Market Overview

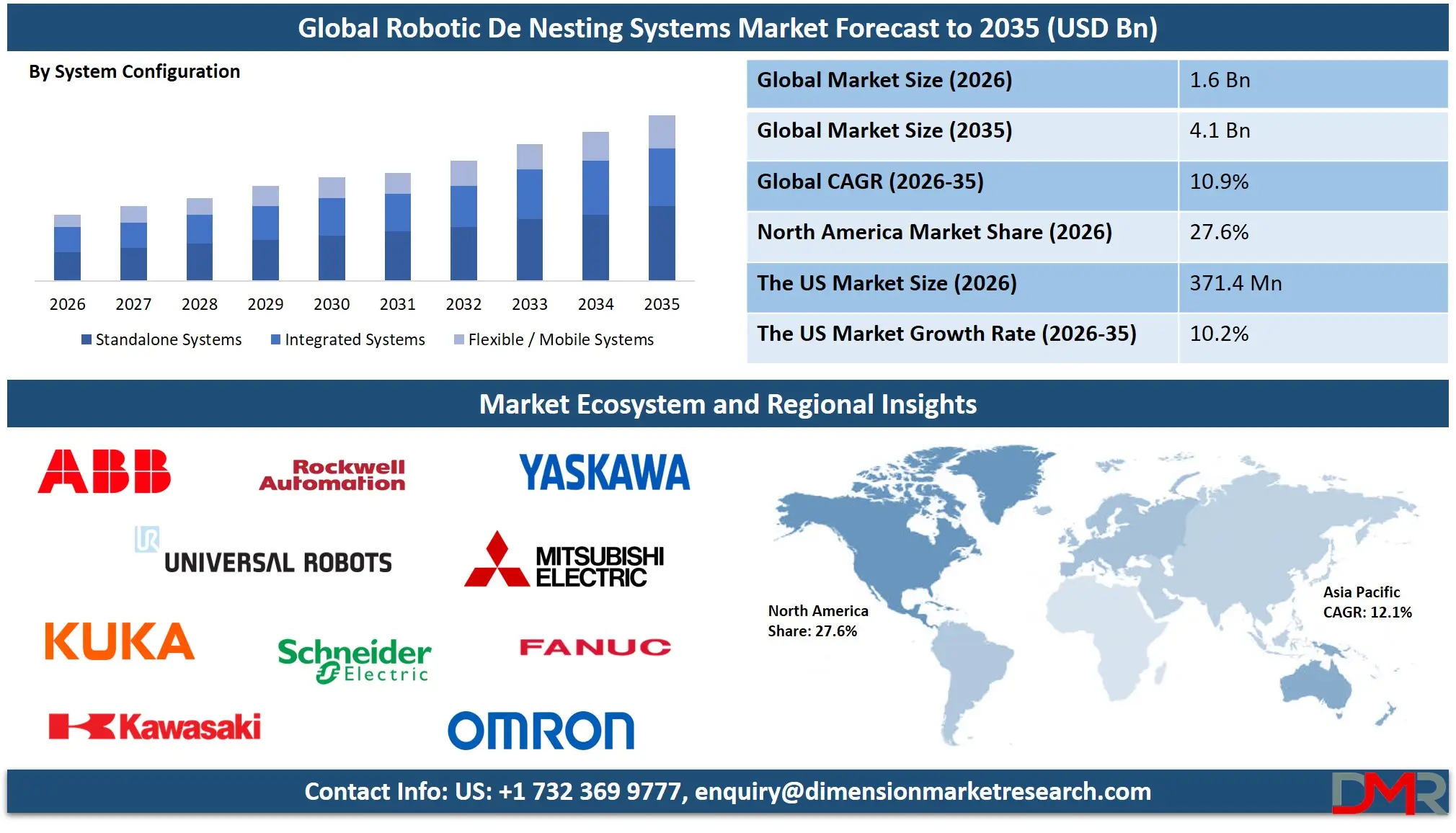

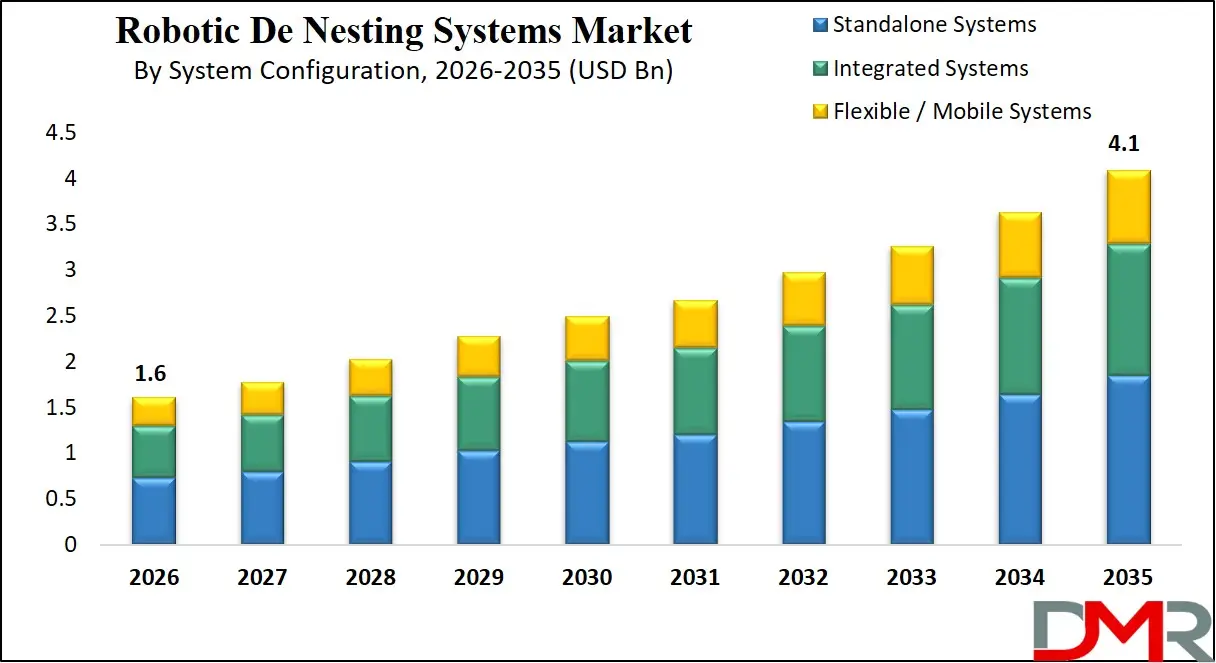

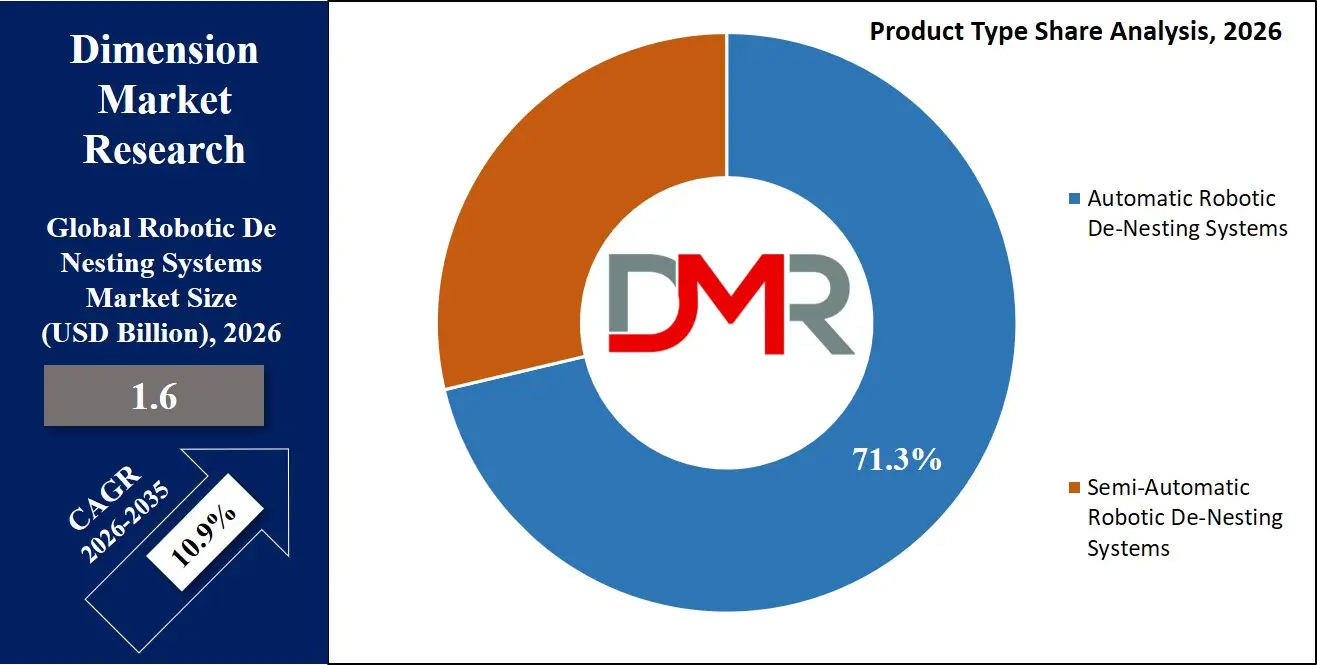

The Global Robotic De-Nesting Systems Market is projected to reach USD 1.6 billion in 2026 and grow at a compound annual growth rate of 10.9% from there until 2035 to reach a value of USD 4.1 billion.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The market's rapid growth is driven by increasing global automation in manufacturing and packaging, stringent workplace safety regulations mandating reduced manual material handling, rising consumer demand for hygienic and damage-free product handling, and the accelerated adoption of Industry 4.0 and smart factory platforms.

Robotic De-Nesting Systems enable intelligent separation and placement of nested products, trays, or containers through advanced vision-guided robotics, adaptive gripper technologies, and real-time path planning algorithms. The model addresses critical industry challenges related to labor shortages, repetitive strain injuries, product contamination risks, and operational inefficiency, supporting manufacturers and logistics providers in achieving superior throughput and quality assurance.

Technological advancements, including AI-powered 3D vision systems, high-speed delta robots, collaborative robot integration, soft gripper end-of-arm tooling, and fully software-defined automation architectures, are transforming the market into a scalable and highly integrated industrial automation ecosystem. Integration of machine learning algorithms for pattern recognition, predictive maintenance scheduling, and adaptive picking strategies is reshaping material handling and production line efficiency standards.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Growing government initiatives mandating workplace ergonomics improvements, industry certifications rewarding automation adoption, and smart manufacturing incentives in industrial corridors further accelerate global adoption. However, barriers such as high initial capital investment in small-to-medium enterprises, complex integration requirements with legacy conveyor systems, varying product dimensional standards across industries, and skilled workforce shortages remain. Despite these limitations, the convergence of collaborative robotics, edge computing, and centralized control architectures positions robotic de-nesting as a central driver of global industrial automation transformation through 2035.

