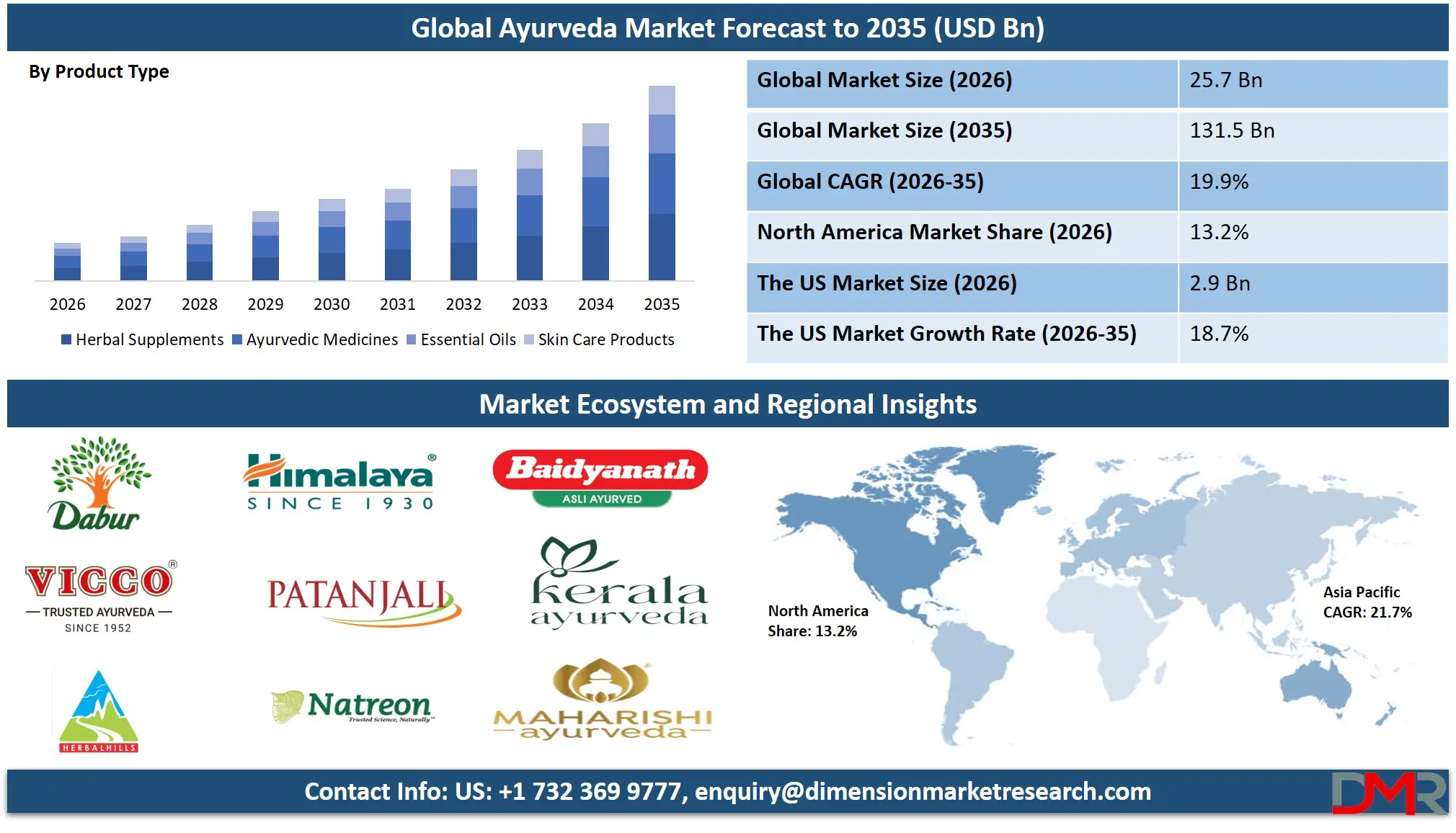

Market Overview

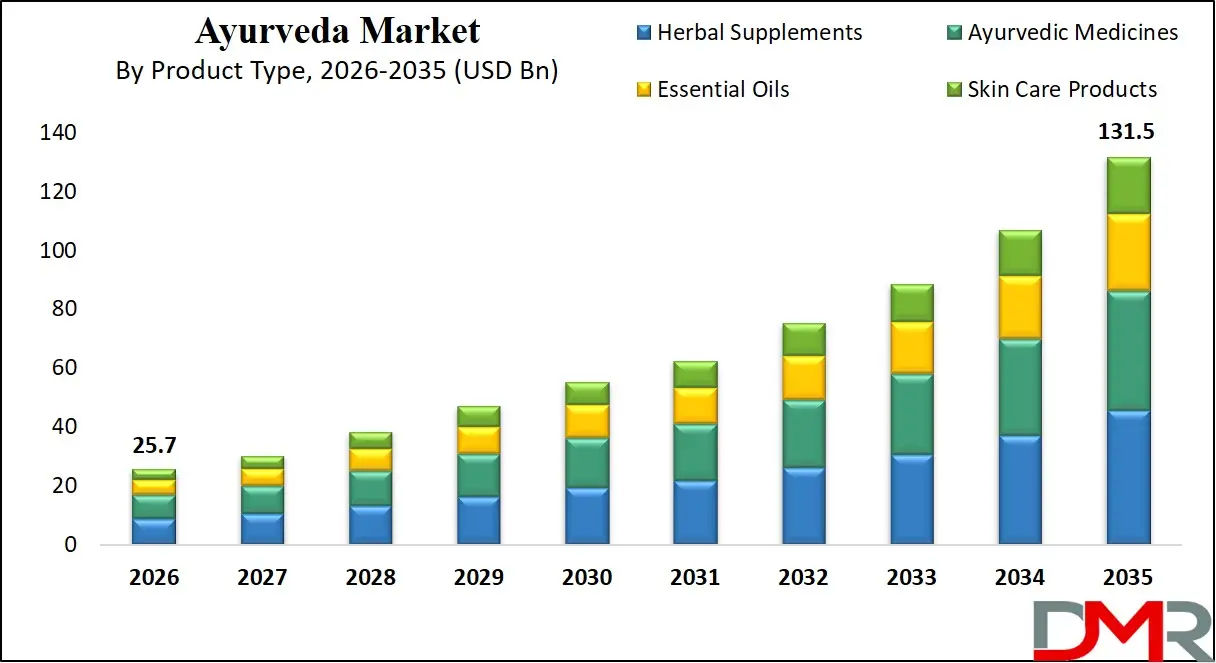

The Global Ayurveda Market is projected to reach USD 25.7 billion in 2026 and grow at a compound annual growth rate of 19.9% from there until 2035 to reach a value of USD 131.5 billion.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Ayurveda is a traditional system of medicine that originated in India thousands of years ago, focusing on holistic wellness through balancing the body, mind, and spirit. It utilizes herbal formulations, herbomineral compounds, and mineral-based preparations derived from natural sources such as plants, metals, and minerals. Ayurvedic products include herbal supplements, medicines, essential oils, and skin care items designed to prevent and manage various health conditions while promoting overall well-being. The approach emphasizes personalized treatments based on individual constitution and lifestyle factors.

Growing consumer preference for natural and organic products, rising awareness about preventive healthcare, and increasing scientific validation of traditional remedies are accelerating global adoption of Ayurveda. Improvements in manufacturing standards, quality control processes, and product standardization are enhancing credibility and consumer trust. Government initiatives promoting traditional medicine systems, favorable regulatory frameworks in key markets, and growing integration with mainstream healthcare are further driving demand. The sector is gradually transitioning from unorganized local markets to organized retail, e-commerce platforms, and institutional sales channels.