What is the AI Sovereignty Infrastructure Market Size?

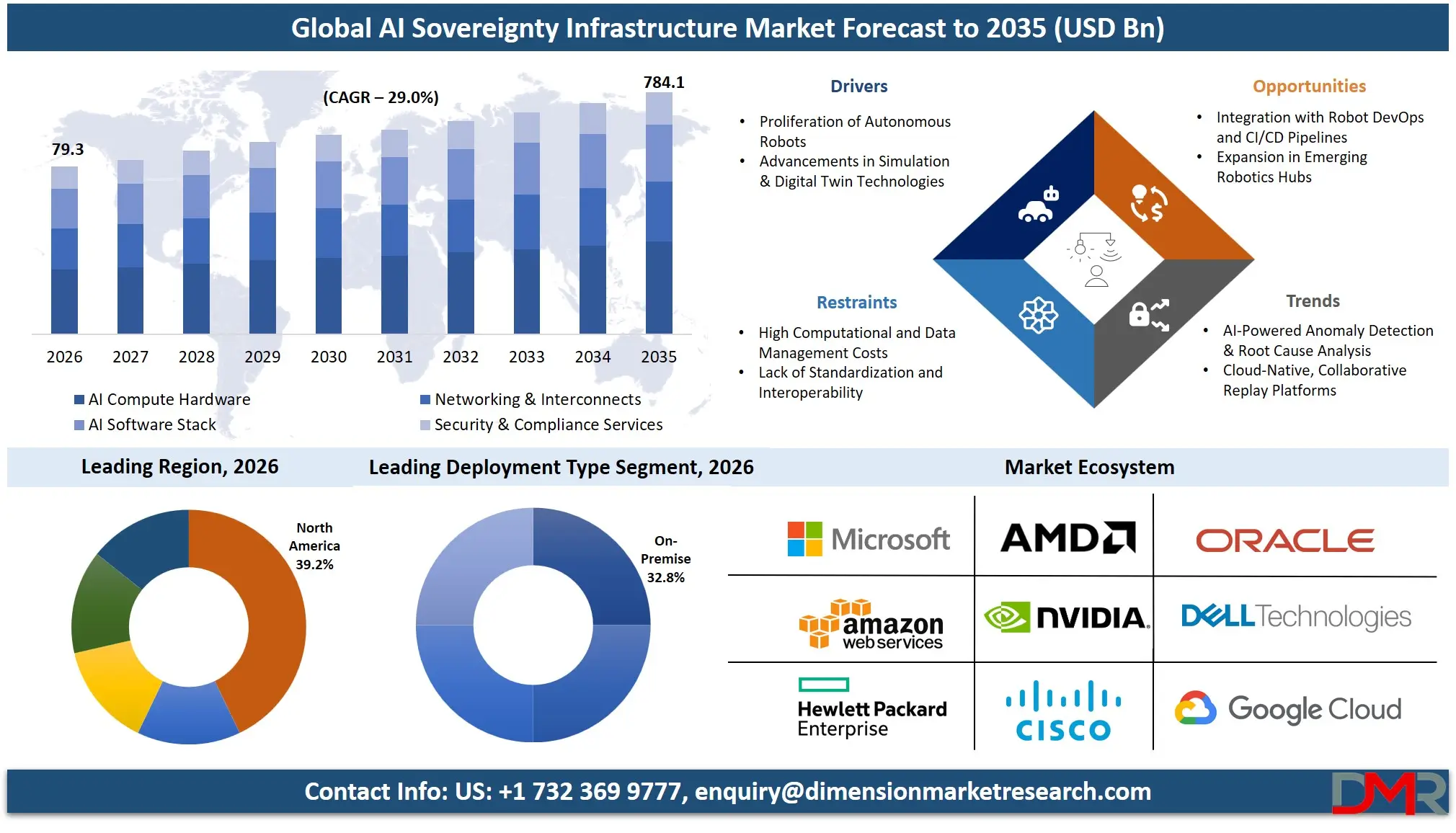

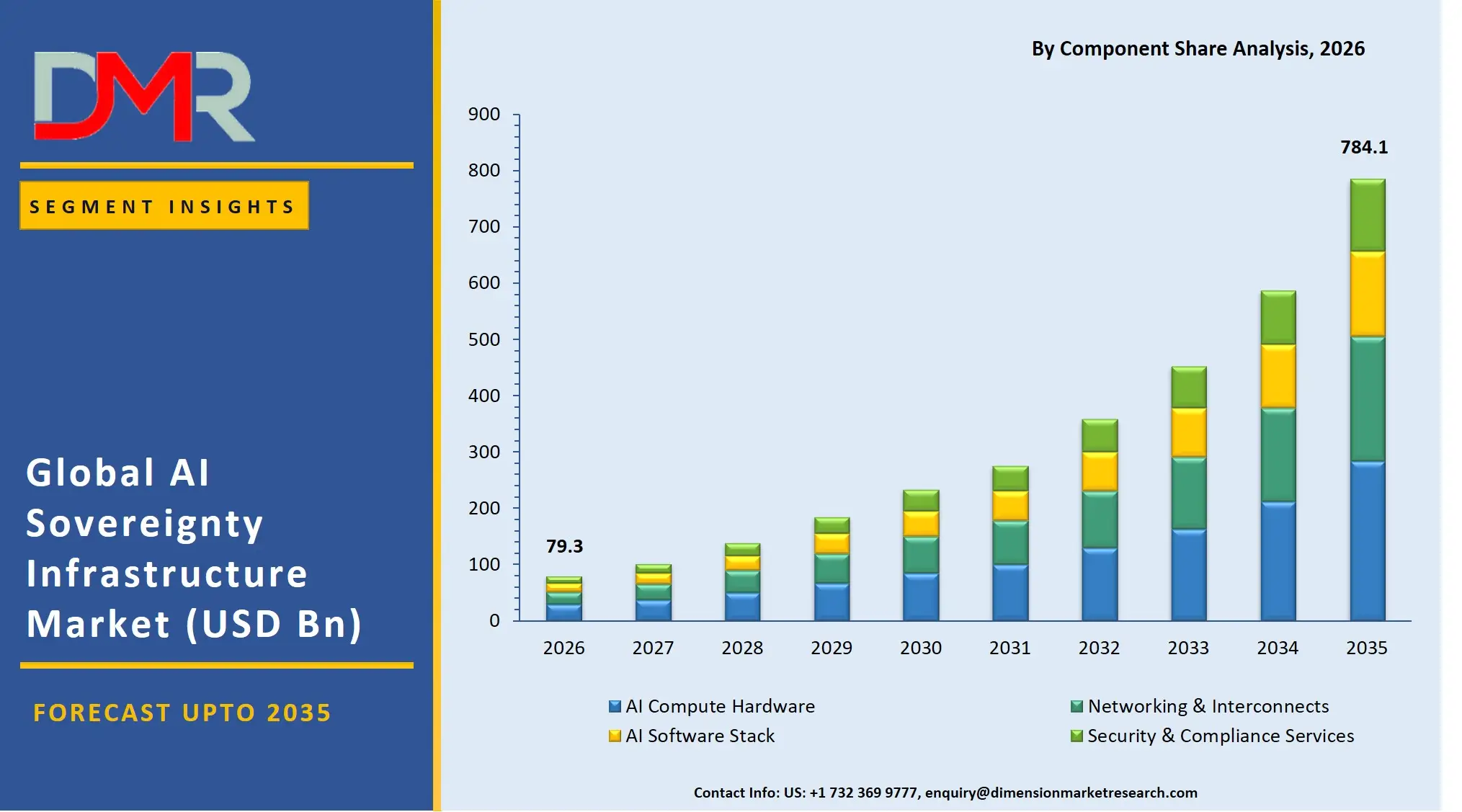

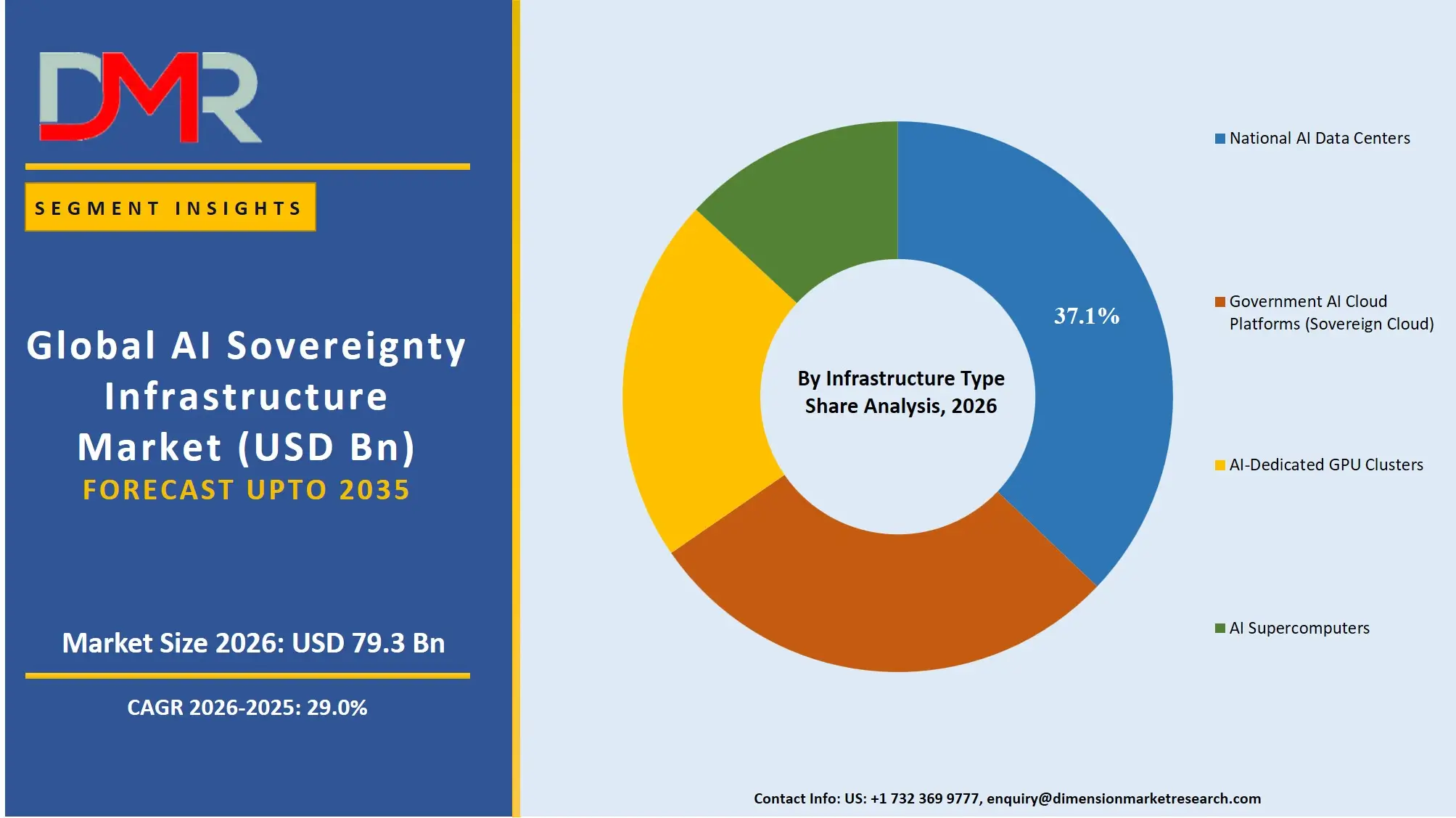

The Global AI Sovereignty Infrastructure Market is expected to reach a value of USD 79.3 billion in 2026, and it is further anticipated to reach USD 784.1 billion by 2035, growing at a CAGR of 29.0% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The AI sovereignty infrastructure market is expanding at an exponential rate as countries and organizations prioritize protecting and nurturing local AI development and digital sovereignty. The market includes specialized hardware, sovereign cloud platforms, AI software stacks, and security services enabling governments and regulated industries to develop, train, and deploy AI models within their jurisdictional boundaries.

As the need for data protection, building national large language models (LLMs), and de-risking reliance on foreign hyperscalers continues to rise, it has created a need for AI infrastructure dedicated to sovereignty. The main adopters are government organizations and defense & intelligence agencies, while on-premises and sovereign cloud deployment models are still the most important for ensuring data localizations and physical control. The BFSI and healthcare, and critical infrastructure, are significant participants in this space because they need secure, compliant and highly available AI compute environments to process citizen information and enable national security applications.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

