Market Overview

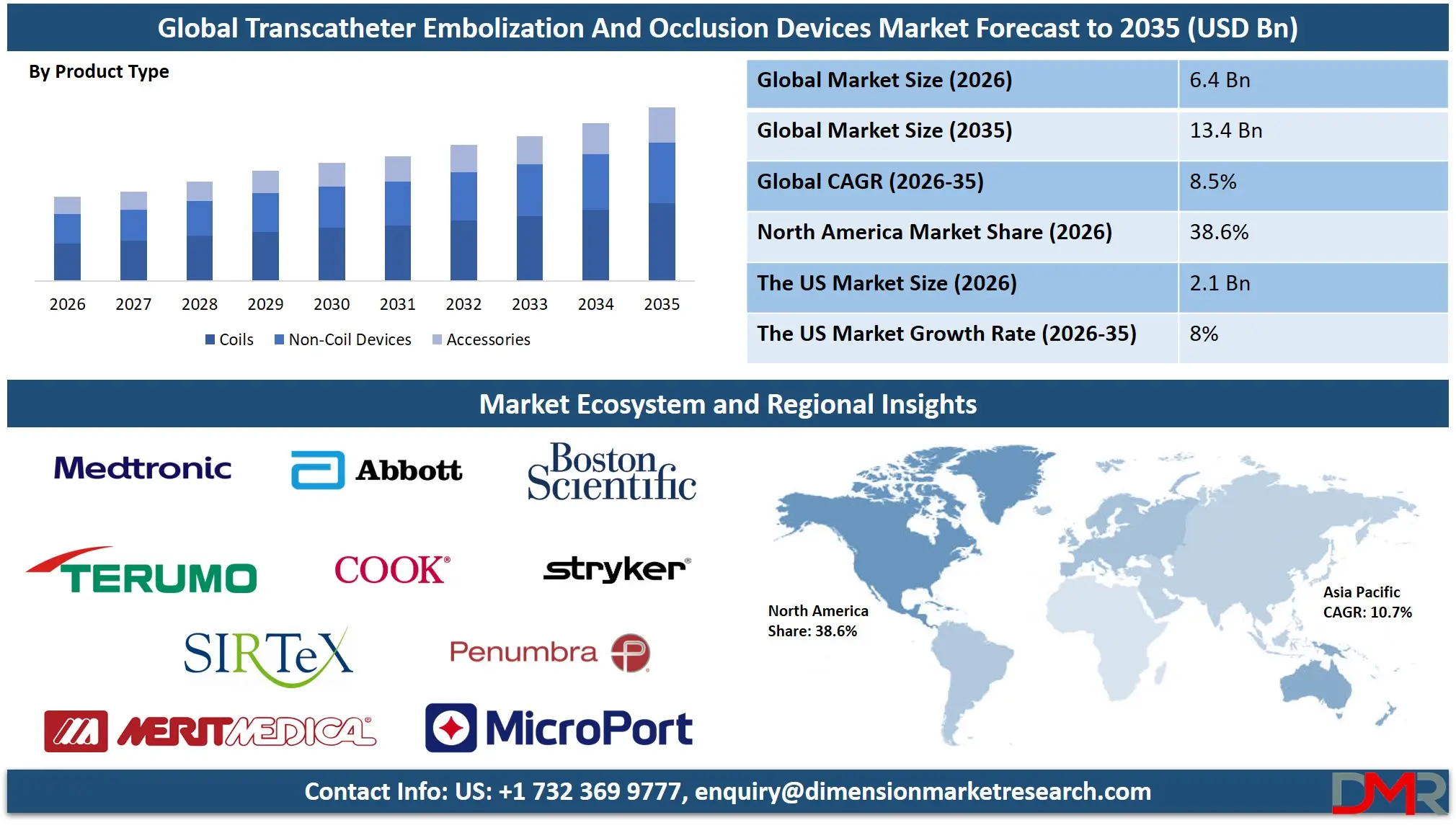

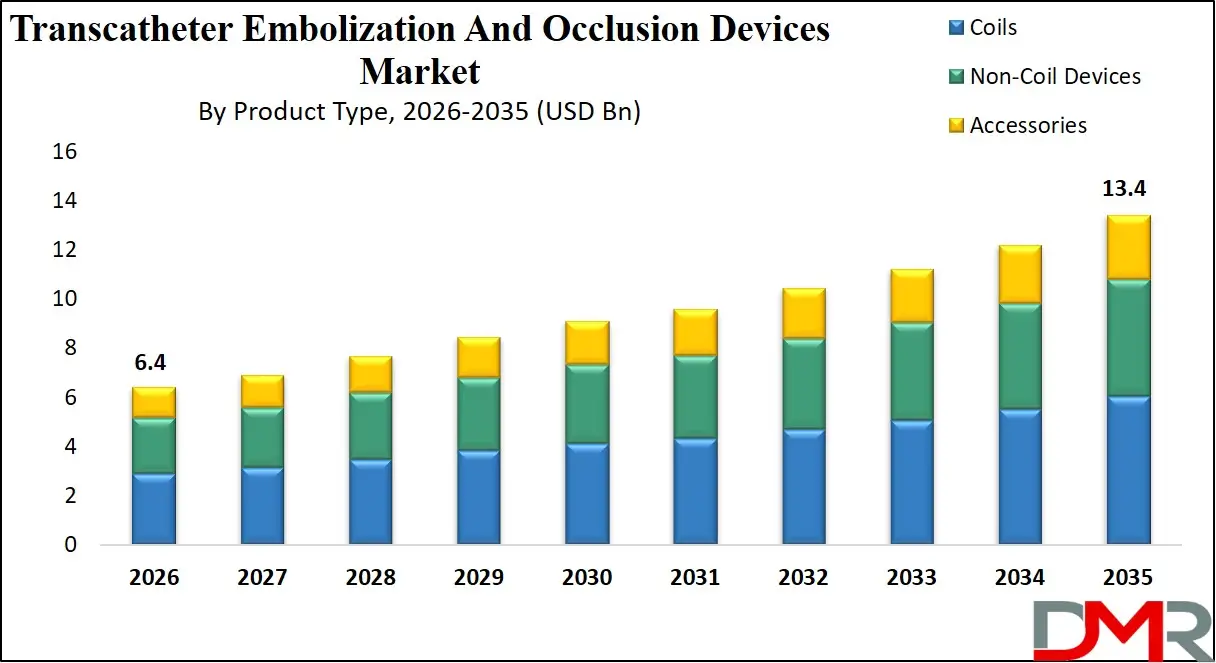

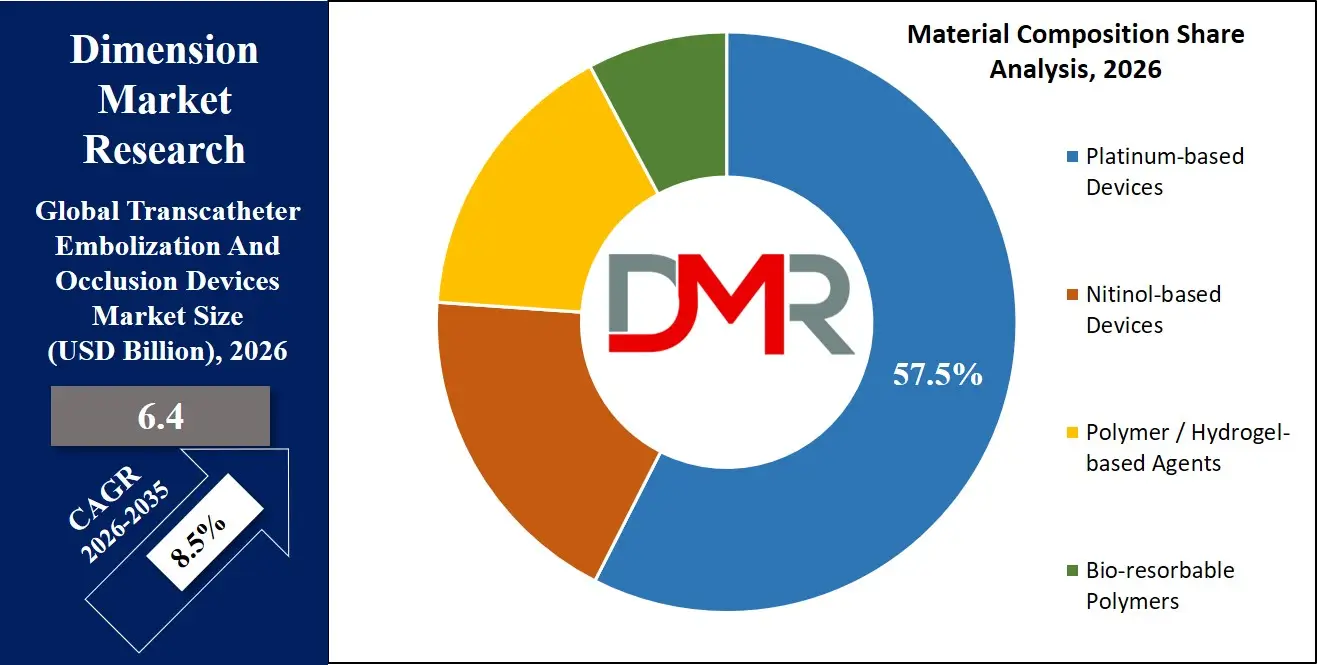

The Global Transcatheter Embolization And Occlusion Devices Market is projected to reach USD 6.4 billion in 2026 and grow at a compound annual growth rate of 8.5% from there until 2035 to reach a value of USD 13.4 billion. This robust growth trajectory is fueled by the accelerating adoption of minimally invasive interventional procedures, rising prevalence of cancer and vascular diseases worldwide, aging population trends, and increasing success rates of embolization therapies across both developed and emerging healthcare markets.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Rising incidences of hepatocellular carcinoma, uterine fibroids, cerebral aneurysms, and gastrointestinal bleeding are compelling patients and physicians to seek advanced endovascular treatments, thereby driving demand for high-precision embolization and occlusion devices. The rapid expansion of interventional radiology departments, hybrid operating rooms, and specialized cancer centers is significantly increasing requirements for reliable, sterile, and precisely deliverable occlusion systems.

Additionally, growing government initiatives and insurance coverage expansions for minimally invasive procedures in countries across North America, Europe, and the Asia-Pacific are further accelerating market adoption. Healthcare providers are increasingly integrating coils, liquid embolics, flow diverting devices, and embolization particles designed to maximize target vessel occlusion while minimizing procedure time and patient complications.

