Market Snapshot

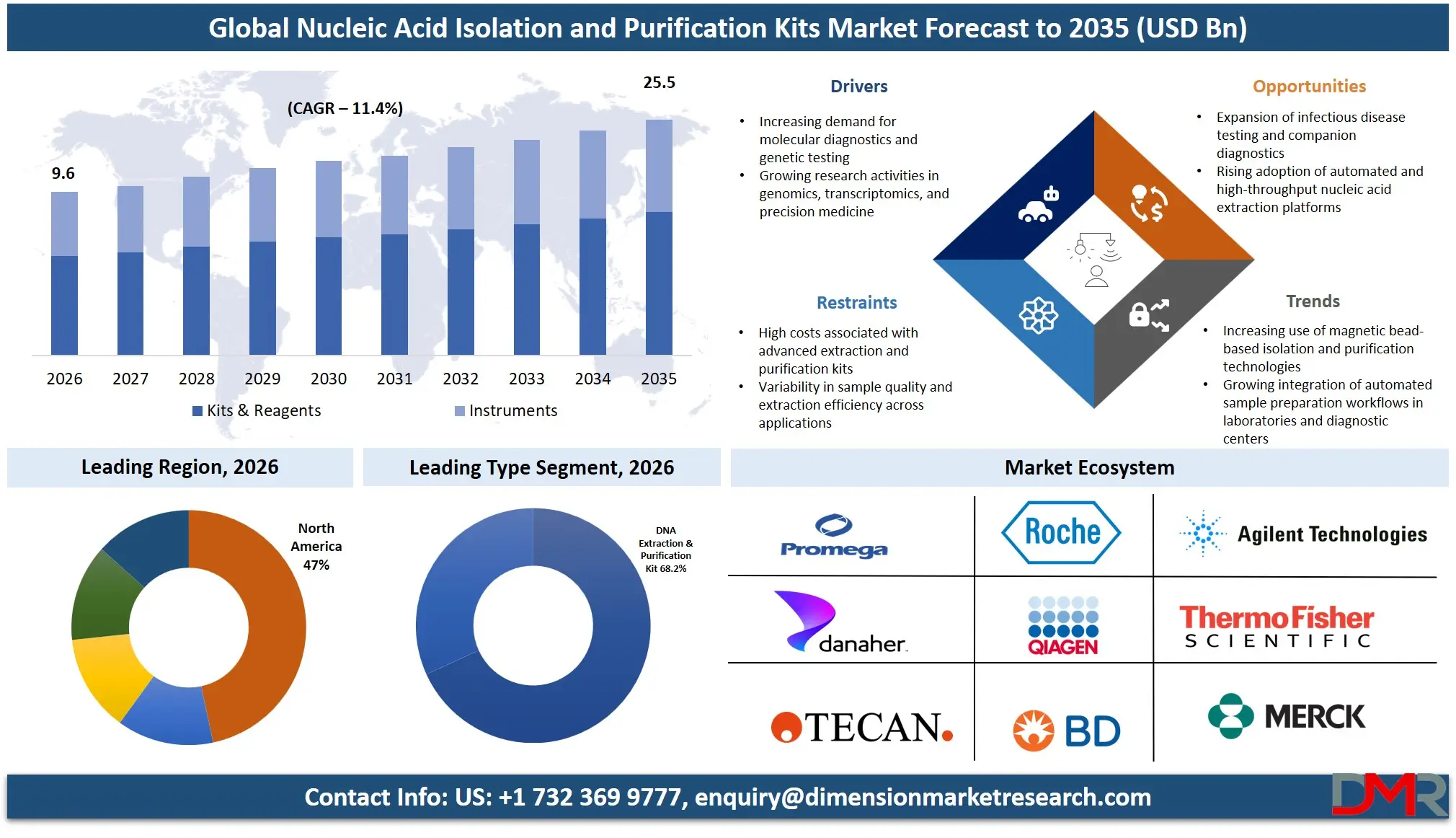

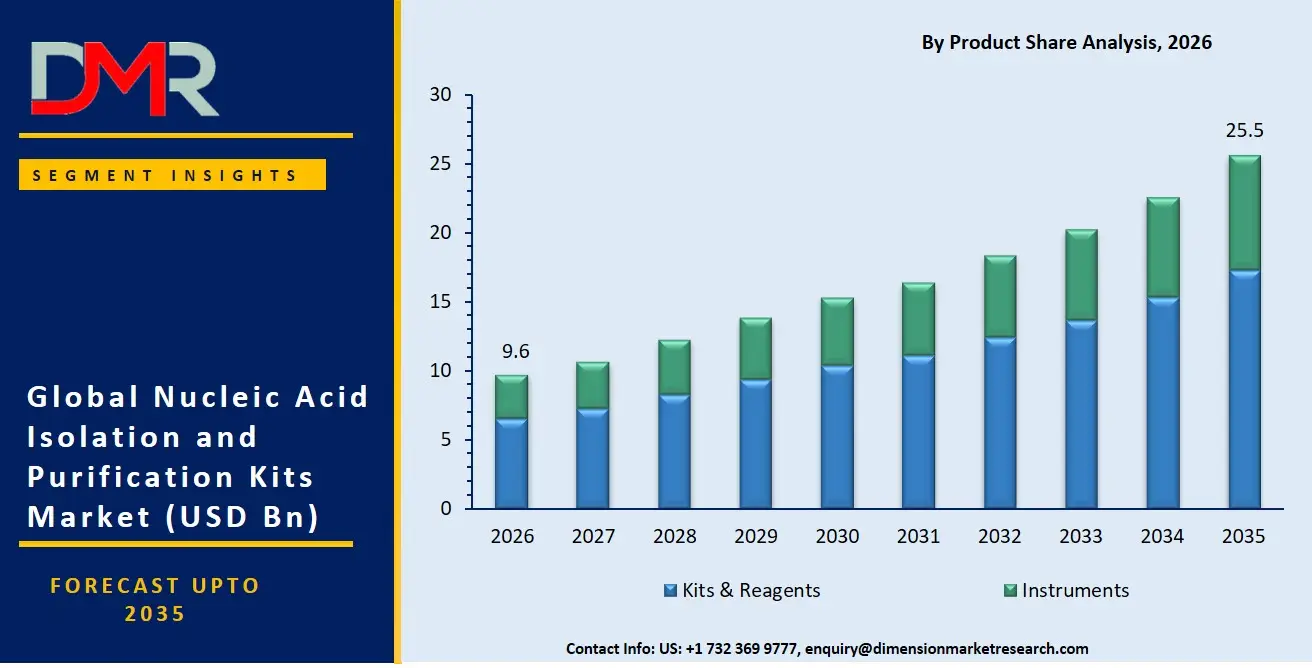

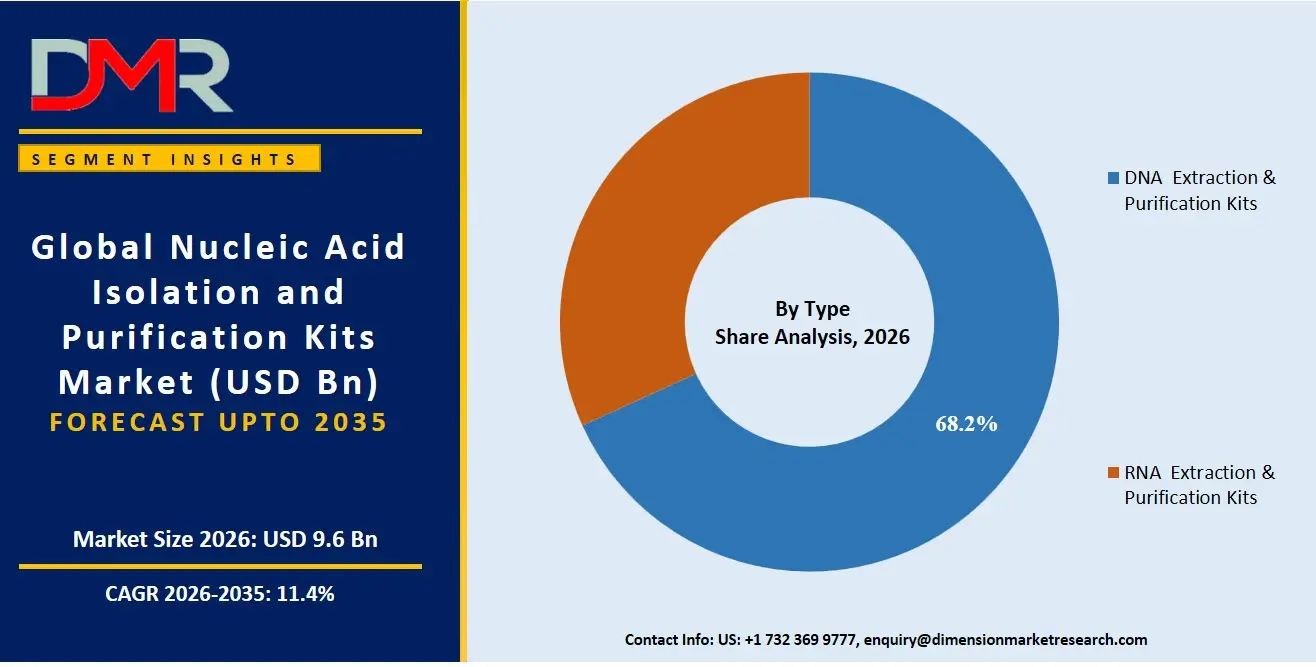

- The global Nucleic Acid Isolation and Purification Kits Market is valued at USD 8.6 Billion in 2025, reached USD 9.6 Billion in 2026, and is projected to hit USD 25.5 Billion by 2035 at a CAGR of 11.4%.

- The US market stands at USD 3.9 Billion in 2026, projected to reach USD 9.3 Billion by 2035 at a CAGR of 9.8%.

- By Product, Kits and Reagents lead with a 67.6% revenue share in 2026.

- By Type, DNA Extraction and Purification Kits dominate with a 68.2% revenue share.

- By Method, Magnetic Beads hold the largest share at 48.3%.

- By End-User, Hospitals and Diagnostic Centers account for 49.2% of revenue.

- Key players include Thermo Fisher Scientific, QIAGEN, F. Hoffmann-La Roche AG, Danaher Corporation, and Merck KGaA.

Market Overview