The US Robotic De-Nesting Systems Market

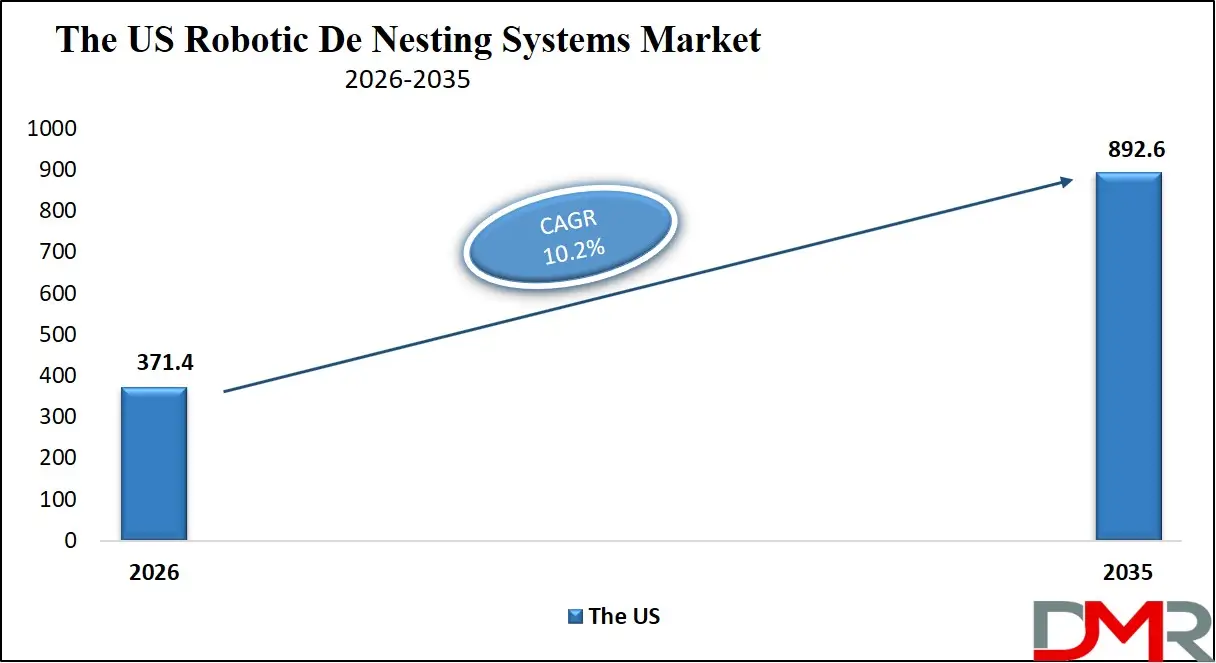

The US Robotic De-Nesting Systems Market is projected to reach USD 371.4 million in 2026 at a compound annual growth rate of 10.2%, reaching USD 892.6 million by 2035.

The U.S. leads global adoption due to its high manufacturing and warehousing automation penetration, OSHA's emphasis on ergonomic hazard reduction, and strong corporate willingness for productivity-enhancing capital equipment. The phase-out of manual de-nesting in food processing and pharmaceutical packaging, coupled with rising e-commerce fulfillment volumes, fuels demand for high-speed vision-guided robotic solutions. Major end-users such as Tyson Foods, PepsiCo, Amazon, and General Motors are integrating robotic de-nesting with conveyor systems and warehouse management software. Tier-1 integrators including ABB, Fanuc, and Rockwell Automation are expanding U.S. engineering centers to support end-user programs.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

U.S. regulatory alignment with ANSI/ISO safety standards for human-robot collaboration, alongside insurance premium reductions for facilities equipped with automated material handling, encourages investment. Training programs and partnerships with Association for Advancing Automation (A3) are emerging to standardize system performance validation and cybersecurity protocols. The rapid rise of AI-powered 3D vision, soft robotic gripping, and cloud-connected predictive maintenance continues to redefine the U.S. industrial automation landscape, positioning the country as a global leader in intelligent robotic de-nesting systems.

The Europe Robotic De-Nesting Systems Market

The Europe Robotic De-Nesting Systems Market is projected to be valued at approximately USD 323.2 million in 2026 and is projected to reach around USD 787.4 million by 2035, growing at a CAGR of about 10.4% from 2026 to 2035. Europe's leadership is anchored by strong regulatory mandates for workplace ergonomics in manufacturing, industry 4.0 funding incentives, and mature automation infrastructure across food, pharma, and automotive sectors.

Countries such as Germany, France, the U.K., Italy, and Spain are widely adopting robotic de-nesting, driven by stringent worker safety requirements, high adoption of collaborative and high-speed delta robot technologies, and government-backed initiatives like EU's Industrial Strategy 2030. German automotive manufacturers and their suppliers are particularly active in developing and deploying vision-guided de-nesting for complex component handling.

Europe's dense industrial environment requiring flexible production changeovers, demand for hygienic design in food processing, and push for energy-efficient automation further drive adoption. Funding through Horizon Europe and national recovery funds supports R&D in AI vision, soft material handling, and human-centric collaborative cells.

High-volume food and beverage production and pharmaceutical serialization programs increasingly deploy 3D vision systems, high-speed picking robots, and anti-microbial robotic solutions. With strong technical standards, digital twin integration, and emphasis on sustainable automation, Europe remains one of the most advanced regions in robotic de-nesting penetration.