Technological advancements in device design, including detachable coil systems with enhanced controllability, radiopaque liquid embolics for real-time visualization, shape-memory nitinol frameworks, and bioresorbable polymer technologies, are enabling interventionalists to perform safer and more effective embolization. As interventional oncology grows and access to endovascular therapies expands globally, the Transcatheter Embolization And Occlusion Devices Market is expected to witness sustained strong growth through 2035, driven by clinical excellence prioritization and minimally invasive surgery awareness initiatives.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Growing public-private partnerships promoting interventional oncology programs, stroke center certifications, and peripheral vascular disease management further accelerate global adoption. However, barriers such as high procedure costs, limited reimbursement in certain regions, stringent regulatory approval processes for medical devices, and a shortage of trained interventional specialists remain. Despite these limitations, the convergence of precision engineering, imaging advancements, and minimally invasive surgical techniques positions transcatheter embolization devices as a critical component of global interventional medicine through 2035.

The US Transcatheter Embolization And Occlusion Devices Market

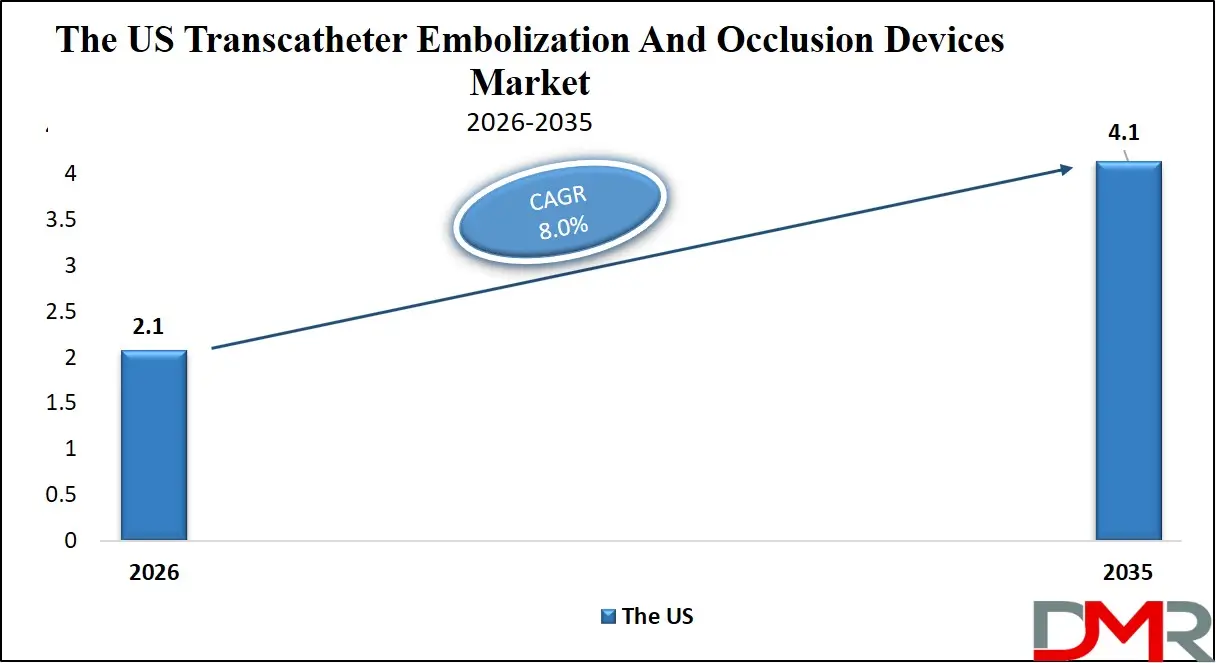

The US Transcatheter Embolization And Occlusion Devices Market is projected to reach USD 2.1 billion in 2026 at a compound annual growth rate of 8.0%, reaching USD 4.1 billion in 2035. The U.S. leads global adoption due to its mature interventional radiology infrastructure, high per capita healthcare spending, and supportive regulatory environment from bodies like the FDA and major medical societies.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The proliferation of hybrid operating rooms, hospital-based interventional suites, and increasing acceptance of minimally invasive procedures fuel demand for high-quality embolization devices. Major hospital systems and cancer centers such as HCA Healthcare, Johns Hopkins, and the Cleveland Clinic are integrating advanced coil systems, liquid embolics, and flow diverting devices to optimize outcomes during oncologic, neurologic, and peripheral vascular interventions.

U.S. regulatory support for interventional procedure accessibility, alongside Medicare coverage expansions for minimally invasive treatments, encourages investment in advanced embolization technologies. The market is witnessing a shift toward specialized device designs, including detachable coils with complex three-dimensional configurations, radiopaque liquid embolic agents, and precision-calibrated embolization particles, enhancing procedural success and reducing recanalization rates. The rise of interventional oncology has further intensified the focus on super selective catheterization and targeted tumor devascularization, positioning the U.S. as a critical innovator in this space.

The Europe Transcatheter Embolization And Occlusion Devices Market

The Europe Transcatheter Embolization And Occlusion Devices Market is estimated to be valued at USD 1.8 billion in 2026 and is further anticipated to reach USD 3.4 billion by 2035 at a CAGR of 7.6%. Europe's leadership is anchored by its comprehensive healthcare coverage under national health systems, particularly in countries with progressive interventional medicine policies and government-funded cancer and stroke programs.

Countries such as Germany, France, the U.K., Italy, and Spain are widely adopting embolization procedures, driven by high success rates in leading European interventional centers and favorable regulatory frameworks. Germany, in particular, has emerged as a European hub for interventional oncology due to its advanced healthcare infrastructure and high concentration of world-class vascular centers. The U.K.'s NICE guidance and the EU's evolving Medical Device Regulation (MDR) further necessitate high-quality, traceable, and clinically validated embolization devices.

