What is the Cell and Gene Therapy Manufacturing Market Size?

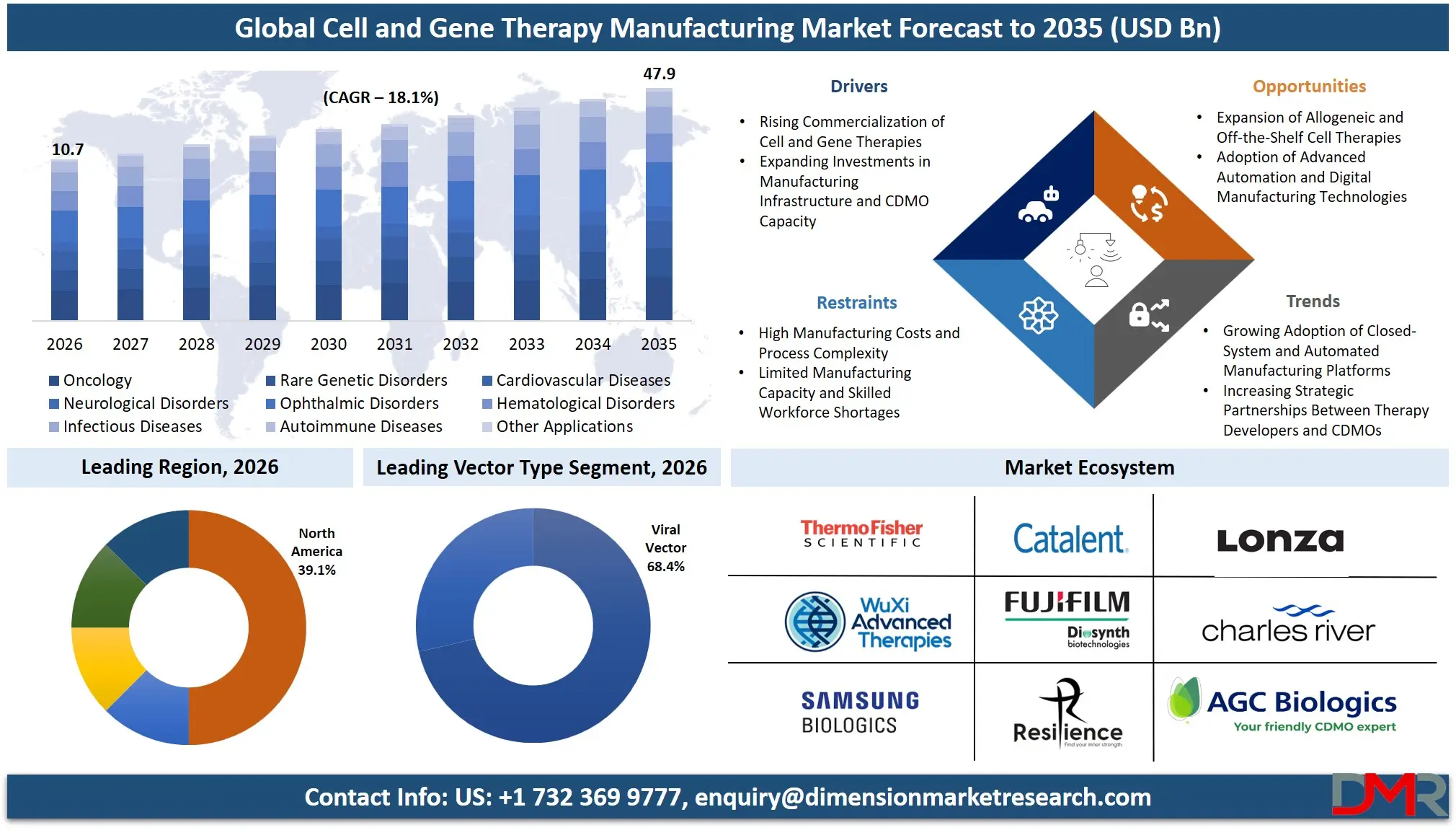

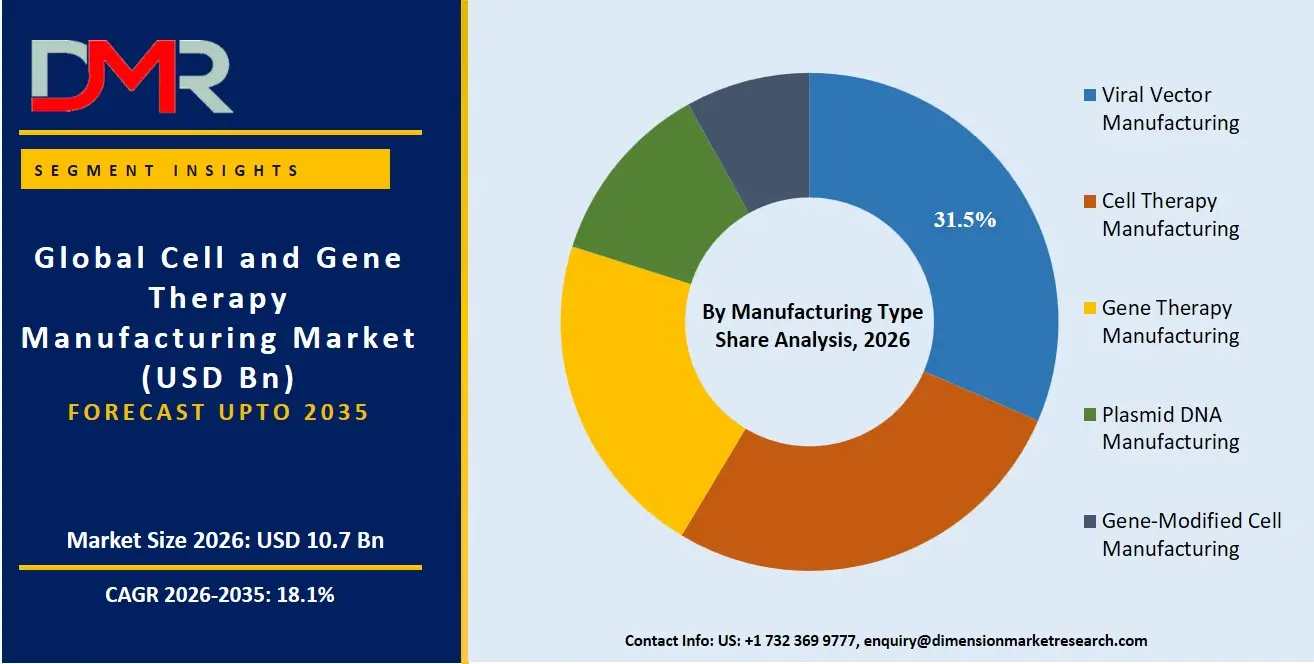

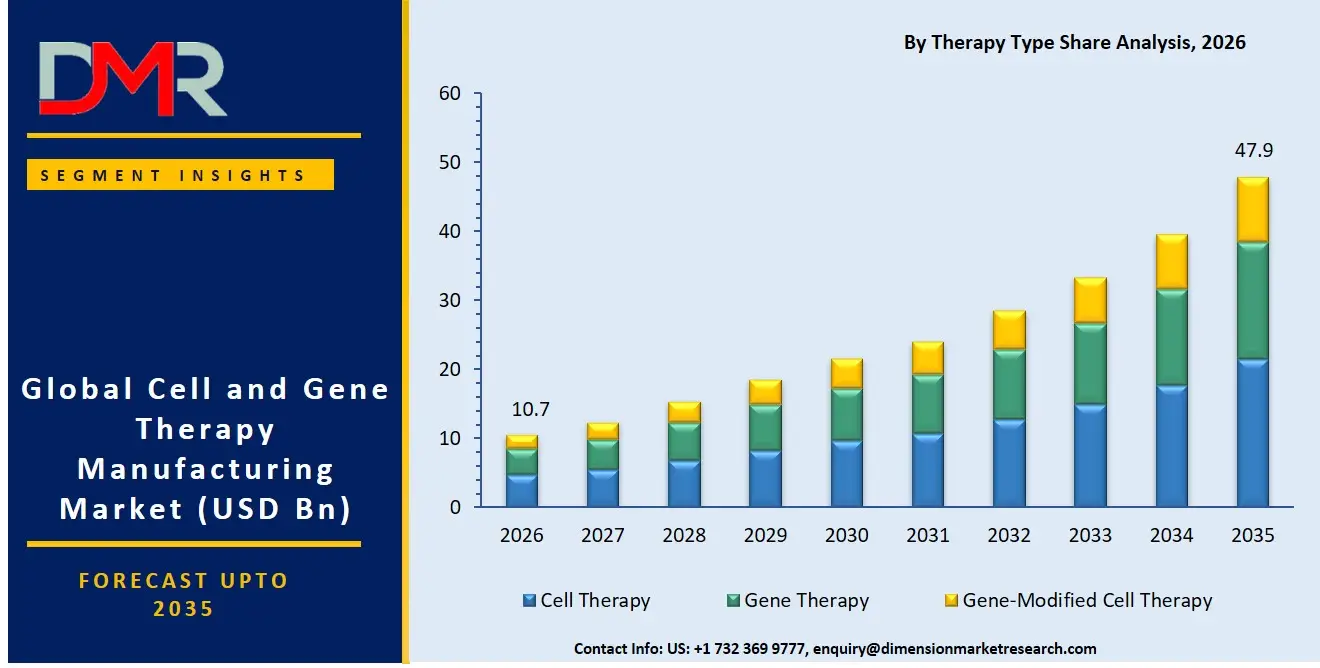

The Global Cell and Gene Therapy Manufacturing Market is expected to reach a value of USD 10.7 billion in 2026, and it is further anticipated to surge to USD 47.9 billion by 2035, growing at a robust CAGR of 18.1% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

There is exponential growth in the market since there is a transition from a science based on promises to reality, and therefore, the need arises to quickly industrialize processes that are very complex in nature. The market includes specialized infrastructure, technologies, and services needed to manufacture viral vectors, plasmid DNA, and living cell-based therapies on a large scale. The rise in the number of approvals for autologous CAR-T cell therapies, advancement of allogeneic "off-the-shelf" platforms and race to cure rare genetic diseases have created an urgent need for advanced manufacturing solutions. Biopharmaceutical firms are the key players; however, CDMOs play a vital role in addressing gaps in specialized manufacturing capacity, especially viral vector manufacturing. There is an increased effort towards decentralization, automation and closure of manufacturing processes in order to ensure sterility, consistency, and cost-effectiveness of these life saving treatments from custom-made clinical procedures to a pillar of modern medicine.

