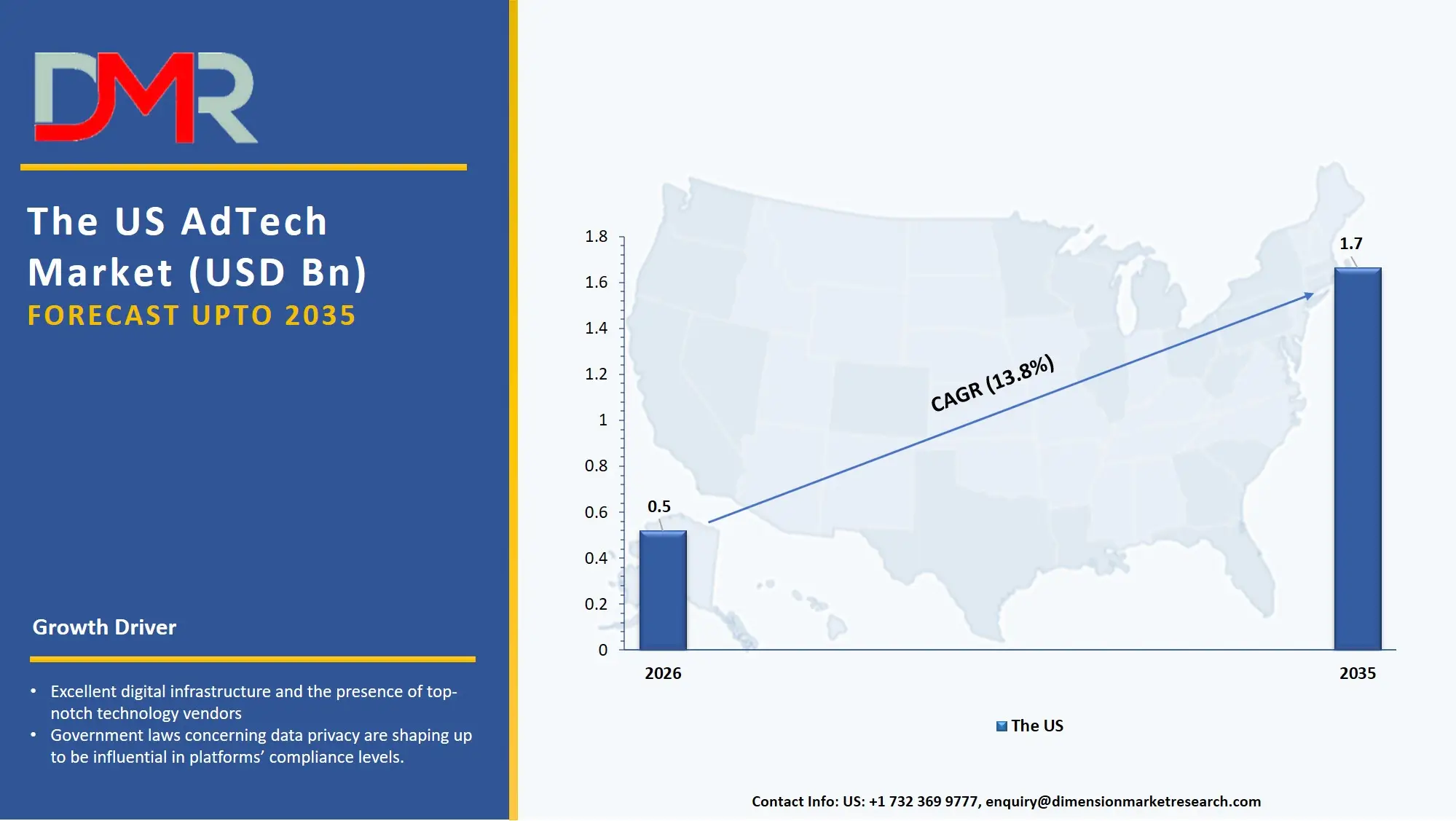

The US AdTech Market

The US AdTech Market size is estimated to be USD 500 million in 2026 and is expected to increase at a CAGR of 13.8% over the forecast period.