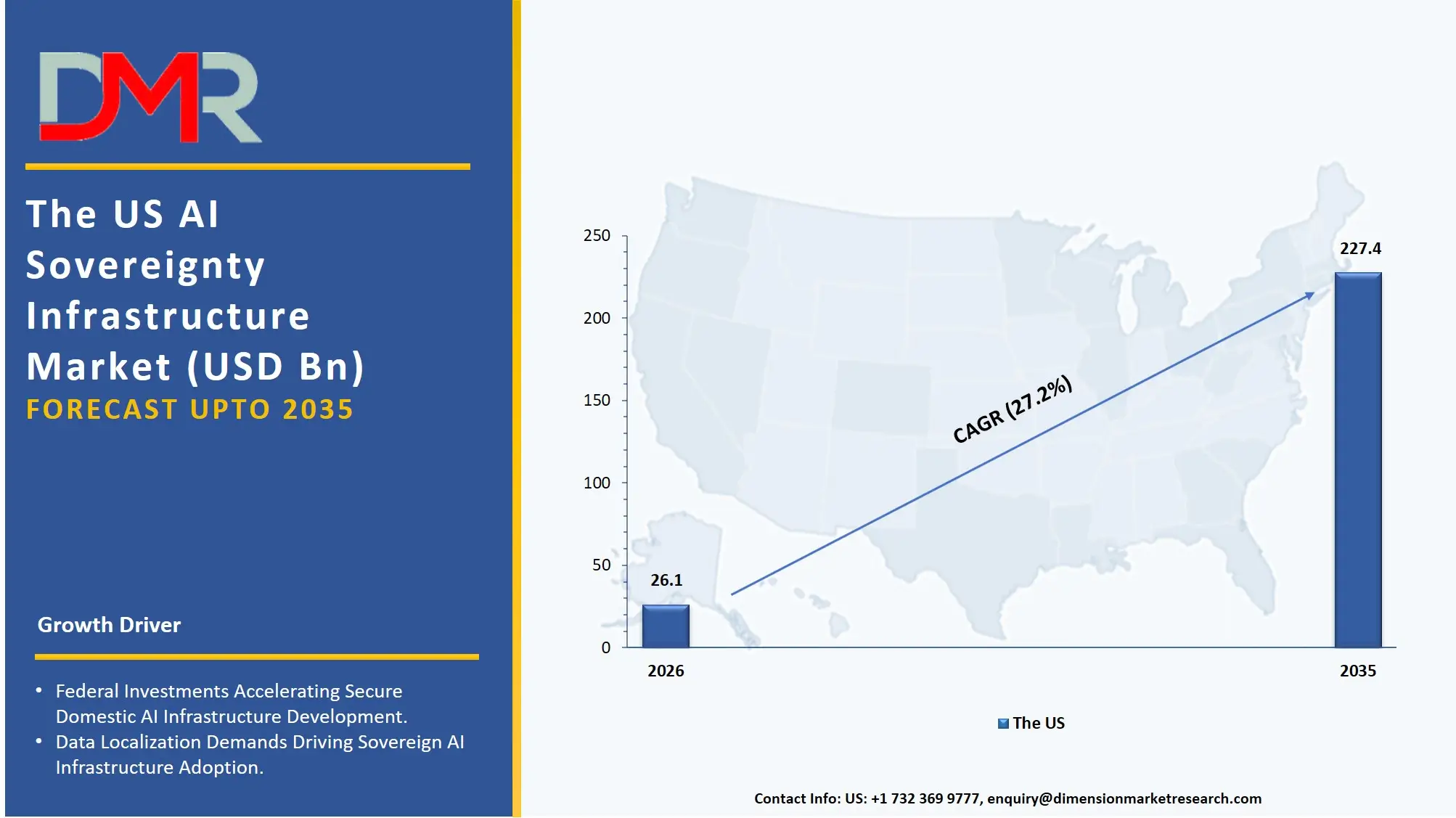

The US AI Sovereignty Infrastructure Market

The US AI Sovereignty Infrastructure Market is expected to grow at a compound annual growth rate of 27.2% to USD 227.4 billion by 2035, growing from a value of USD 26.1 billion in 2026.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US continues to be the biggest and most technologically advanced market for sovereign AI infrastructure, with military agencies investing heavily in their own AI initiatives and intelligence service's rapidly growing classified GPU clusters. The market is represented by AI Compute Hardware, which is primarily high-demand advanced GPUs and processors made under the strict control of national security supply chain. Moreover, the use of Generative AI tools in classified government workflows is creating a similar requirement in Security & Compliance Services to regulate data governance and AI ethics on sovereign cloud platforms.

The Europe AI Sovereignty Infrastructure Market

The Europe AI Sovereignty Infrastructure Market is estimated to be valued at USD 25.8 billion in 2026 and is further anticipated to reach USD 248.1 billion by 2035 at a CAGR of 28.6%. European market is impacted by regulatory frameworks such as GDPR and the groundbreaking EU Artificial Intelligence Act, and this has led to a need for Government AI Cloud Platforms and sovereign cloud solutions. Accelerated growth is also being experienced by Hybrid Sovereign Infrastructure in the region as manufacturing and automotive industries in Germany and France seek to keep up with the balance between operational technology (OT) security and AI-driven analytics that is taking place on localized cloud infrastructure. Furthermore, projects like GAIA-X require the infrastructure providers to develop National AI Data Centers dedicated to supporting data residency and interoperability across the European AI landscape.

The Japan AI Sovereignty Infrastructure Market

The Japan AI Sovereignty Infrastructure Market is projected to be valued at USD 8.8 billion in 2026. It is further expected to witness robust growth, holding USD 83.0 billion in 2035 at a CAGR of 28.4%. he situation in Japan is special, given the national drive to cultivate AI autonomy due to shrinking manpower and the desire to secure high-level industrial technology. A significant portion of the spending is going to the National AI Platforms and secure data processing infrastructure, as big conglomerates and public sector organizations shift their most sensitive workloads away from foreign public clouds and towards sovereign AI ecosystems. There is a strong need for deeply localized Computing Hardware and AI Software Stacks to span the gap between legacy electronic medical record (EMR) systems and next generation AI analytics, which will give rise to specialized MLOps and governance tools.

