Market Snapshot

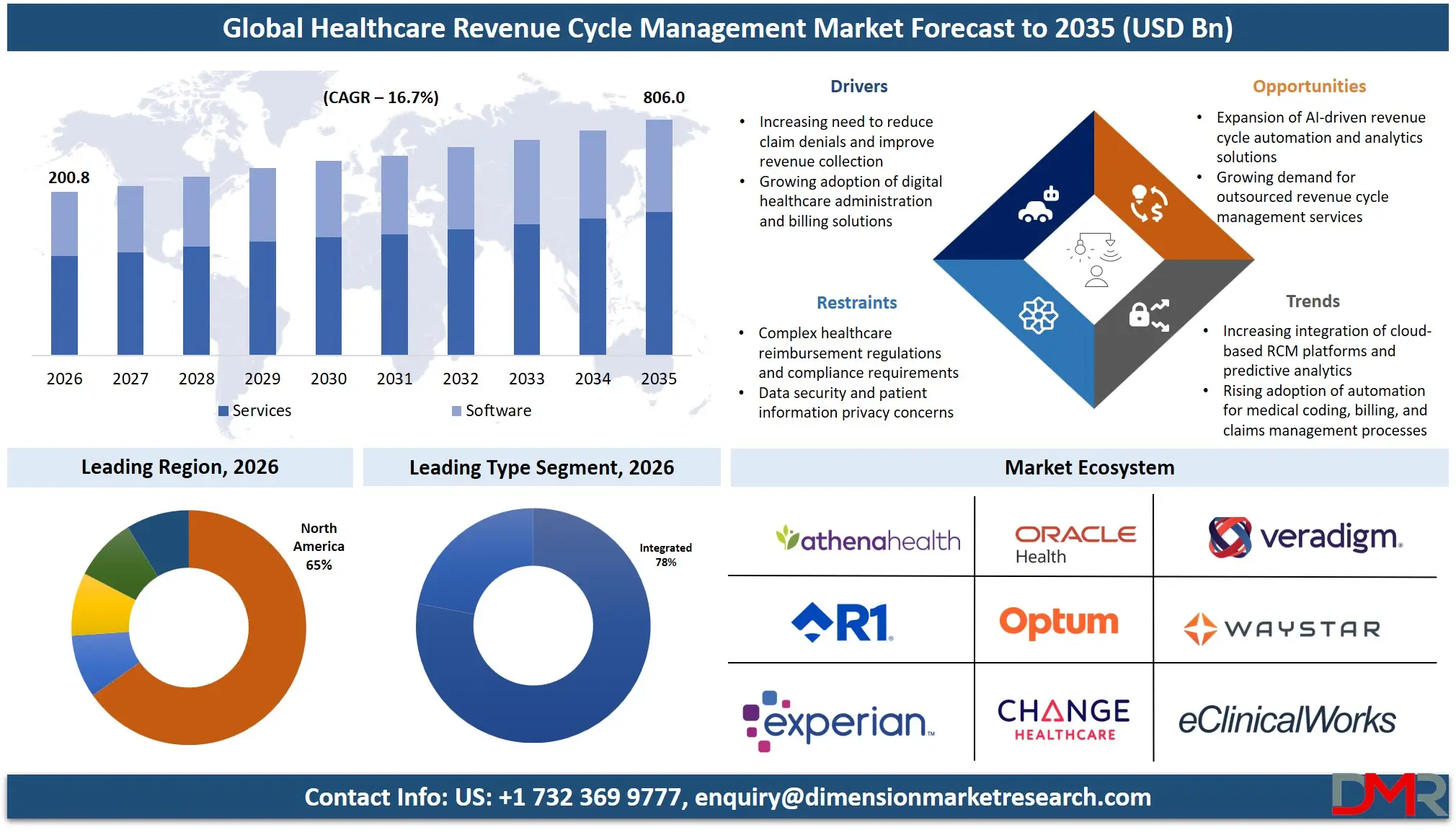

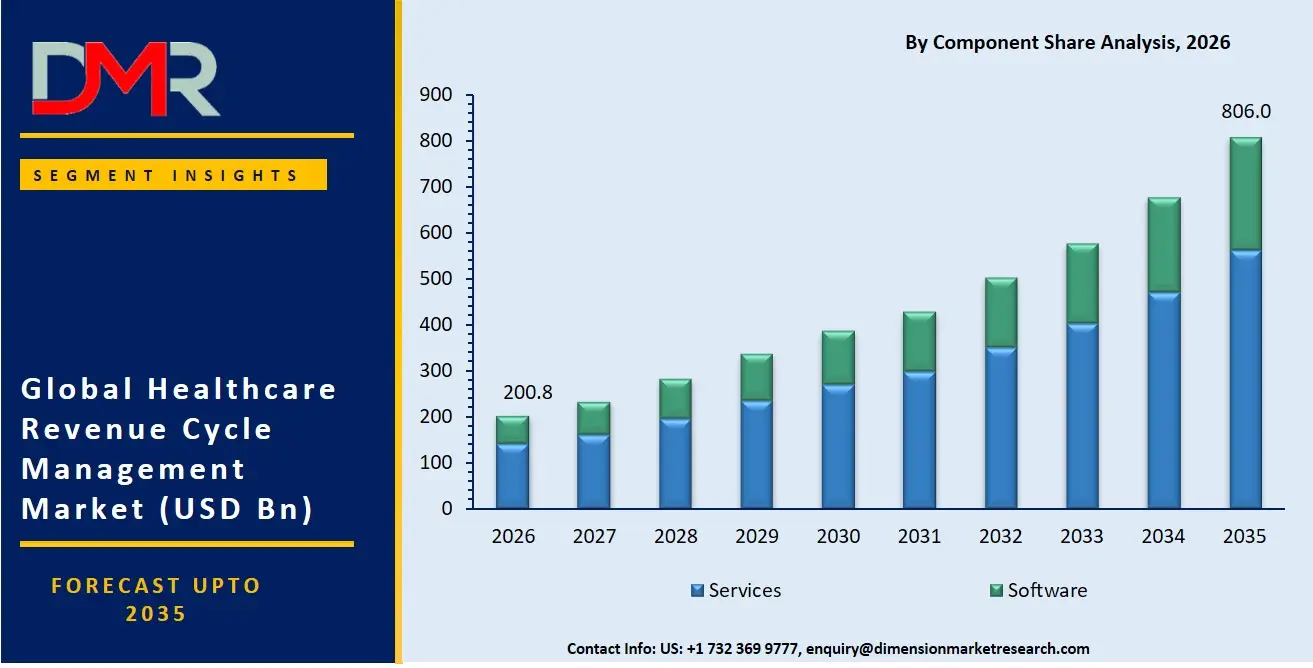

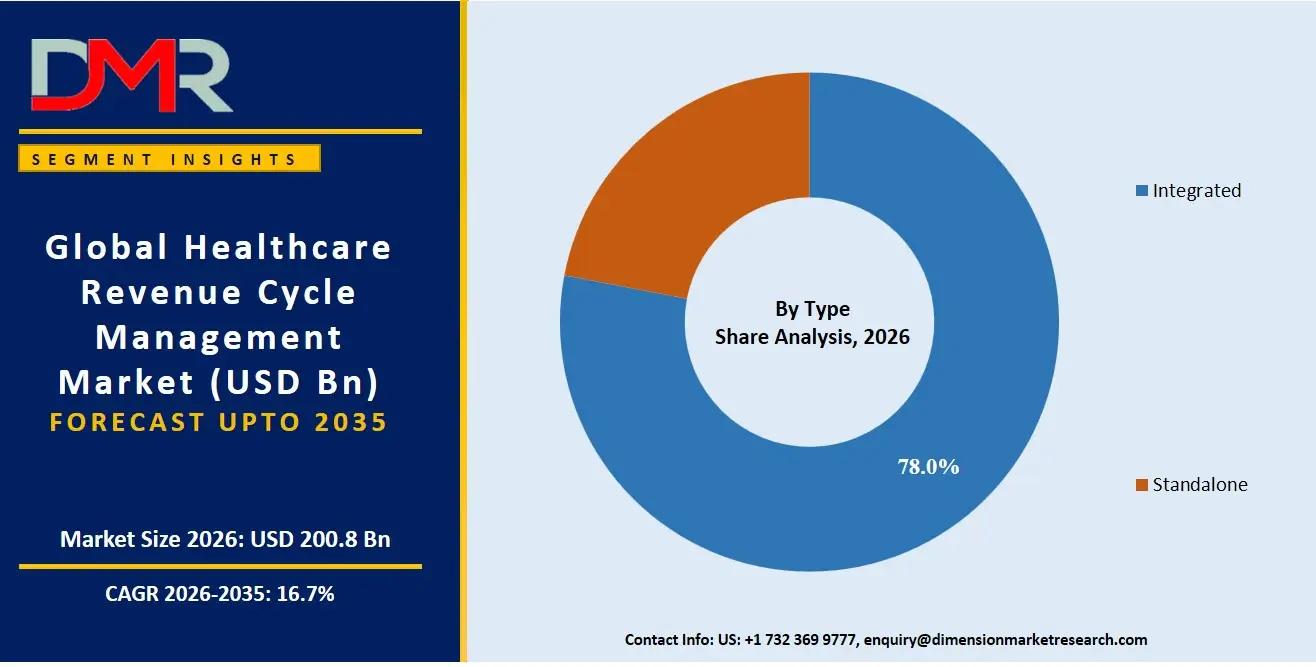

- The global Healthcare Revenue Cycle Management Market is valued at USD 200.8 Billion in 2026 and is forecast to reach USD 806.0 Billion by 2035.

- The market will expand at a CAGR of 16.7% during the forecast period 2026 to 2035.

- The United States market is valued at USD 112.3 Billion in 2026, projected to reach USD 337.1 Billion by 2035, growing at a CAGR of 12.4%.

- China's Healthcare RCM Market was valued at USD 5.5 Billion in 2024 and is projected to reach USD 35.4 Billion by 2035, at a CAGR of 17.3%.

- By Product/Component, Services holds the dominant position with a 69.6% revenue share.

- By Type, Integrated solutions lead with a 78.0% revenue share.

- By Delivery Mode, Web-Based deployment commands a 56.8% revenue share.

- By End-User, Hospitals account for 62.8% of market revenue.