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Recent developments include strategic collaborations between traditional Ayurvedic manufacturers and modern pharmaceutical companies, expansion of product portfolios to include evidence-based formulations, and investments in clinical research to validate therapeutic efficacy. Digital health platforms and telemedicine services are broadening consumer access to Ayurvedic consultations and products. Investments in sustainable sourcing and fair-trade practices are strengthening supply chain resilience, while stricter quality regulations are encouraging adoption of Good Manufacturing Practices and standardized extraction technologies.

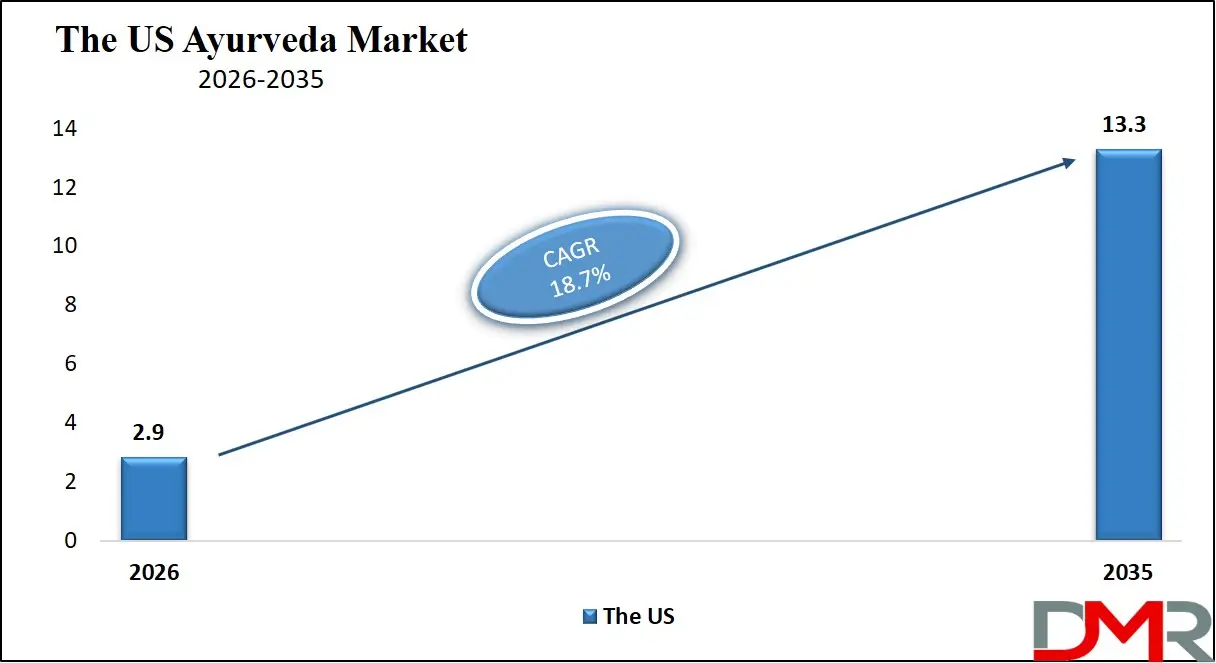

The US Ayurveda Market

The US Ayurveda Market is projected to reach USD 2.9 billion in 2026 at a compound annual growth rate of 18.7% over its forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US Ayurveda landscape is shaped by growing consumer interest in holistic health, wellness tourism, and integrative medicine approaches. Rising prevalence of lifestyle disorders such as stress, anxiety, and digestive issues drives demand for natural alternatives to conventional treatments. The presence of a large yoga and meditation community supports awareness and acceptance of Ayurvedic principles. Regulatory recognition of Ayurvedic products as dietary supplements under the Dietary Supplement Health and Education Act facilitates market entry. E-commerce platforms and specialty wellness retailers are expanding product accessibility. However, variability in product quality and limited practitioner training programs influence adoption rates. Strong consumer spending on preventive healthcare and natural personal care products supports steady expansion across major metropolitan areas.

The Europe Ayurveda Market

The Europe Ayurveda Market is estimated to be valued at USD 2.1 billion in 2026 and is further anticipated to reach USD 8.5 billion by 2035 at a CAGR of 18.0%.