The Japan Robotic De-Nesting Systems Market

The Japan Robotic De-Nesting Systems Market is anticipated to be valued at approximately USD 110.4 million in 2026 and is expected to attain nearly USD 289.2 million by 2035, expanding at a CAGR of about 11.3% during the forecast period. Japan's rapidly aging workforce, high labor costs, and leadership in robotics and precision engineering drive high demand for advanced robotic de-nesting systems.

The Ministry of Economy, Trade and Industry (METI) actively supports next-generation automation through robotics subsidy programs, SME automation grants, and integration of robotic de-nesting into food and pharmaceutical production guidelines. Japan's leadership in compact robot design, high-resolution vision sensors, and miniaturized end-effector mechanisms accelerates innovation in space-efficient, high-speed de-nesting cells suitable for urban manufacturing facilities.

Japan's "Society 5.0" industrial vision, driven by companies like Fanuc, Yaskawa, and Denso Wave, integrates IoT-based predictive maintenance, AI-powered object recognition, and adaptive picking algorithms into seamless production ecosystems. Robotic de-nesting units are being deployed in next-generation food processing lines, pharmaceutical packaging, and automotive component manufacturing. Japan's cultural emphasis on precision engineering, combined with advanced automation integration, positions the country as a high-growth innovator in robotic material handling.

Global Robotic De-Nesting Systems Market: Key Takeaways

- Strong Global Market Growth Outlook: The Global Robotic De-Nesting Systems Market is expected to be valued at USD 1.6 billion in 2026 and is projected to reach USD 4.1 billion by 2035, showcasing rapid expansion supported by rising industrial automation and labor cost pressures.

- High CAGR Driven by Technology Migration: The market is expected to grow at an impressive CAGR of 10.9% from 2026 to 2035, fueled by accelerating transition from manual to automated de-nesting, AI-driven vision algorithms, centralized control architectures, and increasing adoption across mid-sized enterprises worldwide.

- Strong Growth Trajectory in the United States: The U.S. Robotic De-Nesting Systems Market stands at USD 371.4 million in 2026 and is projected to reach USD 892.6 million by 2035, expanding at a CAGR of 10.2% due to e-commerce growth, food safety regulations, and high manufacturing automation.

- Asia-Pacific Dominates with Largest Market Share: Asia-Pacific is expected to capture approximately 44.1% of the global market share in 2026, supported by massive manufacturing base, rapid industrialization, and aggressive automation adoption across China, India, and Southeast Asia.

- Rapid Advancement in Automation Technologies: Innovations including AI-powered 3D vision, soft robotic gripping, high-speed delta robots, predictive maintenance algorithms, and software-defined automation are significantly accelerating functionality, flexibility, and scalability of robotic de-nesting systems.

- Growing Safety Mandates Boost Adoption: Rising global mandates for workplace ergonomics, injury reduction, and hygienic handling, coupled with labor shortages and insurance incentives, is driving sustained demand for intelligent, flexible, and high-speed robotic de-nesting solutions.

Global Robotic De-Nesting Systems Market: Use Cases

- Food Tray De-Nesting: High-speed robotic systems automatically separate and place nested food trays onto conveyor lines for filling, ensuring hygienic handling and reducing manual labor.

- Pharmaceutical Blister Pack Feeding: Vision-guided robots precisely de-nest pharmaceutical blister packs for packaging, maintaining cleanroom compatibility and product integrity.

- Automotive Component Handling: Heavy-duty robotic cells de-nest stacked metal or plastic automotive components for assembly line feeding, reducing ergonomic strain.

- Electronics Tray Denesting: Precision robots handle delicate electronic components from nested trays for PCB assembly, preventing damage and ensuring accurate placement.

- Warehouse Case Depalletizing: Mobile robotic systems de-nest mixed product cases from pallets for order fulfillment in distribution centers.

- Flexible Packaging Changeover: Semi-automatic systems enable quick changeovers between different product formats in high-mix production environments.

Global Robotic De-Nesting Systems Market: Stats & Facts

U.S. Bureau of Labor Statistics (BLS)

- Approximately 50% of workplace musculoskeletal disorders are related to repetitive manual material handling tasks.

- The injury rate per 10,000 full-time workers in manufacturing is about three times higher for manual handling than automated operations.

- About 76% of warehouse injuries occur during manual lifting and stacking activities.

- Back injuries and repetitive strain account for a substantial share of manufacturing compensation claims.

- Ergonomic hazards contribute to over 30% of lost workday cases in food processing.

Occupational Safety and Health Administration (OSHA), U.S. Department of Labor

- In 2022, U.S. manufacturing recorded over 400,000 workplace injuries.

- Nearly half of all manufacturing injuries involve manual material handling.

- OSHA updated ergonomic guidelines in 2022 to encourage automation of repetitive tasks including de-nesting.

- Ergonomic hazard complaints generated over 5,700 industry comments in regulatory review.

- Manual handling is identified as a key factor in injury severity.

Food and Drug Administration (FDA)

- In 2016, only 1 in 5 food processing facilities had automated primary packaging handling.

- By 2023–2024, approximately 50% of inspected facilities had implemented automated tray handling systems.

- Facilities with automated handling show about 19% fewer product contamination incidents.

- Automated facilities show approximately 23% fewer worker compensation claims.

- More than 80% of facilities before 2016 had manual tray handling with hygiene risks.

European Agency for Safety and Health at Work (EU-OSHA)

- The European Union recorded approximately 3.1 million work-related musculoskeletal disorders annually.