AdTech in the US continues to be extremely mature and innovative due to its excellent digital infrastructure and the presence of top-notch technology vendors. Factors driving growth include the widespread use of programmatic advertising, connected television, and data marketing. Regulatory aspects like government laws concerning data privacy are shaping up to be influential in platforms' compliance levels. AI technologies, identity resolution, and cross-channel targeting are priorities for participants in the industry. The high consumption of digital media coupled with significant ad expenditure make the US a powerhouse of AdTech innovation.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Europe AdTech Market

The Europe AdTech Market size is estimated to be USD 400 million in 2026 and at a CAGR of 14.3% over the forecast period.

The AdTech landscape in Europe is highly influenced by strict data privacy laws like GDPR and other activities that align themselves with the European Green Deal. Privacy-centric advertising methods and contextual targeting techniques have become quite common among companies. Programmatic and mobile ads are seeing a surge in demand across Europe, especially in Western Europe. Technological innovations are largely a result of these regulatory issues, which have paved the way for the development of sustainable advertising approaches.

Japan AdTech Market

The market size of Japan AdTech will be USD 80 million in 2026 and at a CAGR of 13.5% in the forecast period.

The AdTech industry in Japan is growing steadily due to heavy internet usage, advanced technology smartphones, and an established digital economy. Programmatic advertising investments and advancements in AI technology have led to the industry's growth trend. Advanced technology and urbanization mean that integration can happen quickly within the advertisement industry. Growth in the industry is being supported by government initiatives on digital transformation. Factors that have influenced adoption trends include the aging demographic and data security concerns. There are a number of opportunities available including mobile-first approach, connected TV technology, and localization of content.

Key Takeaways

- Market Size & Forecast: The AdTech Market size is projected to reach USD 1.6 billion in 2026 and is anticipated to have a value of USD 5.6 billion in 2035.

- Growth Rate & Outlook: The AdTech Market size is set to grow at a compound annual growth rate of 14.7% during the forecast period of 2026 to 2035.

- Primary Growth Drivers: Some of the major growth drivers in the market include Increased Increasing Utilization of Programmatic Advertising, and more.

- Key Market Trends: Some of the major trends in the market are AI & ML Integration in AdTech, and more.

- By Platform: The mobile segment is anticipated to get the majority share of the AdTech market in 2026.

- By Solution: DSP segment is expected to get the largest revenue share in 2026 in the AdTech market.

- By Organization Size: Large Enterprises segment is expected to get the largest revenue share in 2026 in the AdTech market.

- Regional Leadership: North America is set to lead the AdTech market with an estimated 36.9% share in 2026.

What is the AdTech?

AdTech or Advertising Technology can be defined as a collection of tools used by advertisers, advertising firms, and media houses to plan, implement, and analyze their advertising campaigns. The AdTech encompasses different types of tools, including DSP (demand-side platform), SSP (supply-side platform), ad exchange, and DMP (data management platform). In essence, AdTech simplifies the process of buying and selling ad space as well as optimizing marketing campaigns based on the data available. This significance of AdTech becomes apparent through efficient advertising and its optimized profitability.

Use Cases

- Automated Buying & Selling of Ad Inventory: Helps buy and sell advertising space in an automated fashion, thus increasing efficiencies and minimizing errors with the help of real-time data-based decision-making to maximize ROI.

- Targeted Advertising & Personalization: Makes use of advanced analytics and data regarding consumer behavior to show advertisements that are well-targeted and personalized, thus increasing conversion rates.

- Multichannel Campaign Management: Offers the ability to run campaigns across channels such as mobile devices, websites, social media sites, and connected television, among others.

- Performance Analytics for Ads: Allows the monitoring of the success of campaigns by means of performance metrics and analytics.

How AI Is Transforming the AdTech Market

AI has changed the AdTech market in that it can automate campaign management, increase targeting precision, and optimize real-time processes within the system. Algorithms developed through AI technology study large sets of data and discover the preferences, predictions of behavior, and create personalized ads.

Moreover, AI technology helps detect frauds, makes it more efficient to place the ads, and creates dynamic content. Through AI, marketers will be able to make decisions quickly based on the analysis of collected information and reduce operating expenses.