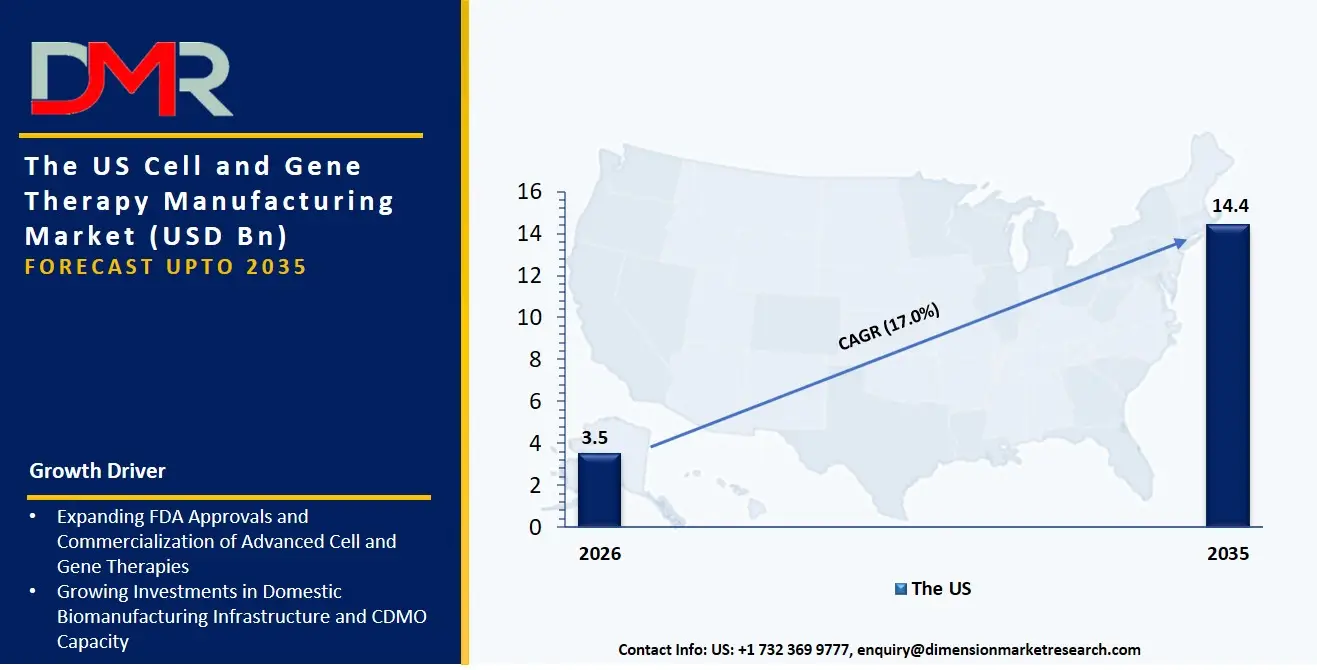

The US Cell and Gene Therapy Manufacturing Market

The US Cell and Gene Therapy Manufacturing Market is projected to reach USD 3.5 billion in 2026, maintaining a compound annual growth rate of 17.0% over its forecast period to culminate in a value of USD 14.4 billion by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US still holds the title as the leading manufacturing center for advanced CGT development owing to the presence of numerous clinical-stage products, well-established financing of the biotech sector, and an active Food and Drug Administration (FDA) that has created specialized procedures for reviews. The US market is dominated by the manufacturing of autologous cell therapies and commercial products with a considerable infrastructure being invested in the manufacturing of viral vectors in order to solve any supply shortages. Thus, the demand for dedicated downstream processes and quality control tests arises because of the challenging release requirements of these innovative products. Additionally, the emergence of in vivo gene therapies through novel non-viral vectors like LNPs is driving demand for the creation of new formulations and fill-finish solutions different from those used in conventional biologics production.

The Europe Cell and Gene Therapy Manufacturing Market

The Europe Cell and Gene Therapy Manufacturing Market is estimated to be valued at USD 3.0 billion in 2026 and is further anticipated to reach USD 12.8 billion by 2035 at a CAGR of 17.5%. The European market is very much dominated by the Committee for Advanced Therapies (CAT) at the European Medicines Agency and the creation of a collaborative but strict regulatory system which has enabled harmonization of quality standards among member states. There is a rapid increase in the number of allogeneic cell therapy platforms which can be attributed to the presence of a strong academic and translational research infrastructure in countries such as the UK, Germany, and France. Cell therapies that have been genetically modified require unique manufacturing processes which have led to increased funding in CDMO companies that specialize in gene-modified cell manufacturing. Also, there is increased manufacturing innovation in the area of AAV gene therapy due to the legacy of rare diseases in the region.

The Japan Cell and Gene Therapy Manufacturing Market

The Japan Cell and Gene Therapy Manufacturing Market is projected to be valued at USD 1.2 billion in 2026, with robust growth anticipated to hold USD 4.7 billion by 2035 at a CAGR of 16.4%. T the Japanese market has an unique feature in terms of the state policy that uses the system of "Sakigake" designation to grant a fast approval to regenerative medicines on a conditional basis. A large amount of financing will be allocated for the production of cell therapies, especially for allogeneic cell therapies derived from induced pluripotent stem cells (iPSCs), which involve extensive cellular expansion and strict processes of differentiation. Additionally, there is an internal need to secure the production of plasmid DNA and viral vectors because Japan is a leader in iPSC technology and therefore requires a quality control and testing service to ensure the safety of genetically modified cells without the involvement of other countries.

Key Takeaways

- Market Size & Forecast: The Global Cell and Gene Therapy Manufacturing Market is projected to reach USD 10.7 billion in 2026, expanding dramatically to USD 47.9 billion by 2035, fueled by the dual engines of an expanding commercial pipeline and the industrial imperative to move beyond artisanal production toward robust, scalable platforms.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 18.1%, driven by a critical shortage of bioprocessing capacity and the escalating complexity of managing diverse vector types and patient-specific supply chains under stringent regulatory oversight.

- Primary Growth Drivers: Key forces include the validation of CAR-T cell therapy as a frontline treatment and its subsequent demand spike, the necessity for novel viral and non-viral vector manufacturing platforms to overcome yield limitations, and the rise of allogeneic therapies that require hyper-scalable manufacturing processes to achieve economic viability.

- Key Market Trends: Major trends include the shift toward closed, automated systems in cell therapy processing to reduce contamination risks and labor costs, the application of in-line analytics and AI for process analytical technology (PAT) within quality control workflows, and the strategic consolidation of CDMOs to offer integrated fill-finish operations and global logistical support.