Europe demonstrates mature adoption supported by growing wellness tourism, established naturopathy networks, and increasing integration of traditional medicine systems. Countries such as Germany, the United Kingdom, and the Netherlands lead in Ayurvedic product consumption and professional training programs. Strict regulations under the European Traditional Herbal Medicinal Products Directive ensure product safety and quality standards. Rising consumer awareness about side effects of synthetic drugs and interest in preventive healthcare strengthen demand. Eastern European nations are witnessing growing interest in natural medicine alternatives. High sustainability standards for herbal sourcing and fair-trade certifications shape market access. Technological innovation in standardized extracts and hybrid wellness solutions accelerates regional market penetration.

The Japan Ayurveda Market

The Japan Ayurveda Market is projected to be valued at USD 0.8 billion in 2026. It is further expected to witness subsequent growth in the upcoming period, holding USD 3.1 billion in 2035 at a CAGR of 16.5%.

Japan's Ayurveda sector is expanding under growing interest in traditional medicine systems and preventive healthcare approaches. The country's aging population and high healthcare expenditure create demand for natural solutions for age-related conditions. Strong consumer appreciation for traditional wellness practices, including Kampo medicine, provides cultural receptivity to Ayurvedic principles. Government initiatives promoting preventive healthcare and healthy aging support market growth. Urban wellness centers and luxury spas increasingly incorporate Ayurvedic treatments. However, regulatory requirements for health claims and product registration present market entry considerations. Technological sophistication and demand for premium, scientifically validated products provide competitive opportunities for established manufacturers and wellness brands. The market demonstrates strong growth potential as consumer awareness increases and distribution channels expand.

Global Ayurveda Market: Key Takeaways

- Strong Global Market Growth Outlook: The Global Ayurveda Market is expected to be valued at USD 25.7 billion in 2026 and is projected to reach USD 131.5 billion by 2035, showcasing rapid expansion supported by rising demand for natural wellness solutions and preventive healthcare approaches.

- High CAGR Driven by Wellness Adoption: The market is expected to grow at an impressive CAGR of 19.9% from 2026 to 2035, fueled by accelerating lifestyle disease prevalence, increasing consumer preference for organic products, and growing awareness of traditional medicine systems worldwide.

- Strong Growth Trajectory in the United States: The U.S. Ayurveda Market stands at USD 2.9 billion in 2026 and is projected to reach USD 13.3 billion by 2035, expanding at a CAGR of 18.7% due to high wellness awareness, established natural products retail infrastructure, and growing integrative medicine acceptance.

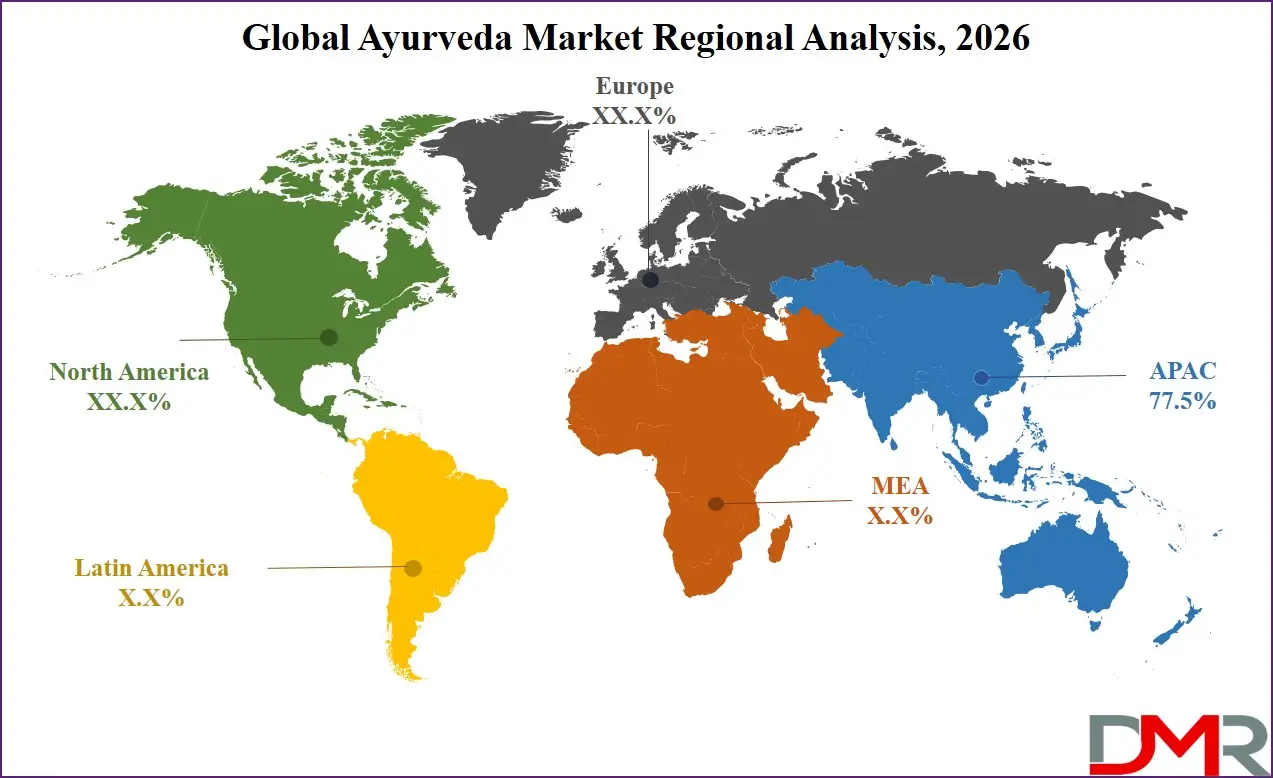

- Regional Dominance: Asia-Pacific is expected to capture approximately 77.5% of the global market share in 2026, supported by traditional medicine heritage, large consumer base, favorable regulatory frameworks, and concentration of leading Ayurvedic manufacturers in India and surrounding regions.