Europe's high acceptance of minimally invasive approaches for uterine fibroid embolization, liver tumor treatment, and cerebral aneurysm repair drives the demand for reliable, sterile, and single-use embolization devices designed to maximize clinical efficacy while ensuring patient safety. With a sophisticated interventional medicine community and regulatory landscape prioritizing clinical outcomes and patient safety, Europe remains a highly advanced and essential region for embolization device manufacturers.

The Japan Transcatheter Embolization And Occlusion Devices Market

Japan Transcatheter Embolization And Occlusion Devices Market is estimated to reach USD 430.2 million in 2026 and is forecast to expand at a CAGR of 6.8% through 2035, reaching nearly USD 780.4 million by 2035, driven by the increasing adoption of interventional radiology techniques and the growing number of specialized treatment centers. Japan's aging population, high prevalence of liver cancer and vascular disease, and government push for minimally invasive treatment options are driving the adoption of advanced embolization technologies, making these devices a cornerstone of national interventional medicine programs.

The Ministry of Health, Labour and Welfare (MHLW) actively supports interventional procedure coverage under national health insurance, with expanded reimbursement policies for embolization procedures and associated medical devices. Japan's leadership in precision medical device manufacturing and rigorous quality standards provides a robust foundation for advanced embolization technologies, including detachable microcoils, liquid embolic systems, and flow diversion devices.

Japan's concept of "supporting healthy aging," driven by national policy initiatives and integrated healthcare delivery, integrates embolization procedures into mainstream oncologic and vascular practice. Hospitals are deploying advanced embolization devices to optimize outcomes in Japan's rapidly growing interventional sector, serving both elderly patients with age-related vascular conditions and younger patients undergoing fertility-preserving uterine fibroid embolization. Japan's cultural emphasis on precision, safety, and minimally invasive techniques positions it as a high-growth, quality-focused market for embolization solutions.

Global Transcatheter Embolization And Occlusion Devices Market: Key Takeaways

- Strong Global Market Growth Outlook: The Global Transcatheter Embolization And Occlusion Devices Market is expected to be valued at USD 6.4 billion in 2026 and is projected to reach USD 13.4 billion by 2035, showcasing rapid expansion supported by rising demand for minimally invasive interventional procedures and advanced endovascular technologies.

- High CAGR Driven by Interventional Procedure Adoption: The market is expected to grow at an impressive CAGR of 8.5% from 2026 to 2035, fueled by accelerating cancer incidence rates, increasing prevalence of vascular diseases, and growing awareness of minimally invasive treatment options worldwide.

- Strong Growth Trajectory in the United States: The U.S. Transcatheter Embolization And Occlusion Devices Market stands at USD 2.1 billion in 2026 and is projected to reach USD 4.1 billion by 2035, expanding at a CAGR of 8.0% due to high interventional radiology adoption, favorable reimbursement policies, and advanced healthcare infrastructure.

- Regional Dominance: North America is expected to capture approximately 38.6% of the global market share in 2026, supported by high procedure volumes, favorable reimbursement policies, and concentration of leading interventional centers and device innovators.

- Rapid Advancement in Embolization Technologies: Innovations including detachable coil systems with enhanced controllability, radiopaque liquid embolics for real-time visualization, shape-memory nitinol frameworks, precision-calibrated embolization particles, and bioresorbable polymer technologies are significantly improving procedural success rates and patient outcomes.

- Growing Disease Prevalence Boosts Adoption: Rising global incidence of cancer, particularly hepatocellular carcinoma, along with increasing prevalence of cerebral aneurysms, peripheral vascular disease, and uterine fibroids, is driving sustained demand for high-quality transcatheter embolization and occlusion devices.

Global Transcatheter Embolization And Occlusion Devices Market: Use Cases

- Interventional Oncology: Interventional radiologists use embolization devices including particles, drug-eluting beads, and liquid embolics for transarterial chemoembolization (TACE) and radioembolization of primary and metastatic liver tumors, achieving targeted tumor devascularization.

- Cerebral Aneurysm Repair: Neurointerventional specialists deploy detachable coils and flow diverting devices for endovascular treatment of cerebral aneurysms, promoting thrombosis and excluding aneurysms from circulation while preserving parent vessel patency.

- Uterine Fibroid Embolization: Interventional radiologists utilize calibrated embolization particles to occlude uterine artery branches supplying symptomatic fibroids, inducing fibroid necrosis while preserving healthy myometrial tissue.

- Peripheral Vascular Occlusions: Physicians employ coil systems and vascular plugs for embolization of peripheral arteriovenous malformations, type II endoleaks, and traumatic vascular injuries, achieving hemostasis or flow redirection.

- Gastrointestinal Bleeding Management: Interventionalists utilize coil systems and particles for super selective embolization of bleeding arteries in cases of upper and lower gastrointestinal hemorrhage, achieving rapid hemostasis without surgical intervention.

Global Transcatheter Embolization And Occlusion Devices Market: Stats & Facts

World Health Organization (WHO)

- Approximately 10 million cancer deaths occur globally each year, with many patients eligible for interventional oncology procedures.

- Liver cancer is the third leading cause of cancer death worldwide, with over 800,000 new cases annually potentially treatable with embolization.

- Cardiovascular diseases remain the leading cause of death globally, accounting for approximately 18 million deaths annually.

Global Cancer Observatory (GLOBOCAN)

- Over 900,000 new liver cancer cases are diagnosed annually worldwide, with TACE being the most common treatment for unresectable disease.

- Approximately 600,000 uterine fibroid cases undergo treatment annually in major markets, with uterine fibroid embolization representing a growing treatment option.

American Cancer Society

- An estimated 40,000 patients undergo transarterial embolization procedures annually in the United States for liver cancer.