Market Dynamic

Driving Factors in the AdTech Market

Increasing Utilization of Programmatic Advertising

Programmatic advertising represents one of the key factors that stimulate the development of the AdTech industry, allowing for purchasing ads in an automated way via RTB. Thanks to data analytics, the process becomes more cost-effective and targeted. The growing need for customized advertising campaigns brings about increased use of such technology. It helps companies improve their ROI and make advertising more scalable.

Restraints in the AdTech Market

Increased Use of Programmatic Advertising

Programmatic advertising serves as one of the major catalysts for the growth of the AdTech industry since it enables effective and efficient ad purchases using RTB platforms. The use of data analytics allows businesses to cut down on operational expenses while increasing the precision of the ad placements. The growing need for customized ads and quantifiable ad campaigns is contributing to its increased adoption.

Opportunities in the AdTech Market

The Emergence of Cookieless Advertising Solutions

The advent of the end of cookie technology has opened up a window of opportunities for organizations to explore new targeting mechanisms like contextual advertising and leveraging first party data. Organisations that have embraced privacy-first technology stand to benefit from gaining an early mover advantage.

Trends in the AdTech Market

AI & ML Integration in AdTech

With the advancement of AI & ML technology, AdTech has seen new trends that include the implementation of predictive analytics, automatic bidding, and personalized content distribution. This is expected to have a positive impact on the efficiency of campaigns since it reduces the need for human involvement.

Research Scope and Analysis

The AdTech market analysis highlights strong growth across DSPs, programmatic advertising, mobile platforms, and large enterprises, driven by AI integration, data-driven targeting, and digital transformation. Rising adoption of cloud-based solutions, mobile advertising, and first-party data strategies continues to expand market opportunities globally.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Solution Analysis

The demand-side platform (DSP) is predicted to account for about 34.6% of the AdTech market share in 2026, mainly because it can automate advertising transactions and allow for real-time optimizations of campaigns. DSPs provide powerful advertising capabilities, including automated bidding, effective ad placements, and deep analysis, which makes them irreplaceable if the goal is to ensure good returns on investments. The implementation of artificial intelligence and machine learning technologies further improves the effectiveness of such services. By contrast, data management platforms (DMPs) are becoming the fastest-growing part of the AdTech sector, thanks to the growing value of first-party data strategies and the need for precise segmentation. With privacy laws restricting third-party data access, DMPs become highly useful.

By Advertising Type Analysis

The most common kind of advertising in this segment is programmatic advertising which will have a 38.2% share of the total market by 2026 due to its scalability, automation and targeting capabilities. Programmatic advertising enables advertisers to make bids in real time and place ads in a matter that makes it quite popular, as well as use more data analytics and artificial intelligence, which adds to its popularity. Besides, mobile advertising is growing fastest because of growing ownership of smartphones and usage of apps. Content is consumed through mobile phones and thus advertisers should invest there.

By Enterprise Size Analysis

Large enterprises have come to dominate the AdTech market, projected to hold a 62.5% market share in 2026. This is due to their ample financial capabilities and ability to adopt cutting-edge advertising technologies. Large firms deploy a full-scale omnichannel marketing approach, utilizing big data analytics, artificial intelligence, and automation technologies. The importance that large firms place on brand visibility and engagement has further consolidated their dominance in the AdTech market. On the other hand, SMEs will be the fastest-growing AdTech market segment, owing to the adoption of cost-effective and cloud-based AdTech platforms by SMEs.

By Platform Analysis

Mobile will continue to hold the largest share of the market, reaching 47.8% by 2026, owing to the increasing use of smartphones and the growing availability of mobile internet access. With its capabilities in delivering personalized and localized ads, mobile advertising provides high engagement rates and effective campaigns. The trend towards consuming videos and using social media via mobile devices also enhances the dominance of mobile platforms in the AdTech market. Web will continue to experience consistent growth based on its existing market base, while CTV and OTT platforms will be rapidly adopted due to their novel nature.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By End User Analysis

Retail & consumer goods constitutes the major share with an expected value of 29.3% in 2026 owing to huge investments by players in digital marketing solutions to help increase their sales via the internet. These include personalized marketing, promotions, and many other data-driven techniques. Moreover, the expansion of e-commerce platforms has been adding to the need for digital marketing solutions in this segment. On the other hand, the healthcare segment is witnessing a faster pace of growth in the digital marketing solutions market due to the rising rate of digital transformation in this industry.

