Market Snapshot

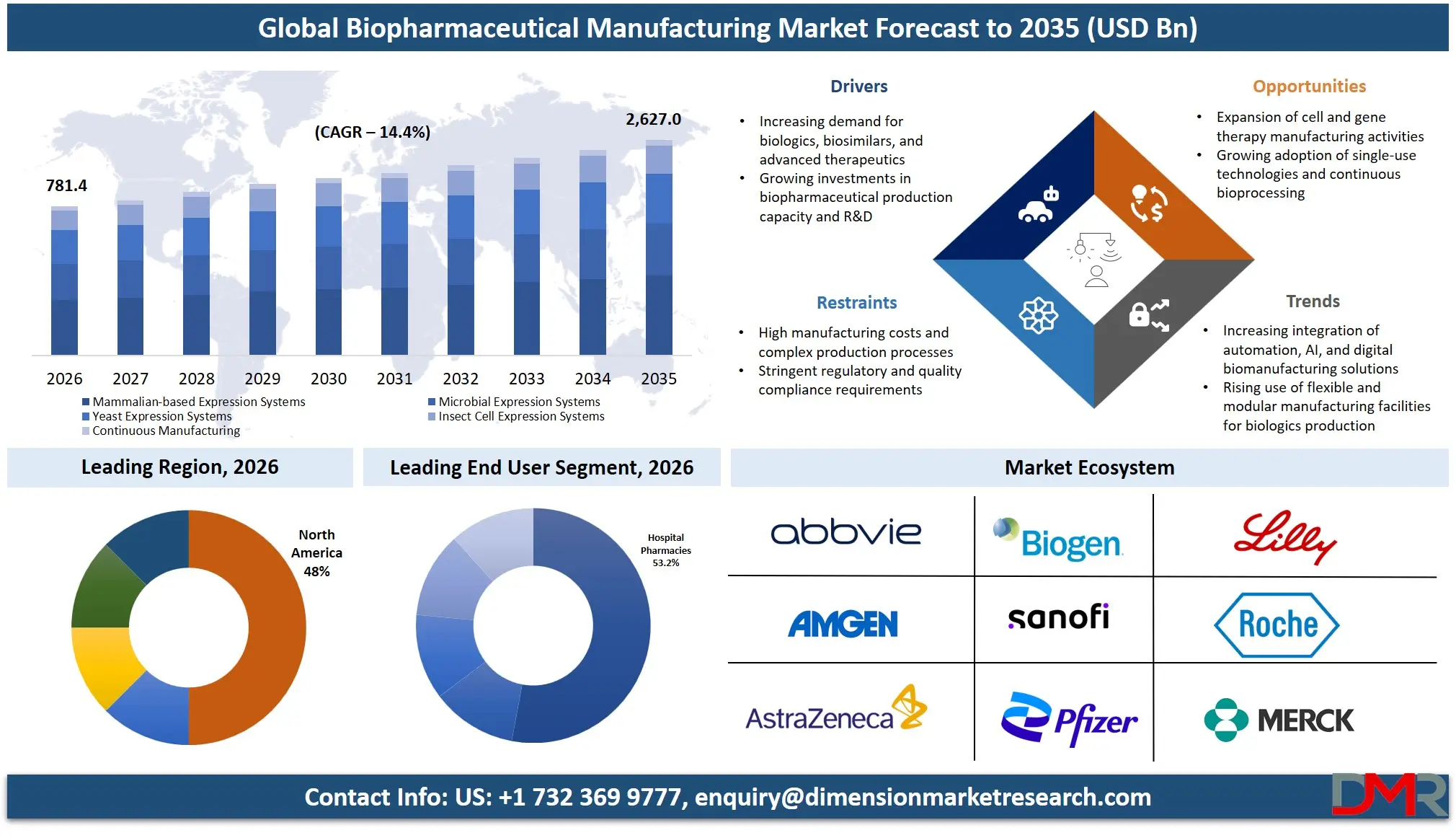

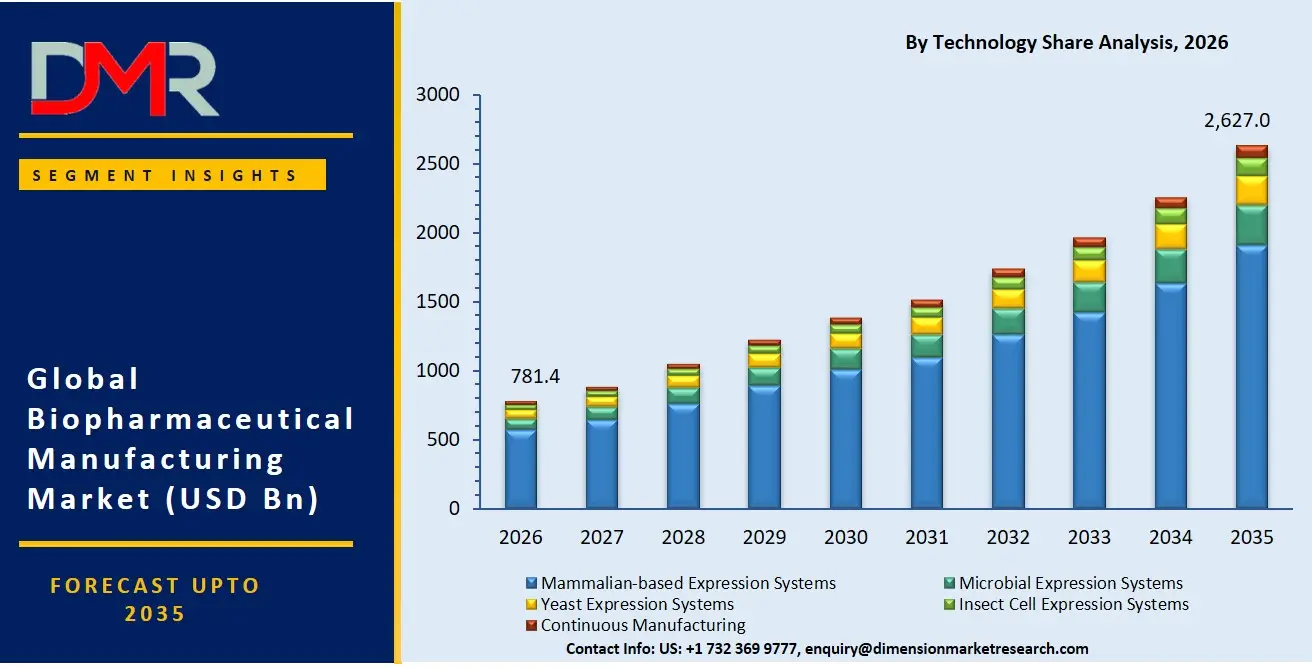

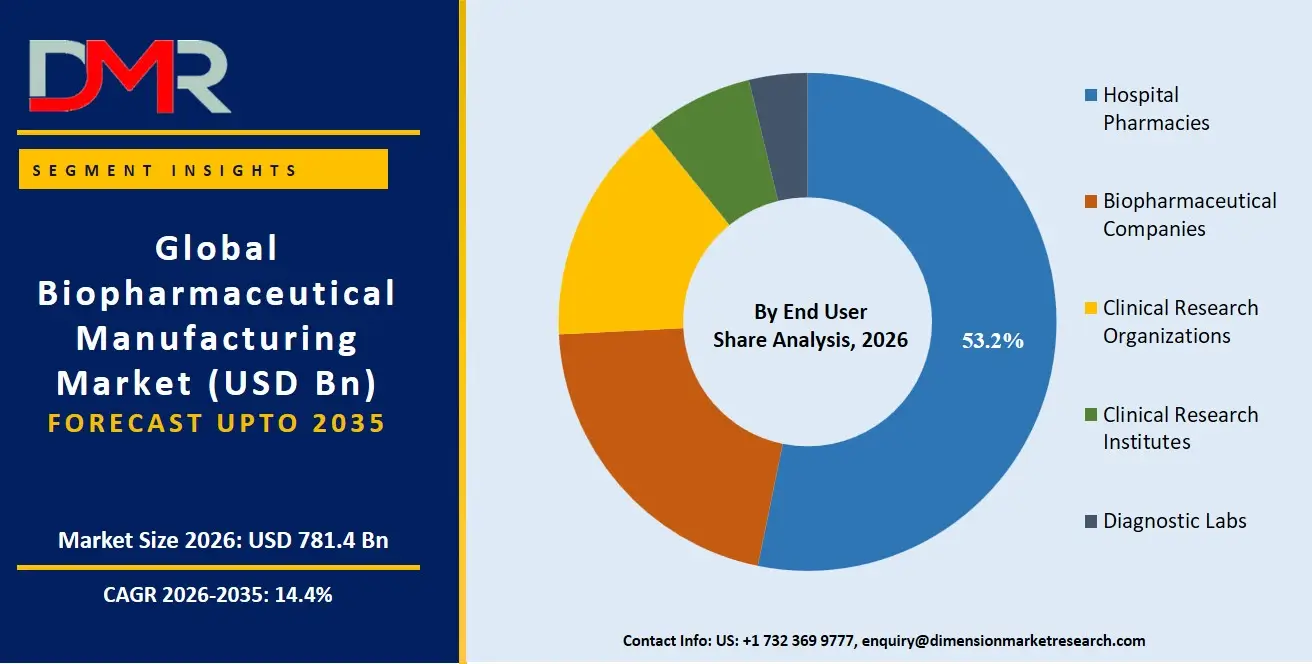

- The biopharmaceutical manufacturing market size is USD 680.3 Billion in 2025, reached USD 781.4 Billion in 2026, and is projected to hit USD 2,627.0 Billion by 2035 at a CAGR of 14.4%.