- By Mode Analysis: Contract Manufacturing by CDMOs is expected to dominate capacity expansion discussions as a majority of small- to mid-cap therapy developers lack the capital to build in-house plants. The competitive edge lies in offering end-to-end services that seamlessly link upstream plasmid DNA production with final downstream formulation and fill-finish.

- By Vector Type Analysis: Lentivirus (LV) and Adeno-Associated Virus (AAV) remain the most critical vector segments, with AAV demand surging for in vivo gene therapy targeting rare genetic and neurological disorders. A parallel growth vector is the Lipid Nanoparticle (LNP) segment, which is attracting massive investment for non-viral delivery.

- By Application Analysis: Oncology dominates the application landscape, overwhelmingly driven by the commercial success of CAR-T cell therapies. However, rare genetic disorders and neurological disorders represent the highest-growth segments as new gene-modified cell platforms address the underlying causes of conditions rather than just symptoms.

- Regional Leadership: North America is poised to dominate this market with a 39.1% market share in 2026 due to its vast clinical pipeline depth, concentration of top-tier CDMOs, and a venture capital ecosystem that aggressively funds innovative vector manufacturing technologies, making it the undisputed leader in this market.

What is the Cell and Gene Therapy Manufacturing?

Cell and Gene Therapy Manufacturing refers to the suite of specialized processes, technologies, and facilities dedicated to producing Advanced Therapy Medicinal Products (ATMPs) at a scale and quality that meets regulatory standards. Unlike small-molecule drugs or conventional biologics, these therapies often utilize a living "product" (the cells or viral vectors themselves), which means the manufacturing process defines the therapy's identity and is inseparable from its clinical outcome. This market covers the entire workflow from upstream processing—which involves cell isolation from a patient or donor, cell expansion, and cell engineering/genetic modification using viral vectors or non-viral systems like electroporation—to downstream processing that includes harvesting, purification, concentration, and sterile fill-finish operations. As 70% of current therapy developers are virtual or small biotech firms, manufacturing services provided by Contract Development and Manufacturing Organizations (CDMOs) are not merely transactional but are fundamental to translating complex science into commercially viable, accessible treatments.

Use Cases

- Autologous Cancer Immunotherapy Production: Academic medical centers and biopharmaceutical sponsors hire specialized CDMOs to manage the vein-to-vein supply chain for autologous cell therapy, coordinating cell isolation, ex vivo lentiviral transduction for CAR-T engineering, expansion, and final formulation before returning the personalized drug product to the clinical site for infusion.

- AAV Gene Therapy for CNS Disorders: Biotechnology companies leverage contract viral vector manufacturing services to produce high-titer, high-purity AAV capsids engineered to cross the blood-brain barrier, requiring ultra-scalable upstream processing and advanced purification steps to deliver therapies for spinal muscular atrophy or inherited retinal dystrophies.

- iPSC-Derived Allogeneic Master Cell Banking: Developers of next-generation off-the-shelf cell therapies utilize advanced cell engineering platforms to genetically modify a single master iPSC line, then rely on scaled-up cell expansion and differentiation protocols to create limitless batches of natural killer (NK) cells or cardiomyocytes for broad patient populations.

- Point-of-Care Gene-Modified Cell Manufacturing: Hospital clinical centers are adopting automated, closed-system bioreactors for bedside autologous cell therapy manufacturing, allowing them to execute upstream gene-modification and a shortened downstream wash-and-harvest cycle within the surgical suite, drastically reducing the vein-to-vein time and cost.

How AI is Transforming the Cell and Gene Therapy Manufacturing Market

Artificial intelligence is fundamentally reshaping the CGT manufacturing market by tackling the biological variability that has historically plagued product consistency and scalability. In quality control and testing, AI-powered digital pathology models can analyze images of cell cultures in real-time during upstream processing, predicting the health and potency of a batch far earlier than traditional end-point assays. This integration of machine vision into bioreactors enables "smart manufacturing," where automated feedback loops instantly adjust nutrient feeds, oxygen levels, and pH to optimize cell expansion and ensure cell engineering efficiency. Furthermore, AI is revolutionizing downstream purification; for viral vectors, deep learning algorithms are being used to model complex chromatography separations, enabling manufacturers to distinguish between full and empty AAV capsids with a precision that maximizes potency while minimizing the immunogenic burden. In clinical and commercial scale-up, generative AI accelerates process development by simulating the impact of different plasmid DNA transfection ratios or electroporation parameters, predicting the optimal therapeutic window for T-cell activation without weeks of physical trial and error, thereby compressing development timelines.

Market Dynamics

Key Drivers in the Global Cell and Gene Therapy Manufacturing Market

Rising Commercialization of Cell and Gene Therapies

The growing number of regulatory approvals for cell and gene therapies is a major driver of manufacturing demand worldwide. As more therapies transition from clinical development to commercial production, manufacturers are investing in larger, highly automated, and GMP-compliant facilities to meet increasing patient demand. Advanced therapies such as CAR-T, gene replacement therapies, and stem cell-based treatments require specialized production processes, creating sustained demand for manufacturing infrastructure. Pharmaceutical companies are expanding internal production capabilities while partnering with CDMOs to accelerate commercialization. Continued innovation, increasing clinical success rates, and broader therapeutic applications across oncology, rare diseases, and regenerative medicine are expected to further strengthen manufacturing activities globally throughout the forecast period.

Expanding Investments in Manufacturing Infrastructure and CDMO Capacity

Significant investments in advanced manufacturing infrastructure are accelerating the growth of the global cell and gene therapy manufacturing market. Biopharmaceutical companies, biotechnology firms, and CDMOs are expanding production facilities equipped with automation, closed-system manufacturing, digital quality monitoring, and scalable bioprocessing technologies. These investments address capacity shortages while improving manufacturing efficiency and regulatory compliance. Governments and private investors are also supporting domestic manufacturing initiatives to reduce dependence on limited global production capacity. Increasing outsourcing trends have encouraged CDMOs to broaden their service portfolios, including viral vector production, analytical testing, fill-finish operations, and process development, enabling faster commercialization of advanced therapies worldwide.