- Rapid Advancement in Product Technologies: Innovations including standardized phytochemical extraction techniques, novel delivery formats, quality certification protocols, and scientifically validated formulations are significantly improving product efficacy and consumer confidence in Ayurvedic products.

- Growing Disease Prevalence Boosts Adoption: Rising global incidence of lifestyle disorders affecting over 60% of adult populations in developed countries, coupled with growing side-effect concerns with conventional medicines and expanding access to traditional healthcare, is driving sustained demand for high-quality Ayurvedic formulations.

Global Ayurveda Market: Use Cases

- Lifestyle Disease Management: Healthcare practitioners use Ayurvedic formulations for managing diabetes, hypertension, obesity, and metabolic disorders through personalized dietary supplements and herbal medicines that address root causes while minimizing side effects.

- Immunity Enhancement Programs: Wellness centers and households utilize Ayurvedic immunity-boosting formulations, including Chyawanprash and herbal decoctions, particularly during seasonal changes and pandemic situations to strengthen natural defense mechanisms.

- Digestive Health Support: Ayurvedic medicines including triphala, hingvashtak, and digestive tablets are widely used for managing indigestion, acid reflux, bloating, and maintaining gastrointestinal health in both clinical and home settings.

- Stress and Mental Wellness: Adaptogenic herbs including ashwagandha, brahmi, and jatamansi are incorporated into daily wellness routines for managing stress, anxiety, sleep disorders, and cognitive decline in increasingly stressed urban populations.

- Skin and Hair Care Applications: Natural personal care products containing Ayurvedic herbs such as neem, turmeric, aloe vera, and amla are used for daily skincare, hair care, and management of dermatological conditions without harsh chemical exposure.

Global Ayurveda Market: Stats & Facts

World Health Organization (WHO)

- Approximately 80% of the global population relies on traditional medicine for primary healthcare needs in developing countries.

- Traditional medicine systems, including Ayurveda, are used by over 170 member states worldwide.

- WHO established the Global Centre for Traditional Medicine in India in 2022 to strengthen evidence base and regulatory frameworks.

- Traditional medicine is the first line of treatment for over 60% of the world's population.

Ministry of AYUSH, Government of India

- India has over 400,000 registered Ayurveda practitioners and more than 3,000 Ayurveda hospitals.

- Ayurveda exports reached approximately USD 550 million in fiscal year 2024.

- Over 9,000 Ayurveda manufacturing units are licensed in India.

- The government has established 50+ research institutes dedicated to Ayurveda and traditional medicine.

National Center for Complementary and Integrative Health (NCCIH)

- Approximately 23% of U.S. adults have used complementary health approaches including Ayurveda.

- Yoga and meditation, often associated with Ayurveda, are practiced by over 35 million Americans.

- Consumer spending on natural products in the U.S. exceeds USD 40 billion annually.

- Over 50% of U.S. medical schools now offer courses in complementary and integrative medicine.

European Federation of Complementary and Integrative Medicine

- Approximately 25% of EU citizens have used traditional or complementary medicine.

- Germany has over 60,000 non-medical practitioners offering complementary therapies.

- The European herbal supplement market exceeds EUR 7 billion annually.

- Over 100 million Europeans use herbal medicinal products.

Japan Ministry of Health, Labour and Welfare

- Traditional medicine systems are integrated into Japan's national healthcare system with over 20,000 Kampo practitioners.

- Kampo medicines, similar to Ayurveda in principle, are prescribed by 90% of Japanese physicians.

- The Japanese traditional medicine market exceeds USD 2 billion annually.

- Over 200 Kampo formulations are covered by national health insurance.

Global Ayurveda Market: Market Dynamic

Driving Factors in the Global Ayurveda Market

Rising Global Lifestyle Disease Burden and Shift to Preventive Healthcare

The increasing prevalence of lifestyle disorders worldwide, driven by sedentary lifestyles, dietary changes, environmental factors, and rising stress levels, represents the primary market driver. Chronic conditions including diabetes affecting over 500 million adults globally, cardiovascular diseases, digestive disorders, and mental health challenges are prompting individuals to seek natural, preventive healthcare alternatives. Additionally, growing awareness of side effects associated with long-term conventional medication use drives demand for safer therapeutic options. As scientific validation of Ayurvedic approaches expands and consumer trust in traditional medicine grows, the volume of Ayurvedic product consumption continues to rise steadily.

Expanding Government Support and International Recognition

Government initiatives promoting traditional medicine systems and WHO recognition of Ayurveda significantly boost market growth. Countries including India, Nepal, Sri Lanka, and Bangladesh have established dedicated ministries and regulatory frameworks for Ayurveda. In Western markets, growing acceptance of complementary medicine, FDA recognition of certain traditional ingredients as Generally Recognized as Safe (GRAS), and EU traditional herbal registration pathways create accessible market entry routes. These institutional support mechanisms reduce regulatory barriers, making Ayurvedic products accessible to broader populations and subsequently increasing demand across all product categories.

Restraints in the Global Ayurveda Market

Standardization Challenges and Quality Consistency Issues

Despite growing acceptance, the lack of uniform quality standards across manufacturing units remains a significant barrier, particularly in export markets with stringent regulatory requirements. Variability in raw material quality, extraction methods, and finished product composition affects therapeutic consistency and consumer confidence. Heavy metal contamination concerns, adulteration risks, and absence of standardized phytochemical markers for many formulations create regulatory hurdles in developed markets. Furthermore, establishing GMP compliance and obtaining international certifications increases production costs, potentially limiting competitiveness against conventional supplements.

Stringent Regulatory Approvals and Documentation Requirements

Ayurvedic products face complex regulatory pathways in international markets, requiring substantial documentation of safety, quality, and efficacy. In the U.S., products may be regulated as dietary supplements, requiring compliance with cGMP regulations and DSHEA requirements. In the EU, traditional herbal registration demands bibliographic evidence of 30 years traditional use including 15 years in the EU. These regulatory pathways require significant investment in documentation, testing, and quality systems, creating barriers for smaller manufacturers. Additionally, divergent requirements across regions complicate global market access strategies and impose ongoing compliance burdens on manufacturers.