- Monoclonal Antibodies lead the By Product Type segment with a 45.0% revenue share in 2026.

- North America holds the largest regional share at 48.0% of global revenue in 2026.

- Oncology is the dominant application segment at 39.7% of market revenue in 2026.

- Mammalian-based Expression Systems account for 72.5% of the By Technology segment in 2026.

- Hospital Pharmacies represent 53.2% of the By End-User segment in 2026.

Market Overview

The biopharmaceutical manufacturing market covers the full production chain for biologics including monoclonal antibodies, recombinant proteins, vaccines, hormones, insulins, interferons, growth and coagulation factors, and cell and gene therapies. Small-molecule chemical synthesis and traditional generic drug production fall outside biopharmaceutical manufacturing market's scope. Coverage spans both in-house and outsourced contract manufacturing operations at commercial, pilot, and clinical scales.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The U.S. sub-market is valued at USD 318.8 Billion in 2026 and is forecast to reach USD 1,090.4 Billion by 2035 at a CAGR of 13.9%, marginally above the global rate. This premium reflects the policy-driven reshoring of manufacturing capacity that has made the United States the world's most active biopharma manufacturing construction zone. Samsung Biologics announced its 6th plant in January 2025, pushing total CDMO biologics capacity toward 964,000 liters, confirming that scale-building is accelerating across both integrated manufacturers and contract operators simultaneously.

Biopharmaceutical manufacturing market connects directly to the broader pharmaceutical industry as the production engine behind the highest-value drug categories. Biologics command premium pricing and growing prescription volumes across oncology, autoimmune, and metabolic disease categories, making manufacturing capacity a strategic asset rather than a cost center. CDMO consolidation is centralizing outsourced production into fewer, larger operators, and corporate procurement decisions now flow through manufacturing capability assessments first and pricing second.

Market Size and Forecast

The Global Biopharmaceutical Manufacturing Market size is estimated at USD 781.4 Billion in 2026 from USD 680.3 Billion in 2025, and is projected to reach USD 2,627.0 Billion by 2035, exhibiting a CAGR of 14.4% during the forecast period.

Novo Holdings' USD 16.5 Billion acquisition of Catalent anchors a CDMO consolidation wave centralizing outsourced capacity into fewer operators with higher throughput targets. Amgen's USD 900 Million Ohio expansion bringing total Central Ohio investment to over USD 1.4 Billion illustrates that mid-tier capital deployments are compounding alongside headline reshoring pledges, confirming the market's growth trajectory is broad-based rather than concentrated in a handful of flagship projects. A market nearly quadrupling in value over a decade implies structural expansion driven by pipeline maturation, new modality launches, and government-backed manufacturing reshoring acting simultaneously.

The upside scenario materializes if cell and gene therapy manufacturing investment rebounds with fresh regulatory approvals and reimbursement clarity. The downside scenario centers on tariff-driven supply chain disruption. If pharmaceutical tariffs escalate beyond current levels, companies already restructuring investment strategies in 2026 may delay or scale back planned U.S. buildouts, compressing the CAGR in the forecast period's middle years before domestic-only operators absorb the volume gap.

Product Type Analysis

Monoclonal Antibodies led the By Product Type segment with a 45.0% share in 2026.

Monoclonal antibody dominance reflects decades of standardized large-scale production via mammalian cell culture, broad therapeutic coverage across oncology and autoimmune indications, and a continuously expanding approval pipeline that sustains long-term manufacturing volume commitments. No competing product type combines commercial maturity, platform standardization, and pipeline depth at an equivalent scale. mAb production infrastructure is the single most commercially critical manufacturing asset in biopharmaceutical manufacturing market today.

Recombinant proteins serve as the foundational biologics category for therapeutic areas requiring precise protein replacement. Vaccines represent a high-volume, government-linked segment with distinct fill-finish and cold-chain requirements. Insulin and recombinant hormones anchor the metabolic disorder segment. Cell and gene therapies are the most capital-intensive and technically complex product type. Multiple CDMOs exited CGT manufacturing in 2026 due to misalignment between production capital intensity and reimbursement stability, creating a supply gap that pipeline approvals will pressure in the near term.

Application Analysis

Oncology accounted for 39.7% of By Application demand in 2026, the highest of any therapeutic category.

Cancer biologics generate the highest per-product manufacturing volume requirements of any therapeutic area. Every new oncology biologic approval triggers a multi-year production commitment, which is why manufacturers allocate disproportionate bioreactor capacity to oncology programs well ahead of market launch. Approved monoclonal antibodies, antibody-drug conjugates, and cell therapies are concentrated in oncology indications, meaning this application segment directly drives the market's two highest-investment product categories simultaneously.