- By Sourcing, In-house operations hold a 71.3% revenue share.

- By Physician Specialty, Others (general practice) leads with 71.6% revenue share.

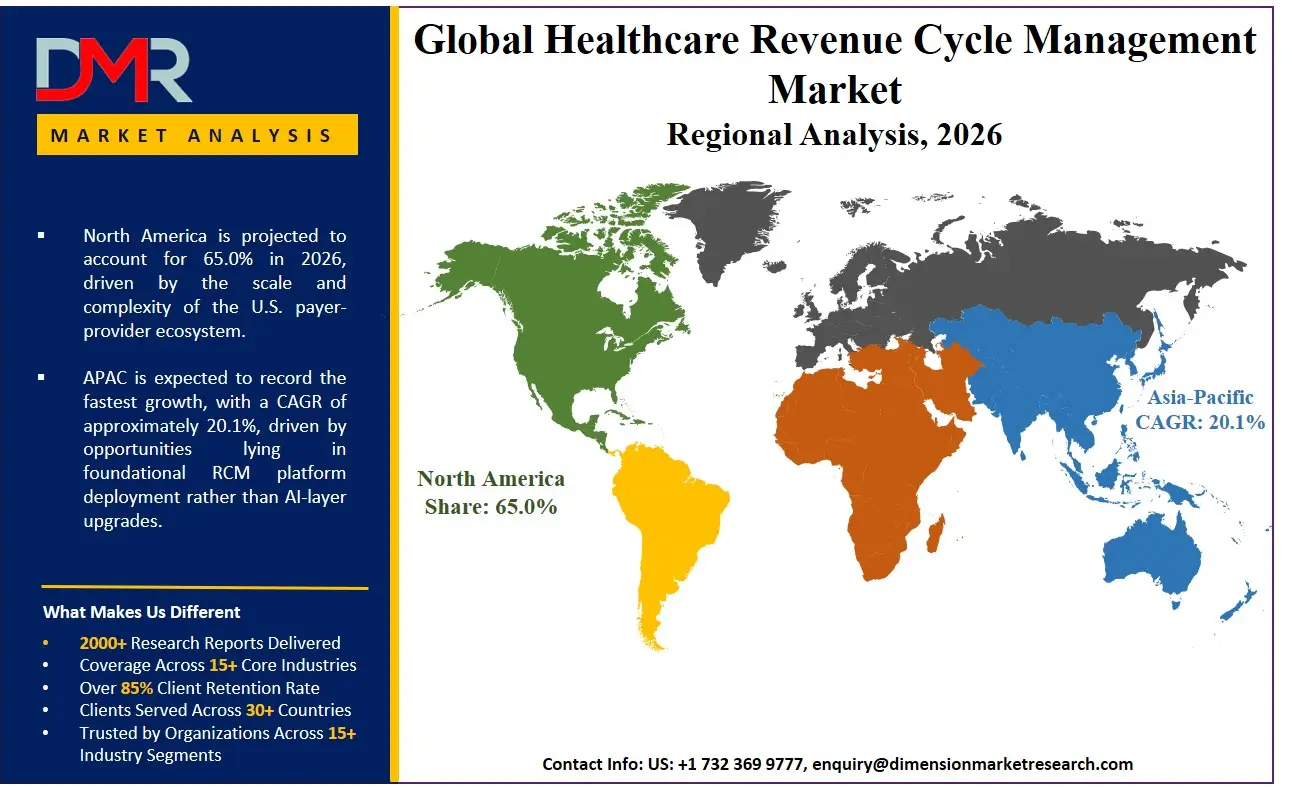

- North America is the dominant region with a 65.8% revenue share in 2026.

- Key players include R1 RCM, Oracle, Optum Inc., McKesson Corporation, Change Healthcare, and others.

Market Overview

The global Healthcare Revenue Cycle Management Market is valued at USD 200.8 Billion in 2026. The market will reach USD 806.0 Billion by 2035, expanding at a CAGR of 16.7% over the forecast period 2026 to 2035.

Healthcare Revenue Cycle Management covers the full financial lifecycle of a patient account. The scope spans eligibility verification and prior authorization at patient access through clinical documentation, coding, claims submission, denial management, and final payment posting. The market includes both software platforms and managed services that providers use to execute these workflows. Electronic health records, clinical care platforms, and hospital information systems that do not directly process revenue transactions fall outside this scope.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Providers cannot sustain operations without efficient claim reimbursement. RCM is one of the most operationally critical technology categories in healthcare. Payer complexity continues to rise. The cost of revenue leakage from denials and coding errors compounds across every care setting.

The market reflects a structural shift away from manual billing departments toward automated, AI-driven platforms. As reported by HFMA, 63% of healthcare organizations now use AI and automation in their revenue cycle. Manual RCM is no longer a viable cost model for mid-to-large providers.

Platform economics are proving durable across top-tier vendors. Waystar reported net revenue retention of 111% in Q1 2026, confirming that existing hospital clients are expanding spend on RCM automation over time. Once a provider adopts a platform, upsell of denial-prevention, AI, and post-acute modules drives consistent revenue expansion. New customer acquisition is not the only growth engine for established vendors.