Opportunities in the Global Ayurveda Market

Expansion into Emerging Wellness Markets

Emerging markets in Latin America, Middle East, Africa, and Southeast Asia represent significant growth opportunities due to rising healthcare expenditure, growing wellness tourism, and increasing awareness of traditional medicine systems. Countries including Brazil, UAE, South Africa, and Malaysia are developing regulatory frameworks for traditional medicines and attracting wellness tourists seeking authentic Ayurvedic experiences. Localized distribution partnerships, region-specific regulatory strategies, and culturally adapted marketing approaches can improve accessibility in these high-growth potential markets.

Scientific Validation and Product Innovation

Continuous advancement in research methodologies creates opportunities for evidence-based product development and premium positioning. Clinical studies demonstrating efficacy in specific indications, standardization of active compounds, and development of novel delivery formats including nano-formulations and sustained-release technologies enhance product differentiation. Manufacturers investing in research collaborations, quality certifications, and clinically validated formulations can capture market share among healthcare providers and informed consumers prioritizing therapeutic outcomes.

Trends in the Global Ayurveda Market

Premiumization and Certification-Driven Purchasing

The shift toward certified, authenticated, and premium Ayurvedic products represents an established trend driven by quality-conscious consumers and regulatory requirements. Organic certifications, non-GMO verification, heavy metal testing reports, and GMP compliance markings increasingly influence purchasing decisions. This trend aligns with broader consumer emphasis on transparency and traceability in natural products and has become standard practice for reputable Ayurvedic brands targeting international markets.

Integration with Digital Health Platforms

Modern Ayurvedic products and services are increasingly integrated with digital health platforms, telemedicine consultations, and personalized wellness applications. Mobile apps offering dosha assessments, personalized product recommendations, and consultation with Ayurvedic practitioners facilitate consumer engagement and treatment adherence. This trend supports the growing preference for personalized, technology-enabled healthcare and enhances accessibility of Ayurvedic expertise beyond traditional geographical boundaries.

Global Ayurveda Market: Research Scope and Analysis

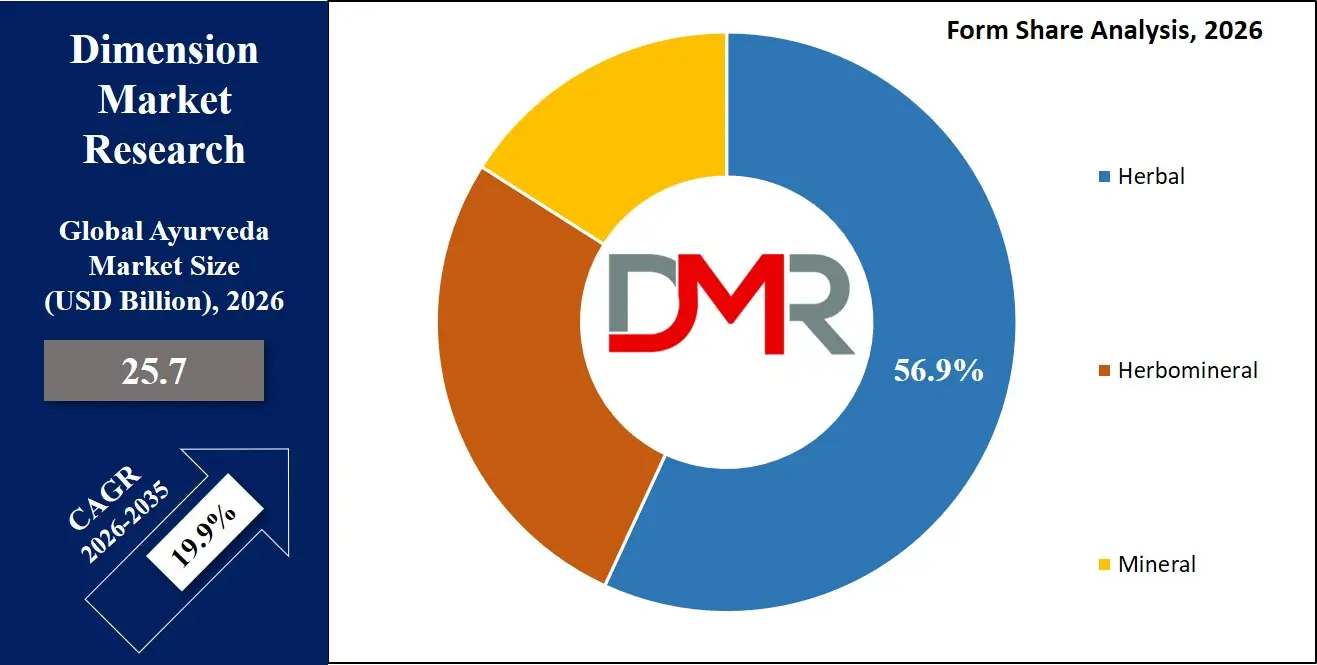

By Form Analysis

Herbal formulations are projected to dominate the global Ayurveda market due to their widespread acceptance, traditional familiarity, and extensive product range spanning medicines, supplements, and personal care items. These products consist entirely of plant-based ingredients processed according to classical Ayurvedic texts or modern extraction methods while maintaining botanical integrity. Because herbal formulations align closely with consumer expectations of "natural" products, they enjoy higher acceptance among first-time users and health-conscious consumers seeking plant-based alternatives. In most wellness categories, consumers prefer purely herbal products when addressing general wellness concerns, which represents the largest volume segment of Ayurvedic consumption. Their relatively simpler manufacturing processes and regulatory pathways also contribute to higher adoption, making them more accessible for manufacturers operating under varying quality standards.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Additionally, herbal formulations often provide sufficient therapeutic benefits for common indications such as digestive health, immunity enhancement, and stress management, reducing the need for complex herbomineral combinations that require specialized manufacturing expertise. Since wellness awareness has been increasing globally due to rising health consciousness, lifestyle disorders, and growing acceptance of traditional medicine, demand for reliable and safe herbal products has grown significantly. Herbal formulations, therefore, remain the preferred option across mainstream retail channels and e-commerce platforms. Herbomineral and mineral preparations (bhasma) are primarily used in chronic disease management under professional supervision, but these procedures represent a smaller proportion of total Ayurvedic consumption. As a result, herbal formulations continue to hold the largest market share within the form segment and are expected to remain dominant due to their accessibility, affordability, and consumer familiarity.