Autoimmune disorders represent the second most commercially significant application, with chronic dosing patterns creating predictable high-volume demand that supports efficient capacity planning. Metabolic disorders are attracting the fastest-moving manufacturing capital in the current cycle due to GLP-1 demand. Hormonal disorders, cardiovascular diseases, neurological diseases, and blood disorders collectively provide manufacturing base load: stable, recurring production runs that help manufacturers amortize fixed infrastructure costs alongside higher-profile programs.

Technology Analysis

With a 72.5% share in 2026, Mammalian-based Expression Systems outpaced all other technology categories.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Mammalian cell culture is the only commercially validated system for producing properly folded, glycosylated complex proteins such as monoclonal antibodies at commercial scale. This is a technical necessity, not a preference. The 72.5% share concentration means bioreactor capacity, particularly single-use and hybrid systems, is a direct constraint on how fast the market can respond to demand signals across oncology, autoimmune, and metabolic biologic programs.

Microbial expression systems serve applications where protein complexity is lower and cost efficiency is prioritized, remaining commercially relevant for insulin, certain hormones, and recombinant proteins where glycosylation is not required. Yeast expression systems occupy a specialized position supporting select vaccine antigens and recombinant proteins. Continuous manufacturing is transitioning from experimental to commercially viable following the WHO's February 2025 draft guideline, which removed a major regulatory adoption barrier for manufacturers evaluating new facility design.

End-User Analysis

Hospital Pharmacies captured 53.2% of the By End-User segment in 2026.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Hospital pharmacies serve as the primary dispensing point for oncology biologics, cell therapies, and injectable treatments requiring clinical administration. These are the same product categories driving the largest manufacturing investment flows. Every major new biologics approval in oncology or metabolic disease translates directly into sustained hospital pharmacy procurement volumes, creating a predictable demand signal that manufacturers can build capacity against.

Biopharmaceutical companies function as both end-users and producers, with in-house manufacturing decisions driving market scale directly. Clinical research organizations and institutes represent the pipeline-facing demand layer, consuming clinical-scale manufacturing output for trial supply. As cell and gene therapy clinical programs advance, demand for specialized manufacturing access will intensify precisely where CDMO capacity pullbacks in 2026 left the deepest supply gaps. Diagnostic labs use recombinant proteins and monoclonal antibodies as reagents, providing a stable, less cyclical demand base tied to precision diagnostics expansion.