The AdTech Market Report is segmented on the basis of the following:

By Solution

- DSPs

- SSPs

- Ad Network

- DMPs

- Others

By Advertising Type

- Programmatic Advertising

- Search Advertising

- Display Advertising

- Mobile Advertising

- Email Marketing

- Native Advertising

- Others

By Enterprise Size

By Platform

By End User

- Retail & Consumer Goods

- BFSI

- Media & Entertainment

- IT & Telecom

- Healthcare

- Others

Regional Analysis

Leading Region in the AdTech Market

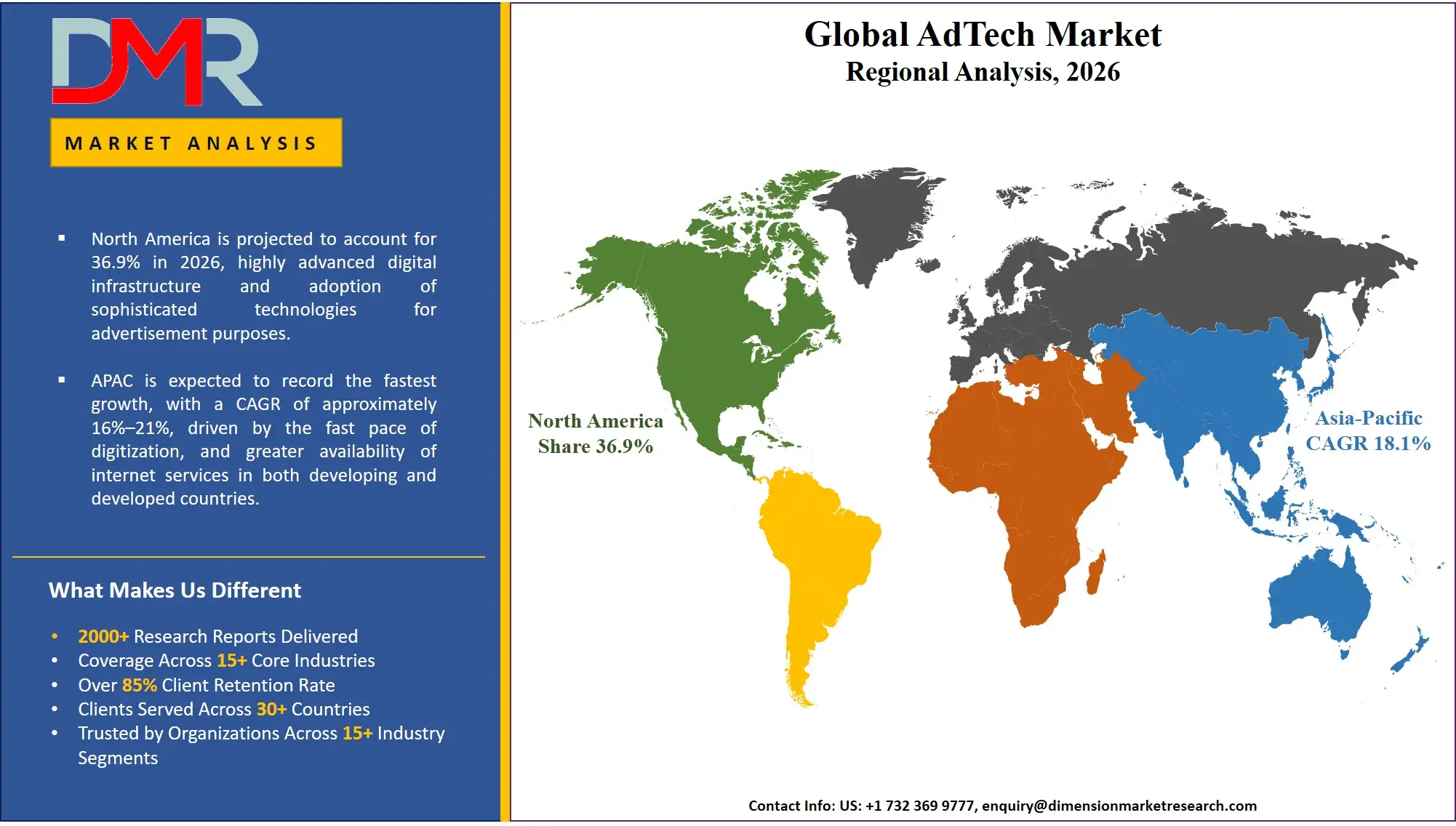

The North American region will lead the AdTech market share with an expected market share of 36.9% in 2026 owing to its highly advanced digital infrastructure and adoption of sophisticated technologies for advertisement purposes. The North American market enjoys several advantages due to its advanced digital ecosystem that includes extensive internet penetration and superior cloud computing infrastructure. Significant investments in the fields of artificial intelligence, programmatic advertising, and big data analysis are another advantage for the North American region. This region has an advanced digital advertising sector coupled with substantial marketing budgets that encourage innovations and developments.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest Growing Region in the AdTech Market

The Asia-Pacific region is projected to lead the way in terms of the most rapidly growing AdTech market owing to the fast pace of digitization, and greater availability of internet services in both developing and developed countries. This region is currently witnessing a rise in the number of users accessing smartphones, cheap internet data plans, and digital media content, resulting in an increase in demand for high-end advertising technology solutions. The emergence of developing nations like India, China, and those in Southeast Asia can be cited as one of the main factors propelling market growth due to their large and digitally savvy populace.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The AdTech industry is one of the most competitive ones with high levels of technology changes and changing consumer needs. Businesses have to innovate to be able to compete effectively, use data analysis, and even integrate artificial intelligence in their operations to win an advantage. It is hard to enter the market because there are many barriers that require special infrastructure and adherence to regulations. Collaboration, acquisitions, and researches are all common ways to enhance the company's position on the market.

Some of the prominent players in the global AdTech are:

- Alphabet Inc.

- Amazon.com, Inc.

- Meta Platforms, Inc.

- The Trade Desk

- AppLovin

- Criteo