The nucleic acid isolation and purification kits market covers products and instruments used to extract, isolate, and purify DNA and RNA from biological samples. The market serves laboratories across drug discovery, personalized medicine, diagnostics, and agricultural research. It excludes downstream assay kits such as PCR amplification reagents and sequencing library preparation consumables sold independently. Sample preparation is the foundational step that determines the quality of every downstream result.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

This market operates as the upstream entry point for molecular biology workflows. Every next-generation sequencing run, every liquid biopsy test, and every pathogen surveillance program depends on a reliable nucleic acid extraction step. That structural dependency ties the kits market to multi-sector expansion simultaneously. No single application failure can pull the market into contraction.

The current market reflects a decisive shift away from manual spin-column methods toward automated, high-throughput workflows. Connected sample preparation platforms crossed 1,000 worldwide placements by late 2024. Laboratories committing capital to automation infrastructure lock in recurring reagent-kit purchases for years ahead. That installed-base dynamic makes this a compounding revenue market, not a transactional one.

Market Size and Forecast

The Global Nucleic Acid Isolation and Purification Kits Market size is estimated at USD 9.6 Billion in 2026 from USD 8.6 Billion in 2025, and is projected to reach USD 25.5 Billion by 2035, exhibiting a CAGR of 11.4% during the forecast period.

The forecast rests on two structural assumptions. Automated purification platform placements continue expanding, sustaining recurring reagent-kit attach revenue. Multiomic and liquid biopsy workflows scale from research into clinical settings, requiring validated extraction chemistries at each step. Both assumptions are supported by the 1,000-plus connected instrument placements already confirmed by late 2024. The US alone accounts for USD 3.9 Billion of the 2025 total, confirming North America's outsized influence on global market direction.