Key Market Segments

By Product Type

- Monoclonal Antibodies

- Recombinant Proteins

- Vaccines

- Recombinant Hormones

- Insulin

- Interferon

- Growth & Coagulation Factors

- Cell and Gene Therapies

By Application

- Oncology

- Autoimmune Disorders

- Inflammatory and Infectious Diseases

- Metabolic Disorders

- Hormonal Disorders

- Cardiovascular Diseases

- Neurological Diseases

- Blood Disorders

By Technology / Expression System

- Mammalian-based Expression Systems

- Microbial Expression Systems

- Yeast Expression Systems

- Insect Cell Expression Systems

- Continuous Manufacturing

By End-User

- Biopharmaceutical Companies

- Hospital Pharmacies

- Clinical Research Organizations

- Clinical Research Institutes

- Diagnostic Labs

By Scale of Operation

- Commercial-scale Manufacturing

- Pilot-scale Manufacturing

- Clinical-scale Manufacturing

By Mode of Operation

- In-house Manufacturing

- Outsourced/Contract Manufacturing

By Bioreactor System

- Single-Use Bioreactors

- Stainless Steel Bioreactors

- Hybrid Bioreactor Systems

Regional Analysis

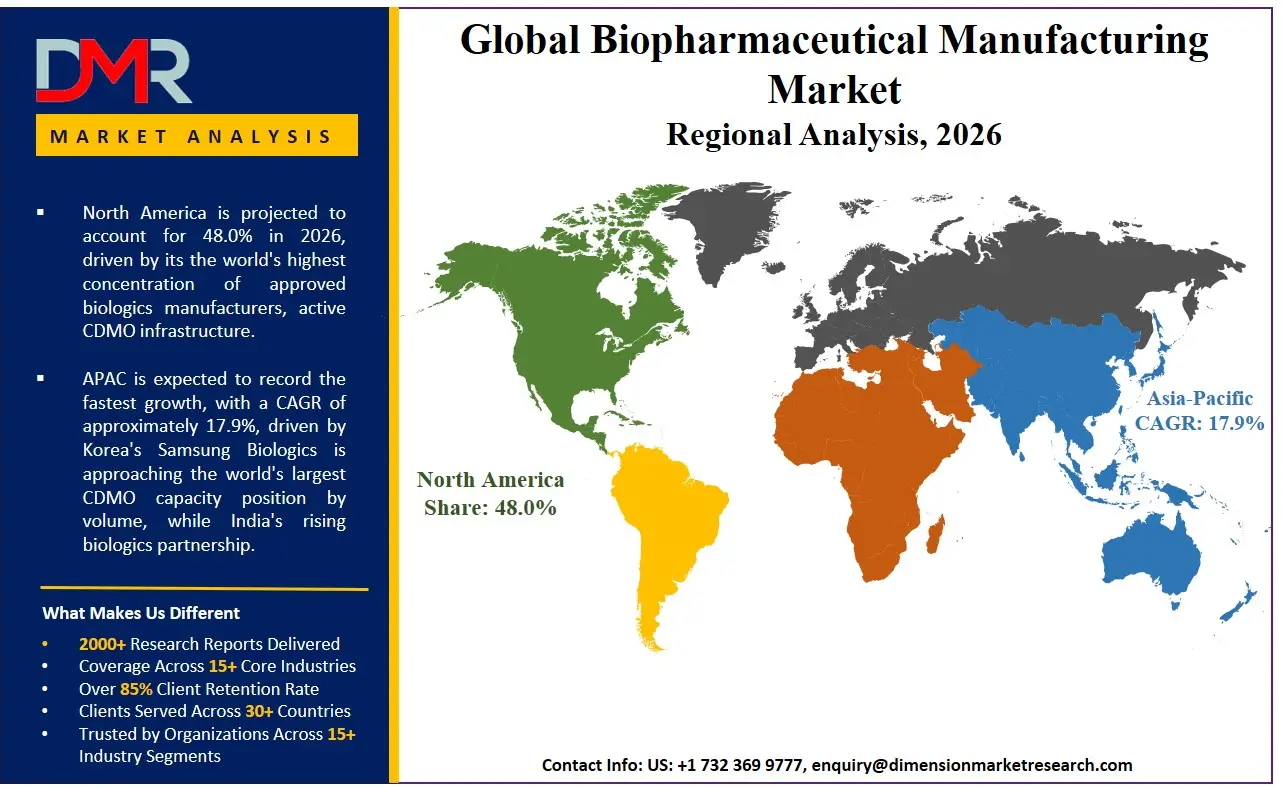

North America held a 48.0% share in 2026, the largest of any region globally.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

North America's dominance reflects the world's highest concentration of approved biologics manufacturers, active CDMO infrastructure, and the largest single-country policy-driven capacity investment wave on record. The U.S. sub-market at USD 318.8 Billion drives this regional position, supported by over USD 480 Billion in newly pledged domestic manufacturing investment following April 2025 tariff threats. In August 2025, WuXi Biologics received EMA approval for its approximately USD 500 Million commercial biologics manufacturing site in Dundalk, Ireland, confirming that European regulators are actively processing next-generation CDMO facility applications even as fresh capital flows disproportionately toward U.S. sites.

Asia Pacific is the most strategically consequential growth region outside North America. South Korea's Samsung Biologics is approaching the world's largest CDMO capacity position by volume, while India's rising biologics partnership activity signals a structural shift in the region's manufacturing role. Europe maintains established production hubs in Ireland, Germany, and Switzerland, but the U.S. reshoring wave is diverting fresh capital commitments away from European greenfield sites, creating a relative investment gap that regional manufacturers must address independently. Latin America and the Middle East and Africa remain early-stage manufacturing geographies where domestic demand for biologics provides a long-term development rationale ahead of full GMP infrastructure maturity.

Key Regions and Countries

North America

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Market Dynamics

Tariff-Driven Reshoring and GLP-1 Demand Redirect Hundreds of Billions in Capital

Following April 2025 tariff threats, U.S. drugmakers pledged over USD 480 Billion across 22+ new biopharmaceutical manufacturing sites and 44,000 jobs. Seven companies alone committed more than USD 305 Billion: Merck over USD 70 Billion, Johnson and Johnson USD 55 Billion, Roche and AstraZeneca each USD 50 Billion, GSK USD 30 Billion, Eli Lilly USD 27 Billion, and Novartis USD 23 Billion. The combined weight of these commitments means construction activity, equipment procurement, and skilled hiring will sustain elevated capacity investment through at least 2030.

Eli Lilly committed USD 27 Billion to build four new U.S. sites in February 2025, more than doubling its U.S. capital deployment since 2020. Samsung Biologics is pushing total CDMO capacity toward 964,000 liters to serve high-volume biologics programs. The FDA declared the U.S. semaglutide shortage resolved in February 2025, confirming that GLP-1 fill-finish scaling programs succeeded and converting supply uncertainty into confirmed production capability across the fill-finish tier.