- A significant proportion of workplace injuries in the EU occur during manual lifting and repetitive tasks.

- The EU's Occupational Safety and Health Directive mandates ergonomic risk reduction from 2022 onward.

- Automated material handling is promoted under EU workplace innovation programs.

International Federation of Robotics (IFR)

- Global industrial robot installations exceeded 550,000 units in 2023.

- Material handling applications account for the majority share of robot installations.

- More than 50 countries have industrial automation incentive programs.

- Collaborative robot installations grew by over 25% annually in handling applications.

- Asia-Pacific accounts for the largest share of global robot installations at approximately 44% of total volume.

International Energy Agency (IEA)

- Global industrial electricity demand exceeded 12,000 TWh in 2023.

- Industrial automation represents about 18% of manufacturing energy optimization potential.

- Robotic systems significantly improve energy efficiency compared to manual operations.

- Industry 4.0 adoption supports increased implementation of energy-efficient automation.

Japan Ministry of Economy, Trade and Industry (METI)

- Japan records a significant share of workplace injuries in manufacturing during manual handling.

- Robotic automation is promoted under Japanese industrial safety programs.

- Japan's robotics market grew at over 11% annually, driven by labor substitution needs.

World Health Organization (WHO)

- Approximately 1.19 million people globally suffer work-related injuries annually from manual handling.

- Musculoskeletal disorders are among the leading causes of work disability globally.

Global Robotic De-Nesting Systems Market: Market Dynamic

Driving Factors in the Global Robotic De-Nesting Systems Market

Stringent Workplace Safety Regulations and Labor Shortages

The growing global mandate for ergonomic injury reduction and worker protection is a major driver for robotic de-nesting adoption. Regulatory frameworks in Europe, Japan, China, and increasingly the U.S. now require or incentivize automation of repetitive manual handling tasks. End-users integrate robotic systems to achieve safety compliance, reduce liability, increase brand reputation, and address critical labor shortages across manufacturing and logistics. Asia-Pacific's rapid industrialization coupled with rising labor costs in China and India further accelerates adoption across the region.

Technology Migration and Cost Downscaling

Robotic de-nesting benefits heavily from rapid progress in vision system cost reduction, miniaturized controllers, AI algorithms, and standardized automation interfaces. Advanced systems feature 3D cameras, single-chip controllers, adaptive grippers, and lightweight carbon-fiber arms. These innovations enable robotic technology to cascade from multinational corporations to SME facilities. The convergence of de-nesting with MES data and cloud-based predictive maintenance further enhances functionality, making robotic automation a democratized productivity tool rather than exclusive large-scale option.

Restraints in the Global Robotic De-Nesting Systems Market

High Capital Investment in SME Segment

The significant upfront cost of robotic de-nesting systems, including robots, vision systems, grippers, and validation cycles, limits adoption in small-to-medium enterprises and price-sensitive emerging markets. Many end-users face budget trade-offs between automation and other capital investments. Additionally, post-installation maintenance costs and skilled programmer requirements create operational friction.

Integration Complexity and Standardization Gaps

Integration requirements, communication protocols, and safety certifications vary widely across different conveyor systems, product formats, and industry verticals, creating engineering complexity. Issues include different dimensional standards, speed requirements, and hygienic design specifications. Furthermore, retrofitting robotic de-nesting in legacy production lines often requires full control system upgrades. Variability in product packaging, weight assumptions, and changeover requirements further limits platform commonality.

Opportunities in the Global Robotic De-Nesting Systems Market

Expansion into Mid-Market and Emerging Regions

Emerging markets represent major growth opportunities due to rapid industrialization, localization of robot component supply chains, and increasing food safety and pharmaceutical quality programs. Countries in Asia-Pacific, Latin America, and MEA are launching manufacturing modernization initiatives where robotic de-nesting can ensure compliance and quality. Local system integration partnerships, simplified robot variants, and government SME automation subsidies can improve accessibility, driving the next wave of market expansion. With Asia-Pacific holding the highest CAGR of 12.1%, the region presents particularly strong opportunities for market penetration.

Software-Defined Automation and Function-on-Demand

The integration of de-nesting functions into centralized production control systems not only for picking but for production tracking, quality inspection, and predictive maintenance creates new value streams. System integrators can offer vision algorithms as software upgrades, remote monitoring subscriptions, and performance analytics, transforming automation from fixed capital equipment into intelligent, upgradable platforms that increase lifetime value.

Trends in the Global Robotic De-Nesting Systems Market

AI-Powered 3D Vision and Adaptive Picking

The rise of AI-powered 3D vision systems with high-resolution depth sensing and real-time object recognition is gaining traction. These systems enable handling of randomly oriented, mixed-size products without pre-teaching, reducing changeover time and increasing flexibility.

Collaborative and Mobile Robot Integration

Integration of collaborative robots and autonomous mobile robots for flexible, human-safe de-nesting applications is accelerating. Mobile manipulators can move between production lines, enabling cost-effective automation for facilities with fluctuating volume requirements.

Global Robotic De-Nesting Systems Market: Research Scope and Analysis

By Product Type Analysis

Automatic Robotic De-Nesting Systems are projected to dominate the Product Type segment of the Global Robotic De-Nesting Systems Market. This dominance is driven by the fundamental shift from manual or semi-automated handling to fully autonomous, high-speed production lines. Automatic systems operate continuously without human intervention, processing inputs from multiple sensors including 3D cameras, proximity sensors, and production line sensors while executing real-time algorithms for path planning, collision avoidance, and gripper control.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

As production demands increase for speed, accuracy, and hygiene, the role of fully automatic systems as the productivity core becomes increasingly decisive. The technology for automatic systems is also the most rapidly evolving, transitioning from pneumatic to electric servo-driven grippers with integrated vision and force sensing. While semi-automatic systems provide flexibility for low-volume applications, automatic systems remain the high-value productivity layer, capturing an increasing share of system investment. Its role as the backbone for lights-out manufacturing and integration with MES/ERP systems secures the automatic systems' leading market position throughout the forecast period.