- Over 200,000 interventional oncology procedures are performed annually across all tumor types.

American Heart Association / American Stroke Association

- Approximately 30,000 cerebral aneurysms rupture each year in the United States, with many more unruptured aneurysms treated prophylactically.

- Endovascular coiling accounts for over 50% of cerebral aneurysm treatments in major neurointerventional centers.

Society of Interventional Radiology

- Over 500,000 uterine fibroid embolization procedures have been performed globally since the technique was introduced.

- Approximately 15,000 interventional radiologists practice worldwide, with growing demand for embolization procedures.

Global Transcatheter Embolization And Occlusion Devices Market: Market Dynamic

Driving Factors in the Global Transcatheter Embolization And Occlusion Devices Market

Rising Cancer Incidence and Interventional Oncology Adoption

The increasing global burden of cancer, particularly hepatocellular carcinoma and other hypervascular tumors treatable with embolization, represents the primary market driver. Transarterial chemoembolization and radioembolization have become standard treatments for intermediate-stage liver cancer, offering survival benefits with minimally invasive approaches. Additionally, expanding applications in metastatic disease, neuroendocrine tumors, and renal cell carcinoma further drive procedure volumes. As interventional oncology continues to demonstrate clinical and cost-effectiveness, demand for precision embolization devices continues to rise steadily.

Expanding Insurance Coverage and Favorable Reimbursement

Government initiatives and insurance policies supporting minimally invasive procedures significantly boost market growth. Countries including the U.S., Germany, Japan, and France provide comprehensive coverage for interventional oncology, neurointerventional, and peripheral embolization procedures. Medicare coverage determinations for TACE and cerebral aneurysm coiling, along with private insurer adoption of similar policies, directly increase procedure volumes. These financial support mechanisms reduce out-of-pocket burden for patients, making embolization procedures accessible to broader populations and subsequently increasing demand for embolization devices.

Restraints in the Global Transcatheter Embolization And Occlusion Devices Market

High Procedure Costs and Limited Access

Despite expanding insurance coverage, the high cost of embolization procedures remains a significant barrier, particularly in developing regions and countries without comprehensive interventional coverage. A single TACE procedure in the U.S. typically costs $15,000-$25,000, with multiple procedures often required for optimal tumor control. This financial burden limits patient volumes and consequently restricts market growth. Furthermore, embolization devices are premium-priced single-use products, adding to overall procedure costs and potentially discouraging adoption in price-sensitive healthcare markets.

Stringent Regulatory Approvals and Quality Standards

Transcatheter embolization devices are classified as Class II or Class III medical devices in most regulated markets, requiring rigorous pre-market clearance through FDA PMA or 510(k), CE Marking under MDR, or equivalent regional approvals. These regulatory pathways demand extensive clinical validation, biocompatibility testing, and manufacturing quality systems, creating significant time and cost barriers for new market entrants. Additionally, post-market surveillance requirements and quality management system certifications impose ongoing compliance burdens on manufacturers, potentially limiting innovation and market competition.

Opportunities in the Global Transcatheter Embolization And Occlusion Devices Market

Expansion into Emerging Interventional Markets

Emerging markets in Asia-Pacific, Latin America, and the Middle East represent significant growth opportunities due to rising healthcare expenditure, growing medical tourism for interventional procedures, and increasing awareness of minimally invasive treatment options. Countries including China, India, Brazil, and the UAE are developing specialized interventional centers catering to both domestic patients and international medical travelers seeking more affordable endovascular treatments. Localized distribution partnerships, region-specific regulatory strategies, and competitive pricing models can improve accessibility in these high-growth potential markets.

Technological Innovations Improving Outcomes

Continuous advancement in device design creates opportunities for differentiation and premium pricing. Detachable coil systems with enhanced three-dimensional configurations improve aneurysm packing density and long-term occlusion durability. Radiopaque liquid embolics enable real-time visualization during injection, reducing non-target embolization risk. Bioresorbable polymer technologies offer temporary occlusion with eventual vessel recanalization for specific applications. Manufacturers investing in these advanced features can capture market share among interventionalists prioritizing clinical outcomes and procedural efficiency.

Trends in the Global Transcatheter Embolization And Occlusion Devices Market

Single-Use Sterile Device Dominance

The predominance of single-use, sterile, disposable embolization devices represents an established trend driven by infection control protocols, patient safety concerns, and convenience. Single-use configuration eliminates cross-contamination risk associated with reprocessing and ensures consistent device performance for each procedure. This trend aligns with broader healthcare emphasis on preventing healthcare-associated infections and has become standard practice in interventional suites worldwide.

Integration with Advanced Imaging Systems

Modern embolization devices are increasingly designed for seamless integration with cone-beam CT, fluoroscopy, and fusion imaging technologies. Device visualization enhancements, including radiopaque markers and intrinsically radiopaque materials, facilitate precise deployment under image guidance. This trend supports the growing preference for image-guided minimally invasive procedures and enhances procedural confidence among interventionalists.

Global Transcatheter Embolization And Occlusion Devices Market: Research Scope and Analysis

By Product Type Analysis

Coils are projected to dominate the global transcatheter embolization and occlusion devices market due to their widespread use in neurovascular, peripheral vascular, and gastrointestinal applications and their established clinical history. These devices consist of platinum or nitinol-based filaments that are deployed through microcatheters to induce thrombosis and occlude target vessels. Because the delivery technique is well-established, coil embolization allows precise placement, controlled detachment (in detachable versions), and reliable occlusion compared with some non-coil alternatives. In most interventional suites, physicians prefer coils for cerebral aneurysm treatment, trauma embolization, and arterial bleeding control due to their predictable behavior and retrievability before detachment. Their longer commercial availability and extensive clinical literature also contribute to higher adoption, making them the default choice for many interventionalists.