Key Takeaways

- Market Size & Forecast: The Global AI Sovereignty Infrastructure market is projected to reach USD 79.3 billion in 2026, expanding dramatically to USD 784.1 billion by 2035, driven by the compelling need for national security and localization mandates for sensitive AI workloads.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 29.0%, driven by the compelling need for national security and localization mandates for sensitive AI workloads.

- Primary Growth Drivers: Key factors driving growth include the broad adoption of dependency-free cloud migration, reliance on Sovereign Cloud platforms, the lack of compute supply chain vulnerabilities, and the growing need for MLOps platforms that demand specialized AI Software Stack skills.

- Key Market Trends: The key market trends are AI-powered monitoring tools in Security & Compliance Services for auto-remediation of policy violations and the adoption of sovereign AI platforms for industry-specific applications, with national security boards placing greater emphasis on AI data sovereignty and the rise of sovereign Governance frameworks.

- By Component Analysis: The component segment is projected to be led by AI Compute Hardware, which is anticipated to see a surge in investments in sovereign AI processing, GPUs clusters, and high-performance computing architecture. The growth of secure AI software, networking solutions and compliance services adds to the acceleration of sovereign AI ecosystems around the world.

- By Infrastructure Type: The national AI Data Centers are expected to lead the infrastructure type segment with growing investments by the government in secure local AI ecosystems. This increase in demand for sovereign cloud deployments, AI supercomputers, cybersecurity, and regulation compliant infrastructure is fueling adoption of nationally controlled AI facilities around the world.

- By Deployment Model: Sovereign Cloud (Localized Managed Cloud) is likely to be the biggest winner in the deployment model category, with increasing demand for secure, scalable, and regulation-compliant AI infrastructure. Sovereign cloud deployment continues to grow within governments and regulated industries and is fueled by growing cybersecurity concerns.