The cybersecurity dimension of RCM demands serious attention from every market participant. UnitedHealth disclosed Change Healthcare cyberattack-related costs of USD 2.457 Billion through Q3 2024. Vendors and providers are now re-evaluating platform concentration risk. Demand for redundant RCM infrastructure and vendor diversification strategies is accelerating as a direct result.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Market Size and Forecast

The global Healthcare RCM Market stands at USD 200.8 Billion in 2026. The United States accounts for the largest national share at USD 112.3 Billion. China contributes USD 5.5 Billion as of 2024. A single country the U.S. represents nearly 56% of global volume, making it the primary battleground for vendor competition and institutional investment.

The global market will reach USD 806.0 Billion by 2035, expanding at a CAGR of 16.7%. The U.S. market grows at a comparatively slower CAGR of 12.4%, reflecting the maturity of its hospital and physician RCM base. China grows at a CAGR of 17.3% to reach USD 35.4 Billion by 2035. An earlier-stage digitization cycle in China's provider ecosystem explains that growth differential.

The forecast assumes continued AI adoption across hospital RCM departments. Expansion of prior authorization automation ahead of CMS 2026 mandates is a second core assumption. Private equity-backed platform consolidation compressing the vendor landscape is a third. Waystar reported full-year 2024 RCM revenue of USD 944 Million, up 19% year-over-year. Its full-year 2026 revenue guidance of USD 1.274 to 1.294 Billion confirms that best-in-class platforms are sustaining double-digit growth.

Market Dynamics

Drivers: AI Integration, Regulatory Mandates, and Private Equity Consolidation Are Structurally Reshaping Provider RCM Investment

Generative AI has moved well past the pilot stage in hospital revenue cycles. In 2026, Optum launched an AI-powered RCM solution automating clinical documentation, coding, and denials workflows. AI deployment has shifted from single-function tools to end-to-end automation covering the full revenue cycle. Vendors still relying on manual or semi-automated processes face a narrowing competitive window.

Regulatory pressure is forcing provider action on a defined timeline. The CMS Interoperability and Prior Authorization Final Rule, issued in January 2024, requires electronic prior authorization APIs by 2026. Providers that delay RCM platform upgrades now face compliance risk, not just operational inefficiency. A regulatory deadline converts modernization from a discretionary investment to a mandatory one.

Private equity capital is accelerating vendor consolidation at the top of the market. TowerBrook Capital Partners and Clayton, Dubilier and Rice completed the USD 8.9 Billion take-private acquisition of R1 RCM in November 2024, representing a 29% premium to its unaffected share price. A Waystar survey confirmed that 100% of healthcare leaders see AI value in RCM. A separate finding confirmed 90% planned to increase technology spend, a demand signal that directly sustains vendor valuations at scale.

Restraints: Prior Authorization Administrative Burden and Cybersecurity Risk Are Compressing Provider Margins

The prior authorization workload on U.S. providers is quantifiably severe. As reported by KFF, nearly 53 Million prior authorization requests were submitted to Medicare Advantage payers in 2024, up from 50 Million in 2023. Revenue cycle teams are already stretched by staffing shortages. That volume translates directly into delayed reimbursements and rising administrative cost per claim.

KFF analysis found that Medicare Advantage enrollees contested only 12% of denied prior authorization requests. More than 80% of those appeals were partially or fully overturned. The gap between denial rates and overturn rates reveals systematic over-denial by payers. Providers are absorbing avoidable revenue losses by not challenging every denial.

Cybersecurity represents the single largest systemic risk to RCM platform continuity. UnitedHealth disclosed Change Healthcare attack-related costs of USD 2.457 Billion through Q3 2024. Change Healthcare connected with 1 in 3 U.S. patient records before the attack. A single vendor compromise at that scale can freeze revenue cycles across thousands of provider organizations simultaneously.

Growth Factors: Post-Acute Digitization, Middle Revenue Cycle Unification, and Medicare Advantage Complexity Create Addressable White Space

Post-acute and skilled nursing facility revenue cycles remain among the least automated segments in U.S. healthcare. Waystar's 2026 guidance explicitly references expansion into post-acute and SNF RCM digitization as a growth lever supporting its USD 1.274 to 1.294 Billion revenue target. Vendors entering this segment now face low competitive density relative to the acute hospital market. That structural advantage erodes as consolidation accelerates.

The middle revenue cycle has historically been managed through disconnected point solutions. Optum's deployment of a single platform embedding clinical language models across CDI, coding, and compliance workflows directly addresses that fragmentation. Providers adopting unified middle-cycle platforms reduce handoff errors and accelerate clean claim rates. The ROI case for consolidation is straightforward when denial rates and coding accuracy are measured against implementation cost.

Medicare Advantage plan complexity is generating a specialized outsourcing demand. Generalist RCM vendors cannot easily address fragmented MA plan rules covering eligibility, prior authorization edits, and plan-specific billing requirements. Providers facing high MA volumes are outsourcing to specialists rather than managing plan-level edits in-house. The addressable market for targeted RCM services is expanding as MA enrollment continues to grow.

Market Trends

Automation, Electronic Prior Authorization, and AI-Embedded Coding Are Converging to Redefine the RCM Operating Model

Robotic Process Automation has crossed from early adoption to standard deployment across U.S. hospital RCM departments. As documented in a Black Book report, providers are deploying RPA specifically for claims submission and denials workflows in 2026. RPA eliminates the labor bottleneck at the highest-volume, lowest-judgment points in the revenue cycle. Measurable cost reduction follows without requiring full platform replacement.