Tariff Uncertainty and CGT Manufacturing Pullbacks Create Bifurcated Investment Risk

The same tariff environment that drove reshoring also introduced planning disruption. Roche, Novartis, and UCB each moved to restructure investment strategies in 2025 in response to pharmaceutical tariff threats. For multinational manufacturers operating global supply chains, unpredictable tariff scope and timing make long-horizon capital allocation inherently risky. Multiple CDMOs exited or reduced CGT capacity throughout 2025, reflecting an industry-wide recognition that CGT production capital intensity does not yet match reimbursement stability or pipeline conversion rates.

CDMO Consolidation, India's Rise, and Next-Generation Builds Open Distinct Entry Points

India's pharmaceutical exports reached USD 27.8 Billion in FY2024, nearly double the USD 14.9 Billion recorded in FY2014. This trajectory makes India a viable secondary manufacturing location for companies seeking cost competitiveness and tariff diversification. Roche's USD 50 Billion U.S. plan covering 13 manufacturing sites, 15 R&D sites, a 900,000 sq ft obesity medicine facility, and a Pennsylvania gene therapy plant confirms that greenfield investment in next-generation capacity is proceeding at scale. For equipment suppliers, engineering firms, and specialized CDMO operators, these projects represent clearly scoped commercial opportunities with confirmed funding.

Market Trends

Continuous Manufacturing, Mega-Capacity Builds, and Digital Integration Redefine Facility Economics

UCB selected Gwinnett County, Georgia for a new U.S. biologics manufacturing facility in June 2025, projected to generate USD 5 Billion in total economic impact with approximately 330 permanent jobs and over 1,000 construction roles. This facility represents the new template for greenfield biologics investment: domestically sited, economically anchored in specific jurisdictions, and designed for multiple product modalities from commissioning. Eli Lilly became the first pharmaceutical company to reach a USD 1 Trillion market valuation on November 21, 2025, driven by its GLP-1 capacity buildout strategy, demonstrating directly that manufacturing scale commands equity premium in biopharmaceutical manufacturing market.

The WHO published a draft guideline on continuous manufacturing of pharmaceutical products in February 2025, marking a pivotal regulatory step toward global harmonization. Early movers embedding automation and digital process controls in current buildouts are building operational advantages that later entrants will not replicate at equivalent cost, particularly as FDA guidance on software validation and AI-driven process controls continues to evolve alongside physical facility approvals.

Market Competition Overview

The biopharmaceutical manufacturing market operates as a two-tier structure: a consolidated upper tier of large integrated manufacturers and a consolidating CDMO tier. WuXi Biologics posted 9.6% revenue growth in 2024, demonstrating that geographic expansion and regulatory credential accumulation are the two dimensions of competitive scale-building for CDMOs with ambitions beyond their home markets. Samsung Biologics' USD 1.3 Billion single-client contract illustrates that buyers at the largest commercial scale are consolidating manufacturing relationships around operators with confirmed throughput, compressing the competitive viability of mid-tier CDMOs without equivalent capacity depth.

Integrated manufacturers are simultaneously internalizing production volume that previously flowed to CDMOs, pushing outsourced competition toward specialized modalities. Digital manufacturing and AI integration are emerging as the next competitive battleground. Operators who embed digital process controls now are building efficiency and yield advantages that will be structurally difficult for later movers to close, particularly as regulatory submission requirements for digital manufacturing systems add compliance complexity that rewards early investment.

Company Profiles

Eli Lilly and Company has positioned itself as the market's defining capital deployer of the current cycle. In September 2025, Eli Lilly selected Goochland County, Virginia for a USD 5 Billion biopharmaceutical manufacturing facility, its first fully integrated API and drug product site for bioconjugates and monoclonal antibodies, creating 650 jobs. In October 2025, Merck broke ground on a USD 3 Billion, 400,000 sq ft pharmaceutical center of excellence in Elkton, Virginia generating 500 jobs as part of its broader U.S. expansion, confirming that the largest manufacturers are choosing long-duration asset investments designed to serve multiple product generations through the 2030s.

F. Hoffmann-La Roche Ltd. anchors its competitive position through multi-modality breadth, hedging across GLP-1, oncology biologics, and CGT simultaneously. Samsung Biologics has constructed a CDMO competitive moat through capacity accumulation, with its pipeline toward 964,000 liters giving it utilization resilience across client wins and losses that no other pure-play CDMO can match at current scale. Merck's plan, the largest individual company pledge in the reshoring wave, prioritizes supply control and domestic policy alignment over short-term capital efficiency, positioning it for structural procurement advantages through the 2030s.

Key Players

- Eli Lilly and Company

- AbbVie Inc.

- Amgen Inc.

- Biogen Inc.

- F. Hoffmann-La Roche Ltd.

- Johnson & Johnson

- Merck & Co. Inc.

- Novo Nordisk A/S

- Pfizer Inc.

- Sanofi S.A.

- Novartis AG

- Bristol Myers Squibb

- Gilead Sciences Inc.