Semi-Automatic Robotic De-Nesting Systems constitute the essential second product segment. These systems require operator assistance for changeovers, exception handling, or low-volume runs. They are widely adopted in SMEs and facilities with high product mix where full automation is not economically justified. Technology is transitioning to quick-change tooling and user-friendly interfaces for rapid manual intervention.

By System Configuration Analysis

Integrated Systems are projected to dominate the System Configuration segment of the Global Robotic De-Nesting Systems Market. Integrated systems are designed to work seamlessly with upstream and downstream equipment including conveyors, palletizers, fillers, and packaging machines through centralized control architecture. Their dominance stems from an unparalleled value proposition: superior overall line efficiency achieving 30 percent or greater throughput improvement compared to standalone cells, exceptional coordination enabling just-in-time material flow, and single-source responsibility for system performance. By integrating advanced conveyor tracking, vision-guided picking, and coordinated motion control, these systems deliver synchronized material flow, minimal accumulation buffers, and real-time production adaptability. The driving forces behind market leadership are tri-fold: the complete transition from island automation to line integration across food, pharma, and automotive industries; the declining cost of industrial communication networks now below USD 500 per node; and the growing end-user expectation of single-vendor accountability across production lines.

As Industry 4.0 prioritizes data continuity and end-to-end automation, the economic case for integrated over standalone systems becomes compelling, solidifying integrated configurations as the cornerstone of modern production architecture.

Standalone Systems constitute the second-largest configuration segment, deployed in applications where integration with existing lines is complex or where systems serve as independent work cells for specific processes. Flexible/Mobile Systems represent the fastest-growing segment, with autonomous mobile robots equipped with de-nesting arms gaining adoption in dynamic warehouse environments requiring reconfigurable automation.

By Application Analysis

Food and Beverage is poised to be the largest and most dominant application segment in the Global Robotic De-Nesting Systems Market, driven by powerful hygiene regulations and high-volume production requirements. The ability to automatically de-nest trays, containers, and packaging materials without human contact addresses fundamental industry needs for contamination prevention, traceability, and sanitation compliance. This functionality, once exclusive to large multinational processors, is cascading to regional producers through cost-optimized vision systems and hygienic robot designs. The sector is also acutely affected by FDA and EU food safety regulations increasingly mandating automated handling in primary packaging, making robotic de-nesting a strategic investment for compliance. Beyond regulatory compliance, robotic systems offer processors visible quality improvements through consistent handling and reduced product damage. From protein processing to bakery and beverage production, the competitive pressure in automation deployment makes robotic de-nesting not merely advantageous but increasingly essential for maintaining market relevance and operational excellence.

Packaging ranks as the second-largest application segment, distinguished by high-speed requirements and diverse product formats. This enables applications including secondary packaging de-nesting, case erecting support, and multi-pack collation. Pharmaceuticals and Automotive represent specialized high-growth segments with unique requirements for cleanroom compatibility and heavy-duty precision respectively. Electronics and Other applications including consumer goods complete the market landscape.

By Distribution Channel Analysis

Direct Sales is anticipated to dominate the Distribution Channel segment as the primary channel for complex, customized robotic de-nesting solutions requiring extensive engineering consultation, site assessment, and integration planning. Robotic de-nesting systems remain primarily direct-sold due to complex application engineering involving facility-specific layout constraints, product dimensional analysis, and integration dependencies. The customization of gripper designs, vision algorithms, and control software necessitates manufacturer or authorized integrator-level engineering coordination that standard channels cannot replicate. Additionally, the trend toward turnkey automation solutions and long-term service agreements further consolidates manufacturer control over system specification and support. Distributors represent a significant channel for standardized, lower-complexity systems and spare parts, particularly serving SME customers. Online Sales and Other channels represent emerging but modest segments, primarily focused on standardized components, spare parts, and basic vision systems.

By End-User Analysis

Manufacturing is projected to dominate the End-User segment, accounting for the majority of global robotic de-nesting system volume. Food and beverage manufacturing, specifically, represents the highest attach rate for hygienic robotic de-nesting, particularly in developed regions where food safety regulations are stringent. Pharmaceutical manufacturing contributes premium system demand for cleanroom-compatible, validation-ready solutions. Automotive manufacturing drives adoption of heavy-duty systems for component handling.

Logistics and Warehousing represent the highest growth end-user segments: e-commerce fulfillment and distribution center automation universally specify robotic de-nesting for case handling and order fulfillment to maximize throughput and reduce labor dependency. These end-users are experiencing accelerated adoption due to labor shortages and the need for 24/7 operation capabilities.

The Global Robotic De-Nesting Systems Market Report is segmented on the basis of the following:

By Product Type

- Automatic Robotic De-Nesting Systems

- Semi-Automatic Robotic De-Nesting Systems

By System Configuration

- Standalone Systems

- Integrated Systems

- Flexible / Mobile Systems

By Application

- Food and Beverage

- Pharmaceuticals

- Packaging

- Automotive

- Electronics

- Others

By Distribution Channel

- Direct Sales

- Distributors

- Online Sales

- Others

By End-User

- Manufacturing

- Logistics

- Warehousing

- Others

Impact of Artificial Intelligence in the Global Robotic De-Nesting Systems Market

- AI for Adaptive Picking: AI analyzes 3D vision data to recognize randomly oriented nested products, enabling robots to pick items without pre-programming or fixturing.