Additionally, detachable coils offer enhanced control during deployment, allowing repositioning and optimization of coil configuration before final release, which is critical in neurovascular applications. Pushable coils provide cost-effective options for peripheral applications where precision requirements are less stringent. Since interventional oncology and neurovascular procedures have been increasing globally due to aging populations and improved cancer detection, demand for reliable and precisely controllable embolization devices has grown significantly. Non-coil devices including flow diverters, embolization particles, and liquid embolics are primarily used in specific applications where coils may be less effective, such as in wide-necked aneurysms or hypervascular tumors requiring distal penetration. As a result, coils continue to hold the largest market share within the product type segment and are expected to remain dominant due to their versatility, clinical familiarity, and procedural reliability.

By Material Composition Analysis

Platinum-based devices are anticipated to dominate the material composition segment of the transcatheter embolization and occlusion devices market due to their optimal balance of radiopacity, biocompatibility, and mechanical properties. In endovascular embolization procedures, device visibility under fluoroscopy is critical for precise deployment and confirmation of proper positioning. Platinum provides excellent radiopacity, allowing interventionalists to visualize devices clearly during placement without requiring excessive radiation or contrast. This property is particularly important in complex neurovascular and peripheral interventions where precise device positioning determines clinical outcomes.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Platinum-based coils also offer favorable mechanical characteristics, including flexibility for navigation through tortuous vasculature and sufficient stiffness to maintain deployed configuration without vessel injury. The material's proven biocompatibility and corrosion resistance ensure long-term stability within the vascular system, with minimal inflammatory response or thrombogenicity. Compared with nitinol-based devices, which offer shape-memory properties but lower radiopacity often requiring additional markers, platinum provides inherent visibility simplifying procedure workflow. While polymer and hydrogel-based agents offer advantages in specific applications requiring vessel filling or bioactive effects, platinum-based devices maintain dominance due to their combination of visibility, deliverability, and established safety profile across multiple clinical indications.

By Application Analysis

Oncology is projected to dominate the application segment of the transcatheter embolization and occlusion devices market because interventional oncology represents one of the fastest-growing areas of interventional radiology and generates high procedure volumes worldwide. During transarterial chemoembolization (TACE) and radioembolization procedures, embolization devices including particles, drug-eluting beads, and sometimes coils are used to occlude tumor-feeding arteries, delivering targeted therapy while inducing ischemic tumor necrosis. Since primary liver cancer and liver metastases affect hundreds of thousands of patients annually, and many are not candidates for surgical resection, embolization procedures represent a critical treatment option.

The increasing prevalence of hepatocellular carcinoma, driven by hepatitis and fatty liver disease, has created sustained demand for embolization procedures. Expanding applications in neuroendocrine tumor metastases, renal cell carcinoma, and sarcoma further contribute to procedure volumes. While peripheral vascular disease, neurology, and urology applications are significant, oncology procedures generally involve higher device utilization per case and often require repeat treatments, generating recurring demand. Clinical guidelines increasingly recommend embolization for intermediate-stage liver cancer, and ongoing research explores combination therapies with immunotherapy and targeted agents, suggesting continued oncology dominance. As a result, oncology remains the dominant application segment in the global transcatheter embolization and occlusion devices market.

By End-User Analysis

Hospitals and clinics are projected to dominate the end-user segment of the transcatheter embolization and occlusion devices market because they perform the overwhelming majority of interventional procedures worldwide. These facilities include tertiary care centers with dedicated interventional radiology departments, cancer centers with interventional oncology programs, and teaching hospitals with neurointerventional services. Since embolization procedures require sophisticated imaging equipment (angiography suites, cone-beam CT), specialized microcatheters and guidewires, and trained interventional teams, they are primarily performed in hospital settings with appropriate infrastructure.

Compared with ambulatory surgical centers, hospitals offer greater capability for managing complex cases, potential complications, and multi-disciplinary care coordination required for oncology and neurovascular patients. Many hospitals have established comprehensive interventional programs with dedicated procedure rooms, recovery areas, and clinical pathways for embolization patients. Additionally, the growth of hospital-based interventional radiology departments in regions such as North America, Europe, and Asia-Pacific has significantly expanded access to embolization procedures. Ambulatory surgical centers contribute to market share primarily for simpler procedures such as uterine fibroid embolization in selected patients, but hospital dominance persists due to case complexity and infrastructure requirements. As a result, hospitals and clinics remain the dominant end-user segment in the global transcatheter embolization and occlusion devices market.

The Global Transcatheter Embolization And Occlusion Devices Market Report is segmented on the basis of the following:

By Product Type

- Coils

- Pushable Coils

- Detachable Coils

- Non-Coil Devices

- Flow Diverting Devices

- Embolization Particles

- Liquid Embolics

- Other Non-Coil Devices

- Accessories

By Material Composition

- Platinum-based Devices

- Nitinol-based Devices

- Polymer / Hydrogel-based Agents

- Bio-resorbable Polymers

By Application

- Oncology

- Peripheral Vascular Disease

- Neurology

- Urology

- Others

By End User

- Hospitals & Clinics

- Ambulatory Surgical Centers

- Others

Impact of Artificial Intelligence in the Global Transcatheter Embolization And Occlusion Devices Market

- AI for Treatment Planning: AI algorithms analyze CT, MRI, and angiography images to identify target vessels, calculate optimal embolization volumes, and predict procedural outcomes, assisting interventionalists in selecting appropriate devices and approaches for individual patients.