China currently advances at a CAGR of 13.2%, the slowest among disclosed markets. Faster-than-expected healthcare infrastructure investment across Asia Pacific could push China's market beyond its baseline USD 10.5 Billion projection by 2035. On the downside, tightening procurement validation requirements in hospital systems could slow clinical channel adoption in the diagnostics segment despite the broader expansion trajectory.

Market Dynamics

Automation and Multiomic Workflows Drive Recurring Kit Demand

Automation is no longer an upgrade option in molecular laboratories. Connected sample preparation platforms surpassed 1,000 worldwide placements by December 2024. Each placement converts a one-time capital purchase into a multi-year recurring revenue stream for extraction kit suppliers. That shift fundamentally changes the demand structure of this market from project-based to subscription-like.

Multiomic next-generation sequencing workflows require integrated DNA and RNA purification chemistries from a single sample. Following May 2024 multiomic library preparation kit launches, laboratories running combined DNA and RNA analyses must use validated extraction kits that preserve both nucleic acid types. This requirement narrows supplier selection and raises switching costs for laboratories already embedded in a platform ecosystem. QIAGEN's QIAcuity digital PCR platform reached more than 2,700 cumulative placements worldwide by end of 2024, creating direct pull-through for extraction kit consumption at scale.

Regulatory Gaps and Infrastructure Limits Cap Clinical Penetration

Multiple nucleic acid extraction kit suppliers confirmed as of May 2025 that none of their molecular extraction kits hold FDA 510(k) clearance or Emergency Use Authorization. Hospitals and clinical laboratories requiring cleared devices face a constrained supplier pool. Procurement gatekeepers applying stricter kit validation requirements compress near-term revenue in the diagnostics end-user segment.

Peer-reviewed research published in July 2024 from Imperial College London documented persistent demand for electricity-free alternatives across 406 clinical respiratory samples. Standard kits require 45 to 60 minutes per extraction cycle and depend on continuous power. Electricity-free alternatives recorded only 77.1% sensitivity in low viral-load samples versus 100% for column-based methods. That sensitivity gap means alternative formats cannot replace conventional kits in clinical diagnostics, keeping low-resource markets structurally underserved.

Instrument Launches and CE-IVD Certification Open New Revenue Channels

Thermo Fisher Scientific launched a sequential protein, DNA, and RNA extraction kit from a single biological sample in February 2026. That product directly addresses specimen scarcity in personalized medicine, where multi-analyte data must be generated from minimal sample volumes. Suppliers that solve this specimen constraint claim a first-mover position in one of the fastest-scaling clinical workflow categories.

Three new automated sample preparation instruments committed for launch across 2025 to 2026 include one capable of processing up to 192 samples per run. Each instrument launch creates a new recurring consumable-kit attach revenue stream. CE-IVD certified one-step extraction chemistries confirmed through 2025 SwiftX-Class Virus Kit launches open European clinical diagnostic procurement channels. European hospitals operating under IVD regulations represent a large installed base of potential clinical customers that previously required multi-step workflows.

Market Trends

Magnetic-Bead Chemistry and Digital PCR Integration Redefine the Extraction Standard

Magnetic-bead chemistry is displacing spin-column workflows as the preferred extraction method across viral nucleic acid recovery applications. The January to April 2025 FDA listings of universal and pathogen magnetic-bead kits under the Class I General Purpose Reagent pathway confirm that suppliers are standardizing on this chemistry. For laboratories evaluating platform decisions now, magnetic-bead compatibility has become a baseline requirement. QIAGEN's QIAcuity platform citations in scientific publications exceeded 550 by January 2025, up from 450 in September 2024, reflecting accelerating research adoption that will feed clinical validation pipelines over the next several years. Suppliers building digital PCR-integrated extraction workflows as end-to-end validated products hold a structural advantage over those still selling standalone kits.