By Product Type Analysis

Among different product categories, herbal supplements are anticipated to dominate the Ayurveda market due to their versatility, ease of integration into daily wellness routines, and growing consumer preference for preventive healthcare. In modern wellness practices, product format plays a critical role in consumer adoption, compliance, and perceived convenience. Herbal supplements, including capsules, tablets, powders, and liquid extracts, provide a standardized dosage form that appeals to contemporary consumers accustomed to convenient health products. Wellness consumers commonly prefer this format because it offers precise dosing, longer shelf life, and easy integration with existing supplement regimens. Compared with traditional formulations requiring preparation, such as decoctions or powders, supplements offer greater convenience for urban consumers with busy lifestyles.

At the same time, they deliver consistent phytochemical content through standardized extraction processes, addressing quality concerns prevalent in the Ayurvedic market. Because preventive health maintenance often involves daily consumption over extended periods, product convenience is an important factor influencing consumer choice. Herbal supplements have therefore become the primary entry point for new consumers exploring Ayurveda and remain the preferred format for established users seeking maintenance wellness. Their compatibility with modern retail formats, including pharmacy chains and online marketplaces, further supports widespread adoption. While traditional Ayurvedic medicines continue to serve therapeutic applications under clinical supervision, the overall consumer convenience and market accessibility of herbal supplements have established them as the dominant product segment.

By Indication Analysis

Reproductive system health is projected to dominate the indication segment of the Ayurveda market due to rising concerns regarding fertility, sexual wellness, and age-related reproductive decline across global populations. Ayurveda offers comprehensive approaches to reproductive health through specialized formulations addressing both male and female reproductive function, hormonal balance, and vitality. Fertility specialists and Ayurvedic practitioners commonly recommend these formulations because they address underlying factors affecting reproductive health without the side effects associated with conventional hormonal interventions. The increasing prevalence of infertility affecting approximately 15% of reproductive-aged couples globally, delayed parenthood trends, and growing awareness of male factor infertility have significantly expanded the addressable market for reproductive health formulations.

Another important factor supporting dominance of this segment is the strong traditional credibility of Ayurvedic reproductive tonics and rejuvenatives including Ashwagandha, Shatavari, Kapikacchu, and Gokshura, which have documented traditional use spanning centuries. The social sensitivity surrounding reproductive health issues often leads consumers to prefer natural alternatives perceived as safer for long-term use compared with conventional pharmaceuticals. Additionally, the aging global population seeking to maintain vitality and reproductive wellness into later decades further expands market potential. While lifestyle diseases including diabetes and cardiovascular conditions represent growing indications for Ayurvedic intervention, reproductive health maintains the largest share due to deeply established traditional positioning, cultural acceptance across regions, and expanding awareness of natural fertility support options.

By Consumer Type Analysis

Adults are projected to dominate the consumer type segment of the Ayurveda market as this demographic represents the primary consumers of both preventive wellness products and therapeutic formulations. Working-age adults face maximum exposure to lifestyle stressors including occupational pressure, sedentary work patterns, dietary irregularities, and sleep disruption, creating demand for natural solutions supporting energy, stress management, digestive health, and immunity. This demographic also possesses greater purchasing power and health awareness compared with younger populations, enabling consistent investment in wellness products. Additionally, adults represent the primary consumers of reproductive health formulations, cognitive support products, and metabolic health supplements addressing early signs of lifestyle disorders.

The adult demographic also demonstrates higher compliance with wellness routines and greater willingness to invest in preventive health compared with younger consumers focused on immediate needs. As the global population ages and the 25-55 age demographic expands in both developed and emerging markets, the addressable consumer base for Ayurvedic products continues growing. While elderly populations increasingly adopt Ayurveda for managing chronic conditions, and children's formulations address specific pediatric indications, adults remain the dominant consumer segment due to their combination of health needs, purchasing capacity, and preventive health orientation.

By Application Analysis

Medical and therapeutic applications are projected to dominate the application segment of the Ayurveda market because therapeutic use represents the foundational purpose of Ayurvedic medicine. During medical application, Ayurvedic formulations are used under professional guidance for managing diagnosed conditions, addressing specific health complaints, or supporting recovery from illness. Since every therapeutic intervention requires targeted formulations based on individual constitution and pathology, the demand for specialized Ayurvedic medicines is directly linked to the prevalence of treatable conditions worldwide. The increasing burden of lifestyle diseases including diabetes affecting over 500 million adults, cardiovascular conditions, digestive disorders, and stress-related illnesses has created unprecedented demand for therapeutic Ayurvedic interventions. Many healthcare systems have also expanded integration of traditional medicine through AYUSH departments and integrative medicine centers, further driving therapeutic adoption.

While personal care applications including skin care, hair care, and oral care are growing rapidly due to natural beauty trends, they still represent smaller portions of overall Ayurvedic consumption in value terms. Food and nutraceutical applications are particularly increasing among health-conscious consumers seeking functional benefits from daily nutrition, but therapeutic applications command premium pricing and higher per-user consumption. Research applications involving Ayurveda are comparatively limited and mainly confined to academic institutions or specialized laboratories. Because therapeutic use remains the primary driver of Ayurvedic consumption and requires ongoing treatment courses, this application segment generates the largest demand for authentic formulations. Consequently, medical and therapeutic applications continue to dominate the application segment of the global Ayurveda market.