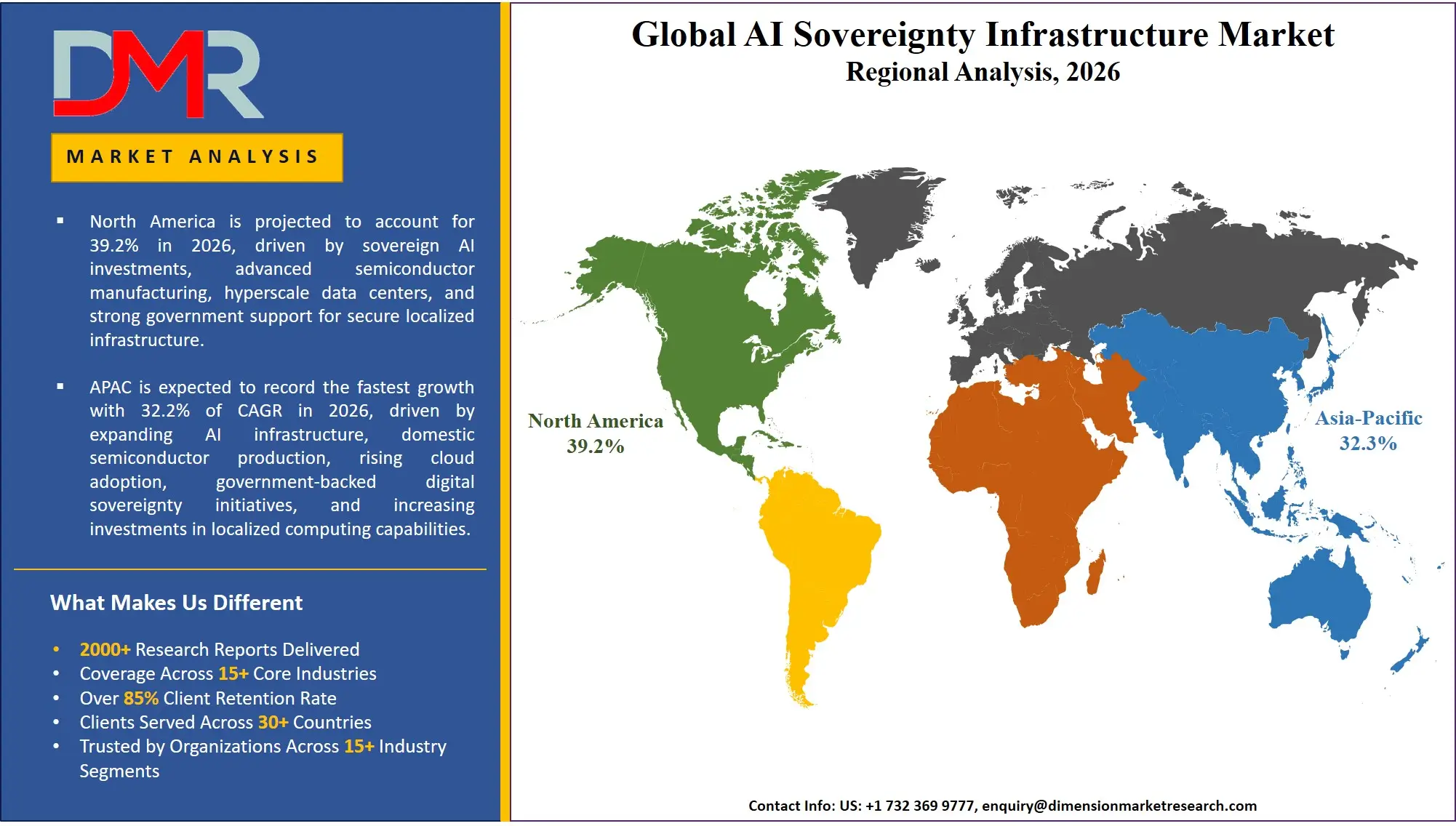

- Regional Leadership: North America is poised to dominate this market with 39.2% of the market share in 2026 due to its well-developed defense technology ecosystem that utilizes this infrastructure to its fullest and makes it a leader in this market.

What is the AI Sovereignty Infrastructure?

AI Sovereignty Infrastructure is the specific hardware, software, and security measures that are purchased by countries and regulated entities to ensure that the development and deployment of AI is fully within their jurisdiction and territory. These technologies are not the typical "cloud AI consumption" technologies, but they are connected to the "where" and the "who" of AI development. The AI Compute Hardware includes GPUs and processors that serve purpose of model training and are managed by AI Software Stacks such as MLOps, orchestration, AI middleware, etc. and are not dependent on third parties. The Security & Compliance Services encompass data localization, data governance and continuous monitoring. 90% of countries are interested in achieving AI self-sufficiency, while 80% of businesses are dedicated to realize absolute data governance, secure supply chains, and strategic autonomy, and thus make investments in AI a key driver of national resilience, rather than technical dependency.

Use Cases

- Classified Defense Intelligence Processing: Defense & Intelligence Agencies buy AI-Dedicated GPU clusters and protect data processing & storage infrastructure to ensure the training of LLMs is conducted on top-secret intelligence data, all within an air-gapped, government-controlled environment, for the purposes of national security analysis.

- Sovereign Genomic Research in Healthcare: National health services employ security & compliance services and sovereign cloud to process petabytes of citizen genomic data, which allows them to comply with local data localization regulations and train AI diagnostic models within the country's borders.

- National Financial Crime Prediction: A central bank deploys a Hybrid Sovereign Infrastructure to run AI Model Training workloads for fraud detection on sensitive financial transactions on-premises, while using a localized Sovereign Cloud for burst capacity and Inference & Edge AI Deployment, maintaining central control under financial sovereignty regulations.

- Critical National Infrastructure Protection: A central bank implements a Hybrid Sovereign Infrastructure to execute AI Model Training workloads for financial fraud detection on critical financial transactions on-premises, and a localized Sovereign Cloud to support burst capacity and Inference & Edge AI Deployment, keeping central control within financial sovereignty regulations.