Product Analysis

Kits and Reagents leads the segment with a 67.6% share, reflecting the consumable nature of extraction products. Every sample processed requires a fresh kit. That non-discretionary repeat purchase cycle sustains revenue independent of new instrument sales and insulates this segment from capital expenditure freezes that periodically affect instrument procurement budgets.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Type Analysis

DNA Extraction and Purification Kits accounts for 68.2% of the segment, driven by the broadest application base of any nucleic acid category. DNA extraction underpins genomic sequencing, liquid biopsy, agricultural research, and forensic diagnostics simultaneously. No other sub-segment serves that range of end-markets, which is why DNA kits generate the highest volume across virtually every end-user category in this market.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Method Analysis

With a 48.3% share, Magnetic Beads holds the strongest position due to direct compatibility with automated liquid handling systems. Magnetic bead chemistry enables hands-free, high-throughput nucleic acid extraction at scale. The January to April 2025 FDA listings of multiple magnetic-bead kits under the Class I pathway confirm this method's expanding regulatory footprint and its position as the extraction standard for high-volume laboratory settings.

End-User Analysis

Hospitals and Diagnostic Centers leads the segment with a 49.2% share, reflecting the continuous extraction throughput that clinical laboratories generate across infectious disease testing, oncology panels, and genetic screening programs. No other end-user category matches the per-facility kit consumption volume of hospital systems. QIAGEN's full-year 2025 net sales of approximately USD 2.09 Billion CER reflect the sustained commercial throughput that this captive, high-volume buyer segment generates.

Key Market Segments

By Product

- Kits and Reagents

- Instruments

By Type

- DNA Extraction and Purification Kits

- RNA Extraction and Purification Kits

By Method

- Magnetic Beads

- Column-Based / Silica Membrane

- Reagent-Based

By Sample Type

- Whole Blood Cells

- Tissue

- Cells

- Plasma/Serum

By Application

- Drug Discovery and Development

- Diagnostics

- Agriculture and Animal Research

- Personalized Medicine

By End-User

- Hospitals and Diagnostic Centers

- Academic and Research Institutes

- Pharmaceutical and Biotechnology Companies

Regional Analysis

North America holds the dominant position in this market. The US alone was valued at USD 3.9 Billion in 2025 and is forecast to reach USD 9.3 Billion by 2035 at a CAGR of 9.8%. The US concentration of pharmaceutical companies, academic research institutions, and hospital diagnostic networks creates the highest per-capita extraction kit consumption of any region. Any pricing or regulatory shift in the US market reverberates across the global forecast. North America's structural lead compounds through the forecast period because its installed base of automated platforms generates recurring consumable revenue that newer markets cannot yet match.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Asia Pacific presents the highest upside potential despite China's baseline CAGR of 13.2%. Public health pathogen surveillance investment and expanding hospital infrastructure are creating demand for magnetic-bead viral extraction kits across diverse sample matrices. Faster-than-expected healthcare investment could push China's market beyond its USD 10.5 Billion projection by 2035.

Key Regions and Countries

North America

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Competitive Landscape

The market operates as a consolidated-at-the-top, fragmented-in-the-middle structure. A small number of established platform suppliers control the largest share of installed-base placements and kit attach revenue. The competitive center of gravity has shifted from kit chemistry alone to integrated platform ecosystems. Suppliers combining automated instruments with validated extraction kits and digital workflow software hold a structurally different position than pure-kit suppliers. A May 2025 acquisition valued at USD 70 Million in cash plus up to USD 10 Million in milestone payments brought an AI-powered clinical genomics platform into a major supplier's portfolio, connecting nucleic acid extraction directly to clinical interpretation software.

Companies competing solely on extraction kit price or chemistry face a narrowing window. The market structurally rewards suppliers that offer extraction as part of a broader sample-to-answer workflow. A patent dispute settlement and cross-licensing agreement concluded in full-year 2023 signals that IP boundaries around extraction-to-detection workflows are actively contested. Mid-tier suppliers face both licensing cost risk and barriers to developing integrated workflow products. New entrants must define a defensible niche through sample type specialization, regulatory certification, or environmental monitoring applications to avoid margin compression.