- Predictive Modeling of Tumor Response: Machine learning models integrate patient characteristics, tumor biology, and treatment parameters to predict likely response to embolization, enabling personalized procedure planning and patient counseling.

- AI-Assisted Device Guidance: Emerging AI systems provide real-time guidance during catheter navigation and device deployment, enhancing target vessel selection and suggesting optimal microcatheter positions for precise embolization.

- Quality Control in Device Manufacturing: Computer vision systems employing AI inspect manufactured devices for dimensional accuracy, coating uniformity, and structural integrity, ensuring consistent product quality meeting stringent regulatory requirements.

- Procedure Outcome Analysis: AI platforms aggregate and analyze outcomes across large patient populations, identifying correlations between device selection, procedural techniques, and clinical success rates to inform best practice guidelines.

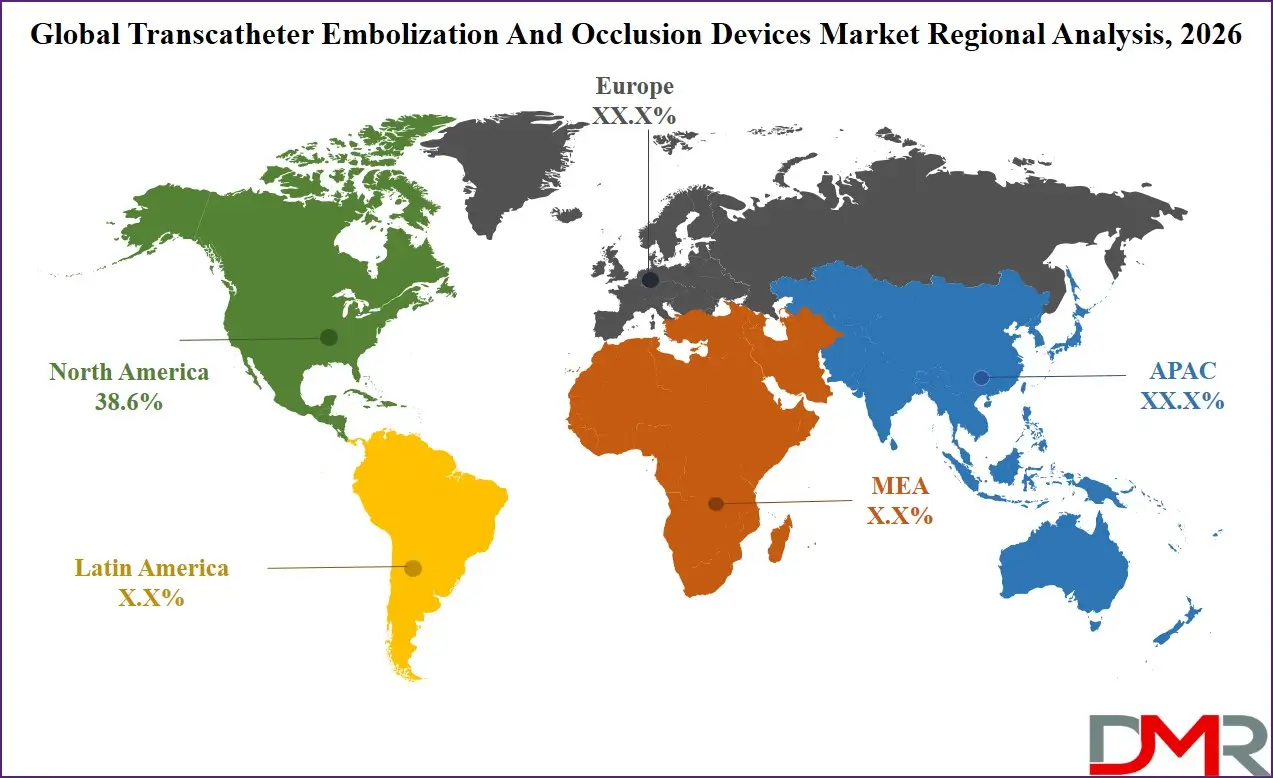

Global Transcatheter Embolization And Occlusion Devices Market: Regional Analysis

Region with the Largest Revenue Share

North America is projected to dominate the regional segment with the highest market share as it is anticipated to hold approximately 38.6% of the total market revenue by the end of 2026, due to advanced healthcare infrastructure, high interventional procedure volumes, and widespread insurance coverage for minimally invasive treatments. The region is home to leading interventional radiology departments and medical device innovators, driving clinical advancements in embolization procedures.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Strong patient awareness regarding minimally invasive treatment options and acceptance of interventional approaches as mainstream healthcare further strengthens demand. The United States, in particular, accounts for the largest share within North America due to its large private-pay interventional market, comprehensive Medicare coverage, and concentration of world-renowned interventional centers. Although Asia Pacific is the fastest-growing region, North America continues to hold the largest revenue share due to premium procedure pricing and early adoption of advanced embolization technologies.