Electronic prior authorization is producing quantifiable time savings ahead of regulatory deadlines. As reported by HFMA, ePA adoption has already delivered a 56% reduction in approval cycle times among early adopters, ahead of CMS 2026 modernization mandates. For providers, that compression directly reduces days in accounts receivable linked to PA-dependent claims. ePA ranks among the highest-ROI RCM investments available in the current cycle.

Clinical language model deployment in coding workflows is reshaping how providers approach documentation accuracy and compliance. Optum embedded proprietary CLMs across documentation review and final coding in 2025 to 2026, moving AI from a supplemental tool to the primary coding layer. Denial-prevention analytics are simultaneously shifting upstream to patient access. Vendors are targeting front-end PA verification as the primary intervention point against rising denial rates, addressing the problem before a claim is ever submitted.

Product Analysis

Services held a dominant position in the By Product/Component segment of the Healthcare Revenue Cycle Management Market in 2026, commanding a 69.6% revenue share. Most provider organizations lack the internal expertise and staffing to manage end-to-end RCM workflows in-house. Outsourced and managed RCM services deliver not just technology but operational capacity, making them the preferred procurement model across U.S. health systems. A vendor that sells execution alongside software captures both the technology budget and the labor budget.

Software is the fastest-growing sub-segment within the product/component category. AI-powered claim scrubbing, denial prediction, and coding automation tools are embedding deeper into provider workflows, accelerating software procurement. The software layer is where margin and differentiation are accumulating fastest among top-tier vendors. Suppliers building proprietary AI models trained on payer-specific adjudication data are establishing defensible positions that pure service operators cannot replicate.

Type Analysis

Integrated solutions held a dominant position in the By Type segment in 2026, capturing a 78.0% revenue share. Integrated platforms manage the full revenue cycle from eligibility and prior authorization through coding, claims, and payment within a single technology environment. Providers choosing integrated solutions eliminate the inter-system data gaps that generate clean claim failures and denial exposure. Integration is a structural performance advantage, and the 78.0% share confirms the market has reached that conclusion decisively.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Standalone solutions are the fastest-growing sub-segment by growth rate, driven by physician practices and specialty groups requiring targeted RCM capability additions. Point-solution adoption is accelerating in high-complexity specialties where prior authorization and coding requirements exceed what general-purpose billing modules handle well. Suppliers entering with specialty-specific standalone tools face a less consolidated competitive field than the integrated platform market. That window narrows as platform consolidation accelerates.

Delivery Mode Analysis

Web-Based delivery held a dominant position in the By Delivery Mode segment in 2026, commanding a 56.8% revenue share. Web-based RCM platforms require no on-site server infrastructure and deploy across multi-site provider organizations without hardware investment. Hospital systems managing distributed billing operations across campuses and affiliated practices benefit most from that accessibility. The installed base in this category is large and retention is high given the operational cost of platform migration.

Cloud-Based deployment is the fastest-growing delivery mode and the forward architecture for enterprise-grade RCM platforms. Cloud infrastructure supports the AI and machine learning workloads that underpin denial prediction and clinical language model deployment. Cloud adoption is a prerequisite for providers seeking the highest level of RCM automation capability. Suppliers that migrate clients from web-based to cloud-native environments capture incremental revenue from AI module upsell, creating a compounding growth dynamic.

End-User Analysis

Hospitals held a dominant position in the By End-User segment in 2026, accounting for 62.8% of market revenue. Hospitals process the highest claim volumes of any care setting and operate across multiple payer contracts simultaneously. The complexity of hospital RCM justifies the largest per-organization technology and services investment, concentrating market revenue within this segment. A hospital system selecting an RCM platform is committing to a multi-year, multi-million-dollar relationship.

Physician Offices represent the fastest-growing end-user segment as ambulatory care complexity increases. athenahealth served more than 200,000 providers in 2026, illustrating the scale of the ambulatory physician market and the commercial opportunity for RCM vendors serving it. Cardiology, oncology, and orthopedics practices manage high-value procedures with dense prior authorization requirements. Vendors with specialty-specific billing capabilities are capturing disproportionate share in this segment.

Sourcing Analysis

In-house RCM operations held a dominant position in the By Sourcing segment in 2026, commanding a 71.3% revenue share. Large health systems with established billing departments and existing EHR-integrated workflows maintain in-house RCM to preserve direct control over coding accuracy, payer relationships, and compliance oversight. In-house models depend on staffing stability. That is a structural vulnerability given persistent healthcare workforce shortages.

Outsourced RCM is the fastest-growing sourcing model as providers confront rising denial rates, staffing costs, and technology investment requirements simultaneously. Black Book named Ensemble Health Partners, TruBridge, Optum360, and Experian Health as top RCM outsourcing vendors of 2025, based on insights from 11,550 revenue cycle, finance, and IT professionals surveyed from Q3 2024 to Q2 2025. Outsourcing transfers both execution risk and technology investment to specialist vendors. For providers facing operational pressure, that transfer has a clear and measurable financial rationale.