Market Dynamics

Key Drivers in the Global AI Sovereignty Infrastructure Market

The Geopolitical Imperative for Digital Independence

Countries around the world are facing an existential threat from reliance on outside technology stacks to control their intelligence, national security, and welfare of their citizens. The national security implications of the strategic capacity to build AI are now becoming direct, and more than open markets can sustainably supply safe solutions. This is driving a change in paradigm whereby national governments directly invest and regulate national AI data centers and sovereign cloud services rather than relying on commercial hyperscalers. Such investments in infrastructure support crucial functions, such as handling Top-Secret data, training indigenous LLMs, and cyber defense. The ability to develop these sovereign capabilities enables countries to have strategic autonomy and reduce the threat of foreign surveillance or supply chain disruption.

Complexity of Multi-Layer Secure AI Architectures

By their nature, sovereign AI systems can be massive and extend across air-gapped on-premises supercomputers, on-premises managed clouds, and secure edge nodes. Having to manage identity management, data lineage, memory encryption, and security compliance across these different areas with a myriad of sovereign trusted standards is an enormous challenge. Without dedicated integration, this complexity can result in security breaches, data sovereignty issues, and suboptimal resource utilization. Therefore, the demand for End-to-End Security & Compliance Services and Dedicated AI Software Stacks that can orchestrate and monitor these highly secure and heterogeneous environments is growing.

Restraints in the Global AI Sovereignty Infrastructure Market

Inertia of Legacy Bureaucratic & IT Infrastructure

A considerable barrier to modernization is the reliance on legacy systems by most government and defense organizations, which have become a central part of critical workflows. However, the act of moving sensitive data and applications from old, legacy mainframes and unconnected data silos to modern National AI Data Centers is too costly and risky. When migrating data to petabyte scale classified archives, it is essential the process is well planned and securely hardened. During the transition, organizations are concerned about catastrophic data leaks, operational paralysis, cross-jurisdictional contamination, etc. As a result, the deployment of sovereign AI infrastructure is slowed down, leading to institutional and technical debt.

Export Controls and Supply Chain Bottlenecks

The very hardware that enables AI sovereignty, primarily advanced GPUs and high-speed interconnects, is subject to intense geopolitical export controls and manufacturing supply chain bottlenecks. This creates a structural constraint where national ambitions for AI independence are throttled by the limited physical availability of cutting-edge components. Even when funding is secured, governments face multi-year lead times for AI-Dedicated GPU Clusters, creating a direct barrier to market growth and delaying strategic programs in AI Model Training for defense and national security.

Growth Opportunities in the Global AI Sovereignty Infrastructure Market

Building National-Level AI Supercomputing Fabrics

One of the most significant growth opportunities lies in assisting nations to design and deploy the entire stack for National AI Data Centers and AI Supercomputers. Most countries want to put massively parallel GPUs, high-speed Infiniband interconnects, and a secure software stack in a functional system for classified workloads but don't have the architectural expertise to do so. This includes advanced expertise of secure data processing & storage, integration of liquid-cooled hardware, and government-grade orchestration middleware.

Verticalized Sovereign AI for Critical Infrastructure

Energy, telecom, and healthcare are areas seeing growth as they face the challenge of the integration of domain-specific operational technology and sovereign AI. The conditions are by no means standard IT environments, but ones where Cyber-Physical AI systems must be able to process real-time sensor data in environments with strict national security requirements. For energy grid operators, threat detection AI is a real-time need, and for healthcare systems, AI to analyze the genome on local data is a requirement. They need implementation partners who understand and are equipped with AI, OT network security and national compliance frameworks. To add value, the infrastructure provider needs to construct hybrid architectures that enable the deployment of edge AI and provide an integrated sovereign cloud backbone.

Trends in the Global AI Sovereignty Infrastructure Market

The Rise of Sovereign MLOps Platforms

As governments realize that the model lifecycle (from ingestion to inference) is just as important as owning the hardware, Sovereign MLOps emerges as a new category. Countries are building internal platforms to offer local scientists trusted and verified toolchains, thus avoiding opaque foreign AI services. Such platforms allow for secure deployment, for model explainability, and for national law compliance audit. Beyond the open-source toolkits, vendors are now offering expertise on how to create government-grade MLOps, with their own layers of orchestration for classified data as well as vendor-locked compute fabrics.

Green Energy Mandate for Sovereign AI

As AI Supercomputers use megawatts of energy, environmental sustainability is becoming a national security and political constraint on sovereign AI expansion. Now countries are being pushed to find a way to secure a route to AI independence that is compatible with climate and grid security. This has brought about the need for green-by-design sovereign data center consulting services. Solution architects are supporting governments to plan National AI Data Centers co-located with dedicated nuclear or renewables energy source, design energy-efficient liquid cooling for GPU clusters and right-size compute resource allocation to optimise the sovereign AI fabric carbon footprint while maintaining strategic performance.