Restraints in the Global Cell and Gene Therapy Manufacturing Market

High Manufacturing Costs and Process Complexity

Cell and gene therapy manufacturing remains one of the most expensive areas of pharmaceutical production due to highly specialized equipment, stringent cleanroom requirements, complex biological processes, and intensive quality control procedures. Personalized therapies require patient-specific manufacturing, increasing production costs and operational complexity. Maintaining product consistency, sterility, and regulatory compliance throughout manufacturing further adds to expenses. Small production batches, expensive raw materials, and sophisticated logistics contribute to high treatment costs, limiting broader market accessibility. These economic and operational challenges continue to slow manufacturing expansion, particularly among emerging biotechnology companies with limited financial and technical resources.

Limited Manufacturing Capacity and Skilled Workforce Shortage

Despite increasing investments, global manufacturing capacity remains insufficient to meet the rapidly growing demand for advanced therapies. Production bottlenecks frequently occur due to limited availability of GMP facilities, viral vector manufacturing capacity, and specialized processing equipment. The industry also faces shortages of experienced professionals skilled in cell culture, vector production, analytical testing, quality assurance, and regulatory compliance. Recruiting and training qualified personnel requires substantial time and investment. These workforce limitations delay facility expansion, technology transfer, and commercial production timelines, restricting overall manufacturing scalability and slowing the introduction of new therapies into global healthcare markets.

Growth Opportunities in the Global Cell and Gene Therapy Manufacturing Market

Expansion of Allogeneic and Off-the-Shelf Cell Therapies

The development of allogeneic cell therapies presents significant opportunities for manufacturing expansion because these therapies can be produced in large batches and distributed to multiple patients. Compared to personalized autologous therapies, allogeneic manufacturing enables improved scalability, lower production costs, simplified logistics, and greater commercial efficiency. Advances in gene editing, immune engineering, and stem cell technologies are improving the safety and effectiveness of off-the-shelf therapies. Manufacturers investing in scalable bioprocessing platforms, automated production systems, and standardized manufacturing protocols are well positioned to capitalize on this rapidly growing segment as clinical adoption continues expanding across multiple therapeutic areas.

Adoption of Advanced Automation and Digital Manufacturing Technologies

Automation and digitalization are creating major growth opportunities by improving manufacturing efficiency, consistency, and scalability. Artificial intelligence, machine learning, robotics, digital twins, and real-time process monitoring enable manufacturers to optimize production while minimizing human error and contamination risks. Automated closed-system manufacturing reduces labor requirements and enhances product quality, particularly for personalized therapies. Digital manufacturing platforms also improve regulatory compliance through continuous monitoring and electronic batch documentation. As manufacturers increasingly adopt Industry 4.0 technologies, production costs decline while throughput increases, supporting broader commercialization and global accessibility of advanced cell and gene therapies.

Trends in the Global Cell and Gene Therapy Manufacturing Market

Growing Adoption of Closed-System and Automated Manufacturing Platforms

Manufacturers are increasingly adopting closed-system and automated production platforms to improve product consistency, reduce contamination risks, and increase operational efficiency. Automated cell processing, robotic handling systems, and integrated bioreactors minimize manual intervention while supporting standardized manufacturing workflows. These technologies also simplify regulatory compliance and enable higher production capacity without proportional increases in labor requirements. Automation is particularly valuable for personalized therapies requiring precise, reproducible manufacturing. As commercial production volumes increase globally, investments in smart manufacturing technologies are expected to continue accelerating across both pharmaceutical companies and specialized CDMOs.

Increasing Strategic Partnerships Between Therapy Developers and CDMOs

Strategic collaborations between therapy developers and contract manufacturing organizations have become a defining trend within the industry. Biotechnology companies increasingly rely on CDMOs for process development, viral vector production, analytical testing, regulatory support, and commercial manufacturing to accelerate product launches while minimizing capital investment. CDMOs continue expanding geographically and investing in advanced production technologies to meet growing global demand. Long-term manufacturing agreements, technology transfer partnerships, and joint investments improve production flexibility while reducing commercialization risks. This collaborative business model is becoming increasingly important as the number of late-stage clinical programs and approved therapies continues to rise globally.

Research Scope and Analysis

The Global Cell and Gene Therapy Manufacturing Market is segmented by therapy type, manufacturing type, mode, scale of operation, workflow, vector type, application, and end user.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Therapy Type Analysis

Cell therapy is poised to dominates the global cell and gene therapy manufacturing market due to the rapid commercialization of autologous and allogeneic therapies, particularly in hematological cancers and regenerative medicine.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Manufacturing demand is driven by the increasing number of approved cell-based products and the expansion of clinical pipelines. Autologous therapies require individualized manufacturing, while allogeneic platforms are enabling scalable production. The segment also benefits from technological advancements in closed-system manufacturing, automation, and cryopreservation. Growing investments in manufacturing infrastructure by pharmaceutical companies and contract manufacturers further strengthen this segment. Continued innovation in immune cell engineering and stem cell therapies is expected to maintain cell therapy's leadership throughout the forecast period.

By Manufacturing Type Analysis

Viral vector manufacturing is anticipated to be the dominant manufacturing type because viral vectors are essential for delivering therapeutic genes and engineering genetically modified cells such as CAR-T therapies. Adeno-associated viruses (AAVs), lentiviruses, and adenoviruses are widely used across commercial and clinical-stage products. The increasing number of gene therapies entering late-stage development has created substantial demand for high-quality vector production. Manufacturing complexity, stringent regulatory requirements, and limited global production capacity have also increased investment in specialized viral vector facilities. Companies continue expanding vector manufacturing capabilities through automation and process optimization, making viral vector manufacturing the largest and most strategically important segment within the overall manufacturing landscape.