Company Profiles

QIAGEN N.V. anchors its competitive position on the depth of its sample technology ecosystem, serving more than 500,000 customers globally across more than 35 locations with approximately 5,700 employees as of December 2025. Its Sample Technologies pillar delivered USD 1.49 Billion CER in full-year 2025 sales with 8% CER growth. That platform model, where instrument placements and kit attach revenue reinforce each other across every product generation, creates a compounding commercial advantage that pure-kit competitors cannot replicate without equivalent installed-base scale.

Thermo Fisher Scientific competes through breadth of product portfolio and speed of innovation across extraction chemistries and sample types. Its August 2025 release of a high molecular weight DNA kit for long-read sequencing shows a strategy of anticipating workflow requirements before customers formally articulate them. That first-mover positioning in emerging application segments creates commercial pull before competitors have comparable products available, making Thermo Fisher a structurally proactive player rather than a reactive one.

Key Players

- QIAGEN N.V.

- Thermo Fisher Scientific

- F. Hoffmann-La Roche AG

- Danaher Corporation

- Merck KGaA

- Agilent Technologies

- Bio-Rad Laboratories Inc.

- Illumina Inc.

- Promega Corporation

- Takara Bio Inc.

- PerkinElmer

- New England Biolabs

- LGC Limited

- Norgen Biotek Corp

- MACHEREY-NAGEL GmbH

- Abcam plc

- AutoGen Inc.

- Bioneer Corporation

- Meridian Bioscience

Supply Chain and Value Chain Analysis

The supply chain flows from raw material suppliers producing silica membranes, magnetic bead substrates, lysis buffer chemical inputs, and plastic consumable components through kit manufacturers to distributors and finally to end-users. Maximum value concentrates at the kit formulation and validation stage. Suppliers that develop and validate extraction chemistries for specific sample types command premium pricing because validated performance data cannot be replicated quickly by competitors. Suppliers controlling both the instrument and the validated consumable kit exercise the strongest buyer-supplier dynamic. End-users locked into platform-compatible kits have limited negotiating leverage on reagent pricing.

The biggest supply chain risk sits at the distribution and logistics layer, particularly for cold-chain-dependent reagent kits. Hospitals and diagnostic centers in resource-limited settings face consistent supply disruptions. The July 2024 peer-reviewed validation of an electricity-free extraction kit across 406 clinical samples reflects real supply chain pressure, not a research novelty. Instrument manufacturing represents a capital-intensive node that only scale players can sustain. Three new automated sample preparation instruments committed for 2025 to 2026 launch require significant engineering and regulatory investment. Suppliers that clear this capital hurdle create a self-reinforcing cycle where instruments generate reagent attach revenue that funds the next instrument generation.

Regulatory Landscape

Multiple nucleic acid extraction kit suppliers confirmed as of May 2025 that none of their molecular extraction kits hold FDA 510(k) clearance or Emergency Use Authorization. The industry relies on Class I General Purpose Reagent exemptions. Hospitals and clinical laboratories requiring cleared devices face a constrained supplier pool, creating compliance risk for procurement teams operating under cleared-device requirements. This is not a temporary gap. It reflects a structural regulatory positioning choice that limits clinical channel penetration for the majority of suppliers in this market.

Europe operates under IVD regulations where CE-IVD certification determines procurement eligibility. The 2025 launch of SwiftX-Class Virus Kits with CE-IVD certification opens European hospital procurement channels. Suppliers with certified one-step chemistries hold a direct commercial advantage over uncertified competitors. CE-IVD certification functions as a market access gate in Europe, not a quality signal. Suppliers without it are structurally excluded from European clinical diagnostic procurement regardless of product performance.

Recent Developments

- January 2025: QIAGEN N.V. Instrument Milestone. QIAcuity digital PCR platform reached more than 2,700 cumulative worldwide placements, up from more than 2,000 at end of 2023.

- February 2026: QIAGEN N.V. Financial Results. Sample Technologies pillar delivered USD 1.49 Billion CER in full-year 2025 sales with 8% CER growth.

- December 2025: QIAGEN N.V. Acquisition. Closing of Parse Biosciences acquisition, signaling commercial commitment to single-cell sample preparation as a distinct investable sub-segment.

- August 2025: Thermo Fisher Scientific. Product Launch. Released a high molecular weight DNA kit targeting long-read sequencing workflows.