Research Scope and Analysis

The Global AI Sovereignty Infrastructure Market is witnessing strong growth driven by rising investments in sovereign AI data centers, AI compute hardware, secure cloud environments, and localized AI model training. Governments, defense sectors, and enterprises are prioritizing data sovereignty, cybersecurity, regulatory compliance, and scalable AI infrastructure to support national digital transformation initiatives.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Component Analysis

AI Compute Hardware is projected to lead the component share of the Global AI Sovereignty Infrastructure Market as AI may clean up the processing power segment with the increasing demand for sovereign AI processing power, high-performance computing environment, and localized AI training infrastructure. As governments and enterprises continue to invest more and more in domestic AI supercomputing clusters and sovereign cloud ecosystems, the revenue share of GPUs and advanced AI processors is the highest. High-speed Ethernet and InfiniBand networking technologies also are key to enabling low latency AI workloads and training large language models. Further, AI software tiers, such as orchestration and MLOps platforms, are also seeing a significant uptake for AI secure operations management. With the increasing focus on data localization, governance, and monitoring in national AI sovereignty policies, security and compliance services are emerging as significant market trends.

By Infrastructure Type Analysis

National AI Data Centers are projected to dominate the infrastructure type segment owing to increasing investments by governments and hyperscale technology providers in secure, sovereign AI ecosystems. Nations around the globe are prioritizing AI infrastructure that is local to them, as a way to minimize reliance on foreign cloud vendors and to achieve strategic management of sensitive data and AI workloads. These will enable the development of AI models, national digital transformation programs and sovereign clouds deployment. Additionally, AI dedicated GPU clusters and AI supercomputers are also trending rapidly, partly because of the growing number of large language model developments and high-performance computing needs. The public sector is rapidly moving towards the adoption of government AI cloud platforms as it looks to provide cloud services that are local, compliant with regulations, and suitable for its specific needs. The pervasive concerns over cybersecurity, geopolitical threats, and digital sovereignty further underscore the need for a national approach to AI infrastructure.

By Deployment Model Analysis

The rising demand for secure, compliant, and scalable AI infrastructure in government agencies and regulated sectors is likely to fuel the deployment model segment's growth, with a primary focus on Localized Managed Cloud (Sovereign Cloud) expected to gain prominence. Cloud sovereignty is becoming more prevalent among organizations seeking to preserve data residency, regulatory compliance, and control while enjoying scalability and enhanced AI features.As organizations need to preserve data residency, regulatory compliance, and operational control, they're increasingly taking advantage of cloud sovereignty to enjoy scalability and advanced AI capabilities. Moreover, hybrid sovereign infrastructure models are also seeing significant growth, as businesses prioritize flexibility and performance optimization by integrating on-premises systems with sovereign cloud environments. Fully sovereign on-premises deployments are still essential for defense, intelligence applications and other workloads that are highly sensitive and demand maximum control and isolation. Sovereign deployment models are accelerating worldwide as the use of AI applications ramps up, cybersecurity issues grow, and government regulations back domestic digital infrastructure.

By Application Analysis

AI Model Training (LLMs, HPC Workloads) is predicted to be the biggest application category, driven by the growth of generative AI technologies and large language models. Sovereign AI compute environments are attracting significant investment from governments, research institutions and enterprises to aid secure AI training and to minimize dependence on foreign infrastructure companies. Growth in data governance concerns, cybersecurity and data privacy are driving a significant market share for secure data processing and storage applications. Governments are increasingly turning to AI-supported citizen services and digital transformation projects, driving high adoption across national AI platforms and public services.Governments are seeing high adoption rates on national AI platforms and public services, with the implementation of AI-driven citizen services and digital transformation projects. The deployment of inference and edge AI is accelerating in both industrial and defense applications, with cybersecurity and intelligence systems being vital for national security and threat detection.

By End User

The end-user segment is expected to be dominated by Government & Defense, as significant investments are being made in sovereign AI infrastructure for national security, intelligence, and critical applications in public sector. Governments are focusing on creating local AI clusters to ensure strategic autonomy, protection of sensitive data, and enhanced cybersecurity resilience. Sovereign AI infrastructure is now being quickly embraced by BFSI organizations as they strive to meet financial regulations and improve their ability to detect fraud, manage risk, and process data securely. The healthcare and life sciences industry is seeing a rise in the use of AI for diagnostics, precision medicine, and secure patient data management. Energy and telecoms companies are investing in sovereign platforms to support their operational security and infrastructure resilience. Sovereign AI environments are also being widely adopted by research institutions and commercial organizations as tools for fostering innovation and scalable AI operations.

The Global AI Sovereignty Infrastructure Market Report is segmented on the basis of the following:

By Component

- AI Compute Hardware

- GPUs

- Processors

- Storage Systems

- Memory

- Networking & Interconnects

- High-Speed Ethernet

- Infiniband

- AI Software Stack

- MLOps

- Orchestration

- Middleware Platforms

- Security & Compliance Services

- Data Localization

- Governance

- Monitoring Tools

By Infrastructure Type

- National AI Data Centers

- Government AI Cloud Platforms (Sovereign Cloud)

- AI-Dedicated GPU Clusters

- AI Supercomputers

By Deployment Model

- On-Premises

- Sovereign Cloud

- Hybrid Sovereign Infrastructure

By Application

- Secure Data Processing & Storage

- AI Model Training (LLMs, HPC workloads)

- Inference & Edge AI Deployment

- National AI Platforms & Public Services

- Cybersecurity & Intelligence Systems

By End User

- Government & Defense

- BFSI (Banking, Financial Services, Insurance)

- Healthcare & Life Sciences

- Critical Infrastructure (Energy, Telecom)