- AI-Driven Object Classification: Neural networks distinguish between different product types, orientations, and nesting patterns, adjusting gripper selection and path planning accordingly.

- Visual Recognition & Product Memory: AI algorithms recognize frequently handled products and recall optimal picking strategies, gripper configurations, and placement positions, enabling continuous learning and performance improvement.

- AI-Based Predictive Maintenance: Machine learning models predict gripper wear, vision system calibration drift, and actuator performance degradation, scheduling maintenance before failure occurs.

- Fleet Learning for Continuous Optimization: AI systems aggregate edge data from thousands of installations to continuously improve object recognition models, picking strategies for different product geometries, and changeover optimization, building a material handling intelligence knowledge base that enhances global system performance over time.

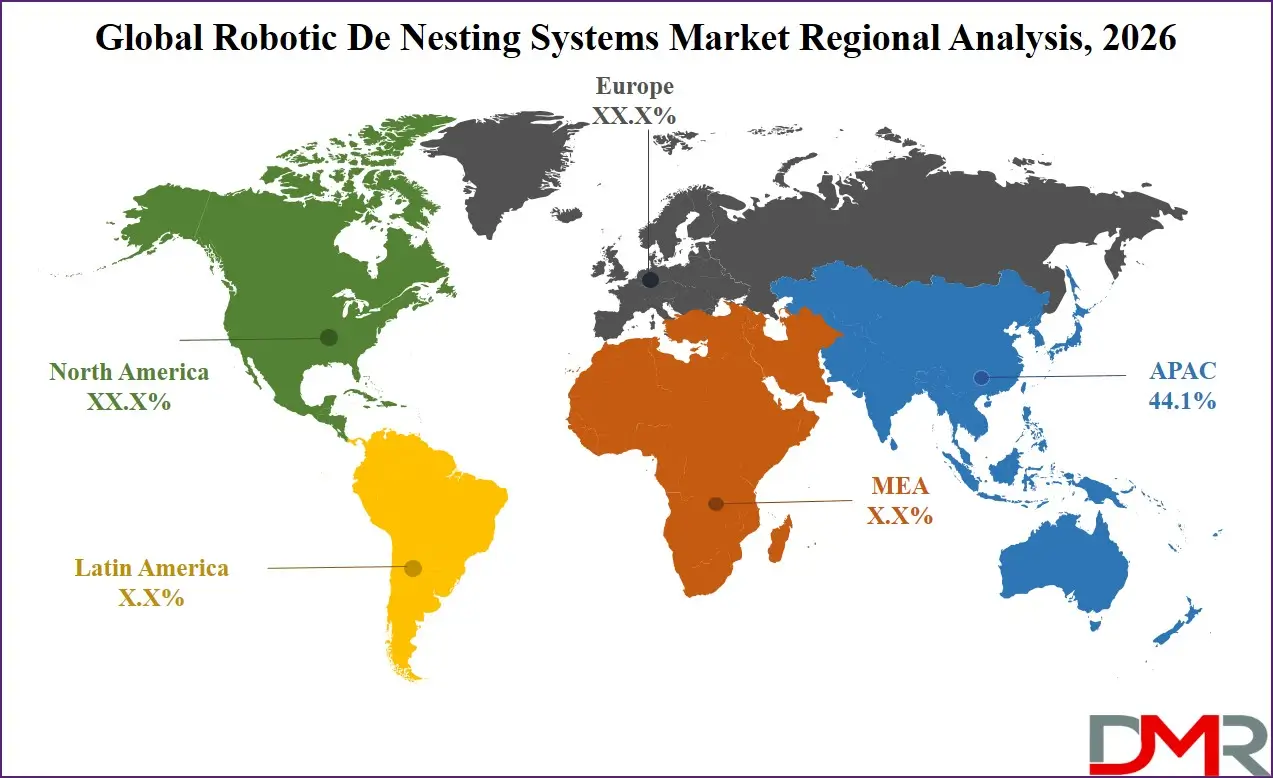

Global Robotic De-Nesting Systems Market: Regional Analysis

Region with the Largest Revenue Share

Asia-Pacific is projected to dominate the Global Robotic De-Nesting Systems Market with 44.1% of market share by the end of 2026, owing to its massive manufacturing base, rapid industrialization, and aggressive automation adoption. China, India, Japan, South Korea, and ASEAN countries are rapidly integrating robotic de-nesting into food processing, electronics, and automotive production, supported by government incentives and rising labor costs. The region's position as the world's manufacturing hub, combined with localization of robot component manufacturing and favorable trade policies, creates the largest market opportunity. Supportive government initiatives including China's "Made in China 2025" and India's Production Linked Incentive schemes further solidify Asia-Pacific's leadership position.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Region with the Highest CAGR

Asia-Pacific also holds the highest CAGR of 12.1% and is poised to achieve the most rapid market share growth due to accelerating automation adoption across emerging economies, rising labor costs, and increasing focus on export quality standards. Countries like Vietnam, Thailand, Indonesia, and India are experiencing particularly strong growth as multinational manufacturers expand automation in regional production hubs. The region's cost sensitivity is being addressed through local robot manufacturing, domestic vision system development, and partnerships between global suppliers and local integrators. This, combined with the world's largest and fastest-growing manufacturing output, positions APAC as both the largest and fastest-growing market for robotic de-nesting systems.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Global Robotic De-Nesting Systems Market: Competitive Landscape

The Global Robotic De-Nesting Systems Market is moderately consolidated, featuring a mix of global industrial robotics incumbents, automation system integrators, and vision technology firms. Leading robotics players Fanuc, ABB, Yaskawa, KUKA, and Kawasaki are leveraging their expertise in robot mechanics, control systems, and programming to develop integrated de-nesting solutions. Pure-play automation specialists such as Codian Robotics, Schneider Electric, and Omron are driving market dynamics with cost-competitive delta robot systems focused on high-speed applications.