Physician Specialty Analysis

Others (General Practice) held a dominant position in the By Physician Specialty segment in 2026, commanding a 71.6% revenue share. General practice encompasses the broadest provider base in U.S. healthcare, generating the highest aggregate claim volumes across primary care, family medicine, and multi-specialty group practices. RCM platforms serving general practice must handle diverse payer mixes and high transaction throughput. Scalable, cloud-native architecture is a competitive requirement, not an optional feature, in this segment.

Cardiology is the fastest-growing physician specialty sub-segment within the RCM market. Cardiac procedures, imaging studies, and device implants require payer pre-approval across most commercial and Medicare Advantage plans, creating dense administrative workflows. Specialized RCM tools are better positioned to manage cardiology billing than general-purpose platforms. The prior authorization burden in cardiology makes denial-prevention analytics a high-priority procurement criterion for practice administrators in this specialty.

Key Market Segments

By Product/Component

By Type

By Delivery Mode

- Web-Based

- Cloud-Based

- On-Premise

- Hybrid

By Function

- Claims & Denial Management

- Medical Coding & Billing

- Clinical Documentation Improvement (CDI)

- Insurance

By End-User

- Hospitals

- Physician Offices

- Diagnostic Laboratories

- Ambulatory Care

By Sourcing

By Physician Specialty

- Others (General Practice)

- Cardiology

- Oncology

- Orthopedics

Regional Analysis

North America holds a 65.8% revenue share of the global Healthcare RCM Market in 2026, anchored by the scale and complexity of the U.S. payer-provider ecosystem. The United States alone is valued at USD 112.3 Billion in 2026 and is projected to reach USD 337.1 Billion by 2035 at a CAGR of 12.4%. No other region approaches this concentration of RCM vendor activity, private equity investment, or regulatory-driven technology mandates. North America is the market's structural anchor for the entire forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Asia Pacific represents the highest-potential expansion geography outside North America. China's market is valued at USD 5.5 Billion in 2024 and is forecast to reach USD 35.4 Billion by 2035 at a CAGR of 17.3%. Healthcare digitization across China, India, and Southeast Asian markets is progressing at an earlier stage than the U.S. The primary opportunity lies in foundational RCM platform deployment rather than AI-layer upgrades. Early movers establishing clearinghouse connectivity and billing automation in China will build integration depth that late entrants will struggle to displace.

Key Regions and Countries

North America

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Competitive Landscape

The Healthcare RCM Market is moderately consolidated at the platform layer but fragmented among specialty and regional service providers. A small number of large integrated vendors holding AI-powered, end-to-end platforms dominate hospital and health system contracts. Hundreds of mid-tier managed service and point-solution vendors compete for physician group and ambulatory care accounts below that tier.

Private equity capital is accelerating top-tier consolidation at a pace that compresses the mid-tier vendor population. The USD 8.9 Billion take-private of R1 RCM in November 2024 at a 29% share price premium represents the largest single RCM transaction on record. Simultaneously, Ensemble Health Partners began a dual-track sale and IPO process in October 2025, targeting a valuation of approximately USD 13 Billion with approximately USD 700 Million EBITDA. Waystar reported 22% year-over-year revenue growth in Q1 2026, confirming that top-tier platforms are scaling aggressively while mid-tier vendors face mounting pressure to consolidate or exit.

Technology differentiation is increasingly defined by AI depth rather than feature breadth. As reported by a Waystar and Qualtrics survey of 600 revenue cycle leaders, AI delivered 13 to 37% improvements across claim follow-up, payment accuracy, denial prevention, and workforce efficiency. Vendors embedding clinical language models across documentation, coding, and denial workflows are capturing disproportionate share among large health system buyers. A measurable performance gap is forming between AI-native platforms and legacy operators.

The outsourcing segment is bifurcating between technology-enabled managed services and traditional labor-arbitrage BPO models. Black Book's survey of 11,550 RCM professionals from Q3 2024 to Q2 2025 confirmed that technology-embedded outsourcing vendors are winning contracts at the expense of labor-only service providers. Vendors that cannot demonstrate measurable AI-driven performance improvements are losing renewals to platforms that can quantify denial-rate reduction and net revenue recovery.

Company Profiles

R1 RCM was taken private in a USD 8.9 Billion transaction by TowerBrook Capital Partners and Clayton, Dubilier and Rice in November 2024. Stockholders received USD 14.30 per share, representing a 29% premium to the unaffected closing price. R1 operates as one of the largest end-to-end RCM service providers in U.S. healthcare, with strategic positioning centered on scale-driven managed services for large health systems. The privatization removes short-term earnings pressure and enables R1 to accelerate platform investment through its R37 AI lab. R1 announced a strategic partnership with Sierra in October 2025 to automate approximately 40 Million annual patient and payer calls.

Optum, through its Optum Insight segment, operates the Change Healthcare clearinghouse and Optum360 managed RCM service. Optum Insight generated USD 19.4 Billion in full-year 2025 revenues, recovering 4% year-over-year following the 2024 ransomware disruption. Optum's deployment of proprietary clinical language models across CDI, coding, and compliance workflows positions it as the most vertically integrated AI-RCM operator in the market. No other vendor combines clearinghouse scale, managed services volume, and proprietary AI depth in a single operating structure.