- AstraZeneca PLC

- Takeda Pharmaceutical Co.

- CSL Limited

- Lonza Group AG

- Boehringer Ingelheim

- Thermo Fisher Scientific Inc.

- Merck KGaA

- Samsung Biologics

- WuXi Biologics

- Ajinomoto Co. Inc.

Supply Chain and Value Chain Analysis

The biopharmaceutical manufacturing value chain begins with raw material suppliers producing cell culture media, bioreactor consumables, specialized buffer components, and single-use systems. GMP validation requirements create high switching costs once a raw material source is qualified in a licensed manufacturing process, giving upstream suppliers structural pricing power independent of market volume conditions. Drug substance manufacturing, where cell lines produce active biologics, is the core physical constraint on market output, making bioreactor capacity the binding variable on commercial throughput.

Novo Nordisk's USD 11.7 Billion acquisition of three former Catalent fill-finish sites concentrated GLP-1 fill-finish capacity within a single operator's control, reducing independent access for other injectable biologics programs. Thermo Fisher's acquisition of Sanofi's Ridgefield, New Jersey steriles manufacturing site extends the same consolidation pattern into the broader sterile injectable fill-finish tier. Buyers seeking fill-finish capacity for non-GLP-1 programs including ADCs, cell therapies, and radioligand products now face elevated contract pricing and a materially reduced set of qualified independent operators, making fill-finish access the most commercially acute supply chain constraint in the current market.

Regulatory Landscape

The biopharmaceutical manufacturing regulatory environment is defined by overlapping jurisdiction across the U.S. FDA, European EMA, and WHO, each with distinct GMP inspection standards and facility certification requirements. Operating across all three major markets requires manufacturers to maintain parallel compliance programs, creating structural cost floors that smaller operators cannot sustain. This complexity concentrates commercial-scale biologics manufacturing among well-capitalized, experienced organizations and functions as a de facto market entry barrier with greater practical force than any tariff or trade measure.

GSK's plan to deploy AI and advanced digital manufacturing technology across five existing U.S. sites in Maryland, Montana, North Carolina, and Pennsylvania as part of its USD 30 Billion commitment introduces a new compliance dimension. Johnson and Johnson's 2026 voluntary agreement with the U.S. government, tying its USD 55 Billion manufacturing buildout to participation in the TrumpRx program and tariff exemption arrangements, signals an emerging model where large-scale manufacturing investment becomes a negotiating instrument for regulatory and trade policy accommodation, creating competitive asymmetry favoring those with capital to deploy.

Investment and White Space Analysis

Novartis is constructing 2 new radioligand therapy facilities in Florida and Texas and expanding 3 existing RLT sites within its U.S. plan, a total of 5 RLT facility actions from a single operator. This concentration signals that RLT manufacturing expertise is scarce enough that Novartis has chosen to build rather than outsource. For CDMOs or specialized operators willing to invest in RLT-compliant infrastructure including radiopharmaceutical handling and containment systems, the addressable market is large and the qualified supplier base remains narrow enough to support premium contract pricing.

Eli Lilly's USD 1 Billion-plus commitment to Indian manufacturing partnerships in October 2025 validates India as a biologics manufacturing partner and opens the investment case for GMP biologics infrastructure upgrades in a cost-competitive environment. Cell and gene therapy commercial manufacturing is the most underserved segment: CDMOs exited CGT capacity in 2025 despite a growing approval pipeline, and no broad-market supply response has emerged to fill the gap. Operators who build credible GMP CGT commercial manufacturing capacity now will face limited direct competition when pipeline approvals accelerate demand, entering a segment where contract pricing is structurally elevated and qualified alternatives remain scarce.

Recent Developments

- February 2026 Johnson & Johnson. Facility announcement. Announced a USD 1 Billion-plus next-generation cell therapy manufacturing facility in Lower Gwynedd Township, Pennsylvania, creating over 500 skilled jobs over a 12-year horizon.

- July 2025 Thermo Fisher Scientific and Sanofi. Strategic partnership. Thermo Fisher set to acquire Sanofi's steriles manufacturing site in Ridgefield, New Jersey, continuing to manufacture Sanofi therapies while opening capacity to additional biopharma customers.

- April 2025 Roche. Investment commitment. Committed USD 50 Billion to U.S. biopharmaceutical manufacturing and diagnostics over five years, covering expansion of 13 manufacturing sites, 15 R&D sites, and creation of over 12,000 jobs including a 900,000 sq ft obesity medicine facility and a Pennsylvania gene therapy plant.

- April 2025 Novartis. Investment plan. Unveiled a USD 23 Billion U.S. manufacturing and R&D investment plan covering 10 facilities over five years, including 7 new sites and a USD 1.1 Billion biomedical research innovation hub in San Diego.