By Mode Analysis

Contract manufacturing is expected to be the dominant the market as many biotechnology companies lack the expertise, infrastructure, and regulatory capabilities required for commercial-scale cell and gene therapy production. Contract Development and Manufacturing Organizations (CDMOs) provide end-to-end manufacturing services, including process development, analytical testing, viral vector production, fill-finish operations, and regulatory support. Outsourcing reduces capital expenditure while accelerating product development and commercialization timelines. The rapid growth of early-stage biotechnology firms has significantly increased reliance on specialized manufacturing partners. Furthermore, expanding global CDMO capacity, flexible manufacturing platforms, and increasing strategic collaborations between therapy developers and contract manufacturers continue to reinforce the dominance of contract manufacturing across the industry.

By Scale of Operation Analysis

Commercial manufacturing is projected to represent the dominant segment due to the increasing number of approved cell and gene therapies entering global markets. As regulatory approvals continue to rise, manufacturers are expanding commercial production facilities capable of meeting stringent quality, consistency, and scalability requirements. Commercial manufacturing requires highly automated production systems, validated processes, advanced quality control, and robust cold-chain logistics, resulting in significantly higher manufacturing value than preclinical or clinical production. Growing patient demand for approved therapies, particularly in oncology and rare genetic disorders, further drives commercial-scale manufacturing investments. Capacity expansion by pharmaceutical companies and CDMOs continues strengthening this segment's market leadership.

By Workflow Analysis

Upstream processing is expected to dominate the workflow segment because it encompasses the most critical and resource-intensive stages of cell and gene therapy manufacturing, including cell isolation, expansion, activation, and genetic modification. Product quality and therapeutic efficacy largely depend on successful upstream operations, making this phase a major focus for manufacturers. Advanced bioreactor technologies, automated cell culture systems, and optimized transfection methods continue improving productivity while reducing contamination risks. The growing complexity of engineered cell therapies and viral vector production further increases investments in upstream technologies. Continuous innovations in process development and automation ensure upstream processing remains the largest contributor to manufacturing activities.

By Vector Type Analysis

Viral vectors is projected to dominate the vector type segment because they provide highly efficient and reliable gene delivery for both gene therapies and genetically modified cell therapies. Adeno-associated virus (AAV), lentivirus, adenovirus, and retrovirus vectors have become industry standards due to their proven safety profiles and high transduction efficiency. Most commercially approved gene therapies currently rely on viral vector technology, driving substantial manufacturing demand worldwide. Although non-viral delivery technologies are rapidly advancing, viral vectors continue to dominate owing to extensive clinical validation and regulatory acceptance. Ongoing investments in manufacturing capacity expansion and improved vector production technologies further reinforce their leadership position.

By Application Analysis

Oncology is anticipated to dominate the application segment because the majority of approved and pipeline cell and gene therapies target various cancers, particularly hematological malignancies. CAR-T cell therapies have transformed the treatment of leukemia, lymphoma, and multiple myeloma, driving significant manufacturing demand. Continuous research into solid tumor therapies, engineered immune cells, and combination immunotherapies further expands production requirements. High disease prevalence, increasing regulatory approvals, and strong investment from pharmaceutical companies contribute to sustained growth. Additionally, oncology receives the largest share of clinical trial funding globally, ensuring continuous expansion of manufacturing capacity and maintaining its dominant position within the cell and gene therapy manufacturing market.

By End User Analysis

Biopharmaceutical companies is expected to dominate the end-user segment as they lead the discovery, clinical development, commercialization, and large-scale manufacturing of advanced cell and gene therapies. These organizations invest heavily in manufacturing infrastructure, automation technologies, process optimization, and regulatory compliance to support expanding commercial portfolios. Large pharmaceutical firms increasingly acquire or partner with biotechnology innovators to strengthen their advanced therapy pipelines, further boosting manufacturing activities. Their financial resources, global distribution networks, and established regulatory expertise enable efficient commercialization of complex therapies. Continuous investments in dedicated manufacturing facilities and strategic collaborations with CDMOs ensure biopharmaceutical companies remain the largest end users in this market.

The Global Cell and Gene Therapy Manufacturing Market Report is segmented on the basis of the following:

By Therapy Type

- Cell Therapy

- Autologous Cell Therapy

- Allogeneic Cell Therapy

- Gene Therapy

- In Vivo Gene Therapy

- Ex Vivo Gene Therapy

- Gene-Modified Cell Therapy

- CAR-T Cell Therapy

- TCR-T Cell Therapy

- Other Genetically Modified Cell Therapies

By Manufacturing Type

- Viral Vector Manufacturing

- Cell Therapy Manufacturing

- Gene Therapy Manufacturing

- Plasmid DNA Manufacturing

- Gene-Modified Cell Manufacturing

By Mode

- Contract Manufacturing

- Contract Development and Manufacturing Organizations (CDMOs)

- Contract Manufacturing Organizations (CMOs)

- In-House Manufacturing

By Scale of Operation

- Commercial Manufacturing

- Preclinical Manufacturing

- Clinical Manufacturing

- Phase I

- Phase II

- Phase III

By Workflow

- Upstream Processing

- Cell Isolation

- Cell Expansion

- Cell Engineering/Modification

- Downstream Processing

- Harvesting

- Purification

- Concentration

- Formulation

- Fill-Finish Operations

- Quality Control & Testing

By Vector Type

- Viral Vectors

- Adeno-Associated Virus (AAV)

- Lentivirus

- Adenovirus

- Retrovirus

- Herpes Simplex Virus (HSV)