By Distribution Channel Analysis

Retail and institutional sales are projected to dominate the distribution channel segment of the Ayurveda market because they encompass the widest network of physical touchpoints where consumers access Ayurvedic products. These channels include pharmacy chains, wellness stores, Ayurvedic retail outlets, hospital pharmacies, and institutional supply to wellness centers and clinics. Since consumer purchasing decisions for healthcare products often involve in-person evaluation, retail presence remains critical for building brand trust and facilitating first-time purchases. Compared with pure-play e-commerce channels, retail outlets offer immediate product availability, professional consultation opportunities, and tangibility that particularly matters for consumers new to Ayurveda. Many traditional consumers also prefer purchasing from established retail outlets with reputations for authentic products.

Additionally, institutional sales to hospitals, wellness centers, and corporate wellness programs provide steady volume demand that complements retail channel dynamics. The growth of organized retail in emerging markets, including pharmacy chains and wellness specialty stores, has significantly expanded access to quality Ayurvedic products. Consumers often prefer retail channels for therapeutic products requiring pharmacist or practitioner consultation, while using e-commerce for repeat purchases of wellness essentials. E-sales and direct sales channels are growing rapidly due to digital adoption, but retail and institutional sales maintain dominant share due to their extensive reach and role in initial consumer conversion. As a result, retail and institutional sales remain the dominant distribution channel segment in the global Ayurveda market.

By End-User Analysis

Home settings are projected to dominate the end-use segment of the Ayurveda market because the majority of Ayurvedic consumption occurs in household environments for daily wellness maintenance and self-management of minor health concerns. These settings encompass individuals and families using Ayurvedic products independently without continuous professional supervision, including daily supplements, digestive aids, immunity boosters, and personal care items. Since preventive healthcare and wellness maintenance represent the largest volume of Ayurvedic consumption, home settings naturally account for the highest usage frequency and product turnover. Compared with hospital and clinical settings where treatments are episodic and professionally supervised, home settings involve continuous daily consumption across family members.

Modern lifestyles have further normalized self-care practices including daily herbal supplementation, natural personal care routines, and kitchen remedies for common ailments, all occurring in home environments. The expansion of e-commerce and direct-to-consumer marketing has made Ayurvedic products more accessible for home users, with educational content supporting appropriate self-use. Additionally, the COVID-19 pandemic significantly accelerated home-based immunity building practices using Ayurvedic formulations, establishing sustained consumption patterns. Hospitals and clinics contribute to demand through professional prescribing and institutional dispensing, but the volume of product moving through home settings remains substantially larger. As a result, home settings maintain dominant end-user status in the global Ayurveda market.

The Global Ayurveda Market Report is segmented on the basis of the following:

By Form

- Herbal

- Herbomineral

- Mineral

By Product Type

- Herbal Supplements

- Ayurvedic Medicines

- Essential Oils

- Skin Care Products

By Indication

- Nervous System

- Cardiovascular System

- Reproductive System

- Infectious Diseases

- Others

By Consumer Type

- Adults

- Elderly

- Children

- Pregnant Women

By Application

- Medical/Therapy

- Lifestyle Disease Management

- Immunity Enhancement

- Digestive Health

- Respiratory Conditions

- Personal Care

- Skin Care

- Hair Care

- Oral Care

- Food & Nutraceuticals

By Distribution Channel

- Retail & Institutional Sales

- E-sales / Online Retail

- Direct/Distance Sales

By End Use

- Hospitals & Clinics

- Home Settings

Impact of Artificial Intelligence in the Global Ayurveda Market

- AI for Dosha Assessment and Personalization: AI algorithms analyze user responses, health data, and symptom patterns to determine individual constitution (prakriti) and recommend personalized Ayurvedic products and lifestyle modifications.

- Predictive Modeling for Disease Prevention: Machine learning models integrate genetic, lifestyle, and clinical data to predict individual susceptibility to lifestyle disorders, enabling targeted preventive interventions using Ayurvedic approaches.

- Quality Control in Herbal Manufacturing: Computer vision systems employing AI inspect raw herbs and manufactured products for authentication, adulterant detection, and quality grading, ensuring consistent product quality meeting regulatory requirements.

- Formulation Development and Optimization: AI platforms analyze traditional text references, phytochemical databases, and clinical outcomes to optimize herbal combinations and extraction methods for enhanced therapeutic efficacy.

- Supply Chain Traceability and Authentication: Blockchain integrated with AI enables end-to-end traceability of herbal raw materials from cultivation to finished product, addressing authenticity concerns and building consumer trust.

Global Ayurveda Market: Regional Analysis

Region with the Largest Revenue Share

Asia-Pacific is projected to dominate the regional segment with the highest market share as it is anticipated to hold approximately 77.5% of the total market revenue by the end of 2026, due to traditional medicine heritage, large consumer base, favorable regulatory frameworks, and concentration of leading Ayurvedic manufacturers in India and surrounding regions. The region is home to the world's largest Ayurvedic manufacturing infrastructure and traditional medicine research institutions, driving product development and clinical advancements. Strong cultural acceptance of Ayurveda as mainstream healthcare, combined with government support through dedicated AYUSH ministries and research funding, further strengthens demand. India, in particular, accounts for the largest share within Asia-Pacific due to its extensive Ayurvedic healthcare network, large manufacturing base, and growing export orientation. Although North America is the fastest-growing Western market, Asia-Pacific continues to hold the largest revenue share due to its traditional consumer base and established manufacturing ecosystem.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Region with the Highest CAGR