- April 2025 Eli Lilly. Investment. Announced plans to invest USD 27 Billion in four new U.S. biopharmaceutical manufacturing sites, more than doubling its U.S. capital deployment since 2020 and creating over 3,000 high-skilled manufacturing jobs.

Report Details

| Report Characteristics |

| Market Value (2025) |

USD 680.3 Billion |

| Market Value (2026) |

USD 781.4 Billion |

| Forecast Revenue (2035) |

USD 2,627.0 Billion |

| CAGR (2026 to 2035) |

14.4% |

| Base Year for Estimation |

2025 |

| Historic Period |

2020 to 2024 |

| Forecast Period |

2026 to 2035 |

| Report Coverage |

Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered |

By Product Type (Monoclonal Antibodies, Recombinant Proteins, Vaccines, Recombinant Hormones, Insulin, Interferon, Growth & Coagulation Factors, Cell and Gene Therapies), By Application (Oncology, Autoimmune Disorders, Inflammatory and Infectious Diseases, Metabolic Disorders, Hormonal Disorders, Cardiovascular Diseases, Neurological Diseases, Blood Disorders), By Technology / Expression System (Mammalian-based Expression Systems, Microbial Expression Systems, Yeast Expression Systems, Insect Cell Expression Systems, Continuous Manufacturing), By End-User (Biopharmaceutical Companies, Hospital Pharmacies, Clinical Research Organizations, Clinical Research Institutes, Diagnostic Labs), By Scale of Operation (Commercial-scale Manufacturing, Pilot-scale Manufacturing, Clinical-scale Manufacturing), By Mode of Operation (In-house Manufacturing, Outsourced/Contract Manufacturing), By Bioreactor System (Single-Use Bioreactors, Stainless Steel Bioreactors, Hybrid Bioreactor Systems) |

| Regional Analysis |

North America – US and Canada; Europe – Germany, France, The UK, Spain, Italy, and Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, and Rest of APAC; Latin America – Brazil, Mexico, and Rest of Latin America; Middle East & Africa – GCC, South Africa, and Rest of MEA |

| Competitive Landscape |

AbbVie Inc., Amgen Inc., Biogen Inc., Eli Lilly and Company, F. Hoffmann-La Roche Ltd., Johnson & Johnson, Merck & Co. Inc., Novo Nordisk A/S, Pfizer Inc., Sanofi S.A., Novartis AG, Bristol Myers Squibb, Gilead Sciences Inc., AstraZeneca PLC, Takeda Pharmaceutical Co., CSL Limited, Lonza Group AG, Boehringer Ingelheim, Thermo Fisher Scientific Inc., Merck KGaA, Samsung Biologics, WuXi Biologics, Ajinomoto Co. Inc. |

| Customization Scope |

Customization for segments and region or country level will be provided. Additional customization can be done based on requirements. |

| Purchase Options |

Three license options: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF). |

Frequently Asked Questions

What is the biggest investment opportunity in biopharmaceutical manufacturing market?

▾ Cell and gene therapy commercial manufacturing is the highest-potential white space. CDMOs exited CGT capacity in 2026 despite a growing approval pipeline, leaving a supply gap with no broad market response. Radioligand therapy manufacturing is a second high-specificity opportunity where the qualified supplier base remains narrow and contract pricing is structurally elevated for operators with compliant infrastructure.

Who are the top companies in biopharmaceutical manufacturing market?

▾ Leading players include Eli Lilly, Roche, Merck, Johnson and Johnson, Novartis, AstraZeneca, GSK, Pfizer, Novo Nordisk, Samsung Biologics, WuXi Biologics, Lonza, and Thermo Fisher Scientific. These companies collectively account for the majority of both in-house manufacturing capacity and CDMO contract volumes globally.

Which segment is growing fastest in Biopharmaceutical Manufacturing Market and why?

▾ Metabolic disorders, driven by GLP-1 therapy demand, is attracting the fastest-moving manufacturing capital in the current cycle. The successful resolution of the semaglutide shortage confirmed that fill-finish scaling works at commercial speed, validating further investment across dedicated API and injectable production infrastructure for this therapeutic category.

Which region is growing fastest in Biopharmaceutical Manufacturing Market and why?

▾ Asia Pacific offers the strongest growth trajectory outside North America, anchored by South Korea's CDMO scale-building and India's rising biologics manufacturing role. The region's cost competitiveness, expanding regulatory maturity, and proximity to large patient populations make it the primary destination for capacity investment not directed at U.S. reshoring programs.

What is the biggest challenge holding biopharmaceutical manufacturing market back?

▾ Pharmaceutical tariff uncertainty is the primary planning constraint. Multinational manufacturers face the risk that long-horizon capital commitments made under current conditions become economically unfavorable if tariff scope escalates, delaying buildouts that the market's growth trajectory depends on materializing by 2028 to 2030.