Region with the Highest CAGR

Asia-Pacific holds the highest CAGR of 10.7% and is poised to achieve rapid market share growth due to its massive population base, rising cancer and vascular disease burden, expanding medical tourism for interventional procedures, and government initiatives supporting advanced healthcare infrastructure. Countries including China, Japan, India, and South Korea are investing heavily in interventional radiology capacity and treatment accessibility. Japan's comprehensive national insurance coverage for interventional oncology and neurovascular procedures, and China's expanding network of certified interventional centers, are creating fertile ground for market expansion. The region's large patient volumes, combined with growing numbers of interventional suites adopting international quality standards, position APAC as the fastest-growing market for transcatheter embolization and occlusion device systems.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Global Transcatheter Embolization And Occlusion Devices Market: Competitive Landscape

The Global Transcatheter Embolization And Occlusion Devices Market is moderately consolidated, featuring a mix of specialized interventional device manufacturers, diversified healthcare product suppliers, and innovative medical technology companies. Leading players like Boston Scientific Corporation, Medtronic plc, and Johnson & Johnson (Ethicon) leverage their established interventional portfolios and global distribution networks to maintain market presence. Specialized manufacturers such as Penumbra, Inc., Stryker Corporation (through neurovascular acquisitions), and Terumo Corporation drive market dynamics with clinically focused innovation and strong relationships with interventional specialists. Medical device conglomerates maintain comprehensive embolization product lines spanning coils, liquid embolics, and flow diverters, while regional manufacturers serve local markets with cost-competitive alternatives. The market also features partnerships between device manufacturers and interventional societies, ensuring clinical feedback integration into product development and physician training programs.

Some of the prominent players in the Global Transcatheter Embolization And Occlusion Devices Market are:

- Boston Scientific Corporation

- Medtronic plc

- Terumo Corporation

- Stryker Corporation

- Abbott Laboratories

- Johnson & Johnson (Cerenovus)

- Cook Medical

- Penumbra Inc.

- Merit Medical Systems Inc.

- Sirtex Medical Limited

- BTG International Ltd.

- Cardinal Health Inc.

- Edwards Lifesciences Corporation

- MicroVention Inc.

- Acandis GmbH & Co. KG

- BALT Extrusion

- Kaneka Corporation

- MicroPort Scientific Corporation

- Shape Memory Medical Inc.

- Meril Life Sciences Pvt. Ltd.

- Other Key Players

Recent Developments in the Global Transcatheter Embolization And Occlusion Devices Market

- January 2026: Boston Scientific Corporation announced that its Embold detachable coil system received CE Mark approval, enabling commercialization across Europe, the Middle East, and Africa for peripheral vascular embolization procedures.

- October 2025: Penumbra, Inc. launched the SwiftSET neuro embolization coil, engineered to optimize vessel wall apposition and support controlled deployment during complex neurovascular embolization procedures.

- September 2025: Medtronic plc presented new clinical evidence supporting the long-term safety and efficacy of the Pipeline Flex embolization device, reinforcing its role in the treatment of large and wide-neck intracranial aneurysms through flow-diversion therapy.

- May 2025: Cook Medical released a new embolization coil platform designed to enhance deployment control and improve vessel packing efficiency during vascular embolization procedures, supporting more precise occlusion of targeted blood vessels in interventional radiology treatments.

- July 2024: Terumo Corporation expanded global distribution of its AZUR detachable hydrocoil embolization system, designed to provide controlled deployment and improved occlusion performance during peripheral vascular embolization procedures.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 6.4 Bn |

| Forecast Value (2035) |

USD 13.4 Bn |

| CAGR (2026–2035) |

8.5% |

| The US Market Size (2026) |

USD 2.1 Bn |

| Historical Data |

2020 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Product Type (Coils, Non-Coil Devices, Accessories), By Material Composition (Platinum-based Devices, Nitinol-based Devices, Polymer / Hydrogel-based Agents, Bio-resorbable Polymers), By Application (Oncology, Peripheral Vascular Disease, Neurology, Urology, Others), By End User (Hospitals & Clinics, Ambulatory Surgical Centers, Others) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia- Pacific– China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

Boston Scientific Corporation, Medtronic plc, Terumo Corporation, Stryker Corporation, Abbott Laboratories, Johnson & Johnson (Cerenovus), Cook Medical, Penumbra Inc., Merit Medical Systems Inc., Sirtex Medical Limited, BTG International Ltd., Cardinal Health Inc., Edwards Lifesciences Corporation, MicroVention Inc., Acandis GmbH & Co. KG, BALT Extrusion, Kaneka Corporation, MicroPort Scientific Corporation, Shape Memory Medical Inc., Meril Life Sciences Pvt. Ltd., and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Transcatheter Embolization And Occlusion Devices Market?

▾ The Global Transcatheter Embolization And Occlusion Devices Market size is estimated to have a value of USD 6.4 billion in 2026 and is expected to reach USD 13.4 billion by the end of 2035.

What is the growth rate in the Global Transcatheter Embolization And Occlusion Devices Market in 2026?

▾ The market is growing at a CAGR of 8.5% over the forecasted period of 2026.

What is the size of the US Transcatheter Embolization And Occlusion Devices Market?

▾ The US Transcatheter Embolization And Occlusion Devices Market is projected to be valued at USD 2.1 billion in 2026. It is expected to witness subsequent growth in the upcoming period as it holds USD 4.1 billion in 2035 at a CAGR of 8.0%.

Which region accounted for the largest Global Transcatheter Embolization And Occlusion Devices Market?

▾ North America is expected to have the largest market share in the Global Transcatheter Embolization And Occlusion Devices Market with a share of about 38.6% in 2026.

Who are the key players in the Global Transcatheter Embolization And Occlusion Devices Market?

▾ Some of the major key players in the Global Transcatheter Embolization And Occlusion Devices Market are Medtronic plc, Terumo Corporation, Abbott Laboratories, Cook Medical, Penumbra Inc., and many others.