AI and software specialists like Cognex (for vision systems), Keyence (for 3D sensors), and Siemens (for control platforms) play increasingly influential roles as enablers and technology partners. End-of-arm tooling leaders Schunk, Festo, and Piab are critical to gripper technology roadmaps. System integrators including Rockwell Automation and Durr are essential for complex line integration. Traditional end-users are also increasing in-sourcing of programming capability, aiming to optimize system performance internally. Asia-based players are gaining market share rapidly, capitalizing on the region's 44.1% global share and 12.1% growth rate.

Some of the prominent players in the Global Robotic De-Nesting Systems Market are:

- ABB Ltd.

- FANUC Corporation

- KUKA AG

- Yaskawa Electric Corporation

- Kawasaki Heavy Industries, Ltd.

- Schneider Electric SE

- Universal Robots A/S

- Stäubli International AG

- Omron Corporation

- Mitsubishi Electric Corporation

- Bosch Rexroth AG

- Rockwell Automation, Inc.

- DENSO Robotics

- Comau S.p.A.

- Sepro Group

- BluePrint Automation (BPA)

- JLS Automation

- Brenton Engineering (ProMach)

- FlexLink (Coesia Group)

- Schubert Group

- Other Key Players

Recent Developments in the Global Robotic De-Nesting Systems Market

- March 2026: ABB and Nvidia announced a partnership to develop AI-enabled autonomous industrial robots, integrating Nvidia's Omniverse simulation platform with ABB's RobotStudio software to train robots in realistic virtual environments before deployment in factories.

- November 2025: Cognex Corporation launched its AI-powered SLX machine-vision solutions, designed to simplify deployment of automated inspection and robotic guidance systems across manufacturing applications. The new system integrates 3D depth sensing and adaptive AI algorithms, enabling faster and more accurate pick-and-place operations in complex production lines.

- September 2025: ABB launched OmniCore EyeMotion, a vision-enabled system that allows robots powered by the OmniCore platform to recognize surroundings using cameras or sensors and adapt in real time in manufacturing and logistics environments.

- June 2025: Rockwell Automation introduced OptixEdge, an industrial edge gateway combining machine-vision processing with automation networking to enable distributed intelligence and real-time data analysis across manufacturing operations.

- April 2025: Cognex Corporation introduced the In-Sight L38 AI-powered 3D vision system, combining AI, 2D, and 3D imaging technologies to improve inspection, measurement, and automation capabilities in manufacturing environments.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 1.6 Bn |

| Forecast Value (2035) |

USD 4.1 Bn |

| CAGR (2026–2035) |

10.9% |

| The US Market Size (2026) |

USD 371.4 Mn |

| Historical Data |

2020 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Product Type (Automatic Robotic De-Nesting Systems, Semi-Automatic Robotic De-Nesting Systems), By System Configuration (Standalone Systems, Integrated Systems, Flexible / Mobile Systems), By Application (Food and Beverage, Pharmaceuticals, Packaging, Automotive, Electronics, Others), By Distribution Channel (Direct Sales, Distributors, Online Sales, Others), By End-User (Manufacturing, Logistics, Warehousing, Others) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia- Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

ABB Ltd., FANUC Corporation, KUKA AG, Yaskawa Electric Corporation, Kawasaki Heavy Industries, Ltd., Schneider Electric SE, Universal Robots A/S, Stäubli International AG, Omron Corporation, Mitsubishi Electric Corporation, Bosch Rexroth AG, Rockwell Automation, Inc., DENSO Robotics, Comau S.p.A., Sepro Group, BluePrint Automation (BPA), JLS Automation, Brenton Engineering (ProMach), FlexLink (Coesia Group), Schubert Group and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Robotic De-Nesting Systems Market?

▾ The Global Robotic De-Nesting Systems Market size is estimated to have a value of USD 1.6 billion in 2026 and is expected to reach USD 4.1 billion by the end of 2035.

What is the growth rate in the Global Robotic De-Nesting Systems Market in 2026?

▾ The market is growing at a CAGR of 10.9% over the forecasted period of 2026.

What is the size of the US Robotic De-Nesting Systems Market?

▾ The US Robotic De-Nesting Systems Market is projected to be valued at USD 371.4 million in 2026. It is expected to witness subsequent growth in the upcoming period as it holds USD 892.6 billion in 2035 at a CAGR of 10.2%.

Which region accounted for the largest Global Robotic De-Nesting Systems Market?

▾ Asia Pacific is expected to have the largest market share in the Global Robotic De-Nesting Systems Market with a share of about 44.1% in 2026.

Who are the key players in the Global Robotic De-Nesting Systems Market?

▾ Some of the major key players in the Global Robotic De-Nesting Systems Market are ABB Ltd., FANUC Corporation, KUKA AG, Kawasaki Heavy Industries, Ltd., Schneider Electric SE, and many others.