- Other Viral Vectors

- Non-Viral Vectors

- Plasmid DNA

- Lipid Nanoparticles (LNPs)

- Electroporation-Based Systems

- Other Non-Viral Vectors

By Application

- Oncology

- Rare Genetic Disorders

- Cardiovascular Diseases

- Neurological Disorders

- Ophthalmic Disorders

- Hematological Disorders

- Infectious Diseases

- Autoimmune Diseases

- Other Applications

By End User

- Biopharmaceutical Companies

- Biotechnology Companies

- Academic & Research Institutes

- Hospitals & Clinical Centers

- Contract Development and Manufacturing Organizations (CDMOs)

Regional Analysis

Leading Region by Market Share

ℹ

To learn more about this report –

Download Your Free Sample Report Here

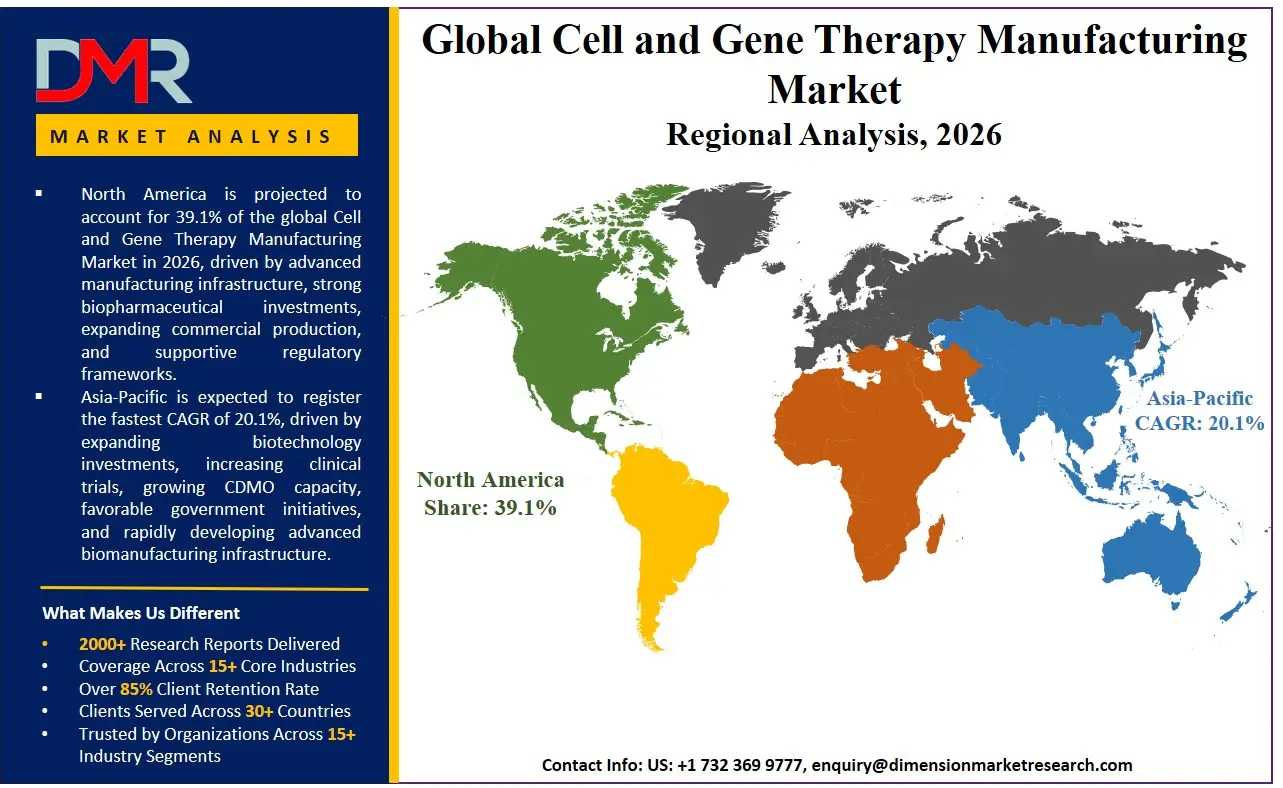

North America is poised to dominate the global cell and gene therapy manufacturing market, holding a projected 39.1% of the market share by the end of 2026. The United States, which anchors North America's leadership, holds the highest share because of an unmatched concentration of FDA-approved CGT products and the most densely developed cluster of advanced therapy CDMOs globally. The region benefits from a synergistic ecosystem where a massive number of clinical-stage biotechnology companies operate within a 30-mile radius of the specialized biomanufacturing hubs in Boston, San Francisco, and Research Triangle Park. Enterprise investment in next-generation gene-modified cell therapy platforms, particularly in allogeneic and autoimmune applications, is sustaining relentless demand for viral vector and plasmid DNA manufacturing capacity. Moreover, an aggressive private equity and venture capital climate persistently finances the construction of "smart factories" equipped for closed-system cell therapy manufacturing and real-time quality control, ensuring the US remains the epicenter of manufacturing innovation.