Asia Pacific holds the highest CAGR among developed regions and is poised to achieve rapid market share growth due to its large wellness-conscious population, rising acceptance of complementary medicine, expanding retail distribution for natural products, and growing research interest in traditional medicine systems. Countries including the United States and Canada are witnessing exponential growth in Ayurvedic product consumption through specialty retail, e-commerce platforms, and integrative medicine clinics. The U.S. market's sophisticated natural products infrastructure, combined with increasing consumer preference for preventive health solutions, is creating fertile ground for market expansion. The region's high per capita spending on wellness products, combined with growing numbers of Ayurvedic practitioners and wellness centers adopting international quality standards, positions North America as the fastest-growing market for Ayurvedic products in the Western hemisphere.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Global Ayurveda Market: Competitive Landscape

The Global Ayurveda Market is moderately fragmented, featuring a mix of specialized Ayurvedic manufacturers, diversified natural products companies, and multinational health and wellness corporations. Leading players like Dabur India, Patanjali Ayurved, and Emami Group leverage their established brand equity, extensive distribution networks, and comprehensive product portfolios to maintain market leadership in traditional markets. Specialized manufacturers such as Himalaya Drug Company, Baidyanath, and Zandu drive market dynamics with clinically focused innovation and strong relationships with healthcare practitioners. Multinational corporations including Procter & Gamble, Unilever, and Nestlé maintain selective presence through natural product divisions, while regional manufacturers serve local markets with culturally resonant traditional formulations. The market also features partnerships between Ayurvedic manufacturers and retail chains, wellness platforms, and e-commerce aggregators, ensuring consistent product supply and collaborative product development based on consumer feedback.

Some of the prominent players in the Global Ayurveda Market are:

- Dabur India Ltd.

- Himalaya Wellness Company

- Baidyanath Group

- Charak Pharma Pvt. Ltd.

- Zandu Pharmaceutical Works Ltd. (Emami Group)

- Patanjali Ayurved Ltd.

- Vicco Laboratories

- Hamdard Laboratories

- Maharishi Ayurveda

- Herbal Hills

- Basic Ayurveda

- Natreon

- Amrutanjan Healthcare Ltd.

- Botique

- Shahnaz Husain Group

- Forest Essentials

- Kerala Ayurveda Ltd.

- Sandu Pharmaceuticals Ltd.

- Jeena Sikho Lifecare Ltd.

- Medimix (AVA Group)

- Other Key Players

Recent Developments in the Global Ayurveda Market

- December 2025: Dabur India Limited commenced a significant consumer engagement initiative aimed at modernizing Ayurveda through its "Ayurveda Samvad" program. The project includes modernized packaging, statewide health camps offering free Ayurvedic check ups, and interactive sessions with experts to integrate Ayurveda into modern wellness practices.

- October 2025: Ashpveda partnered with Dabur NewU to launch a Festive 2025 Ayurvedic product collection. This collaboration expanded Ashpveda's retail presence across 20 Dabur NewU stores and aims to make authentic Ayurvedic skincare, haircare, and personal care products more accessible during the festive season.

- July 2025: Emami Group (through its Zandu brand) announced a new refreshed corporate identity to reflect the company's evolving vision and global ambitions as it strengthens its Ayurvedic and personal care portfolio. This rebrand marked a strategic milestone aligned with the company's 50 year legacy and future growth trajectory.

- February 2025: Organic India completed the acquisition of a significant stake in a South Indian organic spice farm, strengthening its sustainable sourcing of key Ayurvedic ingredients and enhancing product authenticity and traceability across its herbal foods and supplement portfolio.

- January 2025: Himalaya Herbals launched a new line of ready to eat Ayurvedic breakfast porridge products focused on gut health and immunity, blending traditional Ayurvedic herbs with convenient food formats to appeal to time pressed consumers seeking healthy alternatives.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 25.7 Bn |

| Forecast Value (2035) |

USD 131.5 Bn |

| CAGR (2026–2035) |

19.9% |

| The US Market Size (2026) |

USD 2.9 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Form (Herbal, Herbomineral, Mineral), By Product Type (Herbal Supplements, Ayurvedic Medicines, Essential Oils, Skin Care Products), By Indication (Nervous System, Cardiovascular System, Reproductive System, Infectious Diseases, Others), By Consumer Type (Adults, Elderly, Children, Pregnant Women), By Application (Medical/Therapy, Personal Care, Food & Nutraceuticals), By Distribution Channel (Retail & Institutional Sales, E-sales / Online Retail, Direct/Distance Sales), By End Use (Hospitals & Clinics, Home Settings) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia- Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

Dabur India Ltd., Himalaya Wellness Company, Baidyanath Group, Charak Pharma Pvt. Ltd., Zandu Pharmaceutical Works Ltd. (Emami Group), Patanjali Ayurved Ltd., Vicco Laboratories, Hamdard Laboratories, Maharishi Ayurveda, Herbal Hills, Basic Ayurveda, Natreon, Amrutanjan Healthcare Ltd., Botique, Shahnaz Husain Group, Forest Essentials, Kerala Ayurveda Ltd., Sandu Pharmaceuticals Ltd., Jeena Sikho Lifecare Ltd., Medimix (AVA Group), and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Ayurveda Market?

▾ The Global Ayurveda Market size is estimated to have a value of USD 25.7 billion in 2026 and is expected to reach USD 131.5 billion by the end of 2035.

What is the growth rate in the Global Ayurveda Market in 2026?

▾ The market is growing at a CAGR of 19.9%over the forecasted period of 2026.

What is the size of the US Ayurveda Market?

▾ The US Ayurveda Market is projected to be valued at USD 2.9 billion in 2026. It is expected to witness subsequent growth in the upcoming period as it holds USD 13.3 billion in 2035 at a CAGR of 18.7%.

Which region accounted for the largest Global Ayurveda Market?

▾ Asia Pacific is expected to have the largest market share in the Global Ayurveda Market with a share of about 77.5% in 2026.

Who are the key players in the Global Ayurveda Market?

▾ Some of the major key players in the Global Ayurveda Market are Dabur India Ltd., Himalaya Wellness Company, Baidyanath Group, Charak Pharma Pvt. Ltd., Zandu Pharmaceutical Works Ltd. (Emami Group), and many others.