- PubMatic

- Magnite

- MediaMath

- Xandr

- Integral Ad Science

- DoubleVerify

- InMobi

- Taboola

- Outbrain

- Lotame

- LiveRamp

- Zeta Global

- AdRoll

- Amobee

- Other Key Players

Recent Developments

- In December 2023: TripleLift & LiveRamp announced the integration of TripleLift Audiences with RampID, providing marketers with large & scalable first-party audience solutions, which ensures privacy-centric lookalike addressability across the open web without depending on traditional identifiers.

- In November 2023: Amazon Ads launched advanced features in campaign planning, activation, and measurement, empowering advertisers with greater audience control & providing faster, actionable insights into ad performance.

- In March 2023: Adobe & professional services firm Accenture partnered to harness the potential of the content supply chain for enterprise marketers, which centers on leveraging Adobe's integrated Content Supply Chain technologies to develop innovative services that allow marketers to efficiently produce & distribute content, that focuses on to enable personalized & scalable customer experiences, improving the value & impact of content for businesses in a collaborative effort between the two companies.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 1.6 Bn |

| Forecast Value (2035) |

USD 5.6 Bn |

| CAGR (2026–2035) |

14.7% |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Solution, By Advertising Type, By Enterprise Size, By Platform, By End User |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the AdTech Market?

▾ The AdTech Market size is expected to reach USD 1.6 billion by 2026 and is projected to reach USD 5.6 billion by the end of 2035.

Which region held the largest share of the AdTech Market in 2026?

▾ North America is set to lead the AdTech market with an estimated 36.9% share in 2026.

Who are the key players in the AdTech Market?

▾ Some of the key players in the AdTech Market include Amazon, Meta, Alphabet and more.

What is the CAGR of the AdTech Market from 2026 to 2035?

▾ The market is growing at a CAGR of 14.7 percent over the forecasted period.

What factors are driving the growth of the AdTech Market?

▾ Increasing Utilization of Programmatic Advertising, and more are the factors driving the growth of the AdTech Market.

What are the major trends in the AdTech Market?

▾ AI & ML Integration in AdTech, and more are some of the major trends in the market.

How is the AdTech Market segmented?

▾ The AdTech Market is segmented by solution, advertising type, enterprise size, platform, end user.

Which region is expected to grow the fastest in the AdTech Market?

▾ Asia Pacific is the fastest-growing region in the AdTech market during the forecast period