Fastest-Growing Regional Market

The Asia-Pacific region is expected to be the most rapidly expanding CGT manufacturing market, driven by proactive government-led biotechnology industrialization policies in China, Japan, South Korea, and India. The rapid economic development in the region, coupled with a massive, treatment-naive patient population, is forcing both domestic conglomerates and innovative biotech startups to invest heavily in building cGMP-compliant facilities, often leapfrogging legacy bioprocessing methods to install the latest modular, single-use technologies. In-House Manufacturing is being actively promoted by sovereign wealth and state-backed funds, while CDMOs are also proliferating to serve Western sponsors seeking cost-efficient, parallel clinical trial manufacturing sites. The region is also experiencing a critical shortage of experienced CGT bioprocess engineers, which is driving a strategic reliance on technology transfer partnerships and turnkey automated manufacturing solutions from Western equipment providers to rapidly bridge the skills gap and accelerate commercial readiness.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive environment of the global CGT manufacturing market is intensely stratified between multinational pharmaceutical companies with dedicated in-house manufacturing divisions, a dominant tier of global CDMOs, and a fast-moving wave of specialized viral vector and cell processing technology firms. Success hinges on securing long-term strategic partnerships with therapy developers, as early-phase process development collaborations often lock in a CDMO for the lucrative commercial manufacturing phases. The movement toward market consolidation is rapidly progressing, with large bio-production conglomerates acquiring boutique cell engineering and electroporation-based system specialists to provide an end-to-end, "gene-to-product" workflow. Proprietary intellectual property, including high-density suspension-adapted cell lines for AAV manufacturing and chemically defined, serum-free media for T-cell expansion, is a more critical differentiator than cleanroom capacity alone. The dominant strategic vector is the race to integrate vector manufacturing (plasmid and virus) directly with cell therapy manufacturing under a single integrated chain of custody, eliminating the supply hand-offs that represent the single greatest risk to patient delivery timelines.

Some of the prominent players in the Global Cell and Gene Therapy Manufacturing Market are:

- Thermo Fisher Scientific

- Lonza Group

- Catalent, Inc.

- Fujifilm Diosynth Biotechnologies

- WuXi Advanced Therapies

- Charles River Laboratories

- Samsung Biologics

- Danaher Corporation (Cytiva)

- Merck KGaA (MilliporeSigma)

- Sartorius AG

- Novartis AG

- Bristol Myers Squibb

- Gilead Sciences (Kite Pharma)

- Bluebird Bio

- Legend Biotech

- Oxford Biomedica

- AGC Biologics

- Takara Bio Inc.

- Aldevron

- Ori Biotech

- Other Key Players

Recent Developments

- January 2026: Thermo Fisher Scientific expanded its Patheon™ viral vector manufacturing network, announcing a dedicated facility focused entirely on high-yield AAV upstream processing and advanced purification, aiming to produce 10x current industry standard titers for rare genetic disorder applications.

- November 2025: Lonza Group secured a long-term commercial manufacturing supply agreement with a leading allogeneic CAR-T developer, investing significantly in automated, closed-system cell expansion suites to move beyond manual autologous workflows and into scaled, donor-derived gene-modified cell manufacturing.

- October 2025: FUJIFILM Diosynth Biotechnologies acquired a specialized European non-viral vector company, integrating its proprietary Lipid Nanoparticle (LNP) formulation and microfluidic mixing technology to support the surging clinical pipeline of in vivo mRNA and CRISPR-based therapies.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 10.7 Bn |

| Forecast Value (2035) |

USD 47.9 Bn |

| CAGR (2026–2035) |

18.1% |

| The US Market Size (2026) |

USD 3.5 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Therapy Type, By Manufacturing Type, By Mode, By Scale of Operation, By Workflow, By Vector Type, By Application, and By End User |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Cell and Gene Therapy Manufacturing Market?

▾ The Global Cell and Gene Therapy Manufacturing market is poised to be valued at USD 10.7 billion in 2026 and is projected to reach USD 47.9 billion by 2035, driven by the universal need to bridge the chasm between clinical promise and commercial-scale production of these complex therapies.

What is the CAGR of the Global Cell and Gene Therapy Manufacturing Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 18.1% from 2026 to 2035, reflecting the accelerating pipeline of gene-modified cell therapies and the persistent, critical shortage of industrial-scale viral vector and plasmid DNA manufacturing capacity.

What factors are driving the growth of the Global Cell and Gene Therapy Manufacturing Market?

▾ Key drivers include the severe global bottleneck in viral vector manufacturing, the logistical drive to transition from patient-specific autologous production to scalable allogeneic platforms, and the increasing regulatory demand for stringent Quality Control and fill-finish operations that validate living drug products.

Which region held the largest share of the Cell and Gene Therapy Manufacturing Market in 2026?

▾ North America, specifically the United States, held a 39.1% market share in 2026, driven by a mature CDMO ecosystem and aggressive investment by biopharmaceutical companies in clinical and commercial manufacturing facilities for CAR-T and AAV gene therapies.

Which region is expected to grow the fastest in the Cell and Gene Therapy Manufacturing Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by massive government investment in sovereign biomanufacturing capacity, a growing clinical trial density, and the adoption of automated manufacturing platforms that allow new facilities to scale rapidly without decades of legacy bioprocessing inertia.

What are the major trends in the Global Cell and Gene Therapy Manufacturing Market?

▾ Major trends include the integration of closed, automated "GMP-in-a-box" systems, the rise of real-time release testing and in-line analytics to replace traditional sterility assays, the pivot to non-viral vector manufacturing (lipid nanoparticles), and the consolidation of supply chains under single CDMOs offering plasmid-to-patient integration.

Who are the key players in the Global Cell and Gene Therapy Manufacturing Market?

▾ Key players include global CDMO leaders like Lonza, Catalent, and Thermo Fisher, therapy-specific biotech manufacturers like Novartis and bluebird bio, and innovative technology enablers like Cytiva and Miltenyi Biotec that provide the closed-system hardware and reagents underpinning the entire workflow.

How is the Global Cell and Gene Therapy Manufacturing Market segmented?

▾ The market is segmented by Therapy Type (Autologous, Allogeneic, In Vivo, Ex Vivo, CAR-T), Manufacturing Type, Mode (CDMO/CMO vs. In-House), Scale of Operation (Preclinical, Clinical, Commercial), Workflow (Upstream, Downstream, Fill-Finish), Vector Type (Viral and Non-Viral), Application (Oncology, Rare Genetic Disorders), and End User.