- May 2025: Undisclosed Supplier. Acquisition. AI-powered clinical genomics platform acquired for USD 70 Million cash plus up to USD 10 Million in milestone payments.

Report Details

| Report Characteristics |

| Market Value (2025) |

USD 8.6 Billion |

| Market Value (2026) |

USD 9.6 Billion |

| Forecast Revenue (2035) |

USD 25.5 Billion |

| CAGR (2026 to 2035) |

11.4% |

| Base Year for Estimation |

2025 |

| Historic Period |

2020 to 2024 |

| Forecast Period |

2026 to 2035 |

| Report Coverage |

Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered |

By Product (Kits and Reagents, Instruments), By Type (DNA Extraction and Purification Kits, RNA Extraction and Purification Kits), By Method (Magnetic Beads, Column-Based / Silica Membrane, Reagent-Based), By Sample Type (Whole Blood Cells, Tissue, Cells, Plasma/Serum), By Application (Drug Discovery and Development, Diagnostics, Agriculture and Animal Research, Personalized Medicine), By End-User (Hospitals and Diagnostic Centers, Academic and Research Institutes, Pharmaceutical and Biotechnology Companies) |

| Regional Analysis |

North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape |

QIAGEN N.V., Thermo Fisher Scientific, F. Hoffmann-La Roche AG, Danaher Corporation, Merck KGaA, Agilent Technologies, Bio-Rad Laboratories Inc., Illumina Inc., Promega Corporation, Takara Bio Inc., PerkinElmer, New England Biolabs, LGC Limited, Norgen Biotek Corp, MACHEREY-NAGEL GmbH, Abcam plc, AutoGen Inc., Bioneer Corporation, Meridian Bioscience |

| Customization Scope |

Customization for segments and region or country level will be provided. Additional customization can be done based on requirements. |

| Purchase Options |

Three license options: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |

Frequently Asked Questions

What is the biggest investment opportunity Nucleic Acid Isolation and Purification Kits Market market?

▾ Automated high-throughput sample preparation represents the clearest investment opportunity. Three new instruments launching across 2025 to 2026 include one capable of processing up to 192 samples per run, each generating a new recurring consumable-kit attach revenue stream. Suppliers that clear the capital hurdle to build and place instruments create a compounding revenue model that pure-kit competitors cannot access.

Who are the top companies Nucleic Acid Isolation and Purification Kits Market ?

▾ QIAGEN N.V. and Thermo Fisher Scientific lead the market through integrated platform ecosystems that combine automated instruments, validated extraction kits, and digital workflow software. QIAGEN serves more than 500,000 customers globally. Both companies compete through breadth of portfolio and speed of innovation rather than kit chemistry alone.

Which segment is growing fastest and why in Nucleic Acid Isolation and Purification Kits Market ?

▾ Plasma and serum extraction is the most compliance-intensive and fastest-scaling sample type sub-segment, driven by liquid biopsy companion diagnostic adoption. Magnetic Beads hold a 48.3% method share and are the extraction chemistry of choice for plasma workflows. Suppliers with validated plasma extraction chemistries hold a structural advantage as liquid biopsy moves from research into clinical settings.

Which region is growing fastest in Nucleic Acid Isolation and Purification Kits Market and why?

▾ Asia Pacific presents the highest upside potential despite China's baseline CAGR of 13.2%. Public health pathogen surveillance investment and expanding hospital infrastructure are creating demand for magnetic-bead viral extraction kits across diverse sample matrices. Faster-than-expected healthcare investment could push China's market beyond its USD 10.5 Billion projection by 2035.

What is the biggest challenge holding Nucleic Acid Isolation and Purification Kits Market back?

▾ The absence of FDA 510(k) clearance across the majority of suppliers' molecular extraction kit portfolios, confirmed as of May 2025, is the single largest structural barrier to clinical channel expansion. Hospitals operating under cleared-device procurement requirements face a constrained supplier pool. Until suppliers pursue clearance, the diagnostics end-user segment remains structurally under-penetrated relative to its addressable size.