Key Players

- R1 RCM

- Oracle

- Optum, Inc.

- McKesson Corporation

- Change Healthcare

- Experian Information Solutions, Inc.

- GE HealthCare

- Conifer Health Solutions, LLC

- Veradigm LLC

- SSI Group, LLC

- Huron Consulting Group Inc.

- SAP SE

- AGS Health

- TELCOR Inc.

- AdvantEdge Healthcare Solutions

- athenahealth, Inc.

- eClinicalWorks

- Access Healthcare

- Commure

- Aptarro

Supply Chain and Value Chain Analysis

The Healthcare RCM value chain begins at patient access and flows through eligibility verification, insurance confirmation, and prior authorization submission. Clinical documentation, medical coding, claims scrubbing, clearinghouse transmission, payer adjudication, denial management, and final payment posting follow in sequence. Each stage represents a distinct value-creation layer. Failures at any point cascade into downstream revenue loss, making upstream intervention the highest-leverage strategy for protecting net revenue.

Maximum value concentration sits in the claims and denial management layer, where AI-powered automation delivers the most measurable financial return. As reported by HFMA, a hospital deploying AI-based denial prediction tools reduced claim denial rates by 19% within six months. Vendors controlling this layer through proprietary denial-prediction models trained on payer-specific adjudication patterns hold a durable competitive position. Off-the-shelf software cannot replicate that specificity.

The clearinghouse layer represents the highest systemic concentration risk in the RCM value chain. Change Healthcare processed 15 Billion healthcare transactions annually and connected with 1 in 3 U.S. patient records before the February 2024 ransomware attack. A single point of failure disrupted RCM workflows across thousands of providers simultaneously. The structural vulnerability of a value chain dependent on a small number of clearinghouse intermediaries is now a procurement and risk management consideration for every health system.

The outsourced services layer representing 28.75% of sourcing is controlled by managed RCM vendors including Ensemble Health Partners, Optum360, and Access Healthcare. Vendors absorb the full workflow execution burden from provider clients, effectively inserting themselves as the operational layer between provider EHR systems and payer adjudication. Black Book's ranking of top outsourcing vendors confirms that technology-embedded operators are displacing traditional labor-intensive service models. For buyers, the value chain analysis points to a clear procurement priority: integrated platforms spanning patient access through payment posting deliver greater revenue protection than point solutions addressing individual workflow stages.

Regulatory Landscape

The CMS Interoperability and Prior Authorization Final Rule, issued in January 2024, requires payers to implement electronic prior authorization APIs by 2026. The mandate directly forces technology upgrades across both payer and provider RCM infrastructure. Providers that have not yet deployed ePA-compatible platforms face compliance exposure and continued manual PA processing costs. Regulatory-driven RCM modernization is non-discretionary for U.S. hospitals and physician groups operating under this deadline.

Medicare Advantage plan oversight is intensifying through CMS policy action. KFF documented nearly 53 Million prior authorization requests submitted to Medicare Advantage payers in 2024, up from 50 Million in 2023. CMS has signaled continued scrutiny of MA denial practices. More than 80% of contested denials are partially or fully overturned on appeal, a statistic that regulators are using to justify further constraints on MA payer denial behavior.

Cybersecurity regulation is emerging as a distinct compliance layer for RCM vendors. UnitedHealth's disclosed costs of USD 2.457 Billion through Q3 2024 related to the ransomware attack drew congressional and HHS attention to clearinghouse concentration risk. Vendors operating at scale face increasing pressure to demonstrate redundancy, incident response capability, and third-party security certification as conditions of provider contract retention.

The regulatory environment creates a bifurcated competitive dynamic for market participants. Large, well-capitalized vendors can absorb compliance investment in ePA API development, cybersecurity infrastructure, and CMS audit readiness. Smaller RCM service providers and standalone software vendors without resources to meet evolving federal mandates face consolidation pressure. Regulatory complexity is functioning as a barrier to entry that accelerates the platform concentration already underway through private equity activity.

Recent Developments

- February 10, 2026 Omega Healthcare was named a Leader in the 2025 to 2026 IDC MarketScape for U.S. Revenue Cycle Management, recognized for its embedded intelligence and automation capabilities for U.S. healthcare providers.

- March 17, 2026 WELL Health subsidiary WELLSTAR completed two Canadian medical billing acquisitions: PatientSERV in Ontario and Lambert Medico Factures in Quebec, for approximately USD 4.8 Million upfront plus up to USD 6.3 Million in milestone payments, with expected annual revenue of approximately USD 5 Million at approximately 20% EBITDA margin.

- December 17, 2025 Tebra closed USD 250 Million in equity and debt financing led by Hildred Capital, with a debt facility from J.P. Morgan and participation from Toba Capital, Transformation Capital, and HLM Venture Partners, to accelerate AI and automation R&D across its EHR and RCM platform serving more than 140,000 providers.

- June 2025 ACU-Serve, a private equity-backed RCM platform, acquired TANYR Healthcare, an RCM provider focused on the infusion services industry.

- May 2025 Goldman Sachs Alternatives and Everstone Capital sold a co-control stake in Omega Healthcare while retaining significant ongoing stakes in the technology-enabled RCM provider.