- Research & Academia

- Commercial Enterprises

Regional Analysis

Leading Region by Market Share

North America is poised to dominate the global AI sovereignty infrastructure market, as it is projected to hold 39.2% of the market share by the end of 2026. The United States, which dominates North America, has the highest share in the AI sovereignty infrastructure market because of an unmatched concentration of classified AI supercomputing facilities within Department of Energy and Department of Defense programs and the aggressive AI modernization agendas of its intelligence agencies. The region has an established ecosystem of defense prime contractors, specialized security-cleared system integrators, and a rich pool of talent with top-secret AI engineering credentials.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Regional Market

Asia-Pacific is expected to be the most rapidly expanding AI sovereignty infrastructure market, driven by sweeping, state-led national AI strategies in India, China, Japan, and Southeast Asia. The fast-paced economic growth, a rising digital citizenry, and the dynamic expansion of the digital economy are compelling established conglomerates and state agencies to discard reliance on Western hyperscalers. National AI Platforms & Public Services and domestic LLM training are in high demand, requiring massive state investment in National AI Data Centers to head in the direction of fully sovereign AI operating models.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive environment of the global AI sovereignty infrastructure market has become highly bifurcated with a heterogeneous array of defense prime contractors, specialized sovereign cloud providers, niche high-performance computing (HPC) integrators, and the professional service divisions of the large commercial GPU and networking vendors. The key to success will be profound strategic alliances with government science agencies and defense procurement bodies, as they will open the necessary co-selling opportunities and early access to the requirements for next-generation exascale platforms. The movement towards market consolidation is rapidly progressing with traditional defense IT companies acquiring specialized MLOps and middleware security boutiques to provide a fully integrated, secure AI stack.

Some of the prominent players in the Global AI Sovereignty Infrastructure Market are:

- NVIDIA

- Microsoft

- Amazon Web Services (AWS)

- Google Cloud

- Oracle

- IBM

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- Cisco Systems

- Intel

- Advanced Micro Devices (AMD)

- Lenovo

- Huawei Technologies

- CoreWeave

- Equinix

- Digital Realty

- Atos Eviden

- Alibaba Cloud

- SK Telecom

- Fujitsu

- Other Key Players

Recent Developments

- January 2026: NVIDIA announced it will make a major expansion of its sovereign AI program, a joint venture to assist nations in the Middle East and Asia to create proprietary LLMs through locally built AI-Dedicated GPU Clusters and expertise in AI Compute Hardware and Networking & Interconnects.

- November 2025: Palantir Technologies deepened its collaboration with a consortium of European defense agencies, launching a dedicated practice in Security & Compliance Services and Data Localization to support intelligence agencies in migrating classified workloads to a new sovereign cloud, maintaining compliance with strict EU data jurisdiction laws.

- October 2025: HPE acquired a boutique European HPC security firm to further its Government AI Cloud Platform and secure MLOps solutions for Sovereign Cloud facilities, to support the complicated requirements of Government & Defense customers in data residency and tactical edge AI deployment.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 79.3 Bn |

| Forecast Value (2035) |

USD 784.1 Bn |

| CAGR (2026–2035) |

29.0% |

| The US Market Size (2026) |

USD 26.1 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Component, By Infrastructure Type, By Deployment Model, By Application, and By End User |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global AI Sovereignty Infrastructure Market?

▾ The Global AI Sovereignty Infrastructure market is poised to be valued at USD 79.3 billion in 2026 and is projected to reach USD 784.1 billion by 2035, driven by the universal need for specialized, secure infrastructure for national AI model training, classified data processing, and achieving digital independence.

What is the CAGR of the Global AI Sovereignty Infrastructure Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 29.0% from 2026 to 2035, reflecting the accelerating geopolitical imperative for AI self-sufficiency and the persistent shortage of trusted, sovereign-controlled computing fabrics.

What factors are driving the growth of the Global AI Sovereignty Infrastructure Market?

▾ Key drivers include the geopolitical imperative for digital independence, the modernization of legacy classified IT systems, the complexity of managing multi-layer secure AI architectures, and the surge in demand for Data Localization amid evolving national security and data sovereignty laws.

Which region held the largest share of the AI Sovereignty Infrastructure Market in 2026?

▾ North America, specifically the United States, is projected to hold 39.2% of the market share in 2026, driven by a mature defense industrial base and aggressive federal investment in National AI Data Centers and AI Supercomputers for strategic applications.

Which region is expected to grow the fastest in the AI Sovereignty Infrastructure Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid state-led AI strategies in India, China, and Japan, where National AI Platforms & Public Services are critical for transitioning from foreign dependency to sovereign AI operations.

What are the major trends in the Global AI Sovereignty Infrastructure Market?

▾ Major trends include the integration of classified Generative AI into intelligence workflows, the rise of Sovereign MLOps platforms, the mandate for green energy to power AI Supercomputers, and the focus on hardware-level security for multi-tenant, multi-classification data fabrics.

Who are the key players in the Global AI Sovereignty Infrastructure Market?

▾ Key players include hardware leaders like NVIDIA, Intel, and HPE; defense software integrators like Palantir; sovereign cloud service divisions of Microsoft, AWS, and Google; and specialized national champions like Thales, Atos, Fujitsu, and Huawei.

How is the Global AI Sovereignty Infrastructure Market segmented?

▾ The market is segmented by Component, Infrastructure Type, Deployment Model, Application, and End User.