- May 16, 2025 Warburg Pincus and Berkshire Partners began exploring a sale of Ensemble Health Partners at up to USD 12 Billion valuation including debt.

Report Scope

| Market Scope & Coverage |

| Market Value (2025) |

USD 200.8 Billion |

| Forecast Revenue (2035) |

USD 806.0 Billion |

| CAGR (2026–2035) |

16.7% |

| Base Year for Estimation |

2025 |

| Historic Period |

2020–2024 |

| Forecast Period |

2026–2035 |

| Report Coverage |

Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered |

By Product/Component (Services, Software), By Type (Integrated, Standalone), By Delivery Mode (Web-Based, Cloud-Based, On-Premise, Hybrid), By Function (Claims and Denial Management, Medical Coding and Billing, Clinical Documentation Improvement, Insurance), By End-User (Hospitals, Physician Offices, Diagnostic Laboratories, Ambulatory Care), By Sourcing (In-house, Outsourced), By Physician Specialty (Others/General Practice, Cardiology, Oncology, Orthopedics) |

| Regional Analysis |

North America – US and Canada; Europe – Germany, France, The UK, Spain, Italy, and Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, and Rest of APAC; Latin America – Brazil, Mexico, and Rest of Latin America; Middle East & Africa – GCC, South Africa, and Rest of MEA |

| Competitive Landscape |

R1 RCM, Oracle, Optum Inc., McKesson Corporation, Change Healthcare, Experian Information Solutions Inc., GE HealthCare, Conifer Health Solutions LLC, Veradigm LLC, SSI Group LLC, Huron Consulting Group Inc., SAP SE, AGS Health, TELCOR Inc., AdvantEdge Healthcare Solutions, athenahealth Inc., eClinicalWorks, Access Healthcare, Commure, Aptarro |

| Customization Scope |

Customization for segments and region or country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options |

Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Frequently Asked Questions

What is the current size of the global Healthcare Revenue Cycle Management Market?

▾ The global Healthcare Revenue Cycle Management Market is valued at USD 200.8 Billion in 2026. The United States accounts for USD 112.3 Billion of that total, making it the single largest national market by a significant margin.

What is the forecast growth rate for the Healthcare RCM Market?

▾ The global market will grow at a CAGR of 16.7% from 2026 to 2035, reaching USD 806.0 Billion by 2035. The U.S. market grows at a comparatively lower CAGR of 12.4%, reflecting its greater maturity relative to emerging markets.

Which product segment leads the Healthcare RCM Market?

▾ Services holds the dominant position with a 69.6% revenue share in 2026. Provider organizations rely on outsourced and managed RCM services to handle billing complexity that internal teams cannot efficiently manage alone.

Which delivery mode is growing fastest in the RCM Market?

▾ Cloud-Based deployment is the forward architecture for advanced RCM platforms, as it supports the AI and clinical language model workloads required for denial prediction and automated coding. Web-Based deployment currently leads with a 56.8% revenue share, but cloud adoption is accelerating as providers upgrade to AI-capable infrastructure.

Which region leads the global Healthcare RCM Market?

▾ North America dominates with a 65.8% revenue share in 2026, driven primarily by the scale and payer complexity of the U.S. healthcare system. No other region approaches this concentration of RCM vendor activity, regulatory mandates, or private equity investment.

Which region offers the fastest growth opportunity in the RCM Market?

▾ Asia Pacific presents the highest international expansion opportunity, anchored by China's market growing at a CAGR of 17.3% from USD 5.5 Billion in 2024 to USD 35.4 Billion by 2035. Provider digitization across China, India, and Southeast Asia is at an earlier stage, creating demand for foundational RCM platform deployment.

Who are the leading companies in the Healthcare RCM Market?

▾ Key players include R1 RCM, Oracle, Optum Inc., McKesson Corporation, Change Healthcare, Experian Information Solutions, GE HealthCare, Conifer Health Solutions, Veradigm, athenahealth, and eClinicalWorks, among others. R1 RCM was taken private in a USD 8.9 Billion transaction in November 2024, marking the largest single RCM vendor acquisition on record.

What are the primary drivers of Healthcare RCM Market growth?

▾ Three structural drivers define current market momentum: generative AI integration across hospital revenue cycles, CMS regulatory mandates requiring electronic prior authorization APIs by 2026, and private equity consolidation of RCM vendors. A Waystar survey confirmed that 100% of healthcare leaders see AI value in RCM and 90% planned to increase technology spend.

What are the biggest challenges facing the Healthcare RCM Market?

▾ Rising prior authorization administrative burden and cybersecurity risk are the two most material challenges. KFF documented nearly 53 Million Medicare Advantage PA requests in 2024. UnitedHealth disclosed USD 2.457 Billion in costs related to the Change Healthcare ransomware attack through Q3 2024, a figure that reshaped vendor risk posture across the entire industry.

Where is the primary investment opportunity in the Healthcare RCM Market?

▾ Post-acute and SNF revenue cycle digitization, middle revenue cycle unification through clinical language models, and Medicare Advantage specialty RCM services represent the clearest underserved segments. Waystar's 2026 revenue guidance of USD 1.274 to 1.294 Billion explicitly includes post-acute expansion as a core growth driver, confirming institutional validation of this white space thesis.